🚨 THE DEATH OF THE DOLLAR IN EAST AFRICA? 🇹🇿 💵

If you think dedollarization is just a theory, think again. Tanzania just officially locked the U.S. Dollar out of its domestic economy.

As detailed in the legal breakdowns the Bank of Tanzania (BoT) has completely banned the use of USD and other foreign currencies for local transactions. The one-year grace period for existing contracts officially ended this month (June 2026).

Here is what is now strictly ILLEGAL inside Tanzania:

❌ No USD Pricing: You cannot quote, display, or advertise prices in USD or EUR. Everything must be in Tanzanian Shillings (TZS).

❌ No Foreign Cash for Local Deals: Accepting or forcing payments in foreign currency for local goods/services is a criminal offense.

❌ No Rejecting Shillings: Refusing to accept the local currency is officially a punishable crime.

Why does this matter:

This isn't a temporary rule—it is fully codified under Government Notice No. 198. The government is aggressively moving to protect and strengthen the Tanzanian Shilling (TZS) by forcing every single local business, hotel, and supplier to drop the greenback.

Is this the blueprint for the rest of the continent? 👇🏿

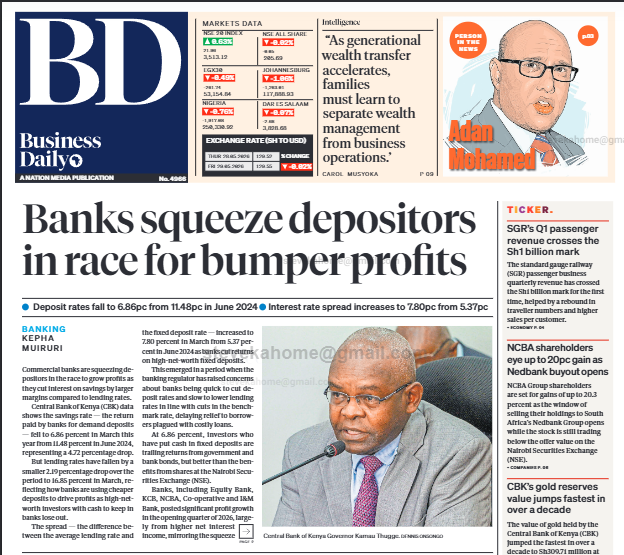

When it comes to your money, the bank is NEVER your friend — you're competitors.

You both want the same shilling, just on opposite sides of the balance sheet.

You want a higher rate on your savings. The bank wants a wider spread: the gap between what it earns lending money out and what it pays you to hold yours. And right now, that gap is winning.

The latest CBK data tells the whole story. Average deposit rates have collapsed to 6.86% from 11.48% a year earlier, while the interest rate spread has widened to 7.80% from 5.37%.

Banks are paying depositors less and keeping more. That isn't an accident — it's the business model. It's also why your savings and fixed deposit accounts pay so little, and why only depositors locking up large sums for long tenors can negotiate anything better.

This is the gap money market funds have stepped into: a) An MMF pools savings into short-term instruments — Treasury bills, bank placements, fixed deposits and high-quality commercial paper — and passes the blended yield back to you. Because it sits at the short end of the curve, that yield typically tracks, and often beats, what a bank offers on savings or fixed deposit accounts.

b) It doesn't discriminate by size or tenor. Whether you invest KES 100 or KES 10 million, you earn the same daily-accruing yield, which moves with prevailing short-term rates. No negotiation required.

c) Liquidity is the clincher. Most funds let you withdraw within one to three working days with no early-exit penalty, and you keep every shilling of interest accrued to the day you exit.

One honest caveat: Unlike bank deposits, MMFs aren't covered by the KES 500,000 KDIC guarantee — your protection is CMA regulation, an independent custodian and diversification, not a state backstop.

For parking short-term cash, that trade-off still favours the MMF for most savers.

The real twist sits with the banks now running asset management arms. Are they steering clients into low-yield deposits, or into their own MMFs and fixed income funds?

The incentives don't point the same way.

As an investor, the maths is simple: if your bank can't beat the prevailing MMF rate net of tax and fees, where you park your money answers itself.

Finance Bill 2026 wants to end anonymous crypto trading in Kenya.

Under the proposed bill:

- Kenyan crypto exchanges must identify their users

- File annual reports to KRA

- Share users’ transaction history with KRA

Kenya shall also enter agreements with foreign countries to compel offshore crypto exchanges to share data of Kenyan traders with KRA.

Meaning: Crypto anonymity is ending in Kenya.

SHOCKED THE WORLD 🤯

@SStricklandMMA defeats Khamzat Chimaev by Split-Decision to become the NEW middleweight champion of the world!

[ B2YB @HSpecialSurgery ]

