So many people are concerned about the $ETH merge that no one is talking about $XRP's important week in terms of regularity clarity. Would the flip finally be switched @thebearablebull ?

I went through @Delphi_Digital’s report on crypto neobanks, and there’s a lot in there.

Here are the bits that stood out to me ↓

1️⃣ Crypto card usage is growing fast

Crypto card volume hit $9.8B cumulative, with 23.43M transactions and 1.6M addresses.

May 2026 alone did $830M+ in monthly volume, roughly 16x growth in two years.

And even that likely undercounts the market because exchange-issued cards like @Coinbase and @Gemini settle some activity internally, so it does not show up onchain.

2️⃣ The market is already concentrated

There are 190+ crypto neobanks now, but most volume still goes through a small group of players.

This feels like one of those markets where everyone launches the same card, but only a few have a real edge.

3️⃣ @Visa is still the king here

Visa handles roughly 96% of all onchain crypto card volume. Actually insane if I'm being honest.

And even when the front-end looks crypto-native, most of the experience still runs through existing card rails.

You tap the card, Apple Pay works, the merchant gets paid, and the crypto part mostly happens in the background.

4️⃣ The card is not the real upgrade

This was the most important part for me.

Because stablecoins make the payment stack more efficient behind the scenes.

Instead of relying on slow settlement cycles, companies get a faster way to move, reconcile, and manage money globally.

The user still gets a normal payment experience, but the backend gets cleaner.

5️⃣ Delphi splits crypto neobanks into 5 models

→ Full-stack issuers

→ Exchange-backed cards

→ Non-custodial DeFi-native cards

→ Stablecoin-native neobanks

→ Remittance-first cards

I liked this framework because it makes it easier to tell which teams are building a real financial product, and which ones are mostly shipping another card with crypto branding.

6️⃣ The picks-and-shovels model looks strong

Because full-stack issuers like @raincards sit closer to the card network layer, and they own more of the infra and capture economics across multiple card programs.

I like this model because full-stack issuers do not need to be the crypto card everyone uses. They benefit when more wallets, exchanges, and apps want to launch cards of their own.

7️⃣ The real demand is in weak banking markets

I don’t think the biggest use case is people in developed markets replacing Apple Pay or their normal credit card.

Those already work fine.

IMO, the stronger use case is in markets where traditional banking is expensive, unreliable, or hard to access, and that’s why @RedotPay stood out in the report to me.

8️⃣ Remittance-first cards feel more practical than “spend crypto” cards

For companies like @Bitso, @Felixpago, and @get_aspora, the card is more like the last step.

The real product is moving money across borders, giving people dollar access, and letting them spend locally after receiving funds.

Felix Pago has already processed over $5B in cumulative volume for more than 1M users across South America, which says a lot about where demand is real.

9️⃣ DeFi-native cards are trying to make the wallet the bank account

Products like @MetaMask, @phantom, @ether_fi, and @gnosispay are taking a different route.

Instead of moving funds from wallet → exchange → bank → card, the idea is to spend from the wallet side.

@ether_fi Cash is interesting here because users keep assets in an onchain vault and borrow against them for everyday spending.

Still early, but I like the direction.

🔟 The endgame is probably convergence

Stablecoins can win without every crypto company winning.

@Visa, @Mastercard, @Stripe, and other incumbents are already moving toward stablecoin settlement, so I don’t think this ends with crypto replacing the entire card stack overnight.

More likely, incumbents absorb parts of the backend upgrade, while a few crypto-native players survive by owning distribution, balances, or a very specific regional pain point.

My read:

A crypto card by itself is not that interesting anymore.

The winners will be the ones people trust to hold, move, and spend their stablecoin balances.

The mechanics underneath @pendle_fi have quietly stacked in $PENDLE holders' favour.

