IG6 is advancing its downstream graphite processing strategy across Aus and EU

✓ Earthworks and civil construction to commence on Collie graphite micronising facility.

✓ Binding JV agreement signed with Italian chemical manufacturer ALKEEMIA to develop graphite hub in EU

✓Targeting ~20ktpa capacity, both operational during H2 2027

https://t.co/G8cWr5MI3d

$GLN update is legitimately strong.

the line that matters most is buried in the middle: 'the company is currently undertaking an optimisation phase & has not yet achieved stabilised production'.

that's the whole market discount in one sentence. dyor. no financial advice.

Initial revenue from the sale of lithium chloride in the coming months‼️

Galan Lithium $GLN $GLN.AX

Added more shares this morning - we will see a rerating 🤘🚀

disclosure: $GLN is currently the only lithium stock i'd repeatedly keep buying into weakness. not 'cause the story is risk free. it isn't. this is a major de-risking step. the remaining risk moved downstream: rate stability, recovery, final concentration, spec & shipment.

💥 NEWS 💥: Q2 Metals Announces 2026 Summer Exploration Program and Project Development Plans for the Cisco Lithium Project $QTWO.V $QUEXF

Read the full update here 👇: https://t.co/IVkS02a7ta

site tours are underrated. they kill the 'middle of nowhere' cope fast. put the market on site, show the access & scale. then let the MRE do the talking. $QTWO.V

Galan Lithium

The trading halt is requested until the commencement of trading on Wednesday, 27 May 2026 or

earlier, pending the release of an operational update on the commissioning of Phase 1 production

at Hombre Muerto West.

$GLN $GLN.AX

the market keeps pricing every dfs like it's a completed operating history. it isn't. a dfs assumes the machine eventually behaves. commissioning is where you find out whether.

$GLN my questions at this point: does wet commissioning behave?

what recovery do they actually achieve?

how much licl concentrate is on spec?

how ugly is early ramp up opex at 4ktpa annualised?

how much working capital gets trapped before first shipment h2 '26?

With sulfur prices this high, the costs of processing lithium clays, oxide ores (copper, nickel, REEs) is going to BLOW OUT.

The smelting of sulphide ores produces sulphuric acid as a byproduct. The processing of oxide ores consumes sulphuric acid.

#LAC's Lithium America's Thacker Pass for example is going to do 40,000 tonnes per year of carbonate in phase 1. They've stated a 2250t/day sulphuric acid plant, which is 821,250 tonnes of acid per year.

So each tonne of carbonate could require 20.5 tonne of sulphuric acid per tonne of Li₂CO₃. That's about 6.8 tonnes of sulphur.

Using the Chinese futures price of US$1050t, that's US$7140t worth of sulphur per tonne of Li₂CO₃.

#LAC will most likely source their sulphur internally. American fertiliser companies during Q1 paid US$488/t for molten sulfur, which is $3318 per tonne of Li₂CO₃. I'd imagine its higher now looking at the Chinese price.

Spodumene uses 50-60% less acid. Food for thought. I love spod.

'but there's plenty of supply coming'. sure. capital has a way of exposing which tonnes are real & which ones are just conference slide decoration. the buyer is paying now for future australian spod instead of waiting for the miracle cargo from every overhyped pegmatite on the internet. this deal says the quiet part out loud: downstream doesn't want bedtime stories.

not much time today. so just a few quick thoughts about $QTWO $QTWO.V. this part matters.