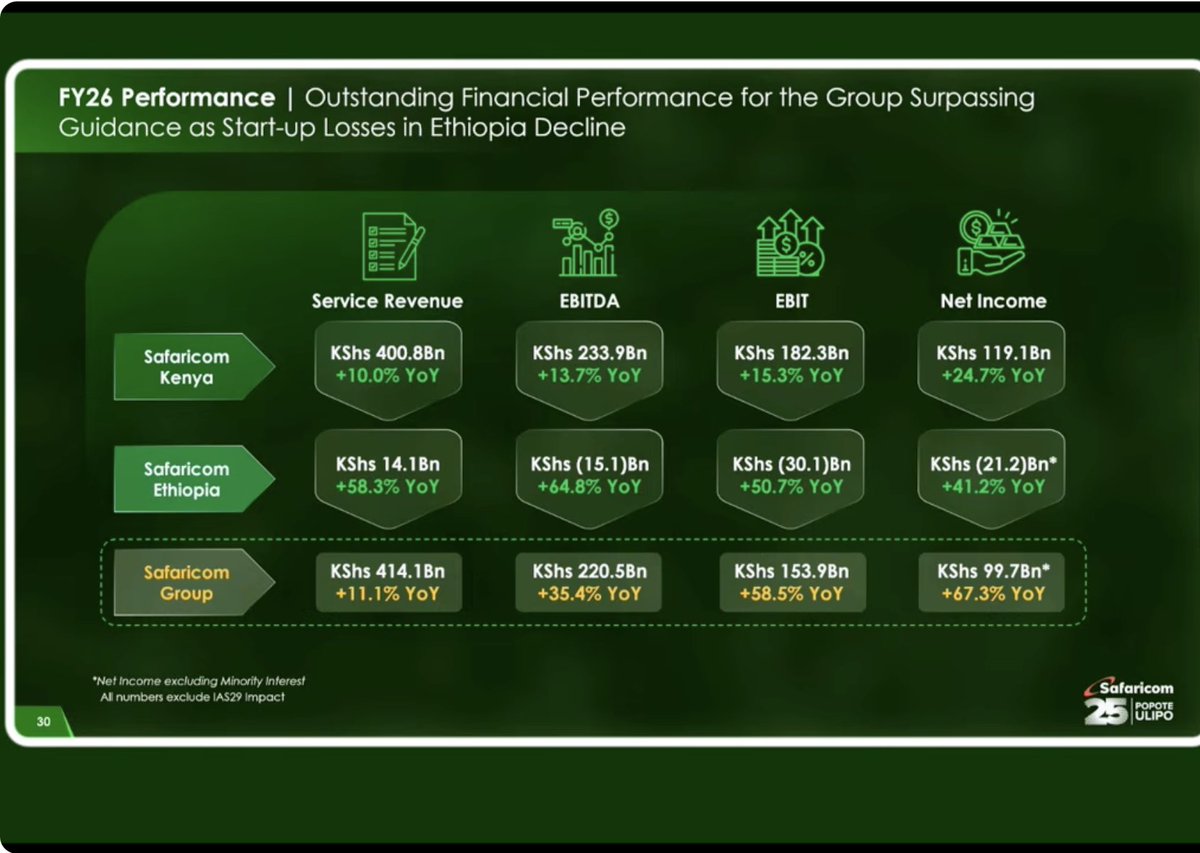

Safaricom full year 2026 Earnings macro level numbers

Group:

· Net Income: up 67.3% y/y to Kes 99.7 billion

· EBIT: up 58.5% y/y to Kes 153.9 billion

· EBITDA: up 35.4% y/y to Kes 220.5 billion

· Service Revenue: + 11.1% y/y to Kes 414.1 billion

Kenya Business:

· Net Income: up 24.7% y/y to Kes 119.1 billion

· EBIT: up 15.3% y/y to Kes 182.3 billion

· EITDA: up 13.7% to Kes 233.9 billion

· Service Revenue: up 10.0% y/y to Kes 400.9 billion

Ethiopia Business:

· Net Income: up 41.2% to (Kes 21.2 billion)

· EBIT: up 50.7% y/y to (Kes 30.1 billion)

· EITDA: up 64.8% to (Kes 15.1 billion)

· Service Revenue: up 58.3% to Kes 14.1 billion

🚨BREAKING: On Friday afternoon, an artificial intelligence coding agent powered by Anthropic's Claude Opus 4.6 deleted a company's entire production database in nine seconds.

The company is called PocketOS. It is a software platform that powers car rental businesses. The database contained months of customer bookings, vehicle records, and operational data that small rental car companies relied on to run their businesses.

When the database was deleted, all of the backups were deleted with it.

Three months of customer reservations evaporated.

The High Court yesterday made a very important decision. When you take a loan from any lending institution, the amount of interest accrued cannot exceed the amount you received from the institution (principal). Meaning if you borrow kshs. 100,000, you cannot pay more than kshs.200,000 in total. This is good news to many Kenyans. Tag that one lending institution wajionee habari kamili.

The High Court of Kenya has made a very important ruling for borrowers across Kenya. It reaffirmed the in duplum rule, which means that once a loan goes into default, the interest charged cannot exceed the original amount borrowed.

In simple terms, if you borrow KSh 100,000, the interest cannot go beyond KSh 100,000, meaning the total recoverable amount should not exceed KSh 200,000.

This is a major win for many Kenyans who have long suffered under runaway loan balances inflated by excessive interest and charges.

The judgment sends a clear message that lenders cannot use default as a licence to trap borrowers in endless debt.

Ever wondered why some people own multiple properties…

…but are still broke?

This is how it happens.

A client was about to take a KSh 35M loan to build rental units.

On paper, it looked perfect.

Then we did the math.

A thread 🧵

I condemn the attack on Senator Godfrey Osotsi in the strongest terms.

Political violence is a crime.

It must be treated as one.

Those responsible must face the full force of the law.

The Houthis have eventually joined the Iran war. If this leads to a disruption in the Red Sea, it is going to complicate economic matters. Iran has also announced the closure of the Strait of Hormuz, which until now was effectively closed. 🧵

![ufc's tweet photo. SHOCKED THE WORLD 🤯

@SStricklandMMA defeats Khamzat Chimaev by Split-Decision to become the NEW middleweight champion of the world!

[ B2YB @HSpecialSurgery ] https://t.co/eIfkTv334n](https://pbs.twimg.com/media/HH7p7H9bsAAjCIs.jpg)