At the moment the setup is really strong:

➥ Trading cheaper than the average DeFi yield protocol on a price-to-fees basis (11.6x vs 12.25x sector median)

➥ 22% of total supply staked as sPENDLE

➥ Major token unlocks already behind us

➥ 80% of all V2 fees route to PENDLE buybacks under sPENDLE

The bid is structural and the catalysts that could compound it are real👇

1. STRC tokenization is already working.

‣ Saturn's sUSDat pool drove a 44% PENDLE rally in 11D as users got onchain exposure to Strategy's 11.5% dividend

‣ apxUSD grew from $13M to $461M onchain mcap in 77D. apyUSD doing the same

Strategy's actual STRC ATM authorization is ~$21B with ~$21B in remaining capacity. The $1.16B raise on April 13 was one day's issuance. If they keep printing, this becomes Ethena-scale flow without the funding rate dependency

2. Regulated stablecoin rails shipped in March. USDG (Paxos / Global Dollar) pools went live and crossed $120M. mEVUSD strategy targets EU institutions at 7-12% returns. Compliant institutional yield is no longer a roadmap item

3. The yield gap is the actual moat. CEX flexible earn for large balances are around ~1.5-4%. The spread runs from +2.6pp to +17.3pp. That's a 3-12x improvement on idle stablecoin yield, sitting right next to the largest pool of idle yield-seeking capital in crypto

4. @boros_fi is the 2nd revenue engine. ~$17.2B in cumulative volume since launch. $150M OI today and ~$600k in cumulative fees across 4 revenue streams and still climbing. Fee:OI ratio is at 0.461% annually. The total perp market is ~$132B, if it has 2% capture = $2.6B Boros OI = $12M annual fees, more than doubling Pendle's current 30D run-rate

5. ~$70B sits idle in CEX stablecoin balances earning ~1.5%. GENIUS Act effective Jan 2027 forces exchanges to either kill their earn products or route to a compliant DeFi backend. Pendle's semi-custodial Highway is purpose-built for exactly this. At 5% capture, sPENDLE buyback yield hits 9% annualized. Binance Labs is already an investor. No deal signed yet. Q4 2026 earliest realistic timeline

Tokenomics are fixed. Float is locked. Distribution surface expanding. Now Pendle is becoming the discount mechanism for the $100T+ global fixed income market moving onchain.

This one is forming one of the cleanest DeFi setups going into the H2 of 2026.

h/t to @EntropyAdvisors@DefiLlama for the data

My $0.02 - as someone who's been equally involved with Hyperliquid and Solana and admires both ecosystems.

If I were working at foundation, this is what I'd want to see to tweak things in Solana's favor.

1. Phoenix needs to get rid of that invite code nonsense asap because brother its 2026..

2. For perpetual exchanges, there are two core aspects that have nothing to do with settlement chain. You need a group of MMs and you need a risk engine. Hyperliquid could bootstrap this fairly well, and the airdrop incentivised MMs. Many of them ended up millionaires and that liquidity went towards HIP-3/HIP4.

Solana folks need to stop looking at this as a liquidity constraint and think who are the best MMs and what are the best assets. And no, thinking you don't need to incentivise those MMs doesn't work because the MMs are booking sufficient margins arbing tradfi stocks and currency pairs on Hyperliquid.

Hyperliquid launched in a zero competition market.

Solana's perp ecosystem is not launching in a blank market.

3. Hyperliquid was consistently early to listing new assets. Often times - that move hurt it because risk assessment is hard (jellyjelly). But it was one of the best places to go long on perps before Binance listed it. Speed of listing new assets was the pitch. It still is - you can trade spacex there before you can trade it on NASDAQ. Phoenix lags (from what I see).

compare this with number of assets on solana native perps.

4. Hyperliquid's core culture is built around a full-fledged product that is aesthetic. The attention to detail on Hyperliquid is often absent on many Solana native perps. You need to get off the feeds and open these products on two large monitors and spend a whole sixty minutes on these things and you will see the stark difference.

5. Solana's core value prop is actually in its RWA ecosystem. Instead of battling on crypto-native perps, or going after what Hyperliquid owns today, Solana should probably look towards the 350 assets Ondo supports and enable perps for them.

Why? You have a base market where MM's can go back to USDC on, MMs will want to hedge on a perp exchange and Solana has a strong lead here (compared to ETH/L2 ecosystem). You have an ecosystem of wallets that will embed these instruments.

You want to bring nasdaq on chain? Brother focus on those assets!! Tokenised compute, commodities, emerging market indices - are all blank spaces. And Hyperliquid does not own those markets today.

