Chart of the Day: Borrowers Just Got a CPI Head Fake

Borrowers, the recent softer core CPI data gave the bond market a short-lived break.

It did not fix the long end of the Treasury curve.

The 10-year Treasury yield dipped, then moved higher again.

The bond market’s message: Inflation matters, but growth matters more right now.

The chart shows two things:

• Inflation expectations have stayed fairly steady

• Investors are demanding more return even after accounting for inflation

Plain English:

Borrowing costs are not rising only because investors fear inflation.

They are also rising because bond investors think the economy can withstand higher rates.

That keeps pressure on fixed-rate debt, refinance sizing, interest rate caps, float-to-fixed interest rate swaps, and DSCR.

A cooler CPI print can help for a few hours. Maybe a day, if the bond market is feeling charitable.

But strong jobs data, sticky services prices, AI spending, and resilient growth keep the Fed focused on whether it needs to sit tight or tighten again.

The 10-year Treasury is still near 4.50%.

The 30-year Treasury is still near 5.00%.

Those are not friendly levels for borrowers hoping one soft inflation report would do the heavy lifting.

The takeaway:

The bond market is not trading like one soft CPI print ends the rate problem.

It is trading like the economy may be too strong for long-term rates to fall much.

Borrowers should model that before the next “CPI saved us” rally disappears before lunch.

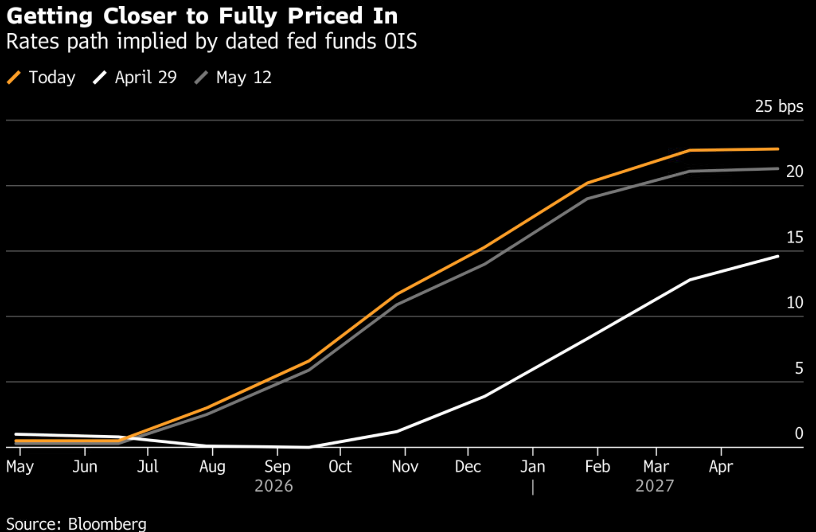

Chart of the Day: Warsh’s Inflation Gauge Could Cool Rate Hike Talk

The Fed’s main inflation focus has been core PCE.

Core PCE removes food and energy, then measures the rest of the basket. Useful, but still vulnerable to big moves in categories like housing, insurance, travel, and medical costs.

The Dallas Fed Trimmed Mean PCE takes a broader filter. It looks across the full basket, cuts out the most extreme price moves on both ends, and focuses on the middle of the distribution.

Kevin Warsh, the new Fed Chair, reportedly prefers that approach.

The latest Dallas Fed Trimmed Mean PCE showed inflation running at 2.35% over the last 12 months, much closer to the Fed’s 2% target than the regular PCE readings.

Translation:

• Core PCE still looks uncomfortably high.

• Trimmed Mean PCE looks closer to target.

• Same economy. Different inflation lens.

For a Warsh-led Fed, that difference could matter.

If recent inflation pressure looks more like a relative-price shock than a broad inflation spiral, the case for a Fed rate hike weakens.

For borrowers, this is where the inflation debate stops being academic. A Fed leaning harder on trimmed-mean inflation may sound less eager to hike, which could lower Treasury yields and refinancing assumptions before the next loan committee meeting.

The next inflation reports will help determine which inflation story carries more weight within the Fed.

Is trimmed mean inflation a better signal, or just a more convenient one?

Chart of the Day: Peace Could Push Yields Higher

Markets love a peace headline. Borrowers should read the fine print.

A truce with Iran would likely take pressure off oil prices. Lower oil prices reduce recession risk and give markets more confidence that economic growth can hold up.

Then the bond market may do what it does best: ruin the mood.

