Tracking the next wave of #Airdrops & Web3 gems. 🛰️

My goal: Bridge the gap between complex tech & real opportunities for the community. 💎

🔹 Early Alpha

🔹 Step-by-step Guides

🔹 Market Insights

Follow @cryptoweb121 and let's win together! 🚀🔔

#Web3#Crypto

A few glimpses from our Credible Vibes event in Bangkok!

where builders, investors, and marketers

came together to connect and exchange ideas

great conversations, great food, and even better energy

exactly how you want to start @money2020😎

Faster payments were supposed to fix everything.

They didn’t.

Yes, money moves quicker now.

Blockchains settle in seconds.

APIs are faster.

Fees are lower.

But for most businesses, payments still feel… slow.

Because speed alone doesn’t solve the real problem.

Payments aren’t just about how fast money moves.

They’re about how easily it can move.

Let’s say you’re a fintech expanding globally.

Even today, you still have to:

• onboard with multiple providers

• sign contracts and commit volumes

• prefund accounts across regions

• manage fragmented liquidity

Before your first transaction even goes through.

So what actually happens?

You get faster rails… sitting on top of the same old system.

-Capital is still locked

-Access is still gated

-Execution is still fragmented

This is why “faster payments” hit a ceiling.

They optimize speed

but ignore structure

Because a payment isn’t just a transaction.

It’s a sequence:

access → liquidity → routing → settlement → payout

If even one part is slow or constrained,

the whole system slows down.

And most systems today break at liquidity.

Money is sitting in the wrong place.

At the wrong time.

In the wrong amounts.

So even if settlement is instant,

execution isn’t.

That’s why faster payments need a new stack.

Not just better rails,

but better coordination.

A modern payment stack needs three things:

1. Instant settlement

so money can move globally without delay

2. On-demand liquidity

so capital is available exactly when needed

3. Smart orchestration

so payments find the most efficient path automatically

Without this, speed is wasted.

You can have millisecond block times

and still wait hours… or days… to complete a payment.

What’s changing now is the shift from:

prefunded systems → to on-demand liquidity

isolated integrations → to unified infrastructure

manual routing → to intelligent execution

This is where the next generation of payment infra is being built.

Where payments don’t rely on static balances.

Where capital doesn’t sit idle.

Where settlement isn’t something you wait for.

We at Credible are taking this approach with an Open Payment Stack.

Combining stablecoin rails, on-demand liquidity, and real-world payment orchestration into a single layer.

So payments don’t just move faster.

They actually work better.

stablecoins are no longer experimental!

they’re being used across payroll, merchants, and banking

the real question now is how seamlessly they integrate into payments infra👀

Most cross-border expansions don’t fail.

They just stop growing.

Everything looks right at the start.

New market, local partner, payments enabled.

-Then momentum fades

-Volumes stall

-Costs rise

-Payments start breaking in small ways

The problem isn’t demand, it’s infrastructure.

Every new corridor adds complexity:

• new integrations

• new compliance

• new liquidity requirements

Fintechs end up stitching systems together with capital locked across regions.

The biggest issue? Liquidity fragmentation

Money sits in the wrong place at the wrong time

So even “instant” rails don’t feel instant.

Add to that:

last-mile chaos

UPI ≠ Pix ≠ bank transfers ≠ wallets

Each behaves differently

each adds friction

So scale doesn’t compound.

It cracks.

The shift now is clear:

From corridor-by-corridor expansion to unified payment infrastructure

Where liquidity is on-demand and payments execute in real time

Because global expansion isn’t about entering more markets.

It’s about making them work together.

That’s what Credible’s Open Payment Stack is built for.

For years, the conversation around global payments focused almost entirely on speed.

Faster settlement, lower fees, and cross-border transfers became the defining features of modern payment infrastructure.

But speed alone does not create a seamless payment experience.

What matters just as much is local accessibility.

A payment only works when it reaches users through the systems they already use every day.

In India, that means UPI.

In Brazil, it’s Pix.

