One of the things that makes @SpaceX so valuable is how valuable it is. The Cursor acquisition costs materially less in dilution because of SpaceX’s high valuation.

SpaceX’s ability to do economically, strategically, and technologically accretive acquisitions is an important component of its value.

There is enormous value inherent to a company with a high value particularly when it is controlled by an entrepreneur that the most talented people want to work for and partner with.

Value begets value.

Talent begets talent.

Whether any of the neoclouds have durable moats is a great debate, but these types of generalities aren’t helpful on the short side. We want to hear why you think the multiple GWs in the backlog for a $CRWV won’t come to fruition or will hit a wall thereafter, why you think GPU useful lives will shorten rather than extend, why the $NVDA relationship doesn’t mean much, why the focus and operational rigor to run these at the highest levels of efficiency don’t really matter, and why multiple things coming together like the supplier relationships, scale, customer trust, financing relationships, software / operational expertise, and focus don’t come together to create a lower cost to serve and high barriers to success for new entrants and/or a destructive, structural price war among incumbents.

Jim Chanos is short the neoclouds.

"It gets back to the point that we've made to clients that anybody that's just a middleman in this chain, like the data center guys are either as rights or equipment leasing companies should never trade at higher multiples than the company that controls their supply."

$CRWV $NBIS $IREN

Seems negative for software incumbents when $MSFT as the biggest of the bunch is riffing on how things should be in a perfect world rather than how they are…at least for a while (absent draconian frontier lab regulation)

Putting the timing of this Satya / $MSFT piece together with the circumstances around Anthropic-Fable ban makes it seem like the non-Ant crowd that is currently behind the true frontier (Fable) is making a coordinated effort to slow Ant down. To me, this seems like a plea for open source (and more control over the agentic layer) to win before those using the frontier including the labs themselves can lap the incumbents or current also-rans. This happens if open source catches up naturally or if Ant is slowed down unnaturally.

All of this seems like many are saying in their own ways that Anthropic is trending towards becoming the most valuable company in the world.

And suggesting tech from Anthropic or others will go back in the bottle or neutered prematurely represents a fundamental misunderstanding of the laws of capitalism.

Investors want to feel smart and different. Allocators also want to feel smart and different. Product-market fit hardens around smaller, “lesser known” companies. More investors then move based on where they see product-market fit. The cycle continues.

