An intelligent equity research platform. Get high quality research reports and chat with the intelligent research assistant to generate insights that matter.

In case you're wondering - the CLI version ran on a different machine that didn't have the mcp installed. The GUI is from my main desktop machine. That's the only difference. Both are Claude Code.

1.1 million tokens and still not done (and hit my 5h limit), compared to 145k tokens and done. All on Sonnet 5 high. A nearly 10x difference and still not done.

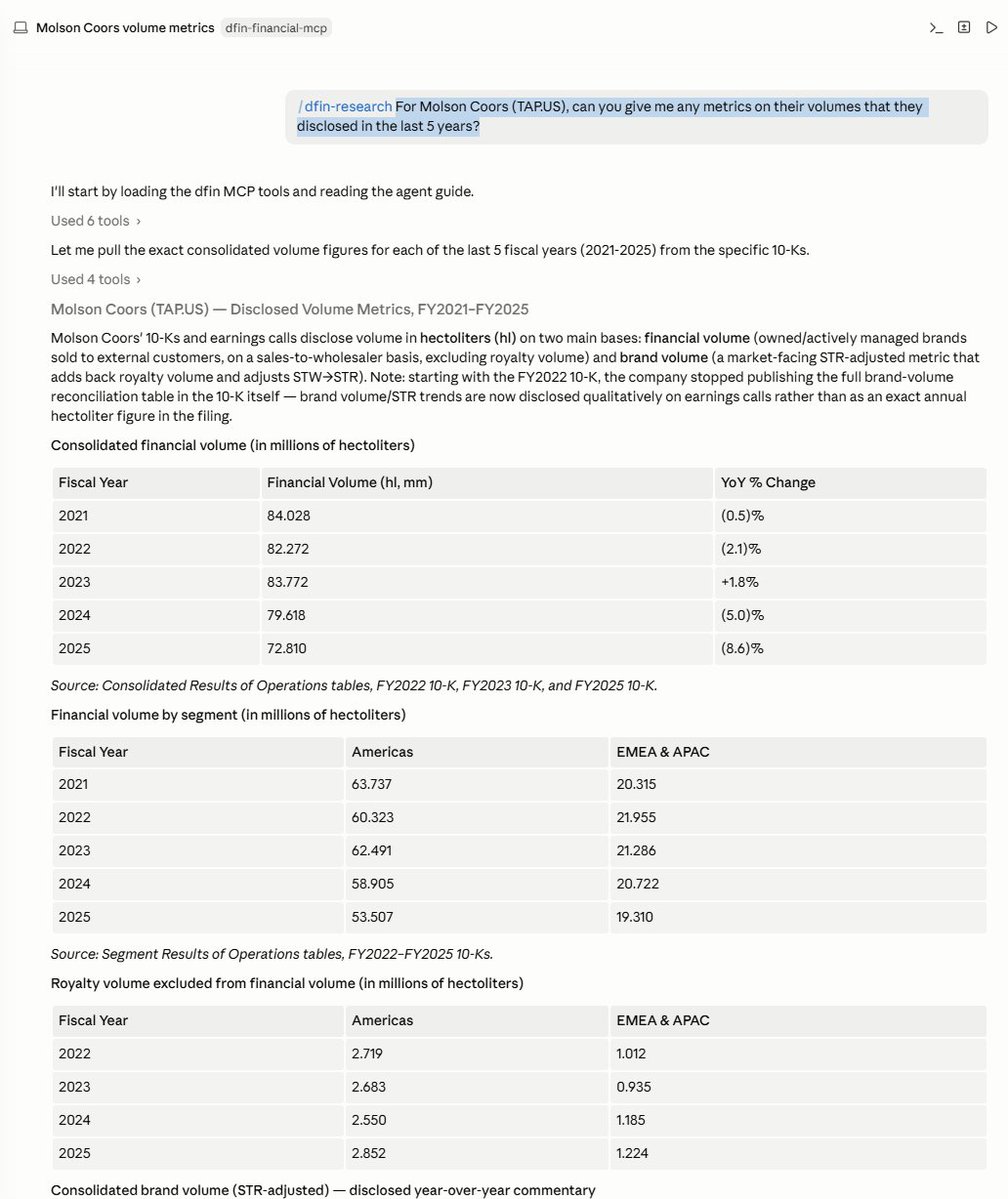

The task? "For Molson Coors (https://t.co/hD5zGkUyrL), can you give me any metrics on their volumes that they disclosed in the last 5 years?"

