@Str_kerX You described the complete arc from participant to contributor in one post. That shift is what makes decentralised ecosystems actually function over time.

@johnnyblast04@theoneboy001 The Privacy Paradox: Most shared infrastructure fails because institutions won't reveal their hand. ZK-tech solves this by allowing verification without exposure. You can prove you have the funds and met the KYC without leaking the trade details to the whole network.

@johnnyblast04@theoneboy001 The "Bank-Grade" Standard: The 2026 roadmap for ZKsync really emphasizes "Bank-Grade Encryption by Default." We're moving away from "experimental" tech and into integrated infrastructure that fits directly into existing ERP and CRM systems.

The $ZK "Infrastructure Gap": Why Privacy is Only Half the Battle

Most people still frame blockchain adoption as a technology problem. For institutions, it’s an infrastructure problem.

Banks do not lack interest in onchain settlement; they lack an environment where sensitive transaction flow stays private, compliance remains enforceable, and execution does not depend on a third-party operator.

This shift requires a move away from public-by-default ledgers toward systems that respect the existing legal and operational mandates of global finance.

That is the gap @zksync ’s Prividium is solving. As it exists today, $ZK acts as the native token of the ZKsync ecosystem, providing the economic coordination and governance necessary for a decentralized network.

By establishing a framework where institutions can manage their own nodes while sharing a common proof system, the network bridges the gap between legacy silos and open internet value.

This creates a scalable path for trillions in assets to move into a cryptographically secured environment without compromising institutional sovereignty.

The important detail is not privacy alone; it’s the structural network effect of verifiable connectivity. **ZKsync’s Prividium delivers all four simultaneously: privacy, compliance, verifiability, and decentralization.

Every additional participant does not simply add another user to the network; it exponentially increases the number of possible settlement relationships across the entire system.

This interoperability ensures that liquidity remains deep and accessible, even when the underlying transactions are shielded from the public eye.

If protocol fees and settlement infrastructure increasingly route through $ZK over time, the asset functions less like a speculative instrument and more like economic coordination infrastructure for the network itself.

The market often obsesses over throughput and TPS, but the real competition is over who becomes the settlement layer institutions actually trust for long-term operations.

By focusing on the intersection of privacy and proof, the ecosystem positions itself as the foundational layer for the future of global institutional finance.

@johnnyblast04 The three-body $ZK governance model keeps failure modes isolated. A compromise in technical upgrade review doesn’t cascade into economic parameters. That separation matters when institutions are committing to infrastructure over multi-year timeframes.

This is what I started fucking doing it for man.

This is my proudest moment so far.

This is why we’re building this shit.

Brick by fucking brick.

Just Like I said!

@johnnyblast04 What makes Prividium’s architecture distinct is that privacy isn’t bolted on as a feature — it’s structural. Execution stays offchain by design, which means compliance isn’t something you configure, it’s something you inherit from the system itself.

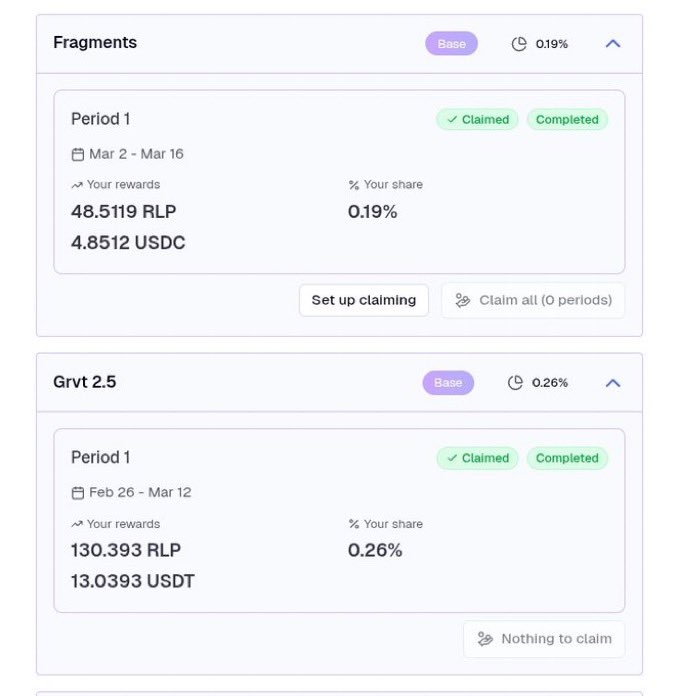

@johnnyblast04@theoneboy001@larcxim@RallyOnChain No vesting, no cliff, just liquid stablecoins. If that’s genuinely how it works then someone finally figured out how to make creator payments feel fair.

Watched my buddy @larcxim casually mention he got paid for posting last week. I laughed.

Then he showed me his @RallyOnChain earns.

Real stablecoins sitting right there.

No “points”

No vague promises

No waiting 6 months for an airdrop that gets cut in half anyway

Just… paid.