A lot of the monopoly conversation around capital intensive industries in Nigeria suffers from one consistent failure. People refuse to distinguish between concentration created by political protection and concentration created because the underlying environment was too difficult for most people to build in at all.

There are industries where concentration is clearly linked to policy choices. Import restrictions remain in place for years, regulatory access becomes uneven, incumbents continue compounding advantages long after the original developmental objective has been achieved, and new entrants struggle to compete on equal terms. I believe those are legitimate competition concerns and they should be discussed honestly.

But there is another category that gets flattened into the same conversation even though the economics underneath it are completely different.

Sometimes a market becomes concentrated because the underlying environment is so difficult that very few people are willing to build at all.

Industrial financing in Nigeria is expensive. Infrastructure is unreliable, power supply is unstable, currency risk is significant while regulatory timelines shift constantly. Large projects can take years before they generate meaningful returns. In many cases, business owners are forced to finance infrastructure the country itself failed to provide.

A 45% operating margin in a developed economy with stable infrastructure and low financing costs will tell you something about pricing power. The same margin in an environment where a business man financed independent power, absorbed years of currency devaluation on dollar obligations, carried 2x digits borrowing costs, and spent years building before scale was achieved may simply reflect the actual cost of taking industrial risk in Nigeria. This is why I find parts of the Nigerian financial community’s analysis dishonest. Not technically wrong in every detail but dishonest in what it chooses to ignore.

The people making many of these arguments understand Nigerian risk extremely well. These are professionals who spend their careers pricing risk, benchmarking returns, and allocating capital. Yet when you look at where domestic capital actually goes, very little of it enters long term productive industry.

Most of it prefers liquidity. Government paper, money markets, short duration fixed income. When equity, it gravitates toward asset light models where the distance between capital deployment and exit is short and the infrastructure risk belongs to someone else. The sectors now being critiqued for concentration are, without exception, the same sectors this capital has spent years avoiding.

Nigeria attracted tens of $B in inflows, yet only a very small fraction consistently goes into long term productive investment. The same finance guys criticising concentration have repeatedly chosen not to deploy their own capital into sectors carrying the heaviest industrial risk.

Because if returns in these sectors were genuinely excessive relative to the underlying risk, competing capacity should emerge over time. Capital markets do not usually ignore obvious excess returns indefinitely.

The truth is that many people privately understand how difficult industrial capital formation is in Nigeria even if public commentary sometimes ignores that fact.

None of this means every dominant operator is innocent. Regulatory capture exist in Nigeria. Some sectors absolutely benefit from policy structures that should have expired long ago.

Concentration built on regulatory capture deserves scrutiny and should get it. Concentration that exists because almost nobody was willing to finance a power plant before building a factory, absorb a decade of currency risk on dollar obligations, and wait years for the returns to materialise, that is a different conversation entirely. The analysis only becomes useful when it knows which one it is looking at.

Watch Western countries become more and more protective of their markets. US already has 100% tariff on Chinese EVs.

The de-industrialization Africa experienced, they are poised to too, just not prematurely for them.

Shall we blame it on “inefficiency”?

China’s industrial strategy threatens hundreds of billions in output across advanced economies, risking a hollowing out of their industrial capabilities, according to the largest US business lobby https://t.co/3PjxOhGstM

Mr. "Gafaaru", congratulations on your appointment o. Some of us have significant holdings in Cadbury, and we have been patiently waiting for the cookies to be delivered. We wish you the best.

