Forgot to send these out Friday. Updated fertilizer/corn ratio charts.

Urea - still not great, but vastly improved

UAN - huge/high value for late spring...waiting for summer fill reset, hoping for big price drop

DAP - near record high's

Potash - not horrible/not great

Weather market is a time for speculations and position-talking. Although we expect to see the consequences of extreme weather, we tend to agree that the timing is off. Had this heat wave struck 2-3 weeks earlier, the damage to early crops would have been far worse [1/3]

🌽U.S. corn conditions were unchanged this week at 68% good/excellent despite declines in Iowa and Illinois. Aside from Nebraska, most top states remain above their five-year average.

#CropWatch26 producers report that corn has fared the cool, wet weather better than soybeans.

🌾The world's wheat cushion for 2026/27 is still largely uncertain.

Current analyst scenarios span a 16.5-million-ton range in ending stocks for the upcoming marketing year, a reminder that global food systems remain highly sensitive to production and demand trends.

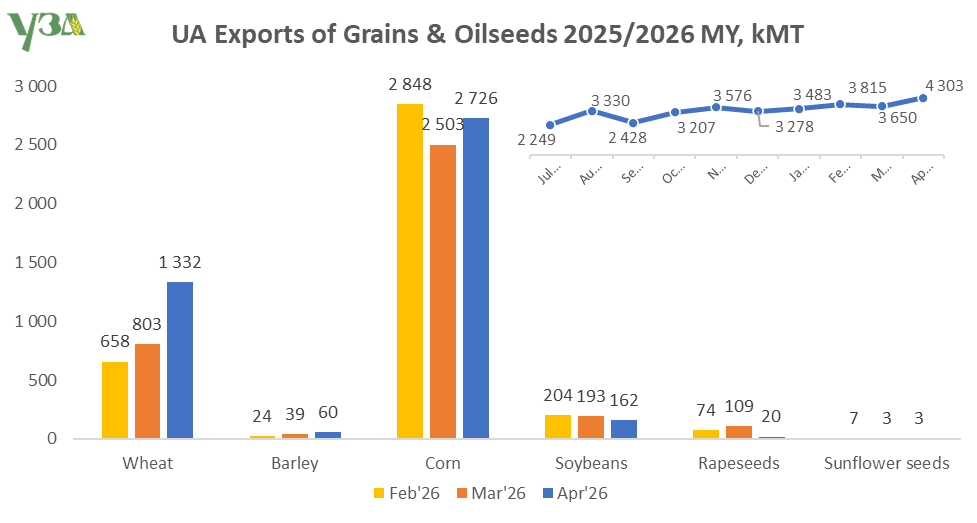

The structure and dynamics of UA grains and oilseeds exports for the last 3 months of 2025/2026 MY as well as the dynamics of monthly export volume since July 2025.

*Fert Tour - Highlights*

Total Brz fertilizer import volume continues to decline. The Lineup YTD is 5% lower YoY. N volume dropped by 14% and P2O5 dropped by 10%. Stocks in Brz are much lower than normal.