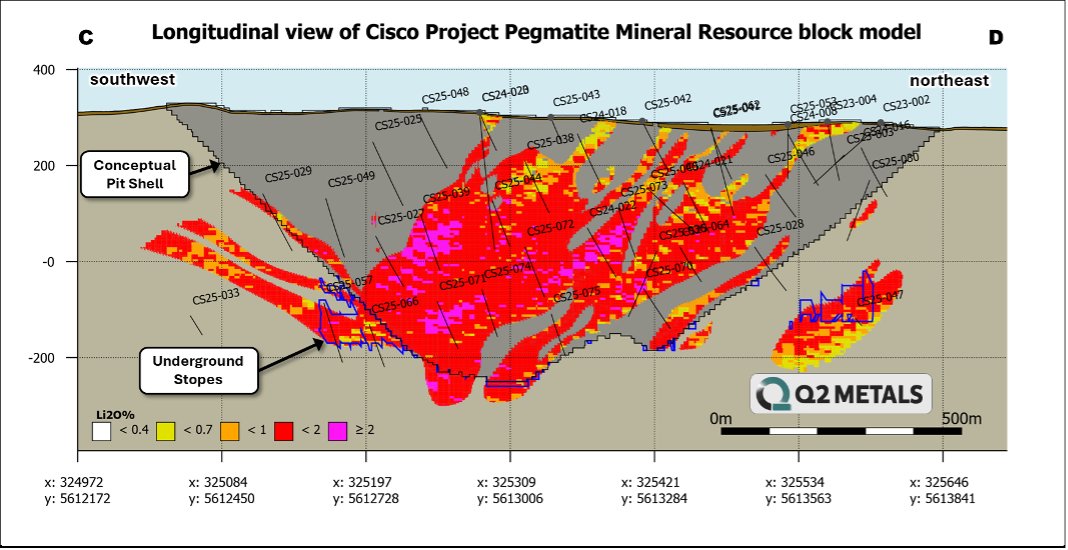

a single connected system wins 'cause it kills the silent value leaks that show up later as operational surprises. coherent geometry is margin insurance. you're mining a plan, not chasing pockets & blending mistakes. that reduces the probability you end up designing the plant for the worst case, then paying that CAPEX/OPEX forever. cisco's model is explicitly framed as one continuous principal body, true thickness up to ~450 m/~1.8 km strike/drilled to >600 m & still open.

it also wins on scheduling physics. the more 'patchwork' your deposit, the more your mine plan turns into a stockpile management job. stockpiles are working capital. working capital is dilution. dilution is spec drift. spec drift is pricing power loss. a coherent, thick body gives you a shot at stable feed, stable head grade, stable fines curve, stable spec. nobody pays a premium for big. they pay a premium for big that behaves.

why it's already more underwritable at this stage vs a lot of early peers: you've got an actual mre & it's constrained by conceptual pit/ug shapes, w/ cut offs tied to a stated price deck. 295 mt @ 1.36% Li2O inferred (270 mt pit @ 0.40% cut off & 24 mt ug @ 0.70% cut off), w/ the constraints explicitly based on US$1,500/t sc6 (6% basis/fob bécancour). that's not economics, but it's already past the global tonnage headline w/o rpep filter phase.

then the boring but paid part: location reduces the number of heroic assumptions you need before you even get to engineering. they're stating 6.5 km to the paved billy diamond highway & ~150 km to the matagami railhead. plenty of early stage projects are 'big' on paper & still die on access/timelines/logistics friction. fewer moving parts makes the whole thing easier to underwrite.

the milestone stack is explicit: they're already talking updated mre later this year/baseline environmental studies/advanced metallurgy & a pea targeted '27. that's why it feels more investierbarer even w/ inferred tonnes: you can map the gates, you can price the risks & you're not guessing what the next 18 months is supposed to look like.

dyor. no financial advice.

💥NEWS: Q2 Metals Announces Inferred Mineral Resource Estimate on the Cisco Lithium Project with 295 Million Tonnes Grading 1.36% Li2O $QTWO $QTWO.V $QUEXF #Lithium

