Here’s how I got $15,000+ worth of travel to Switzerland, Tokyo, and Paris for my 21st birthday for less than $2,000.

And no — I didn’t save up for it.

I used my credit card to buy a Cartier watch.

Most people hit their credit card signup bonus buying groceries, gas, etc. over 3 months.

I hit mine in one purchase.

Step 1 — One swipe. 120,000 points.

Put an $8,500 Cartier Santos on my Chase Ink Unlimited.

$6,000 spend threshold hit instantly.

120,000 Chase points loaded same day.

Step 2 — $15,000 in flights. 120,000 points. Done.

Pulled up https://t.co/i0WNVodSeA.

Found 2 business class flights — LAX to Paris and Paris to Tokyo.

$12,000+ if paid cash.

Transferred Chase points to Air France miles.

Booked both for 120,000 points + a couple hundred in fees.

Done.

Step 3 — The part nobody expects

Came home from 2 weeks across Switzerland, Tokyo and Paris.

Walked straight into a second hand watch dealer.

Sold the Cartier for $6,500.

Paid the card off in full.

Now I know what you’re thinking.

“Gio you lost $2,000.”

Did I though?

I wore an $8,500 Cartier for 3 weeks.

Flew business class across 3 countries.

$15,000+ in travel.

Total out of pocket — $2,000.

That’s not a loss.

That’s the most efficient vacation ever bought.

Credit cards aren’t dangerous.

Not knowing how to use them is.

Was this genius? Or did I just lose $2,000? Let me know what you guys think below 👇

Here’s how I got $15,000+ worth of travel to Switzerland, Tokyo, and Paris for my 21st birthday for less than $2,000.

And no — I didn’t save up for it.

I used my credit card to buy a Cartier watch.

Most people hit their credit card signup bonus buying groceries, gas, etc. over 3 months.

I hit mine in one purchase.

Step 1 — One swipe. 120,000 points.

Put an $8,500 Cartier Santos on my Chase Ink Unlimited.

$6,000 spend threshold hit instantly.

120,000 Chase points loaded same day.

Step 2 — $15,000 in flights. 120,000 points. Done.

Pulled up https://t.co/i0WNVodSeA.

Found 2 business class flights — LAX to Paris and Paris to Tokyo.

$12,000+ if paid cash.

Transferred Chase points to Air France miles.

Booked both for 120,000 points + a couple hundred in fees.

Done.

Step 3 — The part nobody expects

Came home from 2 weeks across Switzerland, Tokyo and Paris.

Walked straight into a second hand watch dealer.

Sold the Cartier for $6,500.

Paid the card off in full.

Now I know what you’re thinking.

“Gio you lost $2,000.”

Did I though?

I wore an $8,500 Cartier for 3 weeks.

Flew business class across 3 countries.

$15,000+ in travel.

Total out of pocket — $2,000.

That’s not a loss.

That’s the most efficient vacation ever bought.

Credit cards aren’t dangerous.

Not knowing how to use them is.

Was this genius? Or did I just lose $2,000? Let me know what you guys think below 👇

You probably think you need a 750+ credit score and a business already making money to get funding.

Unfortunately, that’s what the bank WANTS you to think.

The truth is, the bank is only checking 3 things when it comes to approving you for credit...

1. Personal credit cleaned up and optimized — score above 700, utilization under 10%, zero negatives

2. Business structured the right way — right industry, right address, right banking relationship built before applying

3. Applied at the right banks, in the right order, through a relationship manager — not a cold online application

I’ve helped a bakery owner, a real estate investor, and a medical company founder all get approved for $50K–$150k in business funding at 0% interest.

None of them had an established business.

None of them were already making money.

They just followed my 3 step framework.

.

The banks aren’t looking for a perfect business.

They’re looking for a fundable person.

I broke the entire 3 step framework down step by step in a free video.

Comment “FRAMEWORK” below and I’ll send you the video I personally made👇

You probably think you need a 750+ credit score and a business already making money to get funding.

Unfortunately, that’s what the bank WANTS you to think.

The truth is, the bank is only checking 3 things when it comes to approving you for credit...