Stronger growth expectations can reduce demand for safe-haven Treasuries and push investors toward stocks, credit, and other risk assets. Bond investors may also demand higher yields if inflation remains above target while the Fed sits on its hands.

That is how peace can push Treasury yields higher instead of lower.

For borrowers, the recent rise in Treasury yields has already done some of the Fed’s work. Higher long-term yields tighten financial conditions by lifting fixed-rate loan coupons, pressuring asset values, and making refinancing harder.

Meanwhile, SOFR has been far more stable.

Since SOFR is tied closely to the Fed’s policy rate, a patient Fed can leave floating-rates steadier while fixed-rate debt gets more expensive.

That is why many borrowers are taking another look at floating-rate debt, especially 3+1+1+1 structures. Fixed-rate debt offers certainty, but that certainty now comes with more pain.

Oil is only part of the inflation story.

AI spending is becoming a macro force. Data centers need power, chips, cooling, memory, land, transmission, and massive capital budgets. That demand can feed into electricity costs, equipment prices, and long-term borrowing needs.

The market may stop pricing war risk and start pricing growth, inflation, AI capital demand, and Fed patience.

Bottom line? A peace headline may help oil. It may not save your refinancing assumptions.

What's your strategy for managing persistently higher long-term interest rates?

Chart of the Day: AI Will Be the Next Yield Shock

If the Iran conflict fades, the rates debate may shift fast.

Less oil panic could reduce near-term Fed-hike bets and take pressure off the front end of the curve.

But the long end has another problem: AI is becoming a capital-demand machine.

Data centers, chips, power, cooling, transmission, and industrial infrastructure do not fund themselves with motivational quotes. They require debt, equity, energy, labor, and materials.

That matters for Treasury yields:

- The front end is still tied to the Fed, inflation data, oil, and the labor market.

- The long end is increasingly tied to real yields, Treasury supply, and the amount of money the economy needs to fund government deficits, corporate borrowing, and the AI buildout.

The chart shows why the U.S. setup is different. If oil risk fades, the U.S. inflation story may become less about imported energy shock and more about domestic capital demand.

Inflation expectations in the U.S. have not risen as much as in Germany or Japan. The U.S. exports oil and is less exposed to the direct supply-chain shock created by the conflict.

But AI adds a different kind of inflation risk. Not just chatbot hype. Actual demand:

• More chips and data centers

• More power, cooling, and transmission

• More corporate borrowing

• More competition for skilled labor

There is also a labor-market risk. If AI starts destroying jobs faster than it creates them, the Fed may worry more about employment and less about inflation. That could pull near-term rates lower.

Meanwhile, longer-term yields can stay firm if investors demand more real yield to absorb heavy Treasury issuance and a surge in private-sector borrowing.

That is how you get the annoying version of a steeper curve: Some relief up front. No party at the long end.

For borrowers, the risk is simple: peace headlines may boost the appeal of floating-rate debt, but they will not automatically fix expensive fixed-rate debt, float-to-fixed swap pricing, or refinancing math.

The next rates problem may be less about oil tankers and more about data centers.

Are your refi assumptions built for front-end relief and long-end pain?

Derivative Logic helps borrowers model that curve risk before it shows up in loan economics, hedge pricing, and capital decisions.

