Official transcripts take days to come out after earnings calls.

With our latest update, you don’t have to wait for transcripts anymore.

We deliver concall analysis the same day - well before official transcripts are released.

What you get:

• AI-generated transcripts (PDF included)

• Summaries & key insights

• Full concall recording - listen on the platform

• Track companies via your watchlist

• Filter by sector or market cap

Everything you need for concall analysis, in one place.

Try out now, link in thread 👇

#BHEL received a ₹21,000+ crore EPC order from for the 3×800 MW Meja Stage-II supercritical thermal power project, with execution planned over 70 months.

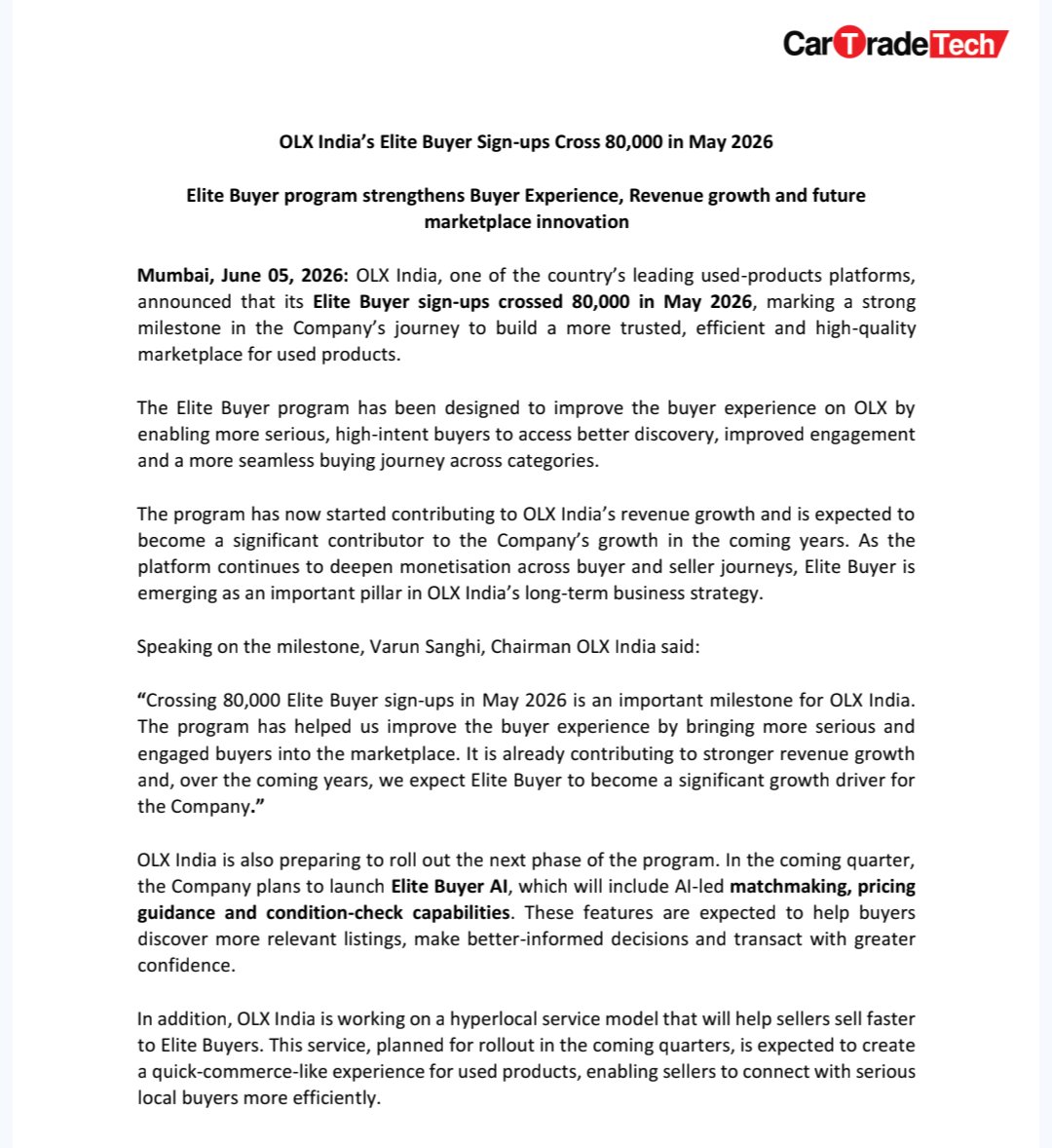

CarTrade Tech's OLX India Elite Buyer sign-ups crossed 80,000 in May 2026, reflecting strong traction and supporting future growth through AI-driven matchmaking and hyperlocal seller services.

#STALLION

Stallion India Fluorochemicals Ltd

At an inflection point with capex story.

China and EU - out of the game.