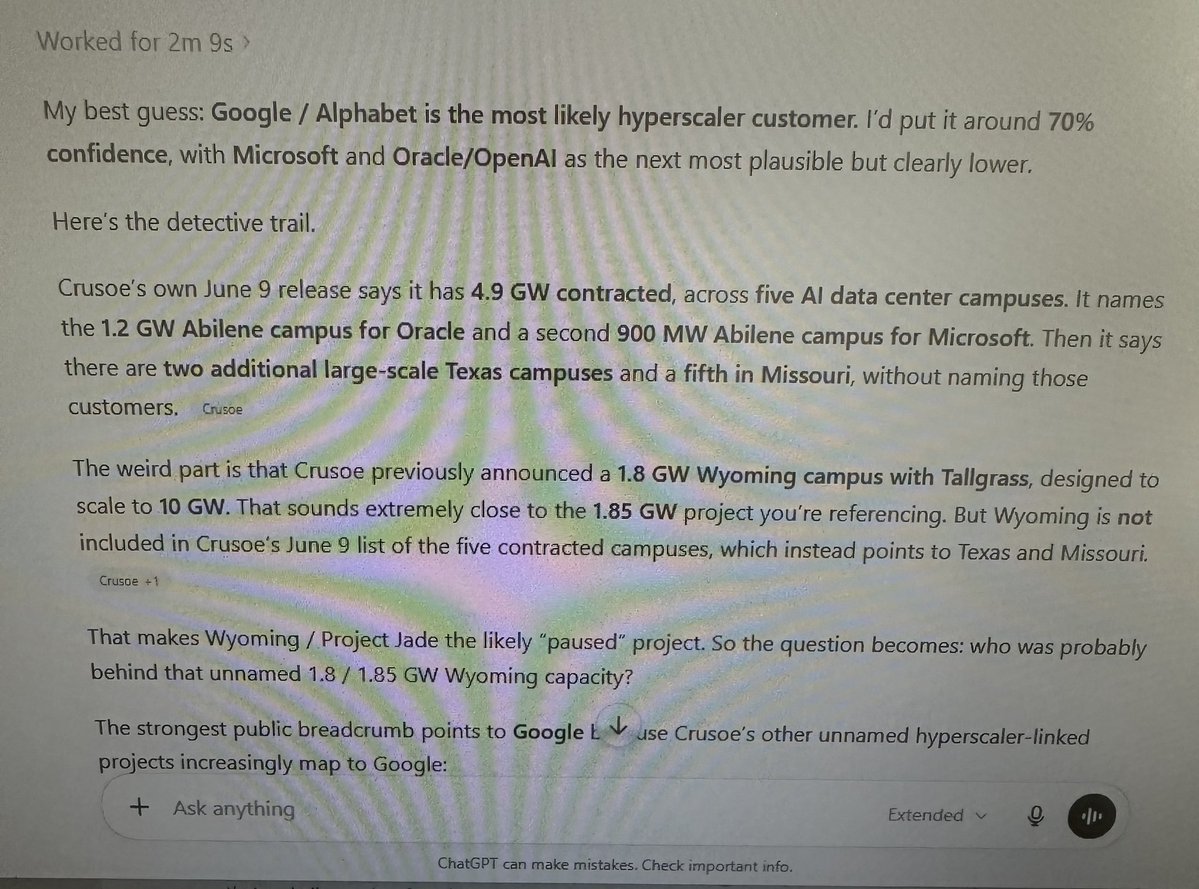

Least surprising news of the day is each of ChatGPT, Claude, and Gemini names a different suspect as the unnamed Crusoe hyperscaler customer that delayed…with confidence…and maybe w bias….

*DATA CENTER DEVELOPER CRUSOE PAUSES AI PROJECT IN WYOMING

Crusoe, a data center developer for hyperscalers, announced they’re pausing development activities of a 1.8GW campus in Wyoming at the request of its customer.

“Crusoe was working with Blackstone Inc.-backed energy company Tallgrass to develop a 1.8-gigawatt campus in Cheyenne, Wyoming, for an undisclosed tenant. “At the request of our customer, Crusoe has paused its development activities” on the site, the company said Tuesday in a statement.””

Customer likely a hyperscaler hitting the pause button. At least partially being attributed to tech dump

$META is one of the best case studies of the emotional business and the behavioral dynamics it creates.

Zuck will run down any new “platform” bet where losing could be existential and winning could be glorious.

Each platform bet has been larger with more at stake. Each time most existing SHs have left and most interested SHs have stayed away during the ramp phase.

Each new bet brings new risks while each prior bet brings more insight into management’s approach to capital allocation and balance.

The emotional business is the enemy of those who need smooth rides but can be the friend of those who appreciate long holding periods.

Ideally you want capex to be linear and operating profits to be an exponential

Meta setting up nice to do the opposite! That sucker ain’t 18x. Prob much higher true multiple

Great company and mngmt but incomplete framing by Leandro. Shows how $MELI and some of their peers are a bit tone deaf at the moment.

The market does a pretty good job of allocating capital, and right now (I think correctly) the market is rewarding token-led investments, not promo-led investments.

Doesn’t have to be either/or but need to show token-based progress like new UXs.

$MELI management always shares so much value. I hope Leandro does more of these interviews and shout out to @Couch_Investor for making this one. Here are some key insights that most investors are unaware of for $MELI from this interview.

Two metrics prove how early Mercado Libre actually is in its growth cycle despite its $86B valuation. Leandro admitted they are only at 1% to 2% of their ultimate goal in using AI to connect Mercado Pago and Mercado Libre data for hyper-personalized consumer experiences. We can potentially see new verticals spin up over the next few years just in this domain alone. Even with their aggressively growing $15B credit book, they are still only the 6th largest credit card issuer in Brazil. The 5th largest competitor is still three times their size! This confirms they have an immense amount of runway left before they hit a market share ceiling.

Wall Street models focus heavily on existing market growth, but Mercado Libre has a massive, unactivated pipeline within its current footprint. They only recently launched credit cards in Argentina in August, and the product is not even available in major markets like Chile or Colombia yet. Beyond their current active zones, there is a combined population of ~130M people in secondary Latin American countries where Mercado Libre currently has very little presence. This represents an untapped market the exact size of a "second Mexico" that is entirely ready for future ecosystem expansion. There is not a single analyst pricing this in.

Management is highly skeptical of corporate acquisitions. Leandro noted that mergers and acquisitions fail to create value half of the time, so their default strategy is to build their technology and networks in-house. They will only buy an external company if there is a severe "strategic urgency." For example, they acquired a Brazilian network of local mom-and-pop shops purely to establish instant drop-off points for apparel returns, which saved them years of organic development time. Otherwise, they do not rely on buyouts for growth.

In Latin America, roughly half of the economy is informal. This means citizens do not have traditional payroll stubs, making it very difficult for standard banks to accurately assess their risk. Mercado Libre’s competitive alpha is that they do not underwrite random people. Instead, they issue credit exclusively based on proprietary behavioral data gathered from within their own closed-loop marketplace. Because they can see exactly how a user buys and sells on the platform, they have a level of granular insight into the real economy that traditional financial institutions cannot match.

What is the absolute positively BEST non-Bam offer the Heat can make for Giannis? Because I genuinely truly cannot believe this is what Milwaukee's going to get, even when I say you don't get great return for a player like Giannis and hear there's confidence it gets done after the Finals.

Herro, Jaquez, one of Jak or Jovic, and picks? THAT'S what you get? For GIANNIS? No stud prospect with star potential, no picks with great longterm value after the lottery changes?