1. Personal credit cleaned up and optimized — score above 700, utilization under 10%, zero negatives

2. Business structured the right way — right industry, right address, right banking relationship built before applying

3. Applied at the right banks, in the right order, through a relationship manager — not a cold online application

I’ve helped a bakery owner, a real estate investor, and a medical company founder all get approved for $50K–$150k in business funding at 0% interest.

None of them had an established business.

None of them were already making money.

They just followed my 3 step framework.

.

The banks aren’t looking for a perfect business.

They’re looking for a fundable person.

I broke the entire 3 step framework down step by step in a free video.

Comment “FRAMEWORK” below and I’ll send you the video I personally made👇

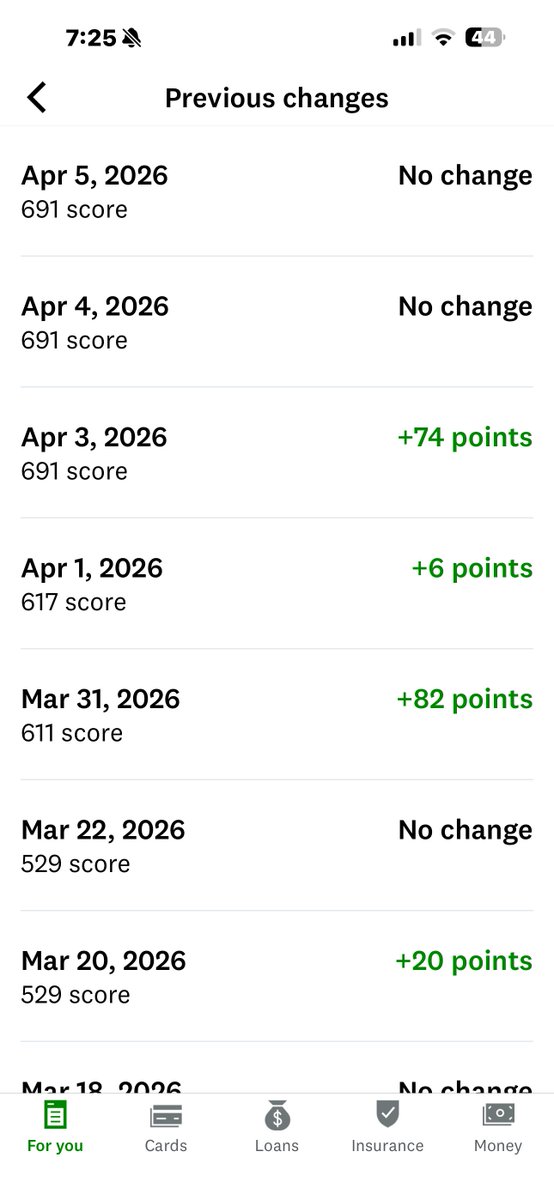

Your credit is 550 and you think it’s over?

Not even in the slightest.

I’ve helped 163 people fix their credit last year alone.

Average increase: 122 points in 90 days

↳ Fastest: 580 → 748 in 67 days

Here’s the exact process the credit bureaus hope you never find out about:

But first — understand how the bureaus actually work:

They are LEGALLY required to delete anything they cannot verify within 30 days

Their record keeping is sloppy

Most people never push back

That silence is what they’re counting on

Let’s change that.

Step 1: Pull Your Reports (Day 1-3)

Go to https://t.co/btY9NlNwvy

Pull all 3 bureaus — it’s free

Screenshot every page before you touch anything

You’re looking for:

→ Late payments

→ Collections

→ Charge-offs

→ Hard inquiries

Write them all down. This is your starting point.

Step 2: Send Debt Validation Requests (Day 4-7)

Contact the bureau AND the creditor directly for every negative item.

Ask them to prove:

→ They have the original signed agreement

→ A full payment history

→ Proof the debt was legally assigned to them

→ That they’re licensed to collect in your state

Send everything via certified mail. Keep every receipt.

Most creditors cannot produce this documentation.

When they can’t verify it — it has to come off.

Step 3: Goodwill Requests for Late Payments (Day 8-14)

For late payments you actually made — reach out to the creditor directly.

Keep it simple:

“I’ve been a customer for X years. I went through a difficult period. I’ve been current ever since and I’m asking you to remove that late payment as a goodwill gesture.”