LINK: https://t.co/20qmsKJsvt

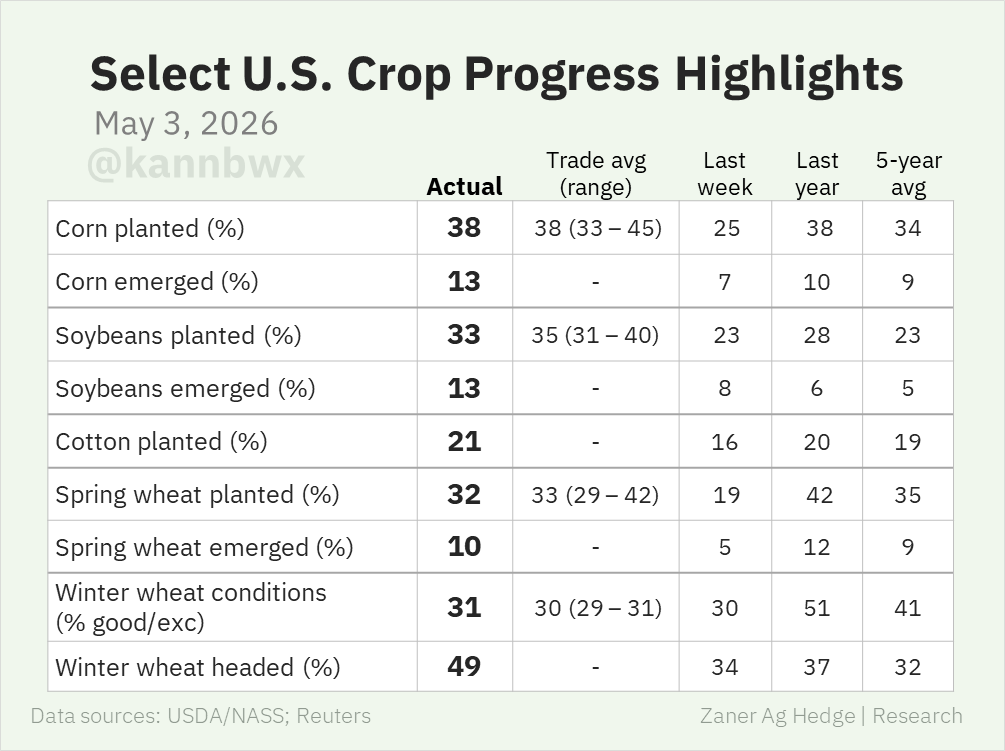

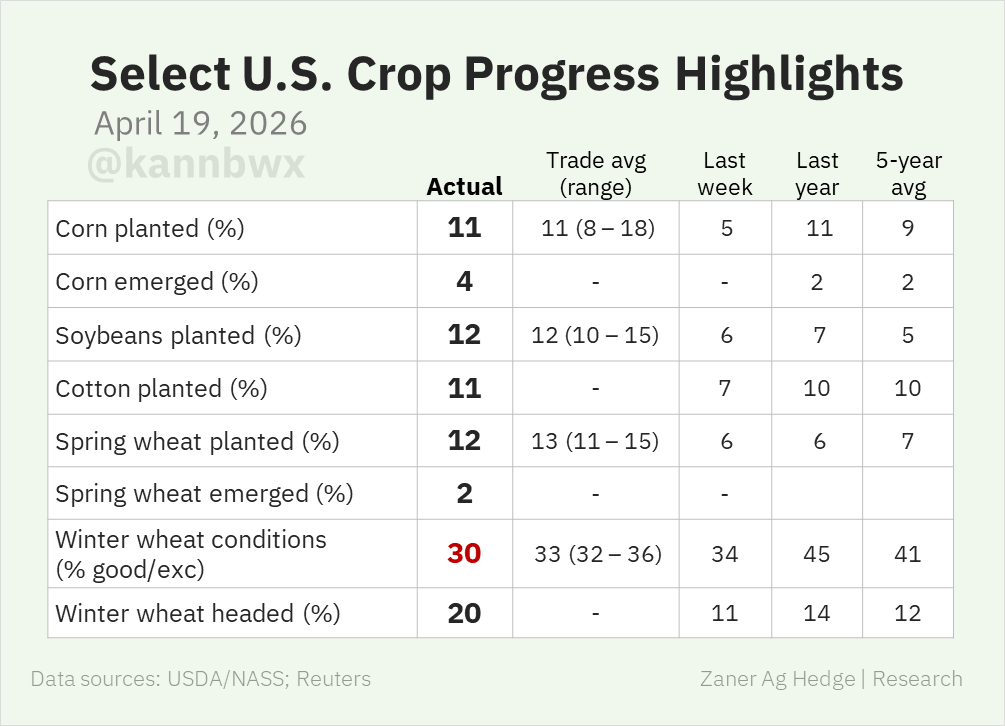

🇺🇸U.S. corn is 38% planted, equal to last year and ahead of average. At 33% planted, soybeans remain on their record fast pace, but analysts expected more progress last week. Winter wheat conditions improved 1 point.