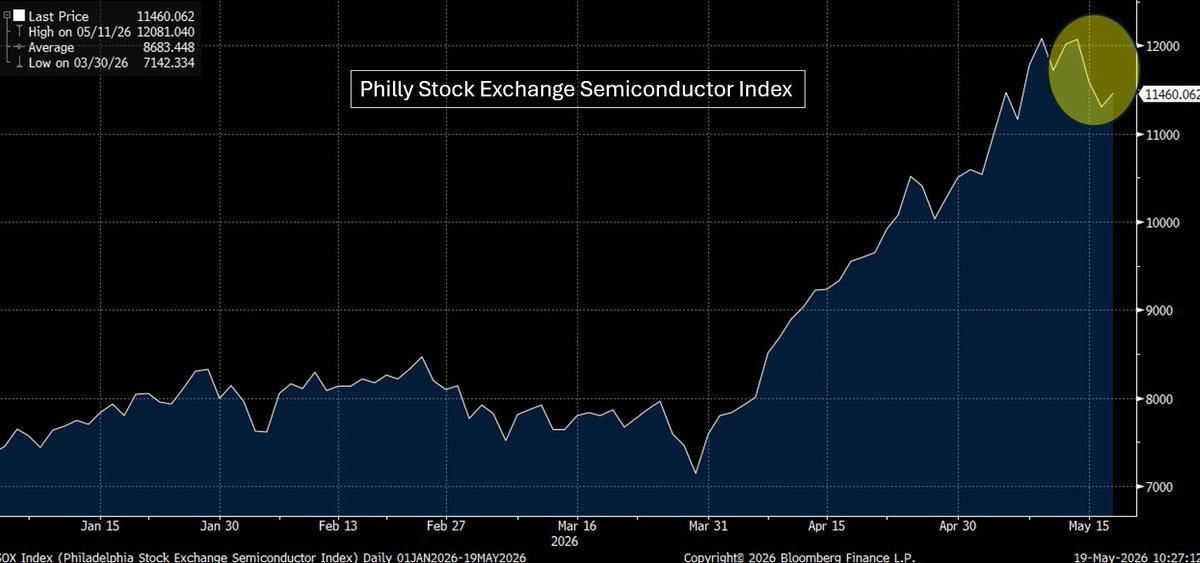

Chart of the Day: Higher Treasury Yields Are Starting to Bite

The cure for higher yields may be higher yields. When yields rise far enough, they stop describing the risk and start creating it.

The U.S. long bond yield is near a 19-year high. Cumulative rate-hike odds for 2026 are now above 80%. Rate traders have stopped treating another Fed hike as a punchline.

Oil is helping drive the reset. January crude futures have jumped more than 20% over the past month, suggesting markets are not pricing a quick de-escalation around the Strait of Hormuz.

Real yields are rising, too. Real yields are regular bond yields adjusted for inflation expectations. They show what investors expect to earn after inflation.

That matters because higher real yields hit valuations directly. They make future earnings worth less today and make safer income streams more competitive against stocks.

The warning light: The Philadelphia Semiconductor Index is already in correction territory, down more than 8% since May 1.

If yields move much higher, the next phase may be demand destruction, weaker earnings guidance, lower equity prices, and tighter financial conditions.

That is how rising yields can eventually plant the seeds of their own decline.

For borrowers, this is where the pain moves from the chart to the model: Higher yields can quickly turn into weaker refinancing economics, tighter credit terms, and less room for error.

Chart of the Day:

The Bond Market Is Repricing Before Inflation Finishes the Job

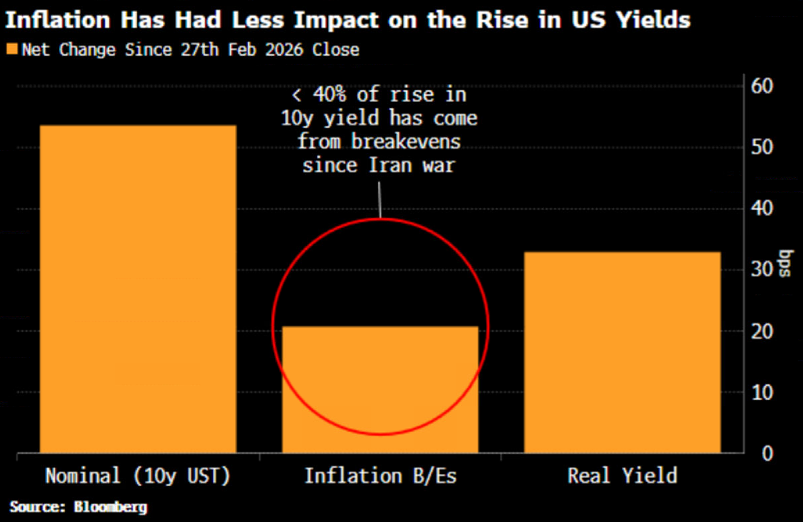

Treasury yields are rising again.

The 10-year Treasury yield is near its highest level in a year, and the uncomfortable part is what is driving the move.

Most of the rise has come from higher real yields. Inflation breakevens have done less of the damage.

Translation:

The bond market is already demanding more yield before it fully prices the inflation risk from oil, supply shocks, and geopolitics.

Borrowers waiting for lower rates just got another postcard from reality.

The next problem is term premium.

Term premium is the extra yield investors demand to own longer-term bonds when inflation, Fed policy, and fiscal risk become harder to price.

For borrowers, that can mean:

• Higher 10-year Treasury yields

• Less forgiving fixed-rate loan coupons

• Firmer float-to-fixed swap rates

• Expensive rate caps

• Refinancing assumptions getting marked to market

SOFR futures already imply a higher peak Fed policy rate than before the latest oil shock.

But inflation breakevens have not done much heavy lifting yet, which leaves room for more trouble.