6. Hyperliquid dominates user mind-share now because it has done the three things necessary to build a cult in crypto. It built a product that speaks to tradfi (pre-ipo/hip3), it made an incredibly powerful stack (hip3/usdh) and it enriched people in the process.

Solana did the same with USDC and fwiw, to a certain extent with meme coins. Trying to battle it out on Hyperliquid's turf is trying to convert a cult. I belong to that cult - unless you have a superior product that has as much - people wont convert over

Hyperliquid has an incredibly powerful flywheel going on for it right now in that when tradfi stocks list, it has become the pricing avenue. The last time this happened with a primitive in crypto was with prediction markets - when they were more effective than traditional outlets at pricing election odds.

Crypto native approaches to competing with a behemoth whose moat is on risk engine, liquidity, a cult-like userbase and tradfi relevance is fairly weak. Teams on solana should frankly be looking a bit more deeper than the surface.

DMs open if you're building on either networks. I think the pie is a lot bigger than what we presume it is on X. We are talking about bringing the world's finances on-chain.

Cumulatively these ecosystems are at $80 billion. I think they will be worth $10 trillion in ten years. Too early to be bickering over size of the slice. Focus on the pie.

GOODBYE, FUND MANAGERS. GOODBYE, BLOOMBERG TERMINAL.

No more $24,000/year subscriptions.

Claude just turned my laptop into a private quant analyst.

Here are 07 prompts to build your own hedge fund at home ↓

I literally have 0 coding experience and had never worked with Dune dashboards before.

It always annoyed me having to rely on other people’s dashboards and never finding the exact data I was looking for, so I figured I’d try building one myself with AI.

With Claude’s help, it took me less than 1.5 hours, and most of that was just understanding how Dune works. The next one would probably take under an hour.

I remember some of our portfolio companies paying thousands of $$ for these and waiting weeks for them to go live.

Even though this trend has been obvious for a while, this really made it click for me just how much AI is eroding the moat and defensibility of developers, and how easy it is now for a complete beginner like me.

Devs are cooked.

With all due respect to Chris, I completely disagree with this take.

Chris argues that "web3," particularly crypto-powered gaming and media, failed due to scams and regulation, and that better regulation will unlock these non-financial cases.

OK, think about this for a second.

Does this pass the smell test?

Do you think web3 gaming failed because of Gary Gensler? Do you think web3 media plays failed because the scammers crowded out the honest media innovators? Really?

If this is true, why didn't they kill financial crypto, which had WAY more of both? Financial use cases were right in the crosshairs of the regulatory harassment, and they also attracted way more scams.

Why shouldn't we instead accept the more obvious answer: non-financial use cases for crypto have failed because no one wants them.

Let's just admit it. They were bad products. They failed the market test. It was not Gensler or SBF or Terra that caused these things to fail, it was that no one wanted any of it. Pretending otherwise is cope.

Enormous sums of capital and talent explored these ideas, and we should acknowledge what we learned. That lesson is not "if we just had better laws, then finally people would finally be using decentralized Spotify" or whatever.

Call a spade a spade. Every single use case in crypto that has worked at scale has been financial in nature.

2008: Bitcoin - non-sovereign store of value

2014: Tether - stablecoins

2015: Ethereum - programmable money

2017: ICOs - capital formation

2018: Prediction markets (Augur, later Polymarket)

2020: DeFi - literally finance is in the name

2021: NFTs - non-fungible financial assets (to the extent they worked)

2024: RWAs (the year BUIDL took off)

All this stuff was adopted bottoms-up. We as investors discovered that people wanted to do these things with crypto. The web3 consumer stuff, on the other hand, was primarily conjured up by investors and pitch decks, ZIRP accelerationism, and "wouldn't it be crazy if" blog posts. This was the opposite of the "what smart people are doing on their weekends" thesis.

In fact, if you go back to the Ethereum white paper from 2014, almost every single Ethereum use case Vitalik describes is financial in nature: token issuance, stablecoins, derivatives, on-chain treasuries/DAOs, on-chain savings, insurance, price feeds, escrow, gambling, prediction markets. It's all in there.