Works 40-60% of the time.

Send it 3x to different reps if needed.

Step 4: Negotiate Pay-for-Delete (Day 15-30)

For any collection under $1,000 — you have leverage.

Offer to pay in full in exchange for a deletion agreement in writing.

Ask for:

→ Removal from all 3 bureaus

→ A written deletion letter

→ Confirmation BEFORE you pay anything

Around 60% of collectors will agree.

Get the agreement first. Always.

Step 5: Get Added as an Authorized User (Day 31-45)

Find someone with:

→ 750+ credit score

→ Account open 10+ years

→ Utilization under 10%

Ask to be added as an authorized user.

You don’t even need to use the card.

Their history attaches to your report.

This alone can move your score 50-100 points.

No one in your circle? Tradeline companies offer this for $150-500.

Step 6: Start Building Fresh Credit (Day 46-60)

While disputes are processing, start stacking positive history:

→ Secured card ($200 deposit)

→ Credit builder loan ($500)

→ Self account

→ 2-3 authorized user accounts

All report monthly.

All move your score in the right direction.

Expect 10-20 points of growth per month just from this.

Step 7: Control Your Utilization (Day 61-75)

Most people get this wrong.

Pay your balance BEFORE your statement closing date — not just the due date.

Target: 1% utilization showing on your statement. Not 0%. Not 30%. 1%.

Example:

$1,000 limit card

Spend $500

Pay $490 before statement closes

Statement reports $10

That one move = 30-50 point jump.

Step 8: Challenge Unauthorized Inquiries (Day 76-90)

Go through every hard inquiry on your report.

Any you don’t recognize? Write to the bureau:

“I have no record of authorizing this inquiry. Please investigate and remove it.”

~30% get removed.

Each one is worth 5-10 points.

Small wins stack fast.

Real people who followed this exact process:

Videographer working 9-5, couldn’t get funded for his first Section 8 property:

↳ 612 → 782 in 63 days

↳ Walked away with $42,000 in business funding

Single mom with a $15,000 eviction destroying her credit:

↳ 562 → 711 in 84 days

↳ Eviction deleted. Housing secured.

9-5 worker with years of missed payments holding him back:

↳ 483 → 763 in 71 days

↳ Clean file. Score unlocked.

After 700+ — here’s how you stay there:

→ Utilization between 1-9% always

→ Automate every payment, no exceptions

→ Apply for new credit strategically every few months

→ Never close your oldest accounts

→ Keep a mix of credit types

And once you hit 680+:

→ Register an LLC or sole prop

→ Get an EIN free at https://t.co/LiAf96SuJ4

→ Open a business checking account

→ Stack business credit cards

Now you have two credit profiles building at the same time.

That’s where real funding starts.

Your 12-week roadmap:

Week 1 — Pull reports, find every negative item

Week 2 — Send validation + goodwill letters

Week 3 — Negotiate pay-for-delete

Week 4 — Add authorized user tradelines

Weeks 5-8 — Build new positive accounts

Weeks 9-12 — Monitor, maintain, watch it climb

Bad credit is not permanent.

It’s a system — and systems can be worked.

Your next 90 days matter more than your last 10 years.

Comment “REPAIR” below and I’ll send you every template, script, and letter I use — for free. 👇

Your credit is 550 and you think it’s over?

Not even in the slightest.

I’ve helped 163 people fix their credit last year alone.

Average increase: 122 points in 90 days

↳ Fastest: 580 → 748 in 67 days

Here’s the exact process the credit bureaus hope you never find out about:

But first — understand how the bureaus actually work:

They are LEGALLY required to delete anything they cannot verify within 30 days

Their record keeping is sloppy

Most people never push back

That silence is what they’re counting on

Let’s change that.

Step 1: Pull Your Reports (Day 1-3)

Go to https://t.co/btY9NlNwvy

Pull all 3 bureaus — it’s free

Screenshot every page before you touch anything

You’re looking for:

→ Late payments

→ Collections

→ Charge-offs

→ Hard inquiries

Write them all down. This is your starting point.

Step 2: Send Debt Validation Requests (Day 4-7)

Contact the bureau AND the creditor directly for every negative item.