I set a task to Claude to get the data using our MCP v/s just setting it loose. Running both on Claude Code.

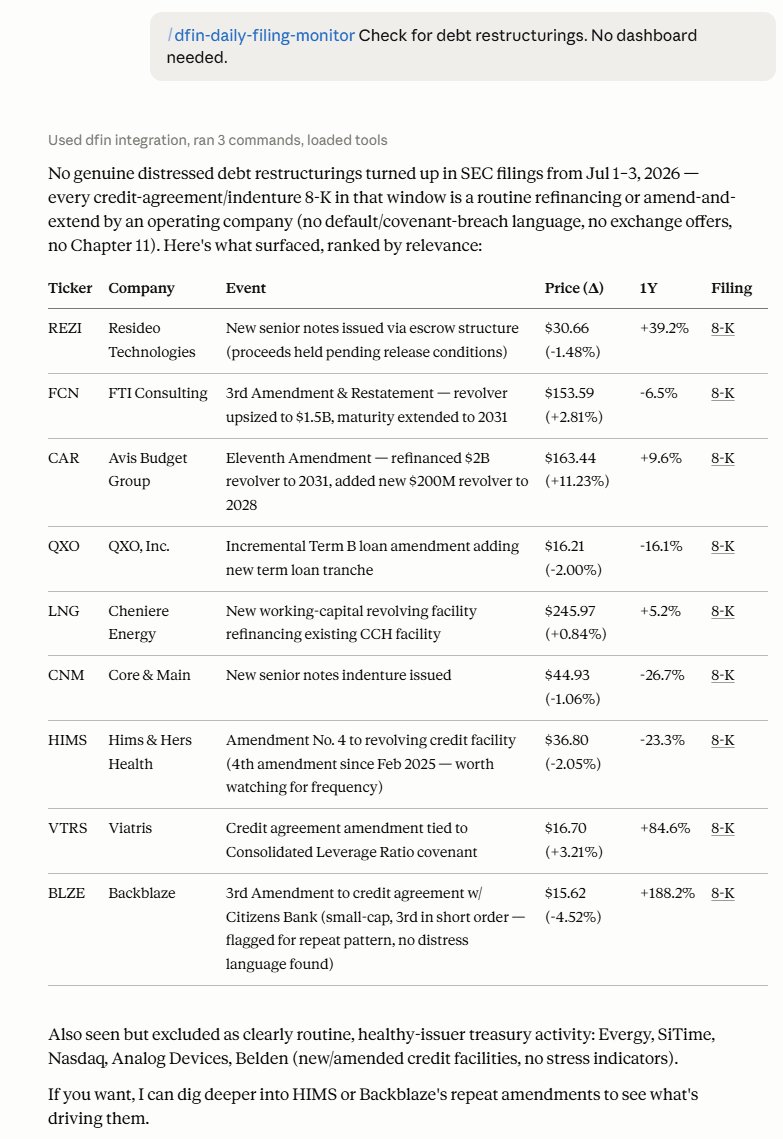

I received a request for a way to scan daily filings to monitor for various events (management changes, debt restructuring, etc.). With the power of our MCP and AI, it's just a simple task to set up and schedule!

I spent a lot of time focusing on making the task as token efficient & simple as possible. With Claude, you can even use Haiku to run these quickly & cheaply.

It's packaged as a skill now /dfin-daily-filing-monitor. Easily accessible and modifiable per your personal requirements.