If higher energy prices start feeding broader inflation expectations, the Treasury market may demand more yield from both sides:

• Higher real yields

• Higher inflation compensation

That is how “rates should drift lower” turns into “who approved this debt-service forecast?”

Borrowers waiting for rates to politely walk themselves down may want to look at this chart twice.

Derivative Logic helps borrowers quantify rate risk before it shows up in swap pricing, cap costs, loan coupons, and refinancing math.

What is your plan if the 10-year keeps rising before your refinancing window opens?

Chart of the Day: The Consumer Is Still Alive. Full Price Is Not.

April retail sales look fine on the surface. Underneath, the consumer is getting more selective, more price-sensitive, and allergic to full price.

Discretionary categories like apparel, personal care, furniture, and other non-essential spending are weakening. Online spending is holding up better, which tells you shoppers have not disappeared. They have just opened seven tabs, found a promo code, and decided gross margins can take a hike.

The message:

• Gasoline is eating more wallet share

• Discretionary spending is fading

• Bargain hunting is becoming a lifestyle

• Weak pricing power is now a problem

• Retailers priced for “resilient consumer” may be one earnings call away from reality

For the Fed, this is a bad tradeoff. Softer discretionary spending says the consumer is under pressure. Higher gasoline spending says inflation risk is still alive.

Time for rate cuts and confetti? Not exactly.

For rates, short-term yields may stay firm if inflation refuses to cool. Long-term yields may struggle to fall if energy keeps pushing inflation expectations higher.

For the U.S. dollar, the setup can still be supportive. If U.S. inflation risk keeps the Fed pinned while global growth worries rise, investors may keep treating the dollar as the least ugly shirt in the closet.

Bottom line: The consumer has not collapsed. But full-price spending is fading, margin pressure is building, and “resilient consumer” is starting to look like a lazy investment thesis.

(Chat source: Bloomberg Professional)

Chart of the Day: Markets Ordered Champagne. PPI Brought Pepto.

PPI just handed markets the bar tab.

Services inflation posted its biggest contribution to final demand PPI since late 2022. That matters because late 2022 was not exactly a spa weekend for risk assets. Back then, the Fed was tightening aggressively, yields were rising, and expensive money was breaking things.

Now markets are flirting with the same problem again.

Rate traders are moving closer to pricing a Fed HIKE early next year. SOFR futures yields are up. Two-year Treasury yields are back near 4%.

Meanwhile, equities have been partying like borrowing costs are someone else’s problem.

That confidence can disappear fast when “higher for longer” turns into “higher again.”

The frothiest parts of the market are the most exposed:

• Semiconductors

• Long-duration growth stocks

• Highly leveraged companies

• Real estate deals built around cheaper refinancing

• Borrowers whose refinancing models still need cheaper money to work

For corporate treasurers and borrowers, the message is simple:

Hotter inflation keeps the Fed pinned down.

Higher yields make refinancing harder.

Firmer SOFR expectations keep pay-fixed swap rates elevated.

Rate caps stay expensive when markets price more inflation risk and less Fed flexibility.

If rate-hike expectations broaden in Fed funds futures and SOFR forward curves, hedge costs, refinancing assumptions, and budget rates get uglier fast.

Derivative Logic helps companies and borrowers quantify rate risk before it shows up in loan economics, hedge pricing, and budget misses.

Because “we thought lower rates were coming” is still not a risk management strategy.

US Dollar: The Quiet Trade That May Not Stay Quiet

The dollar has not fully priced the move in U.S. rates. That looks hard to defend.

U.S. yields are grinding higher as inflationary pressure continues to broaden. PPI added more fuel. Oil prices are still elevated. Geopolitical risk is adding another layer of inflation risk.

Rates markets have noticed. FX markets look slower to react.

If U.S. front-end rates stay firm, the dollar may need to catch up.

That matters for corporate treasurers because a stronger dollar can hit fast:

• Foreign revenue translates into fewer dollars

• USD payables get more expensive for non-U.S. entities

• FX forward rates can become less forgiving

• Hedge costs can shift quickly

• Budget rates can get stale in a hurry

The bigger risk is assuming the dollar stays calm while rates, oil, and inflation pressure all point the other way.

Currency risk does not wait for the quarterly forecast meeting.

Derivative Logic helps companies quantify FX and rate risk before it shows up in margins, cash flow, and hedge execution.

Who's handling your FX risk management?

Chart of the Day: CPI Leaves the Door Open for Higher Yields

April CPI was not bad enough to blow up the market, but it was bad enough to keep rate-cut dreams in timeout.