Across many regions in Southeast Asia and Africa, wallets and mobile-first payment systems dominate everyday transactions.

These are not secondary rails anymore. They are the primary financial interfaces for millions of users.

The challenge is that most global payment infrastructure was never designed around this level of localization.

Fintechs still need to manage separate integrations, fragmented liquidity, varying settlement timelines, and operational complexity across each market they enter.

As stablecoins scale globally, this complexity becomes even more visible.

Because supporting global settlement is one thing.

Connecting it seamlessly to local payment methods is another.

The next phase of payments will be defined by how efficiently global liquidity connects with local rails.

That’s what Credible is building through its Open Payment Stack

We are connecting stablecoin liquidity with real-time local payment systems through a unified infrastructure layer.

For years, the conversation around stablecoins focused almost entirely on supply growth, market capitalization, and transaction volume.

While these metrics helped demonstrate adoption, they never fully explained what gives a stablecoin lasting utility in the real world.

Utility does not come from issuance alone. It comes from distribution.

A stablecoin becomes valuable when it can move efficiently across markets, connect with local payment systems, and integrate seamlessly into the financial workflows people already use every day.

Without distribution, even the largest stablecoin supply risks becoming isolated liquidity sitting within fragmented ecosystems.

This is why the next phase of stablecoin adoption is less about creating new assets and more about building the infrastructure that allows those assets to flow globally.

As stablecoins expand across payroll, remittances, merchant payments, treasury operations, and cross-border settlement, the importance of distribution becomes even more visible.

Businesses do not simply need access to stablecoins.

They need reliable ways to move them between corridors, convert them into local payment methods, and settle transactions in real time without operational friction.

The challenge is that distribution at a global scale is complex.

Every region operates differently, local payment systems vary across countries, and liquidity remains fragmented across multiple providers and rails.

This creates inefficiencies that users rarely see directly but experience through delays, higher costs, and inconsistent execution.

The future of stablecoin utility will therefore depend on how effectively infrastructure layers can connect global liquidity with local payment systems in a seamless and scalable way.

That is the direction Credible is focused on through its Open Payment Stack.

It enables real-time settlement, on-demand liquidity, and access to local payment rails through unified infrastructure.

So far, Credible has processed more than $427M in total payment volume across fintechs, neobanks, and global payment operators.

