„I have no quarrels with this point of view, which animates old-time value investing, but this perspective comes with a cost in terms of investment choices. Investors who are wedded to never buying money losing companies or never paying more than twenty times earnings for a stock will end up with portfolios of mature (and declining) businesses. If that is their comfort zone, the strategy is perfectly defensible, but they should dispense with complaints about never being able to find high growth stocks to invest in or critiques of others who find these stocks attractive, notwithstanding the weak numbers.“

From @AswathDamodaran

Thank you!

This has quietly been a miracle month in medicine.

In the last 5 weeks we’ve got news on:

- retatrutide, the triple agonist GLP-1 from Lilly, basically melting fat and body-wide inflammation at record levels

- RevMed’s new pancreatic cancer drug showing unprecedented abilities to extend life

- small trial of a one-and-done PCSK9 gene editing therapy for slashing LDL cholesterol

- Mayo’s AI-assisted radiology showing vastly improved cancer detection

- this new therapy for metastatic solid tumors

This stuff is at varying levels of evidence. Retatrutide is ~100% on its way, other stuff needs more clinical trial data. But put it together and we’re maybe on the verge of majorly reducing the mortality of heart disease and cancer, the two leading causes of death in America.

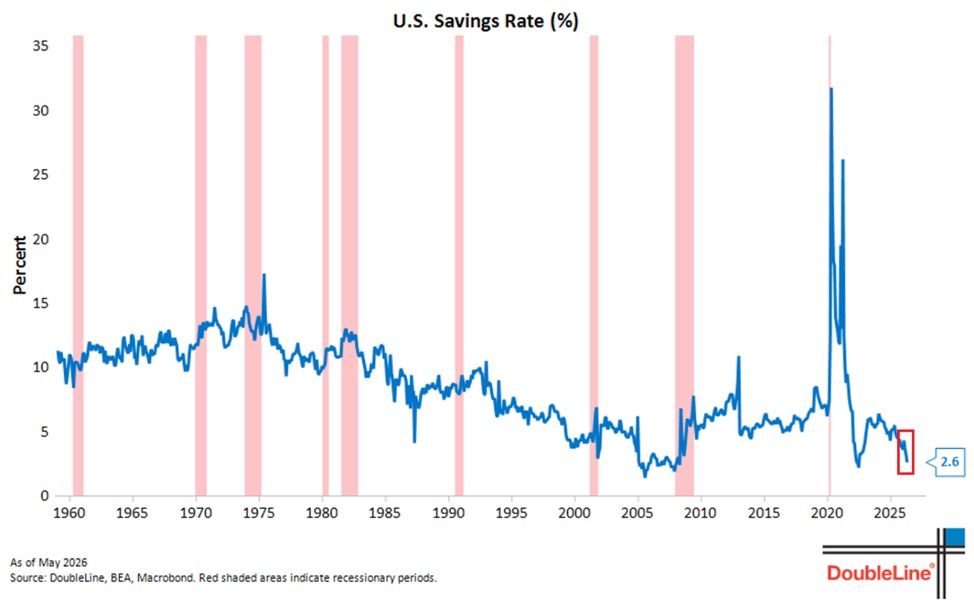

BREAKING: The US personal savings rate fell -0.6 percentage points in April, to 2.6%, the lowest since June 2022.

This marks the 3rd consecutive monthly decline for a cumulative drop of -1.7 percentage points.

This is also the 2nd lowest reading since April 2008.

This comes as consumer spending surged +5.7% YoY in April, outpacing personal income growth of +2.5% YoY, the widest gap since 2022.

This also marks the 12th consecutive month that consumer spending growth has outpaced income growth.

Put simply, rising costs of living are increasingly forcing consumers to cut into their savings to keep up.

American households are running out of savings as inflation takes its toll on their budgets.

