I just published a research piece on Tokenized Money Market Funds and why Ethereum is emerging as the institutional liquidity layer. This isn’t about crypto speculation, but about how regulated, yield-bearing assets are moving on-chain as financial infrastructure.

@SoSoValue

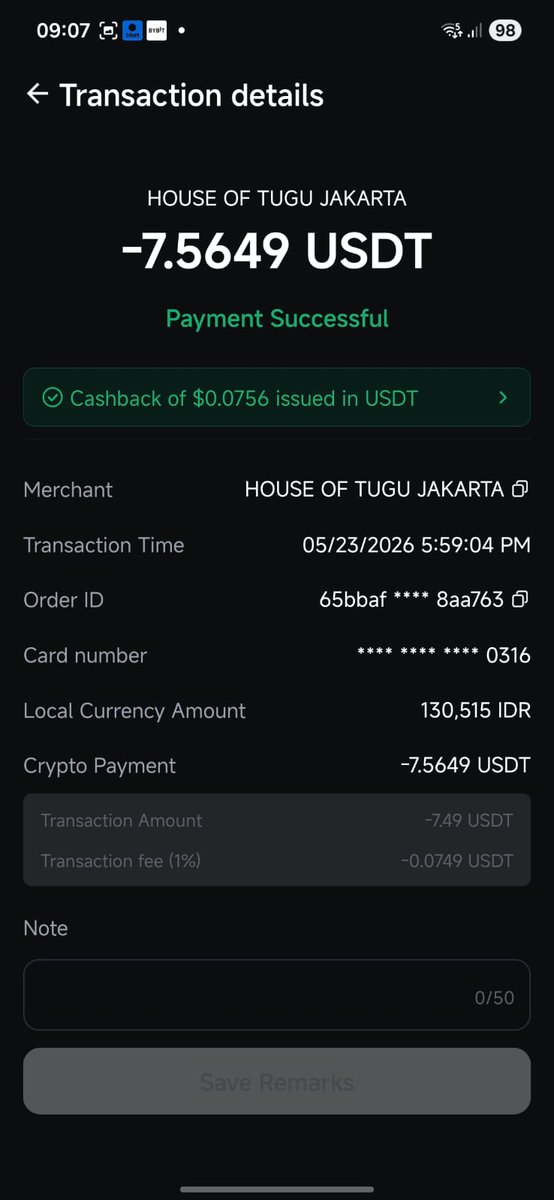

Kemaren nongkrong di House of Tugu Jakarta, bill 130.515 IDR.

Gua bayar pakai Pionex Card. Kepotong 7.5649 USDT, cashback 0.0756 USDT.

Pros: praktis + 1% cashback.

Cons: tetap ada FX/spread/fee, jadi cek rate dulu.

Code: https://t.co/GFGCnbMav4

Kemaren gua jajan di Matalokal, total 78.780 IDR.

Bayarnya pakai Pionex Card, yang kepotong 4.5652 USDT. Cashback masuk 0.0456 USDT.

Pros: stablecoin jadi usable + 1% cashback

Cons: rate final bisa lebih mahal dikit karena FX/spread/fee.

Code: https://t.co/GFGCnbMav4

Just claimed $30 free credit on Pioneer with my Pionex Card.

It has 59 AI models to test in one place: GPT-5.5, Claude Opus 4.8, DeepSeek V4 Pro and more.

Pioneer: https://t.co/lXSfWS4uaS

Pionex Card: https://t.co/GFGCnbMav4

Banyak yang masuk crypto modal FOMO, feeling, dan ikut sinyal.

Pas market berubah arah, baru sadar: mereka nggak punya peta.

Gua buka ulang free download ebook CRYPTOHELL Vol. 1 & 2 buat yang kemarin kelewat:

https://t.co/0sZZr8GhPp

Kemaren gua jajan di NYPD Pizza, total 42 ribu.

Gua bayar pakai stablecoin via Pionex Card. Yang kepotong 2.424 USDT, transaksi sukses, dan dapet cashback 0.0242 USDT

Pros: seamless + 1% cashback.

Cons: final rate bisa beda karena FX/spread/fee.

Code: https://t.co/GFGCnbMav4

This week, I will start breaking down crypto cards and real-world crypto utility.

One product I am watching is Pionex Card, because it connects trading, spending, cashback, and crypto utility.

Join Pionex Indonesia Telegram:

https://t.co/JkL77pTkao

The key crypto question is changing.

It is no longer only:

“What will pump next?”

It is becoming:

“What can people actually use?”

Long-term adoption will not come from hype alone. It will come from repeated, practical usage.

Crypto cards are not just about cards.

They are bridges between digital assets and real-world spending.

If crypto can move from holding and trading into spending, rewards, and cashback, the adoption story becomes much more practical.

CeDeFi sits between two worlds:

CEX simplicity: easy onboarding, support, smoother UX.

DeFi DNA: rewards, yield opportunities, and asset utility.

The result is not just a trading platform, but a more usable crypto financial layer.

Kesimpulan gue:

BI sedang memilih stabilitas dibanding pertumbuhan.

Rupiah harus diselamatkan dulu, walaupun ongkosnya pasar saham bisa goyang dan cicilan masyarakat makin berat.

Menurut kalian, BI sudah tepat atau telat?

BI naikkan suku bunga ke 5,25%.

This is not just a “rate hike”.

Ini sinyal bahwa rupiah sedang masuk mode defense.

Kalau BI sudah pilih obat pahit seperti ini, artinya tekanan ke rupiah memang sudah cukup serius.

Ke masyarakat, efeknya bisa terasa di kredit konsumsi.

KPR floating, kredit kendaraan, kartu kredit, pinjaman multiguna, dan paylater berpotensi makin mahal.

Kalau cicilan naik tapi pendapatan tidak ikut naik, daya beli bisa melemah.