The print suggests inflation pressure is not fading fast enough to give the Fed comfort. That kept the initial market reaction contained.

The less convenient news:

• Rents ran hot, partly due to a widely expected BLS measurement quirk

• Supercore inflation, services excluding housing, rose at the fastest monthly pace since January

• Inflation pressure is broadening across categories

• Core goods are still cooling, but the disinflation story is losing some shine

• Energy remains elevated, even if the Fed prefers to look through oil-driven inflation

A CPI report like this can keep the market leaning toward higher yields, a firmer dollar, and less confidence that rate cuts arrive on schedule.

For companies with floating-rate debt, foreign currency exposure, or refinancing needs, “not terrible” inflation is still not the same as useful relief.

That can show up in:

• Higher borrowing costs

• Firmer hedge costs

• Less favorable FX forward pricing

• Less forgiveness in budget rates

• More pressure on floating-rate debt

• Tougher refinancing math

Derivative Logic helps corporate treasurers and borrowers quantify rate, currency, and hedge risk before it hits borrowing costs, hedge pricing, and FX exposure.

CPI Just Dragged Rate Cuts Behind the Shed

April CPI came in hot enough to make the rate-cut crowd check the exits. Gasoline jumped. Food jumped. Rent jumped. Airfares jumped. Hotels jumped.

CPI rose 3.8% year over year, the fastest pace since 2023. Monthly CPI rose 0.6%. Core CPI rose 0.4%.

The initial Treasury market reaction was muted because traders already expected a hot print. SOFR futures moved only 2 to 5 basis points higher, and two-year Treasury yields were already near one-month highs.

The bigger issue is the long end. The 30-year Treasury has been carrying the pain. Now the 10-year may start catching up.

That matters because the 10-year sits closer to the refinancing math for fixed-rate debt, permanent loans, and longer-dated swap pricing. If the upward pressure moves from the 30-year into the 10-year, borrowers lose the part of the curve they were hoping would bail out the model.

Borrower translation:

• Floating-rate relief just got harder to pencil

• Rate caps likely stay expensive

• Float-to-fixed swap rates likely stay firm

• Fixed-rate refinancing math stays ugly

• The 10-year may feel pressure as the long-end move spreads inward

• The 30-year near 5% is no longer a weird outlier

Derivative Logic helps borrowers quantify rate risk before it shows up in loan economics, swap pricing, and cap execution.

What's your strategy for higher-for-longer interest rates?

5% on the 30-year Treasury is not a ceiling if the U.S. economy keeps adding jobs, spending holds up, and inflation pressure refuses to fade.

CPI and PPI matter this week because the bond market is already nervous.

The mix is ugly:

• Firm job growth

• Higher oil prices

• Large deficit spending

• Policy volatility

• Long-term inflation expectations that refuse to disappear

If inflation expectations move higher, 30-year Treasury yields can stay sustainably above 5% for the first time in more than two decades.

For borrowers, that means:

• Higher rates on fixed-rate debt

• Firmer long-dated float-to-fixed swap rates

• Tougher refinancing math

• More pressure on DSCR assumptions

Oil can light the match. A still-solid economy can keep the fire department stuck in traffic.

Derivative Logic helps borrowers quantify rate risk before it shows up in loan economics, swap pricing, and cap execution.

Chart of the Day: The Fed Can’t Fix Oil With a Rate Hike

Inflation risk is rising again.

Naturally, the market is debating whether the Fed should swing a hammer at a problem that looks suspiciously like a glass table.

The San Francisco Fed splits core PCE - the Fed's favorite inflation gauge - into two buckets:

• Cyclical inflation, tied to demand and monetary policy

• Acyclical inflation, tied to energy, food, supply shocks, and geopolitics

The second bucket is the ugly one. If oil and food prices rise because Iran, Hormuz, and supply disruption are back on the menu, higher rates will not produce more crude, reopen shipping lanes, or make diesel cheaper.

For borrowers, this is where the rate-cut fantasy starts coughing into a napkin:

• Cuts can keep getting pushed out

• Float-to-fixed swap rates may stay firm

• Rate cap costs stay expensive

• Fixed-rate debt looks less appetizing

• Refinancing models may need fewer hopes and more stress tests

Tomorrow’s CPI report matters. But the bigger issue is whether the Fed can do anything useful about this inflation mix.

If inflation is driven by excess demand, the Fed has tools.

If inflation is driven by oil, food, war risk, and supply shocks, the Fed has press conferences, dot plots, and a very serious podium.