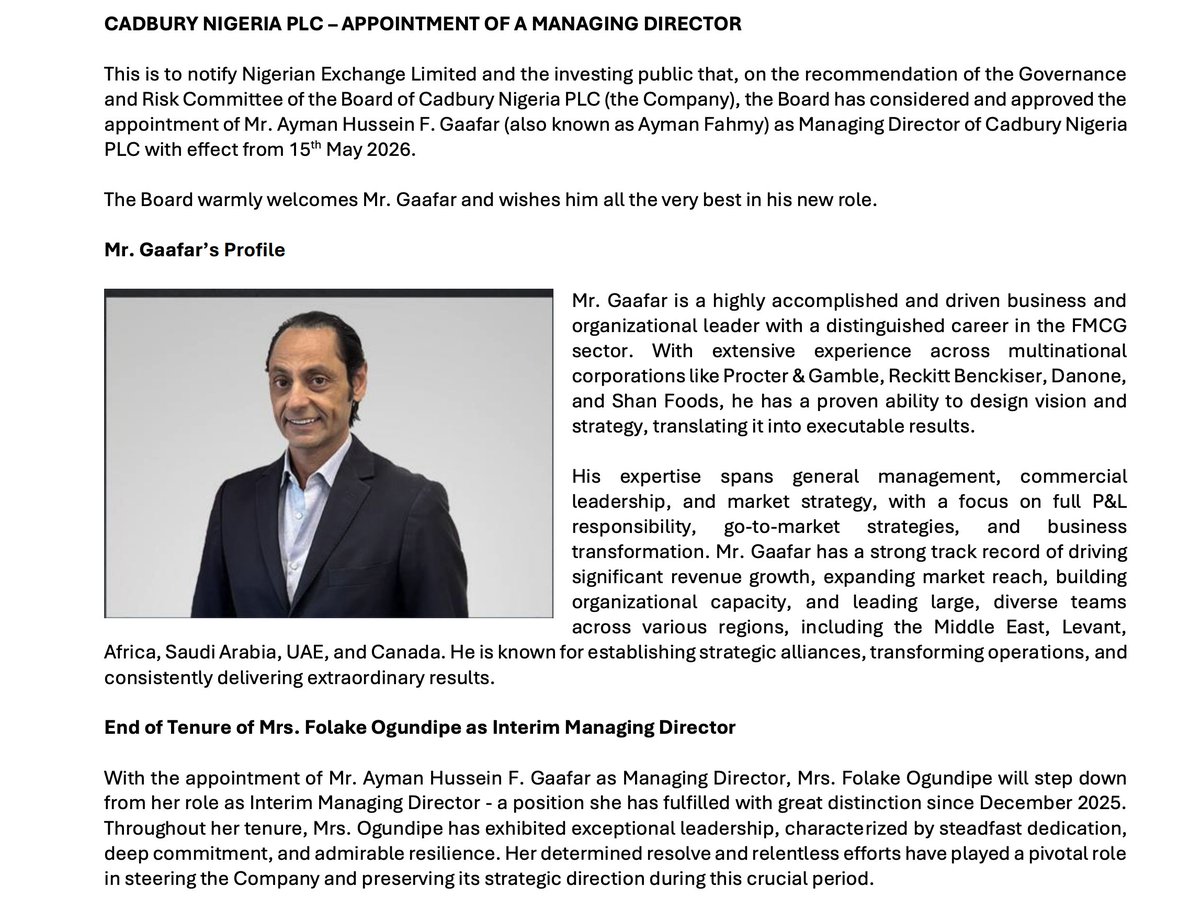

Ayman Gaafar is a proper FMCG-lifer, with 27+ years deep in the sector. He is a Mechanical Engineer by training from the American University in Cairo, but his entire career has been commercial.

He did two decades at Procter & Gamble, and folks will argue that they are the gold standard for grooming FMCG commercial talent globally. At P&G, he held roles across the Middle East, Europe, North America, and Africa.

He later rose to Vice President of Sales (a salesman, I am seeing?) for the Arabian Peninsula & Pakistan (a big deal sorta because that particular region is considered an important one for P&G, hence, they don't just send anyone there).

From P&G he moved to Al Safi Danone as SVP. He later went to Reckitt Benckiser as General Manager for Developing Markets across Africa and the Middle East (okay, okay, I see someone with exposure to African markets, doing commercial operations).

So my sense is that "Gafaaru" should be able to execute, relying on his P&G foundation (P&G is known for producing executives who are rigorous about data and go-to-market discipline). Two decades there should mean something.

I see that "Gafaaru's" career has been almost entirely in "difficult" or "developing" markets (Middle East, Pakistan, Africa). These are markets where brand strength is not enough to rely on; you have to navigate currency volatility, supply chain complexity, regulatory uncertainty, and price-sensitive consumers.

Career progression across top companies like P&G, Reckitt Benckiser, and Danone tells me that "Gafaaru" might have some stuff in him.

So what do I expect from "Gafaaru"?

Given his background, I'd expect him to focus on a few things... Route-to-market optimisation is likely priority one. I would need him to attack this head-on.

Margin discipline across the value chain is another likely focus area. He will probably also look at the product portfolio. I mean, Cadbury Nigeria has strong brands (Bournvita, Tom Tom, Buttermint.. they tried to launch biscuits but it failed miserably), but the question is whether the portfolio mix is optimised for the current Nigerian consumer environment.

(By the way, I once tweeted something about Cadbury here: https://t.co/F2xDyRPc5U)

I think it's a good appointment. His profile seems solid for this role. We'd see.

I entered Berger Paints just on May 4, and it is already looking like one of the positions that will fund my Aqd Nikkah (already sitting at +42.18% MTD).

Ijebu-Ode ya. 😁

When market is up; Your position brings money

When market dumps; you see money making bargains

There is not one bad scenario in the market

its win:win

doesnt matter when u start, so far its not a get rich quick scheme for u

The world’s wealthiest individuals are builders: manufacturers, producers, creators of goods.

Nigeria is no different. The money sits with those who make things.

And the logic is linear: wealth is simply the exchange of value for money at scale.

You either produce a good, own an IP, or deliver a service people cannot do without.

A nation that commits to manufacturing commits to wealth. Not eventually. Inevitably. Because the world must pay you. You control the supply. You set the terms.

Importers are middlemen. They move wealth they don’t create it. Every container that lands in Apapa is a transfer of Nigerian money to a foreign producer.

The countries that figured this out are rich: China, Germany, South Korea, the US.

Production guarantees your sovereignty.

Yes! God bless my Manager that gave me the first chance. Quite unfortunate we fell out, but I will forever be grateful to her. My best wishes wherever she is.

Along the way somebody was gracious enough to take a chance on you because you had the right attitude even if you didn't have the skills to match. It's only right you extend the same grace to someone else.

When your fx reserves are perpetually under pressure, your banks auditioning for ‘World’s Most International Balance Sheet’ isn’t a priority.

Face home first. Build domestic resilience before exporting capital.

The problem is complex, and this brushes them a bit. I once made a thread about it:

https://t.co/piJ3FqDxtE

Make una sha come buy stocks so that we brokers can make money.

The reason Blanchard > Mankiw imo is that the former represents the mindset I love seeing in analysts.

A mindset that interrogates assumptions, avoids authority bias, and thinks in trade-offs, not absolutes.

Students once walked out of Mankiw’s class.

Repressive actions against street vendors increase unemployment, disrupt supply chains, and create social instability.

Projects like SA’s Warwick Junction Urban Renewal show what works.

But excusing lack of state capacity seems better for y’all.

Of course, everyone likes the AI version. Beautiful, clean, orderly. The question isn't whether we WANT that; it's HOW we GET there.

You can't photoshop poverty away. Those street sellers aren't in the AI render because AI doesn't model survival economics.

We've done this loop for >30 years: evict → vendors return → repeat. 79.6% failure rate.

Again, read: https://t.co/abQvcHGEQA

If you want the clean AI vision to be real and lasting, you need economics to match the aesthetics.

Otherwise na just render.