🚨 IMPORTANT UPDATE

✅ Today I made a very hard decision. I sold a large chunk of my Tesla $TSLA shares.

✅ I added more $MU & $SNDK with the proceeds.

✅ It’s all about Opportunity Cost ( make sure to read the post below)

✅ Tesla is being overshadowed by SpaceX and it looks like it will be acquired/ merged at a low valuation.

✅ Elon said Robotaxis would be in half of US cities at the end of 2025. Here we are after one year of the Robotaxi launch and there’s not much traction. Also Elon said that Robotaxis won’t be a significant source of revenue anytime soon.

✅ Optimus is going to be huge but we don’t know when. Again read my Opportunity Cost post below.

✅ Tesla was a super huge position for me and after today’s move it sits at #3 after $MU and $SNDK.

@cperruna Portnoy is biased to a very particular type of pizza .. cracker or over done pizza .. doesn’t care if the sauce is bland etc .. those r his only 2 criteria..mind is blown why anyone cares what he thinks

Data from Altimeter:

Morgan Stanley now projecting $GOOG to spend $299B on CapEx next year up 57% from $190B this year

The biggest revision to previous estimates by a country mile.. $MSFT. CapEx est. revised from $178B to $276B in 2027 🤯

Hyperscaler CapEx now est. >$1.1T

One thing most investors are missing about the $SPCX IPO:

At a $2.1T valuation, institutions own just 6.8% of the company, or about $143B worth of stock.

The valuation debate is obvious. The positioning debate is not.

If SpaceX remains eligible for broader index inclusion and institutional ownership eventually moves toward 15-20%, that's hundreds of billions of dollars of potential demand still ahead.

Near term, flows may matter more than fundamentals.

After listening to Google, Amazon, Microsoft and Meta earnings call:

The AI buildout just got bigger. Combined 2026 capex now tracking $700B+

- $GOOGL: raised to $180-190B (from $175-185B). Cloud +63%, backlog doubled to $460B

- $META: raised to $125-145B (from $115-135B). Pure internal spend, no cloud resale

- $AMZN: $200B maintained. AWS +28%, fastest in 15 quarters. TTM FCF collapsed to $1.2B

- $MSFT: $31.9B in Q (below $34.9B est). Demand still > supply. AI run-rate $37B (+123%)

Theme: Every CEO said the same thing - capacity constrained, not demand constrained.

Winners downstream:

GPUs/Accelerators: $NVDA, $AMD, $AVGO, $MRVL, $ARM

Custom ASIC/Silicon: $AVGO, $MRVL,

Foundry/Equipment: $TSM, $ASML, $AMAT, $LRCX, $KLAC, $ICHR, $UCTT

Memory/HBM: $MU, $HBM (SK Hynix), $WDC, $STX

Connectivity/Interconnect: $CRDO, $ALAB, $MRVL, $AVGO

Networking/Switching: $ANET, $CSCO

Optical/Transceivers: $COHR, $LITE, $CIEN, $FN, $AAOI

Power Generation: $CEG, $VST, $NRG, $TLN, $OKLO

Power Equipment/Grid: $VRT, $GEV, $ETN, $PWR, $HUBB, $NVT, $BE, $FPS

Cooling/Thermal: $VRT, $MOD

Cabling/Components: $APH, $GLW

My take: demand is still accelerating, supply is still catching up - this cycle likely runs longer than most expect.

@cperruna Everywhere I’m traveling people seem to rely on Google Translate more n more … I’m guessing AI makes it even more user friendly and I think most people are lazy and would rather use that then $duol. I imagine $duol will always have a niche user base but growth…

$RDW (March 18, 2026-daily chart)

Watch the momentum bars at $10.19 and $10.96—these are serving as temporary resistance right now. A decisive close above them could ignite more bullish momentum.

