🧵 Circle just received final OCC approval to establish a federally regulated national trust bank.

But the bigger story is what happens when that regulatory foundation meets USDC, CCTP and the @StellarOrg.

@circle National Trust will operate under direct supervision of the U.S. Office of the Comptroller of the Currency.

At launch, it will provide federally regulated digital-asset custody for Circle and its affiliates, with USDC reserve management planned as a future capability.

This is an important distinction:

Circle National Trust is not a traditional commercial bank offering checking accounts or loans.

It is a national trust bank designed to safeguard digital assets under federal fiduciary standards.

For institutions, that means stronger oversight, governance and transparency around the infrastructure supporting USDC.

Jeremy Allaire described the broader ambition clearly:

Leading financial institutions should be able to build on public blockchains with clarity and confidence.

That is where @StellarOrg enters the picture.

USDC is already natively issued on Stellar, a public blockchain built for fast, low-cost payments and global value transfer.

And Circle’s Cross-Chain Transfer Protocol is already integrated with the network.

CCTP allows native USDC to move between supported blockchains through a burn-and-mint process.

USDC is burned on the source network and an equivalent amount is minted on the destination network.

No wrapped version of USDC is required.

No traditional liquidity bridge is needed.

That matters because conventional bridges often introduce additional smart-contract, custody and liquidity risks.

CCTP does not eliminate every technical or operational risk, but it removes the need to rely on third-party wrapped assets.

Now combine the layers:

Circle National Trust

Federally supervised custody and potentially future USDC reserve management.

USDC

A regulated digital dollar designed for payments, settlement and capital markets.

CCTP

Native cross-chain mobility without wrapped USDC.

Stellar

A fast and inexpensive public payment rail connected to the wider USDC ecosystem.

The result is a potential end-to-end model:

Regulated custody → native USDC → Stellar settlement → cross-chain mobility through CCTP

Circle strengthens trust at the institutional layer.

Stellar provides an efficient rail for moving value.

CCTP connects USDC liquidity across supported networks.

Circle’s OCC approval does not mean that banks will automatically use Stellar.

But it strengthens the regulated foundation beneath USDC, while Stellar and CCTP already provide infrastructure capable of moving that digital dollar across networks and borders.

The significance is not that one blockchain has “won.”

It is that regulated financial institutions are gaining clearer access to digital dollars that can operate across public blockchain infrastructure.

And Stellar is already connected to those rails.

Federal oversight above.

Public blockchain settlement below.

CCTP connecting the liquidity between them.

That is the real power scenario.

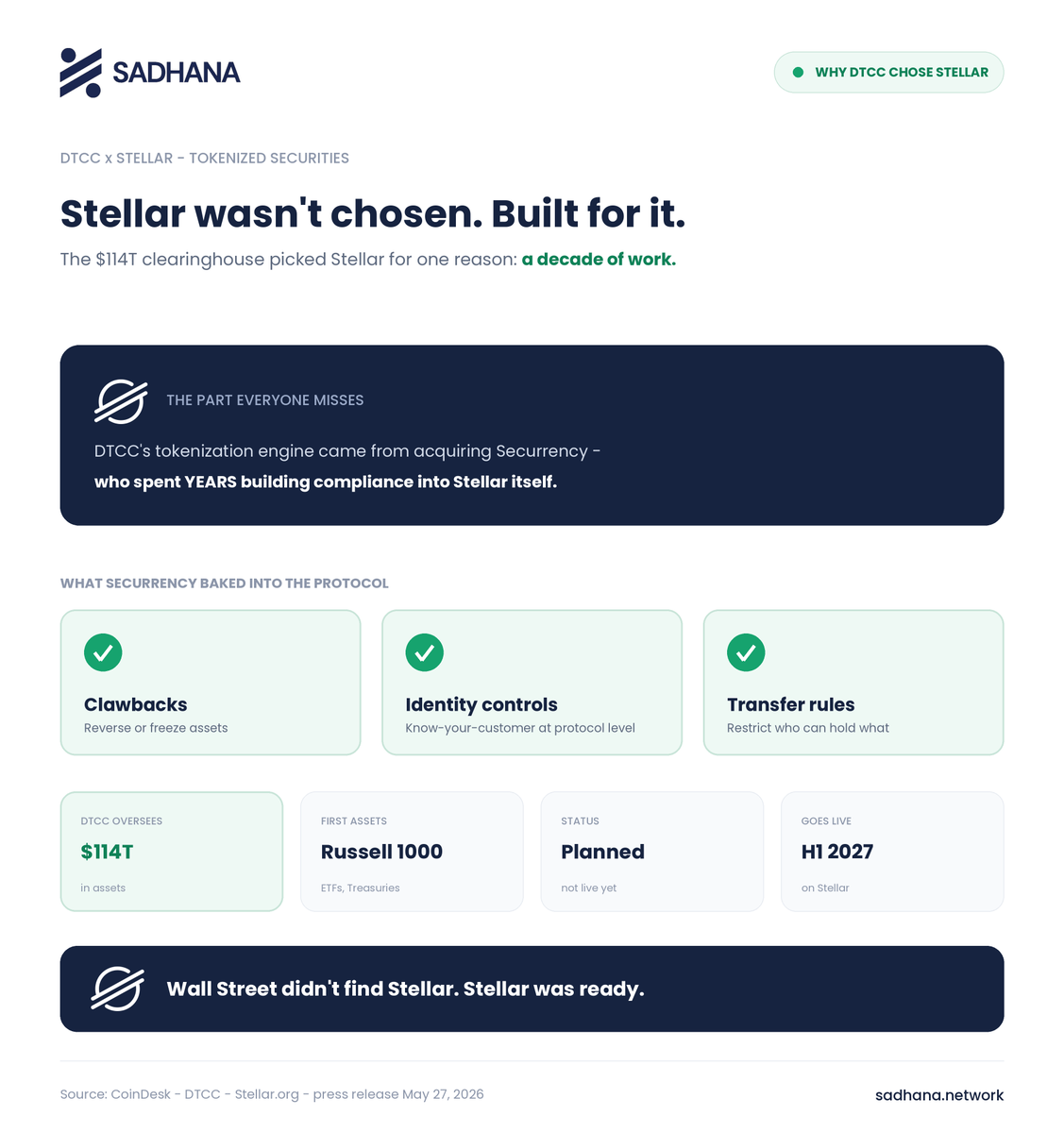

Everyone asks why DTCC picked #Stellar.

Here's the part they miss: 👇

DTCC's tokenization engine came from acquiring Securrency — who spent YEARS embedding compliance tools into Stellar itself.

Clawbacks. Identity. Transfer rules.

stellar:native wasn't chosen. It was built for this.

Amid endless misinformation,

Current blockchain networks integrated by The DTCC:

Stellar stellar:native — Public & Private

Hyperledger Besu — Private

Canton Network $CC — Private