I don't see anything that can justify the $META valuation gap with peers.

It has higher revenue CAGR estimates for the next 3 years than the hyperscaler peers:

$AMZN: 13.90%

$MSFT: 17.20%

$GOOG: 19.10%

$META: 20.70%

Yet, it's trading at the lowest forward earnings multiple at 18x.

It's already generating ROI from AI capex in its core businesses in the form of higher conversion rates and impressions. This is the hard part; no other hyperscaler is seeing ROI from AI capex beyond their cloud businesses.

If $META ends up with excess compute, it can easily monetize it at a significant premium to its cost of ownership in the current demand environment.

So, $META is actually the best-positioned company to see ROI from AI capex.

I don't see how its discount is justified given this.

People will look at this a few months down and say $META was obvious.

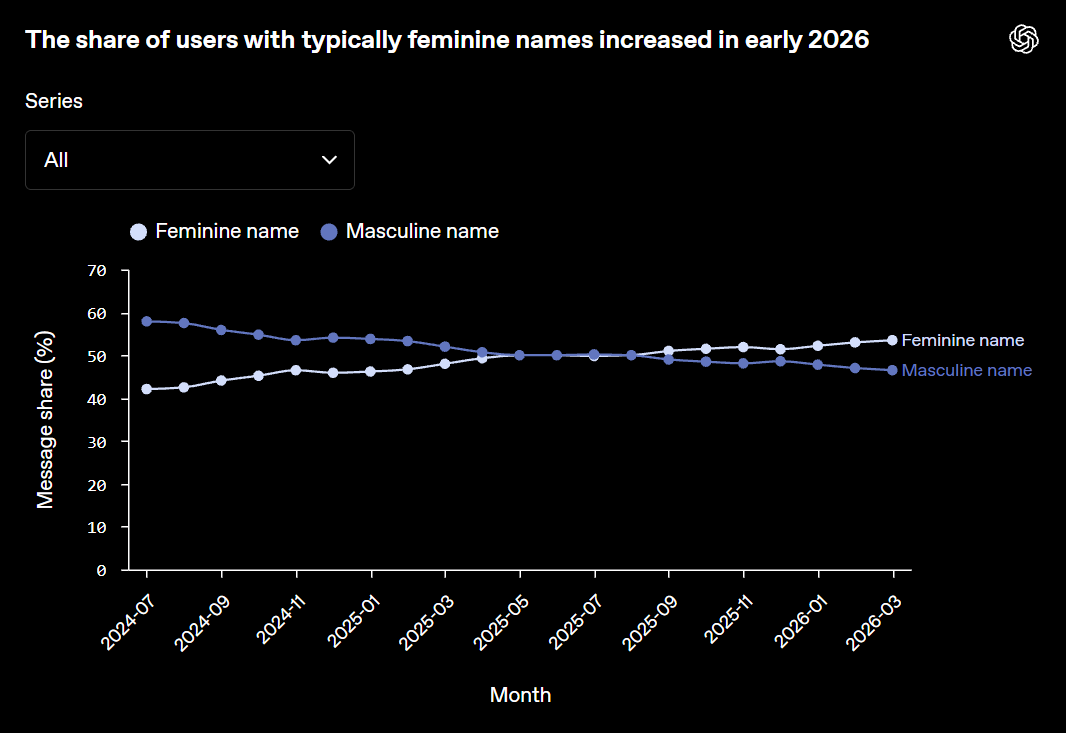

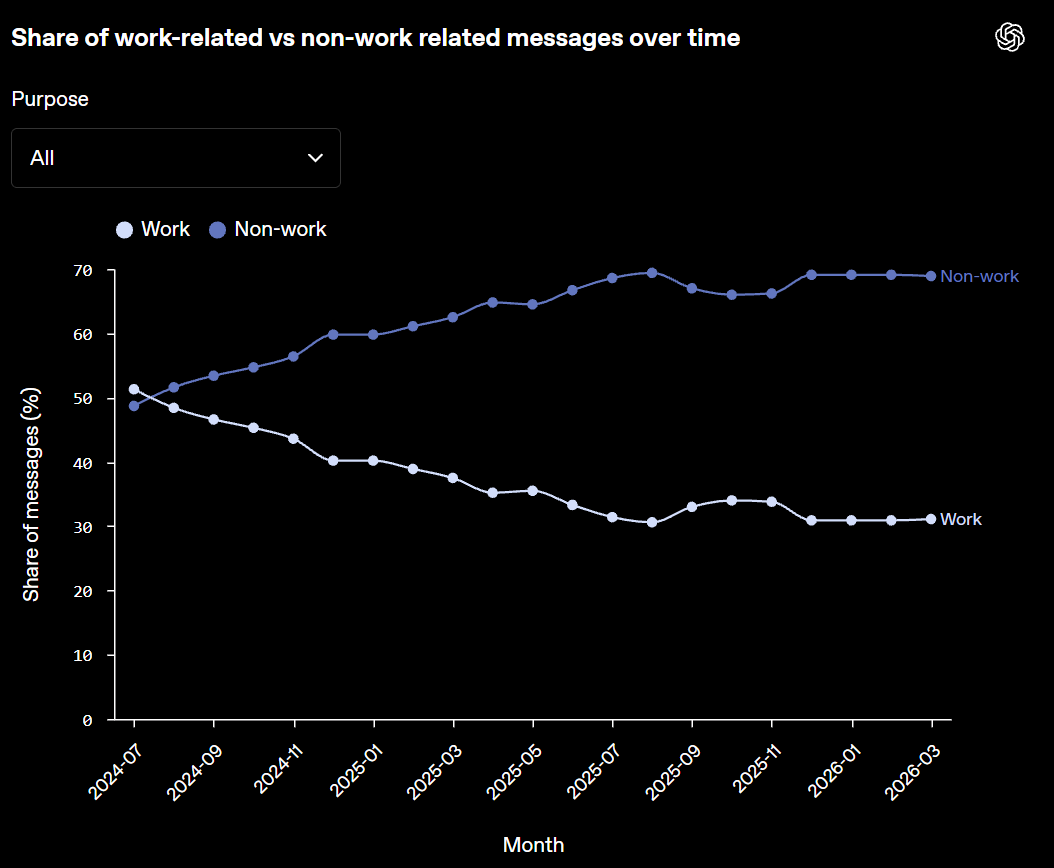

Women now use ChatGPT more than men. And the proportion of non-work usage is now much larger than work usage, with the main use-case seeming to be answers/advice. https://t.co/9LvzWIfRUP

@elonmusk companies at their best don’t win the game; they change the rules through scale.

He makes all-in bets not by making rational short-term business decisions, but by starting with the desired end state and working backwards.

#ElonMusk#MentalModels

The more the economy runs through the market, the more a market decline stops being a market event and becomes an economic one. So the market gets backstopped. Which makes it more central. Which makes the next decline scarier. And around it goes.