Pressure-test your models against higher-for-longer rates, firmer swap rates, and cap pricing that still requires adult supervision.

Derivative Logic helps quantify rate risk before it shows up in loan economics, swap pricing, and cap execution.

What's your strategy for higher-for-longer rates?

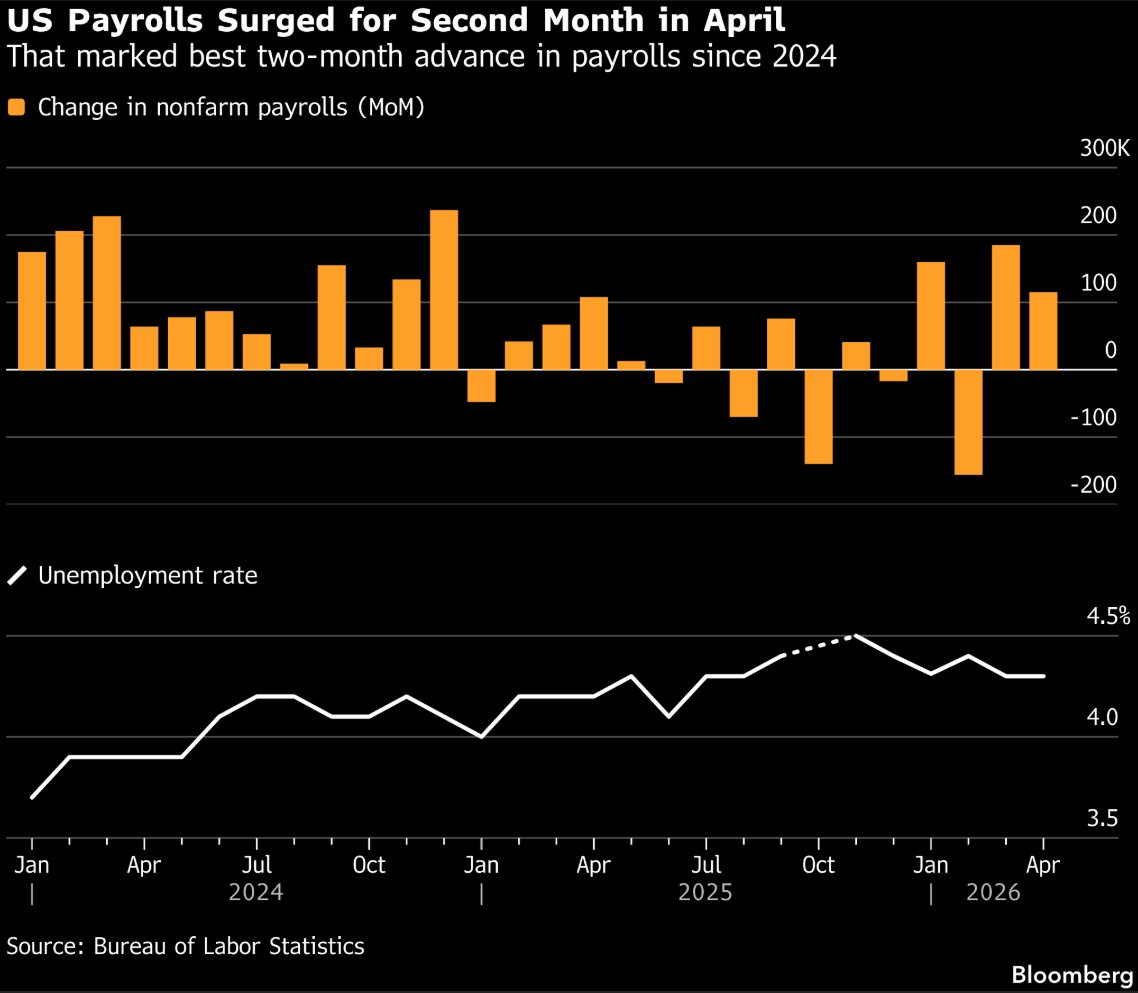

Jobs Data Just Punched the Rate-Cut Story in the Mouth

The economy is still hiring. Roughly 300,000 jobs were created over March and April, even with gasoline prices up more than 50% year over year.

That is great for equities. It is awkward for anyone praying for Fed rate cuts.

Fed Chair Powell already said the labor market looks more stable while inflation remains elevated.

Translation for borrowers:

The Fed does not cut rates just because you want your refi model to work.