This is nothing to be ashamed of. Finance is almost 10% of GDP. It's an enormous part of the world economy, and banks are some of the lowest NPS score companies in the world. People hate their banks and the outdated financial architectures their money runs on. It's literally why Bitcoin was created. There is so much to innovate in the realm of finance, and I truly believe we are only at the beginning of that displacement. You don't need to assume anything more to project the next 10x in crypto.

The old saying goes "crypto will do to finance what the Internet did to every other industry."

I respect Chris's optimism. But 18 years in, we should not be propagating this meme about consumer web3 use cases as though they're inevitable. If you are hanging around the rim hoping that crypto is going to disrupt media and gaming, you should know the history and look at it with clear eyes.

Now if you as a founder believe that despite that, you know the secret to cracking this market--I respect that, and I certainly don't begrudge anyone to follow their convictions.

But I think it's important that investors be honest that all the evidence points the other way.

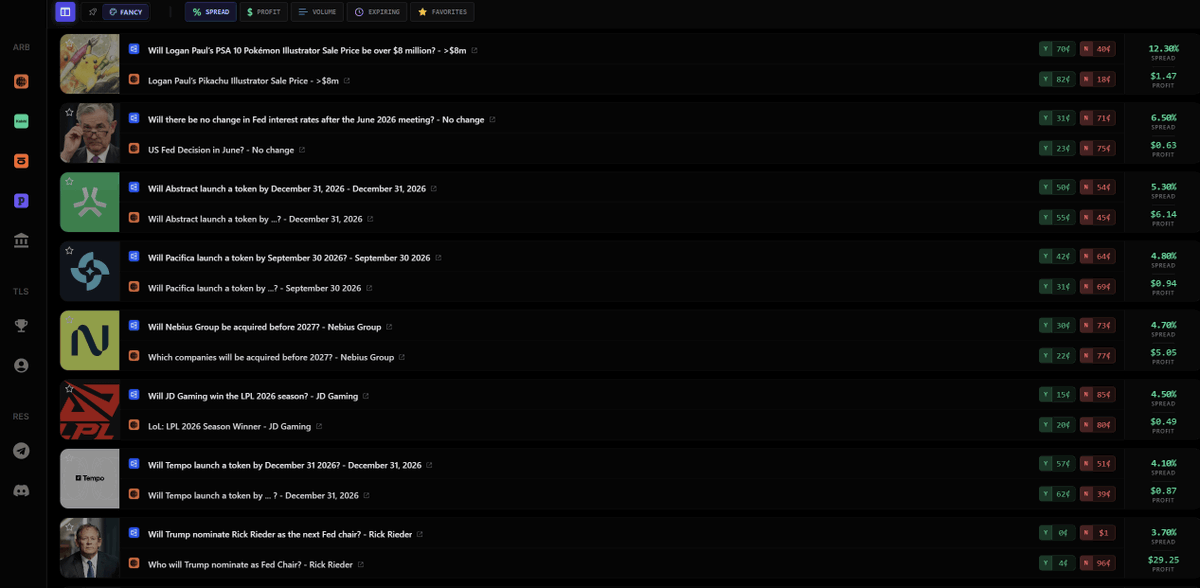

Have you ever thought about placing bets on the @Polymarket with leverage?

As in all perps? Instead of betting $50, would you bet $100 or $500 when you only have $50 in your account

This project is supported by Polymarket Builders and Binance.

This is -> @ultramarketsxyz

Here, just like on perps, you can open LONG and SHORT positions with different bets on the Polymarket

For example, I opened a LONG position that the OS would only be $1b FDV with 3x leverage.

The project is in closed beta testing and is only accessible with codes

I have 5 of them ->

UM8H95P91T

UMNHJWXXDH

UM2JB5A96H

UMILYR8M3K

UM3QVABM4J

One of my favorite DeFi strategies lately has been prediction market arbitrage.

It's a great way to make solid profits while also farming Polymarket's upcoming airdrop.

Here's how it works:

• Go to @opinionlabsxyz or Polymarket

• Find an identical prediction market that is available on both platforms

• Check if there's a spread difference between the odds for that market on the two platforms

• If you can buy YES + NO shares for less than 99.9c, then do it to lock in a profit

When that prediction market expires, it's guaranteed that each 1 YES + 1 NO share will be worth $1 regardless of the outcome.