🚜 Farms in the south are struggling:

78% of Southern farmers say they can’t afford all required fertilizer this year, the highest of any region.

The South is exposed for two reasons: crop mix and pre-booking behavior.

Just 19% of Southern producers pre-booked fertilizer ahead of the season, vs. 30% in the Northeast, 31% in the West, and 67% in the Midwest.

Cotton, rice, and peanut growers, largely concentrated in the South, barely locked anything in before fertilizer prices skyrocketed.

Only 13% of cotton growers and 9% of peanut growers pre-booked.

Those are also the most fertilizer-intensive crops on the board.

Rice runs $1,308/acre to produce, peanuts $1,166, and cotton $943 vs. $658 for soybeans and $396 for wheat.

U.S. farm sector losses have exceeded $50 billion across the past three crop years.

Nearly all (94%) farmers say their financial situation has worsened or stayed the same vs. last year.

Farms are getting squeezed.

I was talking with some traders this week. Depending on rainfall for the next 15 days (GFS and EC agreed on Dryer and warmer), they will lower by 5-6 Mi t in GO, MGDS and PR. Export program at 37 Mi t will be the number.

Replacement remains very expensive, around 60-80 c/b above Fob levels. Premiums Fob Santos up 15 c in the last 2 weeks and Arg down 5-8 for nearby.

🌱 Aceite de soja: energía firme, biocombustibles y fondos sostienen al mercado

El mercado de aceite de soja continúa mostrando fortaleza, incluso con algunas bajas técnicas en los futuros.

El contrato mayo todavía mantiene una suba acumulada importante.

¿Qué está sosteniendo al mercado?

1️⃣ Los fondos mantienen una posición compradora récord, cercana a 150.000 contratos.

Esto significa que el mercado sigue apostando por precios firmes, aunque también aumenta el riesgo de una toma de ganancias.

2️⃣ La energía sigue siendo un factor clave.

El petróleo se mantiene fuerte y eso impulsa directamente al aceite de soja por su relación con los biocombustibles.

3️⃣ Indonesia refuerza su estrategia energética.

Indonesia anunció que dejará de importar diésel desde el 1 de julio para avanzar con su programa obligatorio B50.

Esto implica mayor uso de aceites vegetales para biodiésel y más presión sobre la oferta global.

4️⃣ En Asia, el aceite de palma también sube.

Los futuros en Malasia avanzaron, mientras China mostró mejoras en oleína y aceite de soja.

Todo esto genera mayor sostén para el complejo de aceites vegetales.

El mercado no solo mira oferta y demanda.

Hoy también observa energía, biocombustibles y decisiones políticas que pueden cambiar el equilibrio global.

Y ahí, el aceite de soja sigue siendo protagonista.

Por Esteban Moscariello

#AceiteDeSoja #Soja #Biocombustibles #Biodiesel #Indonesia #AceiteDePalma #MercadoDeGranos #Agronegocios #CBOT

🌾 El mercado agrícola sigue atento a Medio Oriente, pero el foco empieza a cambiar.

Mientras la tensión geopolítica mantiene bajo presión a la energía, los granos comienzan a mirar nuevamente sus propios fundamentos.

Hoy, tres temas dominan la atención del mercado:

1️⃣ Trigo de invierno en EE.UU.

El USDA informó que solo el 30% del trigo de invierno está en condiciones buenas o excelentes.

Es una caída importante frente al 33% esperado por el mercado y sigue dando sostén al trigo HRW, que permanece en los niveles más altos del complejo.

2️⃣ Costos de producción y siembra

La siembra avanza con trigo de primavera en 12%, soja en 12% y maíz en 11% en EE.UU.

Sin embargo, el verdadero debate está en los fertilizantes.

El aumento de los costos de insumos podría llevar a una reducción de área en maíz y favorecer una mayor superficie de soja.