Ask them to prove:

→ They have the original signed agreement

→ A full payment history

→ Proof the debt was legally assigned to them

→ That they’re licensed to collect in your state

Send everything via certified mail. Keep every receipt.

Most creditors cannot produce this documentation.

When they can’t verify it — it has to come off.

Step 3: Goodwill Requests for Late Payments (Day 8-14)

For late payments you actually made — reach out to the creditor directly.

Keep it simple:

“I’ve been a customer for X years. I went through a difficult period. I’ve been current ever since and I’m asking you to remove that late payment as a goodwill gesture.”

Works 40-60% of the time.

Send it 3x to different reps if needed.

Step 4: Negotiate Pay-for-Delete (Day 15-30)

For any collection under $1,000 — you have leverage.

Offer to pay in full in exchange for a deletion agreement in writing.

Ask for:

→ Removal from all 3 bureaus

→ A written deletion letter

→ Confirmation BEFORE you pay anything

Around 60% of collectors will agree.

Get the agreement first. Always.

Step 5: Get Added as an Authorized User (Day 31-45)

Find someone with:

→ 750+ credit score

→ Account open 10+ years

→ Utilization under 10%

Ask to be added as an authorized user.

You don’t even need to use the card.

Their history attaches to your report.

This alone can move your score 50-100 points.

No one in your circle? Tradeline companies offer this for $150-500.

Step 6: Start Building Fresh Credit (Day 46-60)

While disputes are processing, start stacking positive history:

→ Secured card ($200 deposit)

→ Credit builder loan ($500)

→ Self account

→ 2-3 authorized user accounts

All report monthly.

All move your score in the right direction.

Expect 10-20 points of growth per month just from this.

Step 7: Control Your Utilization (Day 61-75)

Most people get this wrong.

Pay your balance BEFORE your statement closing date — not just the due date.

Target: 1% utilization showing on your statement. Not 0%. Not 30%. 1%.

Example:

$1,000 limit card

Spend $500

Pay $490 before statement closes

Statement reports $10

That one move = 30-50 point jump.

Step 8: Challenge Unauthorized Inquiries (Day 76-90)

Go through every hard inquiry on your report.

Any you don’t recognize? Write to the bureau:

“I have no record of authorizing this inquiry. Please investigate and remove it.”

~30% get removed.

Each one is worth 5-10 points.

Small wins stack fast.

Real people who followed this exact process:

Videographer working 9-5, couldn’t get funded for his first Section 8 property:

↳ 612 → 782 in 63 days

↳ Walked away with $42,000 in business funding

Single mom with a $15,000 eviction destroying her credit:

↳ 562 → 711 in 84 days

↳ Eviction deleted. Housing secured.

9-5 worker with years of missed payments holding him back:

↳ 483 → 763 in 71 days

↳ Clean file. Score unlocked.

After 700+ — here’s how you stay there:

→ Utilization between 1-9% always

→ Automate every payment, no exceptions

→ Apply for new credit strategically every few months

→ Never close your oldest accounts

→ Keep a mix of credit types

And once you hit 680+:

→ Register an LLC or sole prop

→ Get an EIN free at https://t.co/LiAf96SuJ4

→ Open a business checking account

→ Stack business credit cards

Now you have two credit profiles building at the same time.

That’s where real funding starts.

Your 12-week roadmap:

Week 1 — Pull reports, find every negative item

Week 2 — Send validation + goodwill letters

Week 3 — Negotiate pay-for-delete

Week 4 — Add authorized user tradelines

Weeks 5-8 — Build new positive accounts

Weeks 9-12 — Monitor, maintain, watch it climb

Bad credit is not permanent.

It’s a system — and systems can be worked.

Your next 90 days matter more than your last 10 years.