Here's an actual example:

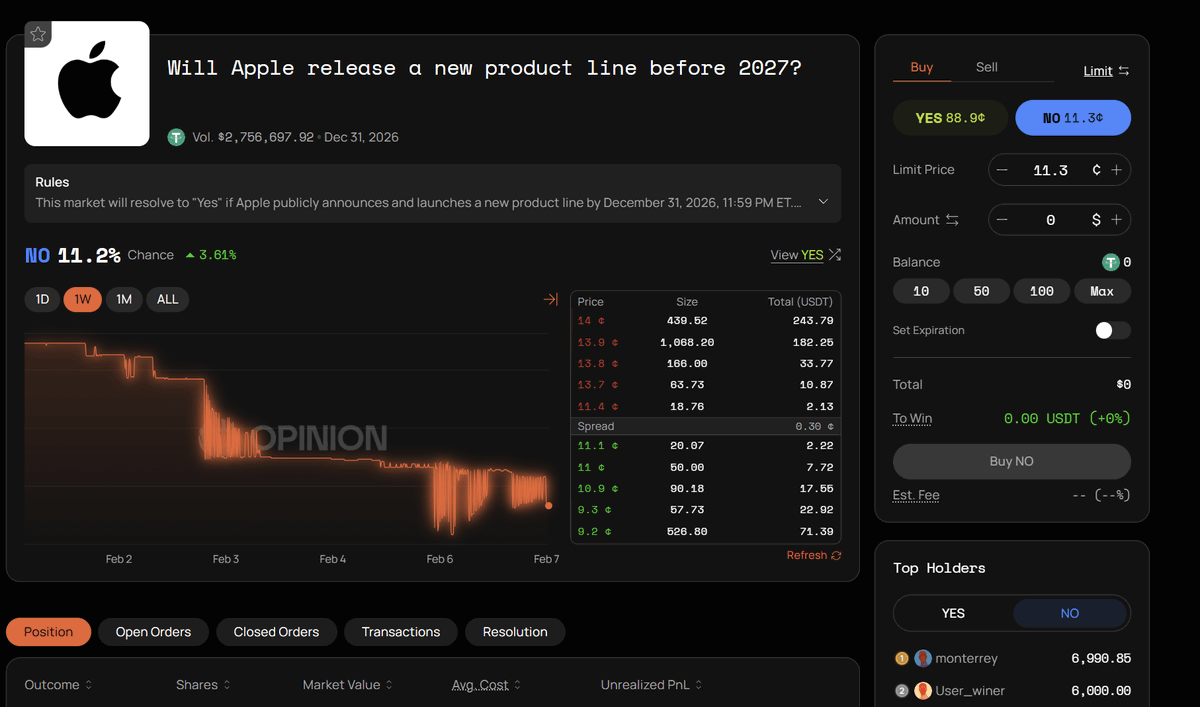

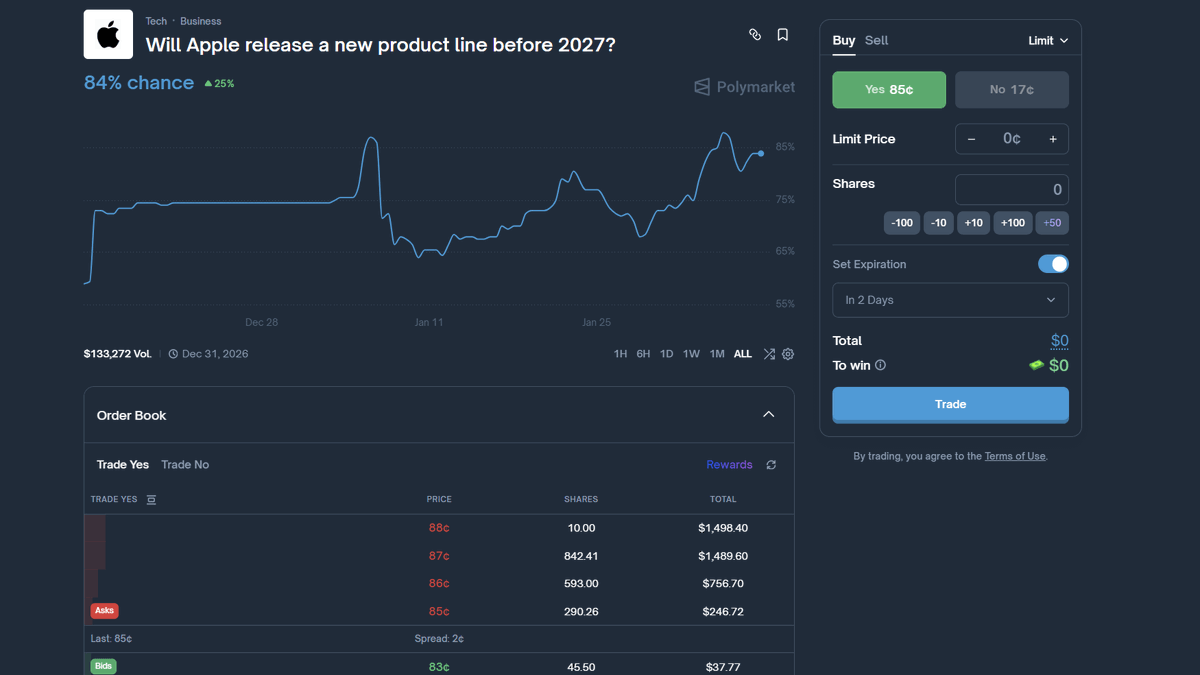

On Polymarket, you can bet that Apple will release a new product line before 2027 by buying YES shares at 85c.

On Opinion, you can buy NO shares for the exact same market at 11.4c.

Buy the same number of YES shares on Polymarket and NO shares on Opinion, and you will lock in a profit as 85c+11.3c=96.4c and is less than $1.

If you invest $1000, you'll make $36.

Now ideally, you want to use this strategy only for markets that expire soon (within 2-3 months at most), so you don't have to wait too much until you can collect your profit.

You can read the market rules to see the end date.

You can find opportunities like this in 2 ways:

• Manually - search the identical markets on Polymarket and Opinion, and see if there's any arbitrage opportunity

• Automatically - A tool like AlertPilot dot io built by @securezer0 uses AI to automatically find prediction market arbitrage opportunities

In this example, AlertPilot requires paying a subscription, but if you want to do arbitrage with significant capital, it might be worth it.

Why do I believe that arbitraging prediction markets is a good idea?

Because with this strategy, you not only make a decent profit, but also farm Polymarket and Opinion.

If Polymarket launches a token, it could easily do the biggest airdrop of 2026. The valuation of Polymarket's latest funding round is $9 billion.

Let's say that its token has a $10b FDV at launch and there's only a 5% token airdrop allocation. Its airdrop will still be worth $500M.