3️⃣ Harina de soja y fondos

El contrato mayo se mantiene cerca de USD 331,80 por tonelada, pero el mercado observa con atención a los fondos.

Actualmente mantienen una posición neta compradora de 131.556 contratos, uno de los niveles más altos de los últimos años.

Esto genera una pregunta importante:

¿seguirán sosteniendo esa posición o comenzará una toma de ganancias que presione los precios?

Además, en Argentina, el USDA elevó la producción de maíz a 61 millones de toneladas, una cifra récord que suma presión sobre el mercado global.

Menos geopolítica, más fundamentos.

Ese parece ser el nuevo eje del mercado.

Por Esteban Moscariello

#Soja #Maíz #Trigo #HarinaDeSoja #USDA #MercadoDeGranos #Agronegocios #CBOT #Argentina #Chicago

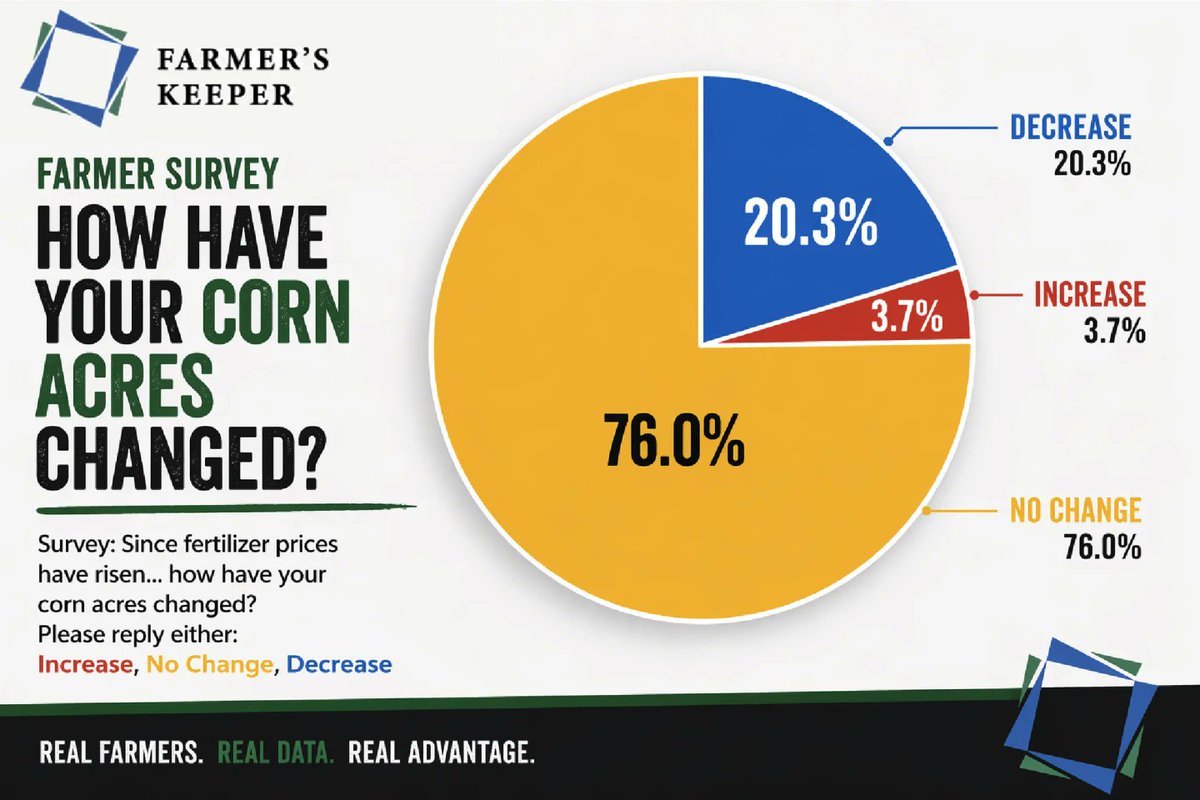

A private survey conducted by grain merchandiser Farmer’s Keeper shows a sizable cut in corn acres since USDA’s March Prospective Planting report.

