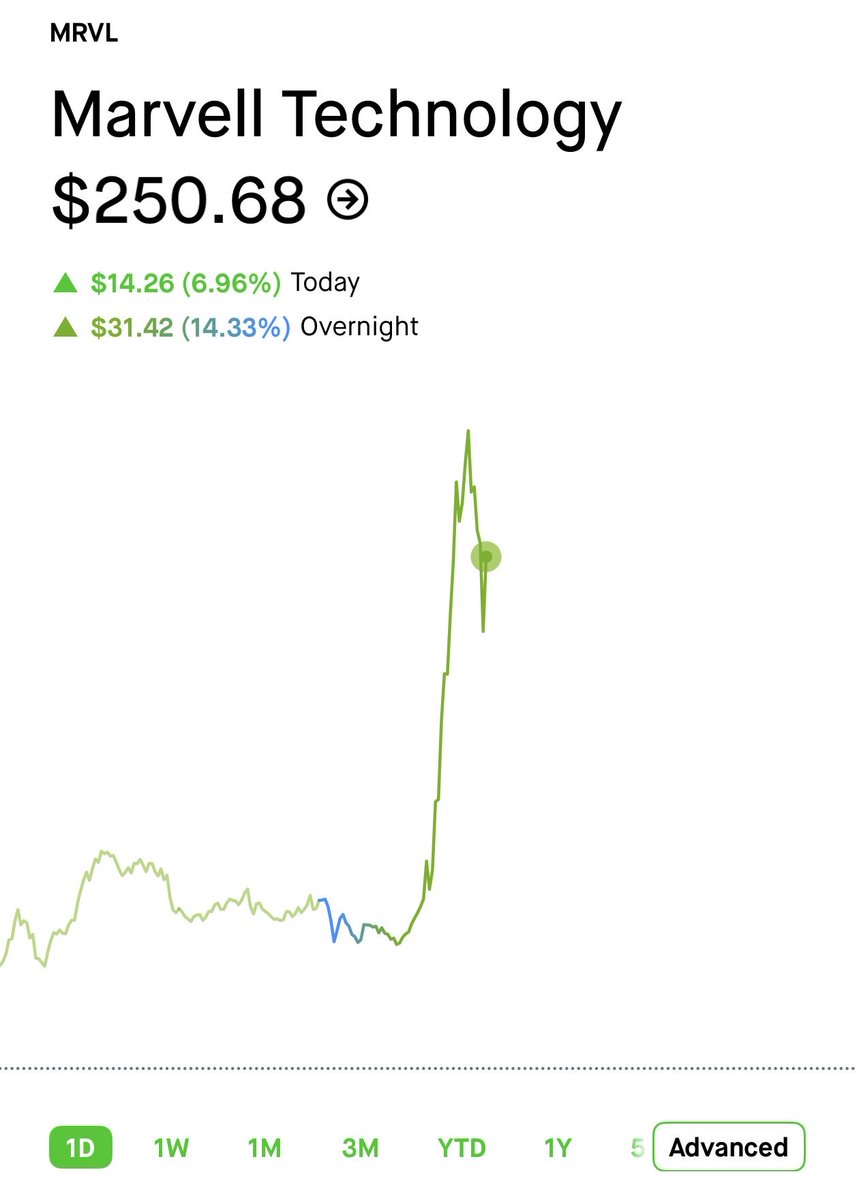

$NVDA Jensen Huang:

“ $MRVL the next $1T company ladies and gentlemen “.

Marvell is currently trading at $191B.

I have positions in Marvell… but how much faith do we have in Jensen for the 5x?