The Treasury market now has a problem:

• Strong jobs keep the Fed patient

• Higher oil keeps inflation risk alive

• Long-term Treasury yields are moving up with energy

• Float-to-fixed Swap rates may stay firm

• Rate cap costs stay expensive

Yes, lower-income consumers are getting squeezed. Yes, durable goods demand is cracking.

But if oil keeps inflation hot while hiring holds up, the Fed has less room to ride in with a rate-cut cape.

What's your plan for uncomfortably high Treasury yields and SOFR? Borrowers should stop building financing plans around wishful thinking.

Derivative Logic helps borrowers quantify rate risk before it shows up in loan economics, cap pricing, and swap execution.

The long bond is now taking orders from oil.

The 30-year Treasury yield is hovering near 5%, and its correlation with oil is the highest since the pandemic.

Translation for borrowers: Oil goes up, inflation risk rises, and the long end of the Treasury curve gets cranky.

WTI spiked above $107 Monday, then fell below $90 later in the week. That helped keep the 30-year yield under 5%. Barely.

If oil turns higher again, the 30-year may not ask permission before breaking 5%.

That means:

• Higher fixed-rate loan coupons

• Firmer longer-dated swap rates

• Worse refinancing math

• More pressure on DSCR

Hormuz is still the pressure point. Until there is a signed agreement, oil is sitting in the Fed’s chair with muddy boots on the desk.

Derivative Logic helps borrowers model this before it hits loan quotes, swap pricing, and hedge costs. Because “we thought rates would fall” remains undefeated as the worst hedging strategy in finance.

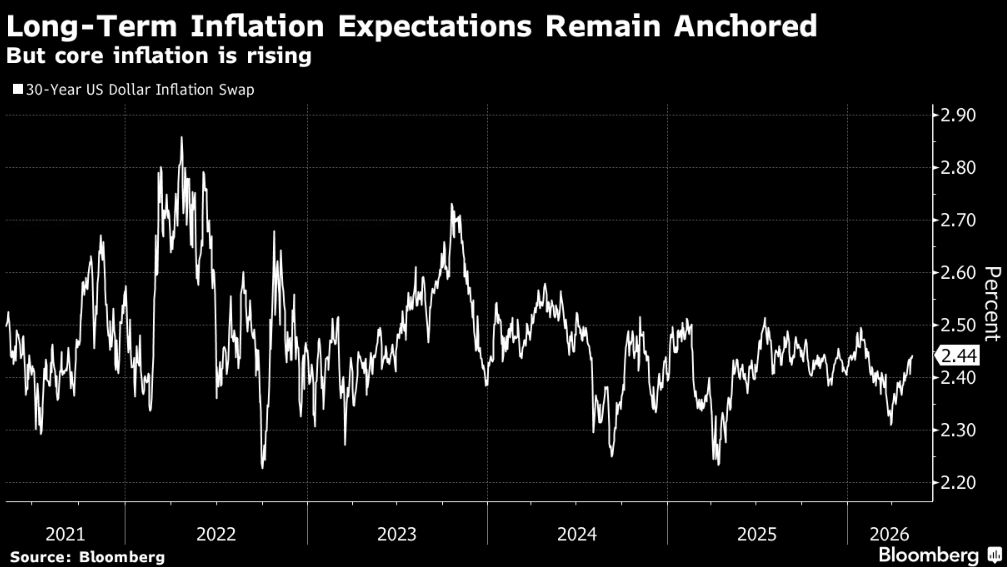

Inflation Expectations Jump. Treasury Yields Hit Snooze.

The NY Fed’s 1-year inflation expectations measure rose to 3.64%, the highest since September 2023. Cue the scary chart. Cue the inflation headlines.

Cue every borrower wondering why their rate cap cost or float-to-fixed swap rate did not immediately explode higher.

Here’s why:

* Treasury yields are not panicking because the Treasury market still sees this as an oil shock, not a full inflation jailbreak.

* Oil prices are off their highs. Market-based inflation gauges, like 1-year inflation swaps, remain lower. The bond market is basically saying, “Wake me when this shows up somewhere that matters more.”

For borrowers, that is useful. For now.

If inflation expectations keep rising, the Fed gets less room to cut. If the Fed has less room to cut, SOFR relief gets sent back to the waiting room. If SOFR relief gets delayed, float-to-fixed swap rates and rate cap costs stay annoyingly high.

Borrowers should watch the things that can turn a survey scare into real rate pressure:

• Oil prices

• PCE inflation

• Wage pressure

• Market-based inflation expectations

• The SOFR forward curve

Consumer surveys alone may not move borrowing and hedging costs.