https://t.co/8h2R4XzSdg

����🇷Brazil: #corn exports are stuck in a seasonal slump, with only 48KMT shipped last week. Current lineup indicates 360KMT could be exported in April. #Iran is the largest market for #Brazilian corn, but there are currently no vessels in the #lineup scheduled for that destination

https://t.co/qB0hh6dfMf

Strong BRL, late planting in ~1/3 of safrinha area, bigger domestic demand and warmer and dryer weather ahead (MW models). Exporters are very far from getting excited about export program.

Weekly Tour - Grains

Apr 20th: https://t.co/8WhQF4Lopz

🇺🇸U.S. export inspections were as expected last week with corn volumes staying above the threshold needed to achieve the full-year export forecast. About 17% of the corn was to South Korea, 15% was to Mexico. About 60% of the week's soybean inspections were bound for China.

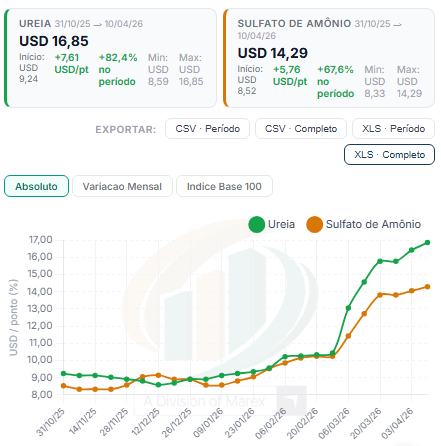

The N cost for Brz farmers jumped and grains prices dropped. The most imminent decision is wheat and summer corn. The N cost (per point) rose by 70% for urea in 50 days and 43% for Ammonium Sulphate.

🇺🇸U.S. winter wheat conditions fell below all trade estimates to 30% good/excellent. That's approaching 2022 & 2023, among the lowest scoring years in recent memory.

Despite some wet weather, U.S. corn & bean planting pace met expectations and remain ahead of average levels.

📈Money managers established record bullish bets in CBOT soybean oil futures & options for a second consecutive week, their net long position reaching nearly 151,000 contracts.

Funds' pre-2026 max net long in bean oil was 127,000 contracts.

🌽📉 Guerra + costos altos = cambio de reglas en el mercado de maíz

1️⃣ El mercado ya anticipa una caída en el área de maíz en EE.UU., con la soja ganando terreno. La decisión responde a un combo claro: costos más altos y mejor relación insumo/producto para la oleaginosa.

2️⃣ El conflicto en Oriente Medio disparó los precios de los fertilizantes, especialmente los nitrogenados, afectando directamente la rentabilidad del maíz.

3️⃣ Menos área sembrada en EE.UU. podría traducirse en una reacción alcista en Chicago. Algunos analistas ya proyectan precios por encima de US$5/bushel para equilibrar el mercado.

4️⃣ China también entra en juego: restringe exportaciones de fertilizantes y podría ajustar su propia siembra, favoreciendo soja sobre maíz.

5️⃣ En Brasil, el foco está en el clima para la safrinha 🌧️ Abril y mayo serán meses clave para definir el potencial productivo.

6️⃣ Aunque hoy los stocks son cómodos, el mercado ya mira hacia adelante: superficie, clima y demanda serán determinantes.

7️⃣ Con este escenario, el maíz entra en una nueva fase donde la geopolítica y los costos pesan tanto como la oferta y la demanda.

+ Por Esteban Moscariello

#Maíz #Agro #Commodities #Chicago #Soja

![BarvaInvest's tweet photo. Weather market is a time for speculations and position-talking. Although we expect to see the consequences of extreme weather, we tend to agree that the timing is off. Had this heat wave struck 2-3 weeks earlier, the damage to early crops would have been far worse [1/3] https://t.co/286OqJnNM6](https://pbs.twimg.com/media/HLl8z4uWEAAzjQf.jpg)