Read the full press release here 👇: https://t.co/NnYWvaGTZJ

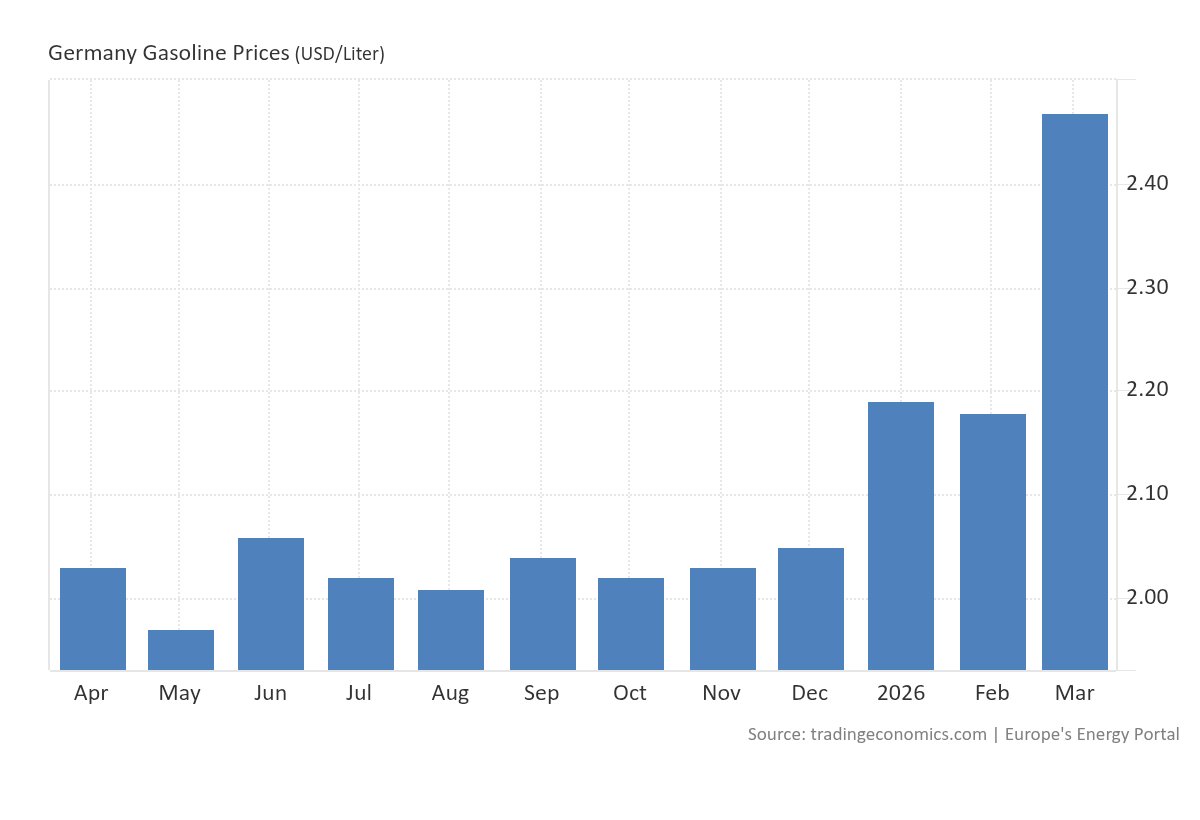

the part i enjoy most isn't being right. it's watching the same people who couldn't be bothered to care about the scenario suddenly talk about it like an unfortunate act of god. no. this was a visible chain: chokepoint stress, damaged flows, sticky risk premium, germany's tax stack & consumer squeeze. nothing mystical about it. & we're still early. the first move is at the pump. the uglier part comes after it bleeds into everything else.

same barrel. different tax stack. different pain threshold. at $194-276 brent, germany isn't dealing w/ an oil move. it's dealing w/ a consumer squeeze that turns political fast. the uk gets squeezed hard. the us still feels it, but from a much lower all-in base.

europe treats an energy shock like a fairness debate instead of a throughput problem. tax the producer. regulate the symptom. subsidise the voter. then act surprised when none of it fixes supply.

germany already burns extra fuel today 'cause the state let core infrastructure drift into congestion, bottlenecks & reliability problems. that is not theory. the council of economic experts says the poor condition of transport infrastructure is increasingly causing motorway congestion. in addition traffic delays rose in ~77% of german urban areas in last year (source: inrix global traffic scorecard).

so before the next shortage is even fully priced, part of the fuel bill is already being wasted by policy failure at home.