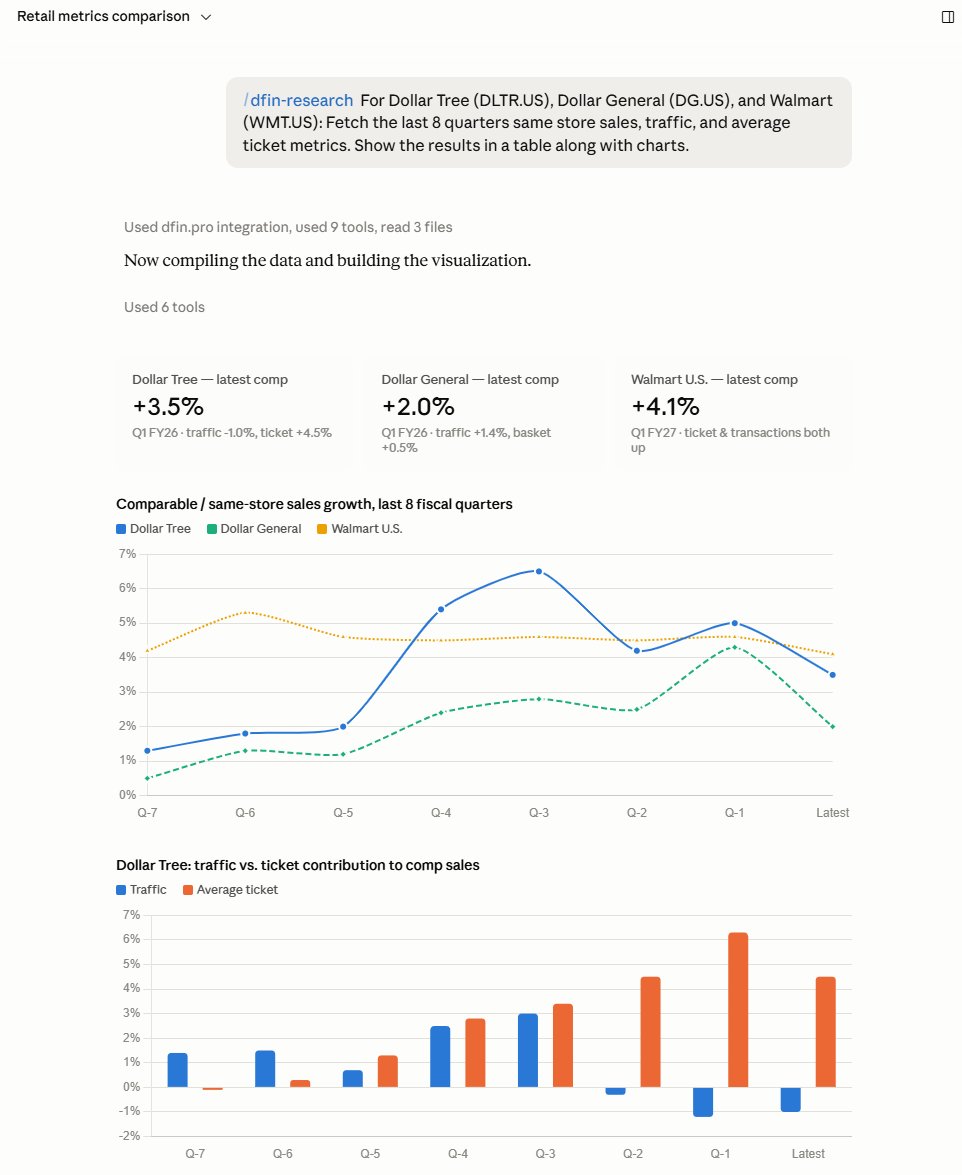

Excited to share that our MCP is coming along nicely. Here's a simple prompt that fetches metrics for the Dollar stores and Walmart.

That's 8 quarters x 3 companies = 24 filings at a minimum from which the data is collected. The key is token & time efficiency. Without the MCP your agent's context would be exhausted already reading through full filings & transcripts. Our MCP lets you do a lot more with limited token budgets.

Here're a couple of screenshots.

Using agents (Claude & Codex) with our MCP is proving to be a huge unlock. It's still in beta testing, but it is genuinely making my life easier.

It's easily delivering responses from our filings, transcripts, and reports database. Directly responds to queries on metrics, financials, etc. I've been working on some screening use cases as well.

If you'd like to be part of the beta testing team, please do ping me!

Who's smarter - $MU or SK Hynix? Micron is buying back stock at these levels while SK is issuing new equity to raise $29 B. SK has $21B of net cash on their balance sheet and FCF for FY26 and 27 is expected to be $98B and $173 B. They don't need the cash, but still choosing to raise capital.

Seems like SK believes this just another cycle and if the shares get cut in half in the future, this will seem like a genius decision.

Or is there something I'm missing?