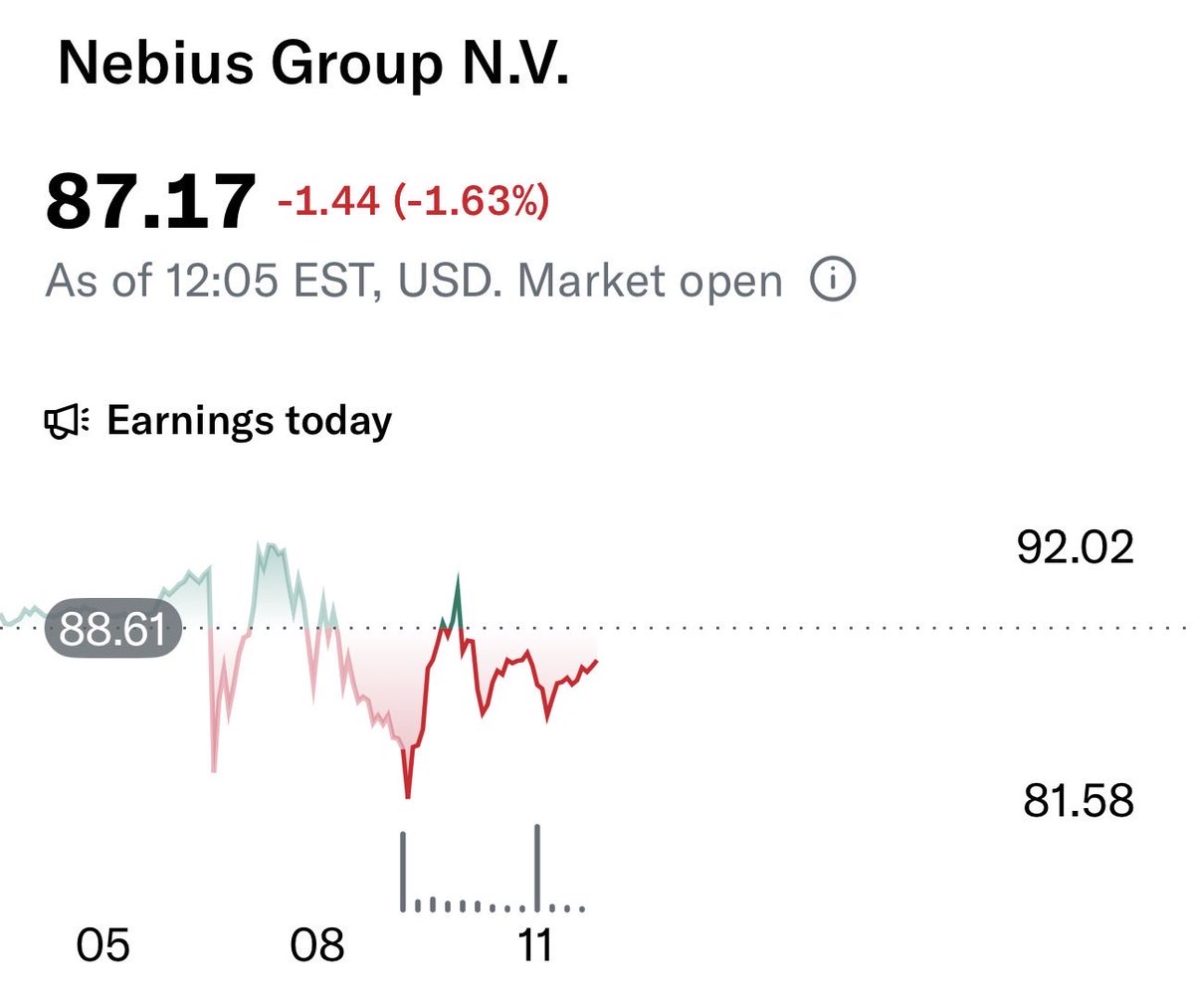

Earnings day and $NBIS is red.

Down ~1–2%… that’s it?

After +500% revenue growth, $1.25B ARR, Microsoft + Meta live, and first positive operating cash flow?

If that’s the market’s reaction to those numbers, it tells me positioning was loud… but conviction might be louder.

Let’s see who blinks first.