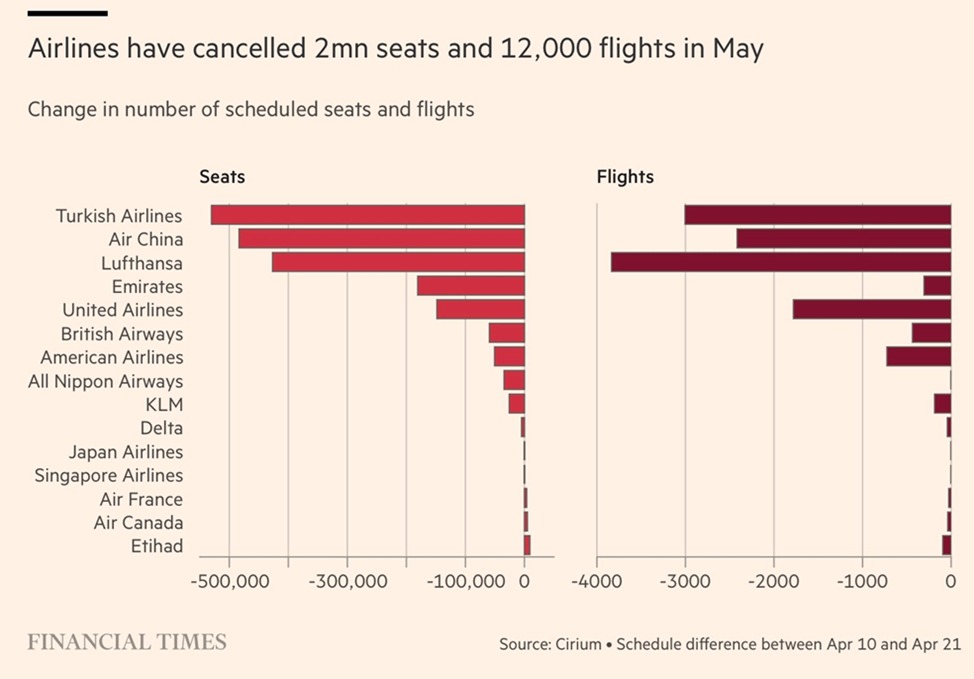

Global airlines are cancelling flights at an unprecedented pace:

Airlines have cut 2 million seats and 12,000 flights worldwide from their May schedules over the last 2 weeks, reducing the total available seats to 130 million.

This comes as jet fuel costs have DOUBLED since the Iran war began, forcing carriers to cancel unprofitable routes, switch to smaller aircraft, and raise ticket prices.

Turkish Airlines and Air China account for the largest seat reductions, cutting ~520,000 and ~490,000 seats, respectively.

Lufthansa leads in flight cancellations, at ~4,000 flights in May alone, with the airline having removed 20,000 flights from its schedule between May and October.

Meanwhile, Gulf carriers, including Emirates, Etihad, and Qatar Airways, are still operating well below pre-conflict capacity, as the closure of Gulf airports has disrupted ~33% of all European journeys to Asia.

Singapore and Tokyo airports asked carriers not to add extra services to limit jet fuel use, and Vietnam introduced jet fuel rationing.

The global aviation shock is spreading.

Bill Ackman and Warren Buffett have different opinions about the current market…

“Then we don’t do anything. Of the 60 years I’ve been in the business, 5 have been real juicy.”

– Warren Buffett

$BRK.B

Fair point. I agree $10.75 is painful. My question is whether a Beam-like debt deal was actually available to Intellia on acceptable terms, given the remaining regulatory/commercial risk. ATM would have been cleaner, but slower and could have capped the stock. So for me the issue is not only “equity vs. debt,” but whether management sacrificed too much price for certainty.

This essay by @alexolegimas is the best thing I've ever read on why AGI won't lead to mass unemployment. A compelling argument backed up by substantial empirical data.

GOLDMAN: MARKETS MISREAD FED AS OIL SPIKE FUELS RATE FEARS

Goldman Sachs says investors are overestimating the chance of Fed rate hikes as oil prices surge.

Brent crude above $115 has fueled inflation fears and pushed traders to price a more hawkish Fed, but Goldman argues this reaction is overdone and out of line with history.

The bank points to 1990, when markets expected tightening after an oil shock — but the Fed ultimately cut rates as growth weakened.

Bottom line: markets are pricing higher rates, but slowing growth could force the Fed in the opposite direction.