A $500M airdrop would be massive given that Polymarket TVL is only $353M at this moment.

And I think that Opinion airdrop will also be pretty good.

I strongly believe that farming prediction market platforms will pay off tremendously.

My friend @arndxt_xo built a personal AI “intern” using Clawdbot, an open-source agent running locally or on a free cloud server, connected to his everyday tools (Telegram, email, browser, files, etc.).

The system captures thoughts, organizes information, runs research, schedules tasks, and automates workflows.

By externalizing memory and execution to an AI agent, he transformed chaotic information into structured, reusable knowledge and real productivity.

Here’s how he did it, step by step:

1/ He used an always-on machine: either a Mac mini or a free AWS server (EC2 micro).

2/ On AWS, he launched an Ubuntu instance (Free Tier micro), enabled billing alerts, and connected via SSH/terminal.

3/ He installed Clawdbot with a one-liner

4/ He ran the setup wizard to choose the model/provider and configure a channel (Telegram first).

5/ He created a Telegram bot via @BotFather, copied the token, and plugged it into the wizard.

6/ He locked the bot by restricting access to his user ID.

7/ He defined the agent’s identity, role, and timezone (assistant, ops, research, etc.).

8/ He then used Telegram as the control center to capture ideas, summarize content, organize files, recall projects, run research, and automate scheduled routines.

Really worth the read, you’ll learn a lot!