Comment “REPAIR” below and I’ll send you every template, script, and letter I use — for free. 👇

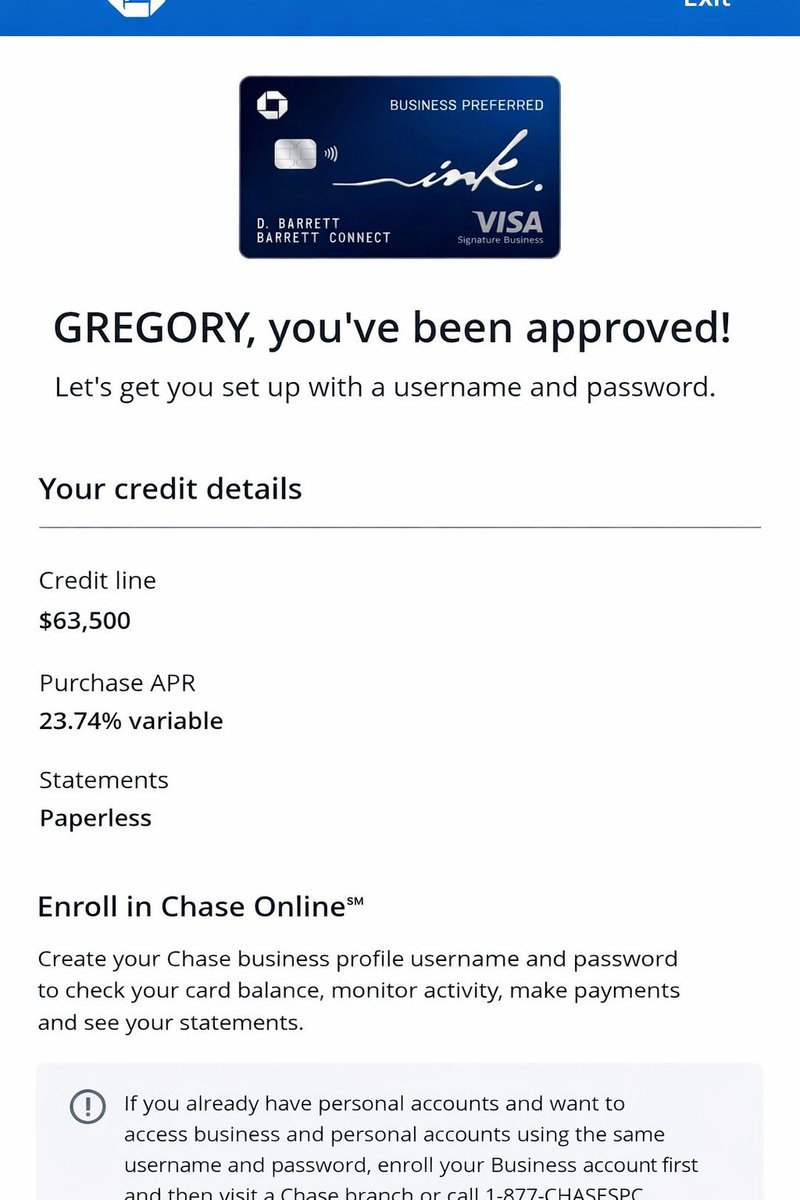

I got Gregory $251,500 in business funding in 26 days.

(he started with a poor credit score)

Here’s how in 15 steps:

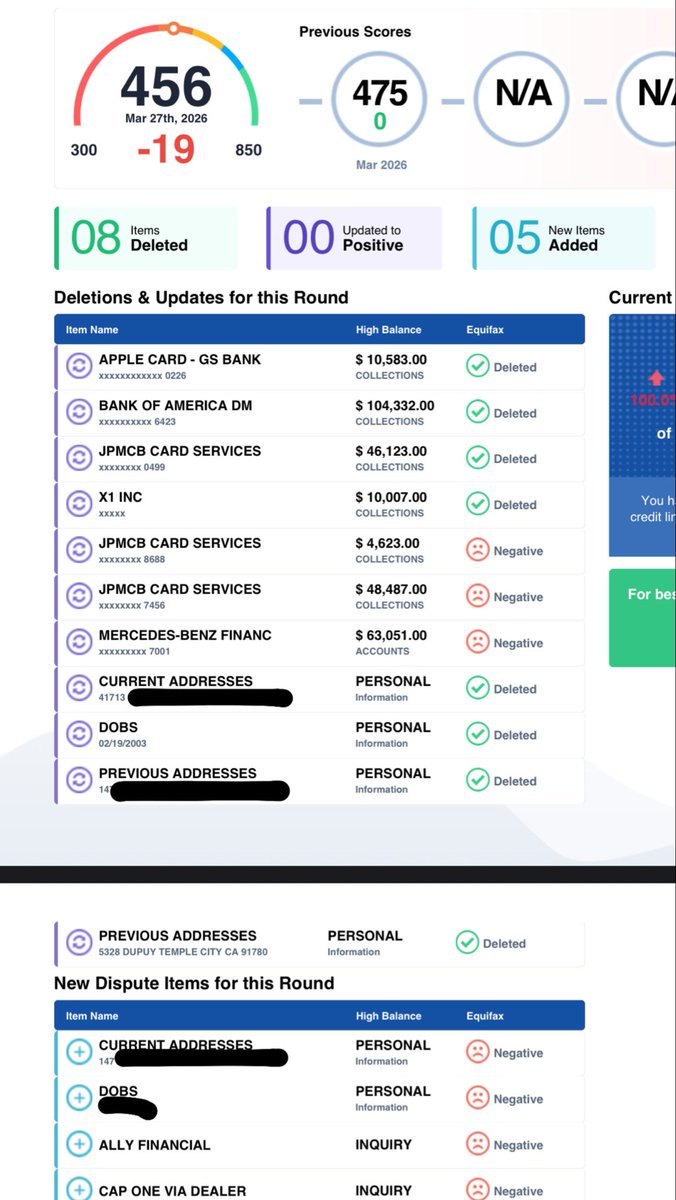

1. Pulled his credit report and found every negative item (10 mins)

2. Disputed all incorrect personal info — old addresses, wrong names (1 day)

3. Removed hard inquiries that didn’t belong (3-5 days)

4. Paid down all credit card balances to under 10% utilization (7-14 days)

5. Got his score above 700 (>30 days)

6. Filed his LLC (10 mins)

7. Got an EIN from the IRS website (5 mins)

8. Set up a business address (1 day)

9. Set up a business phone number (1 day)

10. Opened a dedicated business checking account (1 day)

11. Applied for a Chase business card using our relationship ($63,500 approved)

12. Stacked another Chase 0% interest business card ($38K approved)

13. Applied for Amex Blue Business Cash ($25K approved)

14. Applied for Amex Blue Business Plus ($25K approved)

15. Secured a $100K business line of credit with Citizens Bank

Total: $250,000 in funding.

In 30 days.

The banks didn’t say maybe.

They said yes. Every single time.

Because we made his profile impossible to deny.

Comment “FUNDED” below and I’ll send you the exact method. 👇

Must be Following and Retweet to Receive

I got Gregory $251,500 in business funding in 26 days.

(he started with a poor credit score)

Here’s how in 15 steps:

1. Pulled his credit report and found every negative item (10 mins)

2. Disputed all incorrect personal info — old addresses, wrong names (1 day)

3. Removed hard inquiries that didn’t belong (3-5 days)

4. Paid down all credit card balances to under 10% utilization (7-14 days)

5. Got his score above 700 (>30 days)

6. Filed his LLC (10 mins)

7. Got an EIN from the IRS website (5 mins)

8. Set up a business address (1 day)

9. Set up a business phone number (1 day)

10. Opened a dedicated business checking account (1 day)

11. Applied for a Chase business card using our relationship ($63,500 approved)

12. Stacked another Chase 0% interest business card ($38K approved)

13. Applied for Amex Blue Business Cash ($25K approved)

14. Applied for Amex Blue Business Plus ($25K approved)

15. Secured a $100K business line of credit with Citizens Bank

Total: $250,000 in funding.

In 30 days.

The banks didn’t say maybe.

They said yes. Every single time.

Because we made his profile impossible to deny.

Comment “FUNDED” below and I’ll send you the exact method. 👇

Must be Following and Retweet to Receive

At 21 I defaulted on $100,000+ in credit cards.

My business collapsed. Relationships fell apart. Credit got destroyed.

I thought it was over.

Then I learned something most people don’t know —

In America you can legally remove debt from your credit report AND discharge what you owe once it’s sold to collectors through litigation

Fast forward to 23.

Credit back in the 700s. Just got a new Tesla. Debts wiped.

And that is why, It’s not over until it’s over.

This is why I’m obsessed with the credit game.