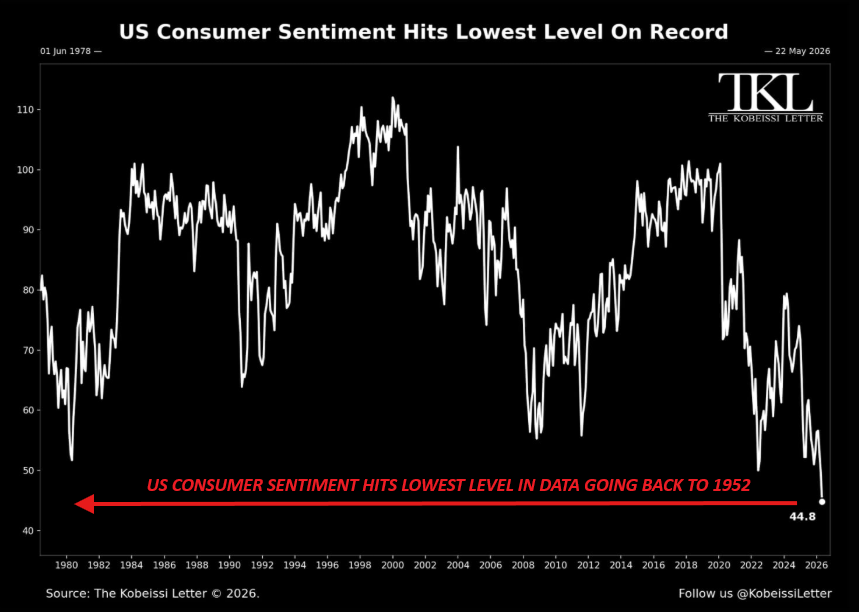

BREAKING: US Consumer Sentiment officially falls to its lowest level on record in data going back to 1952, down another -10% last month.

Consumers now see inflation rising to 4.8% over the next 12 months.

This puts the Consumer Sentiment index down -21% since February 2026, before the Iran War.

Not even the 1980s saw Consumer Sentiment this low.

$PLTR currently testing resistance. Last long position is well in profit. Monitoring today’s earnings for a potential trend reversal breakout; otherwise, eyeing a move lower toward $100.

As for 3x brrrs these levels:

1. $SIVE

2. MSSCORP (6830)

3. Auros (322310)

Are my best guesses. Here's my thought process:

1. $SIVE: I genuinely do see them being $10B+ next year, they're the literal bleeding edge for CPO lasers alongside $LITE and $COHR.

At a $1.3B MC... For likely mapping:

Photonics: $AMD CPO, $MRVL Celestial CPO, $JBL 1.6T, Lightmatter, Ayar, ALChip, GUC, O-Net (ELS), $POET.

For Space + Defense: Golden Dome via $YSS, $RTX / $ERIC / Bae Systems.

Silicon Photonics: $AAPL (Apple Watches).

This is just a stupid amount of customers and it's still increasing.

They can always TAM expansion downstream through IP acquisitions or vertically integrate to speedrun $LITE's $60B MC one day once they get more funding.

2. MSSCORP (6830): CPO monopoly over inspection at ~$1.2B.

100% monopoly over CPO yields, $TSM, $AMAT, $NVDA, $LCRX, $INTC, and others are all likely customers.

"The company’s goal is to seize a 90 percent share of the CPO inspection market"

This basically means 100%, they just don't want antitrust. If they defend their monopoly and CPO ramps, can easily see this worth ~$5B-$9B from $1.2B

3. Auros (322310): Samsung / SK Hynix supplier at ~$210M for Hybrid Bonding Metrology.

Basically pure play on two products:

-> HBM4 / HBM4e / HBM5 cycles, that $KLA had a monoply over for IR metrology.

---> Getting qualified now likely in Samsung factories, H2 volume ramp est. Sk Hynix likely qualifying too when they upgrade to hybrid bonding.

-> Thin-film thickness measurement.

---> Getting qualified now, with "major domestic chipmaker" (either Samsung/Sk hynix), targets mass supply this year.

They've been developing for the past decade, only to volume ramp two products from years of qualification H2 this year.

Seems extremely likely to 3x to $630M if they switch to volume ramp, feels like an undiscovered gem in the Korean market?

Of course, not sure how they play out and this is all speculative but high confidence supply chain mapping.

But off the top of my head these three that I own are the most likely ones at this level.

BREAKING: Microsoft stock, $MSFT, falls -5% after announcing that its OpenAI license will now be nonexclusive and it will no longer pay revenue share to OpenAI.

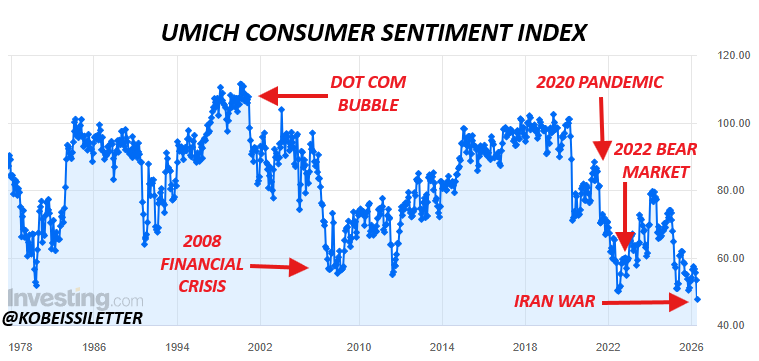

BREAKING: The UMich Consumer Sentiment index officials falls to a record low of 47.6 for the month of April amid the Iran War.

Not even March 2020 or 2008 saw consumer sentiment levels remotely near as low as they are right now.