I found recent launches to reflect reality disturbingly well

I ran it on a free tool that exposes why 84.7% of 2025 tokens are underwater

I've been saying this forever, beucase teams obsess over tge and ignore post-launch mechanics.

the result is often too much sell pressure that rugs the prices within months

here is the sell pressure simulator built by @Delphi_Digital the monte carlo model for token unlock dynamics.

founders, if you are launching a project here is how you can use it:

- input unlock schedule vesting terms

- selling assumptions liquidity conditions

- shows you 25th-75th percentile price paths across thousands of scenarios

the 84.7% stat proves what I already knew:

- tokenomics is broken industry-wide

- teams copy-paste vesting schedules without modeling outcomes

- shocked when holders dump

I'm comparing different allocation strategies side by side. longer vests don't always help if unlock amounts are huge. smaller frequent unlocks sometimes better than large quarterly ones

I'm bookmarking this for every founder who asks me about tokenomics. run your model through this BEFORE finalizing allocations

most won't. they'll launch with beautiful deck and 18-month lockup thinking that's enough.

tool is live

no excuse for bad tokenomics anymore

just wilful ignorance

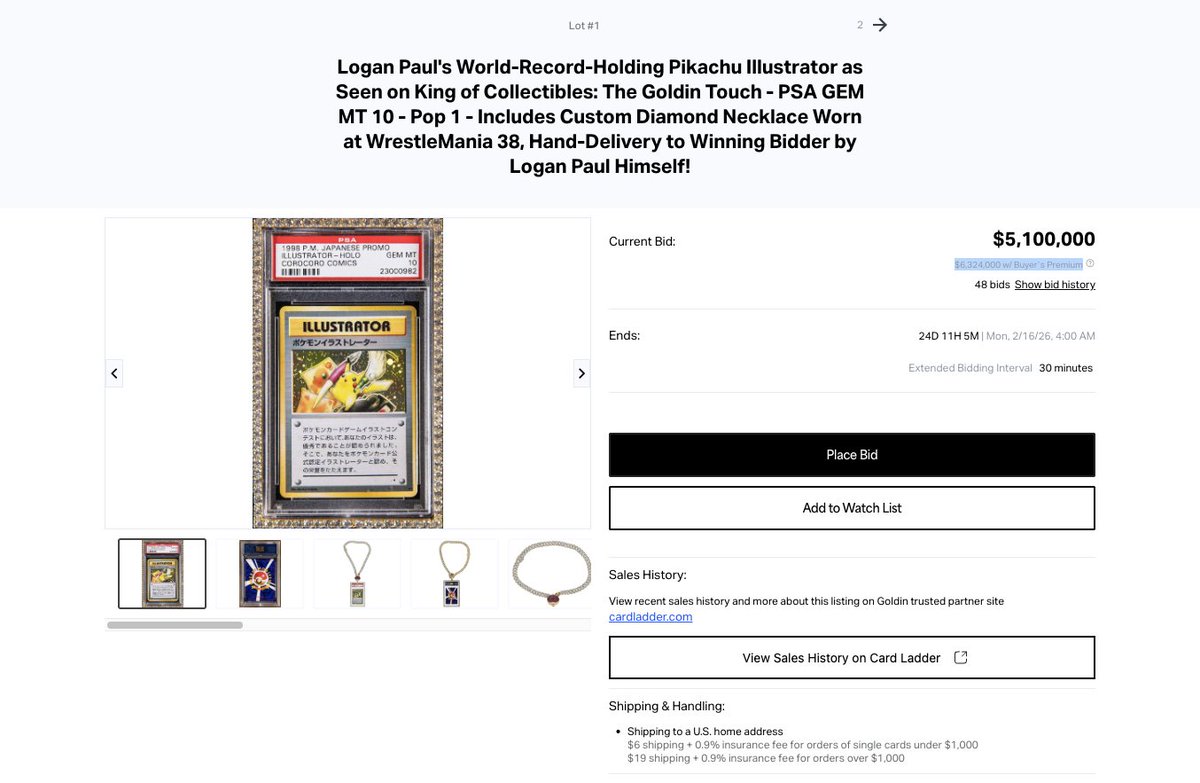

The Pickachu Illustrator card from @LoganPaul is projected to sell for $7-12M on Goldin.

This would mean that the winning buyer will likely pay around $2-3M in fees alone.