But if inflation expectations start spreading into the data the Fed actually trusts, the rate-cut fairy gets reassigned to compliance training.

Supply chain stress is creeping back into the inflation story.

The New York Fed’s Global Supply Chain Pressure Index is moving toward levels not seen since the last major inflation cycle.

Why borrowers should care:

• Supply bottlenecks often show up later in inflation data

• Higher input costs can slow the path toward Fed cuts

• Oil and gasoline pressure can keep inflation expectations elevated

• Long-term Treasury yields may need more yield cushion if inflation risk rises

• Float-to-fixed Swap rates and fixed-rate loan coupons may stay firmer than borrowers hoped

The uncomfortable part? Even if Middle East tensions cool, supply chains rarely normalize overnight.

And if core PCE - the Fed's favorite inflation gauge - keeps running above the Fed’s forecast while growth holds up, the 10-year Treasury yield has less reason to fall and more reason to test higher levels.

For borrowers, this means rate relief may arrive late, arrive smaller, or get eaten by volatility before it reaches your loan economics.

Derivative Logic helps borrowers model that risk before it shows up in cap costs, swap pricing, and refinancing assumptions.

Because “we thought supply chains were fixed” is not a hedging strategy. (Chart source: Bloomberg Professional)

The Fed May Need More Than Patience to Keep Treasury Yields Here

Long-term Treasury yields are orbiting 5%.

Markets are now pricing a Fed hike as more likely than a cut during Kevin Warsh’s first year as Fed Chair.

Why? Oil. Iran. Inflation risk.

For borrowers, this means:

• Fixed-rate debt stays expensive

• Float-to-Fixed interest rate swap rates stay firm

• Rate cap costs stay elevated

• Refinance math gets uglier

Do you believe the Fed's next move is a rate hike?

Oil Is Testing the Bond Market’s Pain Threshold

The 30-year Treasury, near 5%, used to pull in pension funds and insurers.

Now? Oil is elevated. The Middle East is tense. Inflation expectations are moving the wrong way.

If long-term Treasury yields break above 5% and stay there, borrowers could face:

• More expensive fixed-rate financing

• Firmer long-dated float-to-fixed interest rate swap rates

• Less refinancing relief

• Worse defeasance math

The Fed may need to talk tougher, or even consider hiking, to keep inflation expectations contained.

Yes, hiking into an oil shock sounds awful. So does surgery with a spoon. But if the Fed hesitates, long-term yields may do the tightening instead.

Borrowers should not assume 5% is the ceiling. It may be the cover charge.

Derivative Logic helps borrowers model that risk before it lands in loan coupons, swap rates, cap costs, and refinancing economics.

Because hoping the 30-year Treasury yield politely stops at 5% is a lovely bedtime story.

What's your strategy for managing higher long-term interest rates?

What Japan’s Yen Intervention Means for Borrowers Watching U.S. Rates

Japan is back in the currency intervention game.

The Ministry of Finance appears to have spent roughly $35 billion buying yen after USD/JPY pushed through 154. That is the first official intervention since 2024.

Why should U.S. borrowers care?

Japan is one of the largest foreign holders of U.S. Treasuries.

When the yen weakens, inflation pressure rises in Japan. When inflation pressure rises, Japanese yields can move higher. When Japanese yields move higher, Japanese investors have less incentive to reach overseas for yield, especially after currency-hedging costs are considered.

That matters for the U.S. Treasury market.

If Japanese buyers demand fewer Treasuries, or require more yield to justify buying them, U.S. long-term yields can face upward pressure.

For borrowers, that can show up in:

• Higher 10-year Treasury yields

• Firmer fixed-rate loan coupons

• Higher longer-dated float-to-fixed swap rates

• Less relief in refinancing economics

Japan’s issue is awkward. Inflation has cooled, but not enough to declare victory. The yen is weak. Energy prices are a problem. Ten-year Japanese government bond yields are back above 2.5% for the first time since the mid-1990s.

Yes, the Ministry of Finance can buy yen. No, it cannot repeal global inflation math with a press release and a Bloomberg terminal.

For borrowers, the takeaway is simple:

- Stop treating U.S. rate moves as a Fed-only story.

- The Fed can influence the front end of the US Treasury yield curve.

- Foreign demand helps shape the long end.

Currency stress, oil, deficits, foreign demand for Treasuries, and global yield competition all feed into your borrowing cost.

Derivative Logic helps borrowers quantify that risk before it shows up in swap pricing, cap costs, and loan economics.

Because “we thought cuts were coming” is not a hedging strategy.