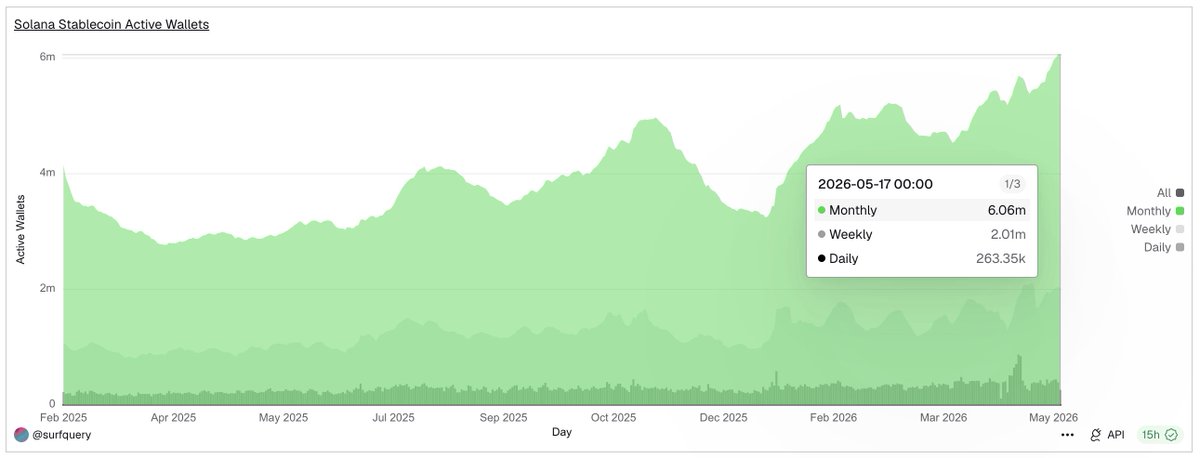

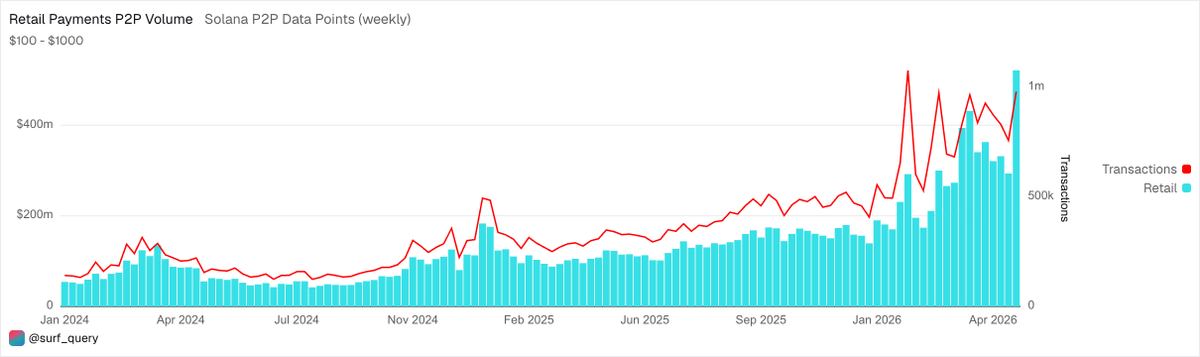

Solana’s stablecoin economy just had one of its biggest weeks ever:

1) Rolling 30D active stablecoin wallets reached a new ATH of 6.06M wallets

2) @Tether supply on Solana hit a new ATH of $3.75B

3) Retail peer-to-peer stablecoin payments ($100 to $1K) on Solana reached a new ATH of $521M in weekly volume alongside a record 981K transactions

Japan opening its framework to foreign stablecoins is a major step toward mainstream global adoption.

Regulatory clarity has always been one of the biggest missing pieces for stablecoin-powered finance.

What matters now is turning that clarity into real-world payment infrastructure, liquidity movement, and seamless global settlement.

The opportunity is no longer theoretical.

The rails for internet-native money are actively being built.

Credible has crossed $427M in total payments processed.

The volume comes from active fintech and cross-border use cases

Settlement is happening in real time, with liquidity available when needed.

This is what consistent infrastructure growth looks like.

live stats: https://t.co/SVSFlMc8NE

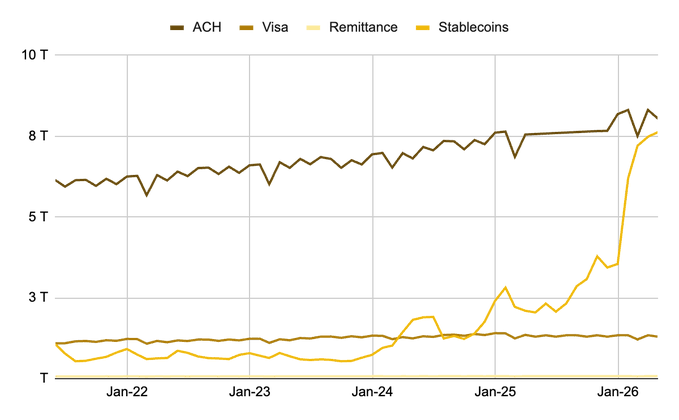

Binance Research reports that stablecoin volume is now nearing $8T, already surpassing Visa and moving closer to ACH scale.

That is a major signal for the future of global payments.

Stablecoins are no longer operating at the edges of finance. They are increasingly becoming part of real payment infrastructure used for settlement, transfers, and cross-border movement of capital.

As volume continues scaling, the focus shifts toward liquidity coordination, real-time execution, and seamless access to local payment systems.

That is the infrastructure layer Credible is focused on building through its Open Payment Stack.