That's literally the entire thesis on why platforms like @Collector_Crypt and @Beezie will eat the entire collectibles market alive.

1) The market is way bigger than you think.

Most people laugh at trading cards and collectibles as a "niche hobby."

The reality though is that trading cards alone are a $30B+ market. Total collectibles are even a $500B+ market, outpacing the growth of the overall economy significantly.

This isn't some small corner of the internet. It's a massive alternative asset class and a global market that's barely getting started.

2) Crypto rails will destroy traditional incumbents.

Current platforms are absolutely rinsing collectors:

- Goldin: 22-24% buyer's premium

- Sotheby's: 15-27% buyer's premium

- eBay: 13%+ seller fees + international fees + customs nightmares

Now compare that to Collector and Beezie:

- Much lower fees

- Instant settlement = no waiting weeks for payment

- Instant digital delivery = no waiting weeks for shipping

- Borderless access = no insane import duties

- On-chain provenance and authentication

- Secure vault storage

Same cards. Fraction of the cost. Faster. Global. Better.

3) Gamification brings back the magic.

But they're not just making collecting cheaper, they're making it exciting again.

Collector's Gacha Machine and Beezie's Claw are basically pack ripping on steroids for adults. The dopamine hit of opening packs, but for high-value grails.

Collecting slowly but surely became a boring transaction process. They turned it back into an experience again.

Now look at Logan Paul's auction through this lens:

1) It proves the market is massive, people are about to pay $10M+ amounts for a single Pokémon card.

2) It's wildly inefficient: at $12M, the buyer pays $2.88M in fees to Goldin. For what?

3) Logan probably left money on the table, gamified mechanics like Gacha or tiered pack drops could have driven much more engagement while achieving much higher sale prices

Buyers save millions. Logan makes even more millions. The platform still wins without being extractive.

That's not zero-sum. That's a bigger pie for everyone.

If you can't see these gems becoming unicorns, I can't help you.

Day 415: How to farm the @opinionlabsxyz airdrop without taking directional risk

If you don’t want to gamble on outcomes, this is the cleanest way to farm points:

> Find a market with bonus points enabled

> Prefer markets that are ending soon

> Use “split shares” and enter your amount

By splitting shares, you hold both YES and NO.

No matter the outcome, your PnL stays flat but Opinion rewards points based on how long you hold the position.

At current OTC prices, 1 point ≈ $30, so this effectively becomes a solid APR on stables while getting exposure to prediction markets without risk.

I started a fresh wallet with $50k this week to track points earned and calculate the real APR. Will share results once there’s enough data.

Bullish catalysts for $PENDLE:

- vePENDLE replaced by sPENDLE, removing multi-year locks and reducing friction to a 14-day withdrawal

- liquid, fungible sPENDLE enables full defi composability while still earning governance and rewards

- sharply lower staking risk profile opens the door to conservative and institutional capital

- ~20% staking participation leaves large upside as barriers to entry fall

- up to 80% of protocol revenue used for open-market PENDLE buybacks

- shift from inflationary vote-to-earn to buyback-and-distribute creates constant price-agnostic demand

- ~$40m annualized revenue now directly supports token value instead of emissions leakage

- manual gauge voting removed, eliminating complexity and expert-only reward extraction

- algorithmic emissions reduce total emissions by ~30%

- emissions routed to high-performing pools instead of politically favored ones

- fixes structural inefficiency where ~60% of pools were historically unprofitable

- higher capital efficiency improves margins and long-term protocol sustainability

- rewards are passive by default, voting only required during active proposals

- sPENDLE deployed in defi integrations remains reward-eligible, encouraging ecosystem usage

- legacy vePENDLE holders receive boosted virtual sPENDLE up to 4x based on remaining lock duration

- loyalty boost materially increases effective yield during the transition period

- linear decay of boosts smooths supply impact and avoids hard unlock cliffs

- no new vePENDLE locks creates a clean path to a single governance token

- removal of ve-based lp boosting reduces incentive distortion in new pools

- end of bribe-driven “pendle wars” cuts capital misallocation and short-term gaming

- tokenomics refactor removes growth bottlenecks instead of masking them with emissions

- allows liquid funds to allocate towards sPENDLE

- linn perpetually tweeting "pendle"