Every old house has that one wall the inspector tells you not to touch, because the whole place is sitting on it. That's what the stock market became. So the real question isn't whether stocks are cheap or expensive. It's that we made it so important it can't be allowed to break.

Nvidia CEO Jensen Huang: “Four years ago, five years ago, Nvidia was spending about $10, $15 billion dollars a year in Taiwan. Now we’re spending $100, going to $150 billion dollars in Taiwan each year.”

$NVDA $TSM $AMD

This is absolutely incredible.

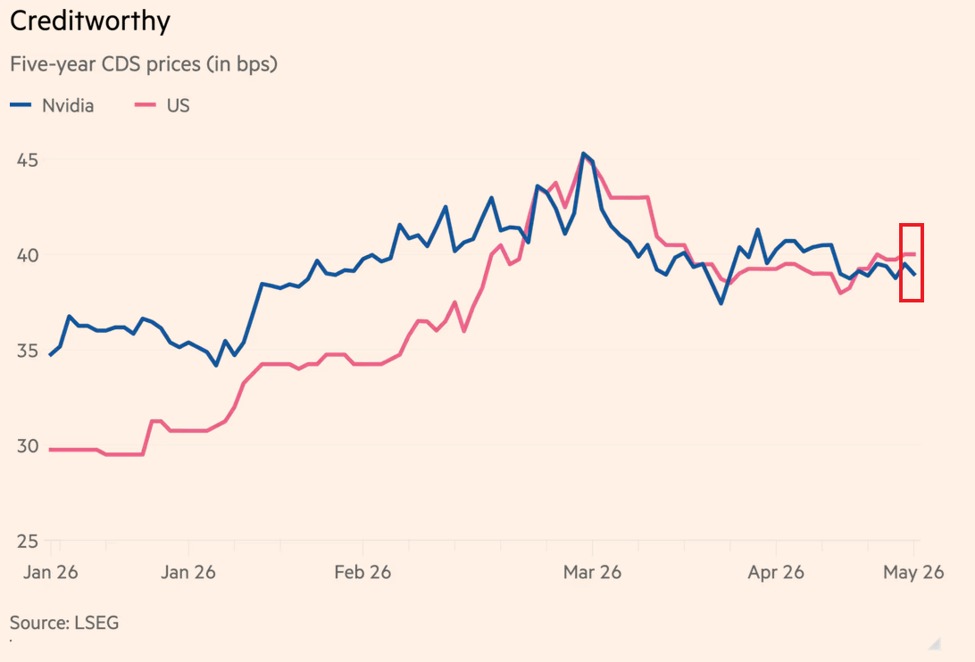

Investors now perceive Nvidia to be as creditworthy as the US government.

Nvidia's $NVDA, 5-year credit default swap (CDS) is trading at ~38 basis points, slightly below the US sovereign CDS, at 40 basis points.

In other words, markets consider the world's largest company to be less likely to default on its obligations than the US federal government.

This comes as in FY2026, Nvidia carried only ~$8.5 billion in total debt against ~$10.6 billion in cash and generated nearly $100 billion in free cash flow, giving it one of the strongest balance sheets of any company in the world.

Even if Nvidia's earnings dropped -90%, it would still rank among the 100 most profitable companies in the world.

Markets are treating Nvidia as one of the safest companies on the planet.

. When it comes to #AI, distribution and transaction costs are still free — the two preconditions for Aggregators — which means that the winners should be those with the most compelling products.