FY27: 100 PAT ( YoY : 120% growth)

@concall_in snippet 👇

JD Cables Q4 FY26 concall insights - Capacity Expansion Meets EPC Execution

📈 Growth remained strong

• FY26 revenue grew 46% YoY while PAT increased 44% YoY

• H2 growth accelerated with revenue and PAT rising ~70% YoY

🏭 Next phase starts now

• New conductor facility starts this month and cable division follows shortly

• Capacity set to double initially with room for further expansion

🔌 Moving up the value chain

• Expanding into HT cables, HTLS conductors and other higher-value products

• New products expected to carry better margins than existing portfolio

🏗️ EPC is becoming meaningful

• EPC contributed ₹30 Cr revenue in FY26

• Management targets ₹200+ Cr EPC revenue in FY27

• Current EPC project execution is only around 10%

📦 Visibility remains healthy

• Order book stands at ₹515 Cr

• Company has bid for ₹1,000+ Cr worth of new projects

🎯 Growth guidance stays ambitious

• Management guides for 50-60% revenue growth in FY27

• Order book target of ₹700-800 Cr by FY27 end

⚠️ Execution will be key

• Margins moderated to ~12-13% in H2

• Working capital needs and debt are likely to increase with EPC scale-up

#JDCables #Q4FY26 #Concall

Angel One monthly business update for May 2026 - client base grew 19.5% YoY to 38.17 million, avg client funding book up 57.5% YoY to ₹63.09 Bn, and F&O market share expanded.

Atlanta Electricals secured an order worth approximately ₹285.15 crore from Punjab State Transmission Corporation Limited (PSTCL) for the supply of 23 units of 160 MVA, 220/66 kV Power Transformers with associated systems.

#ATLANTAELE#OrderWin

#IEX May 2026 Business Update

- Electricity traded volume reached 12,983 MU, up 18.6% YoY.

- DAM volume grew 24.9% to 4,417 MU, RTM up 15.9% to 5,529 MU, and Green Market up 13% to 1,034 MU.

Lumax Industries Q4FY26 Concall Highlights

• LED is only the light source; future innovation will come from technologies built on top of it

• Focus is shifting toward Adaptive Driving Beam (ADB), multi-pixel LED projection systems, and laser-based lighting solutions

• The company is particularly strong in front-lighting technologies, where adoption is increasing.

• These innovations will increase content per vehicle, enhancing both safety and user experience, driving future growth beyond traditional LED lighting

Source - @concall_in

Disclaimer: No recommendation. For educational purposes only.

Link to Tenneco Clean Air India Q4 FY26 concall & insights:

https://t.co/0DgbwzBNMg

Disclaimer: For educational purposes only. Not a buy or sell recommendation.

Tenneco Clean Air India Q4 FY26 concall insights - Margin Expansion & Export Growth

📊 Financial Performance

• FY26 value-added revenue up 12.3% YoY to ₹4,918 Cr

• EBITDA grew 13.5% to ₹926 Cr with record 18.8% margin

• Q4 revenue increased 17.5% YoY and EBITDA rose 17.6%

• PAT grew 9.3% YoY to ₹604 Cr with zero debt balance sheet

• ROCE surged to 94% from 57% last year

🚀 Growth Drivers & Order Wins

• Lifetime order book at ₹12,400 Cr gives visibility till FY28

• Won major Clean Air and bearing systems programs with global OEMs

• DaVinci DCX suspension seeing strong traction from 3-4 OEMs

🌍 Export Opportunity

• Exports currently 5-6% of sales vs 14-20% order book share

• Export ramp-up expected from FY28 driven by China+1 shift

• High localization of 89-90% boosts global competitiveness

🏭 Capacity Expansion & Outlook

• Investing ₹140 Cr in two greenfield plants

• New facilities to be commissioned within 6-12 months

• Management expects sustained double-digit growth trajectory

• CAFE 3 and BS VII norms can unlock ₹1,300-1,400 Cr opportunity

#TENNIND #Q4FY26 #Concall

Link to Exato Technologies Q4 FY26 concall recording, transcript & insights:

https://t.co/Se8vr0lsAM

Disc: Not a buy / sell recommendation. Only for educational puprose.

Exato Technologies Q4 FY26 concall insights - Strong Guidance & Expansion Plans

📈 Financial & Order Book Strength

• FY26 revenue grew 35% to ₹168 Cr with PAT up 67% to ₹16.1 Cr

• PAT margin expanded to 9.5% while ARR surged to ₹118 Cr

• ₹600 Cr order book provides strong visibility with ₹330 Cr pending execution

🚀 Strategic Initiatives & Outlook

• FY27 guidance strong with revenue and PAT expected to grow 50-60%

• International revenue targeted at 50-55% from ~30% within 2 years

• AI-as-a-Service, Agentic AI and Exato IQ emerging as key growth engines

• AI infrastructure business targeted to contribute 30-35% of revenue in 2-3 years

🌍 Global Expansion

• US, Australia and Singapore subsidiaries to drive larger enterprise deal wins

• Customer base targeted to expand from 150+ to 500-600 in next 3-4 years

• ₹500 Cr revenue ambition over next 2 years via organic and inorganic growth

💰 Margin Drivers

• Export margins at 30-35% versus 22-24% domestically

• Higher export mix and managed services expected to drive faster PAT growth

🧠 Leadership & IP Focus

• New CRO, Chief AI Officer and healthcare-focused board addition strengthen execution

• Proprietary IP contribution targeted at 15-20% of revenue within 3 years

#EXATO #Q4FY26 #Concall