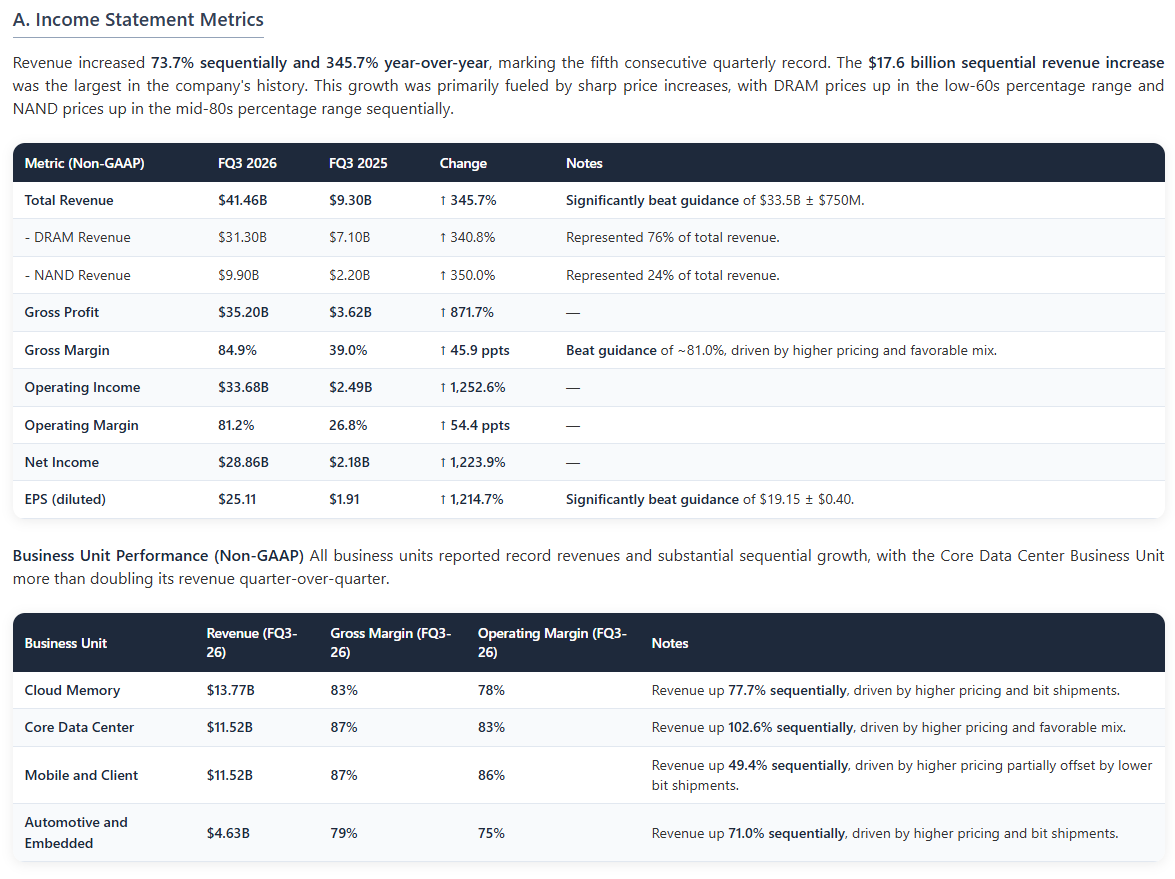

$MU Micron reported a fifth consecutive record quarter, with FQ3 revenue of $41.46 billion and non-GAAP EPS of $25.11, substantially exceeding prior guidance. Performance was driven by continued tight supply-demand conditions and significant sequential price increases in both DRAM and NAND.

The quarter's defining development was the execution of 16 Strategic Customer Agreements (SCAs), which management frames as a fundamental transformation of the business model. These multiyear, take-or-pay agreements cover a significant portion of future volume and include floor pricing designed to secure gross margins "well above our peak quarterly margins in any past cycle." The company disclosed a related ~$100 billion in Remaining Performance Obligations (RPO) and expects to receive $22 billion in cash deposits and related financial commitments.

Looking ahead, Micron issued a record FQ4 revenue forecast of $50.0 billion ± $1.0 billion and raised its FY2026 CapEx plan to ~$27 billion. Management extended its outlook for industry tightness by a full year, now expecting it to persist beyond calendar 2027. The execution of SCAs at scale marks a pivotal shift aimed at mitigating historical cyclicality by securing a large portion of future business with favorable terms, fundamentally altering Micron's long-term financial profile.

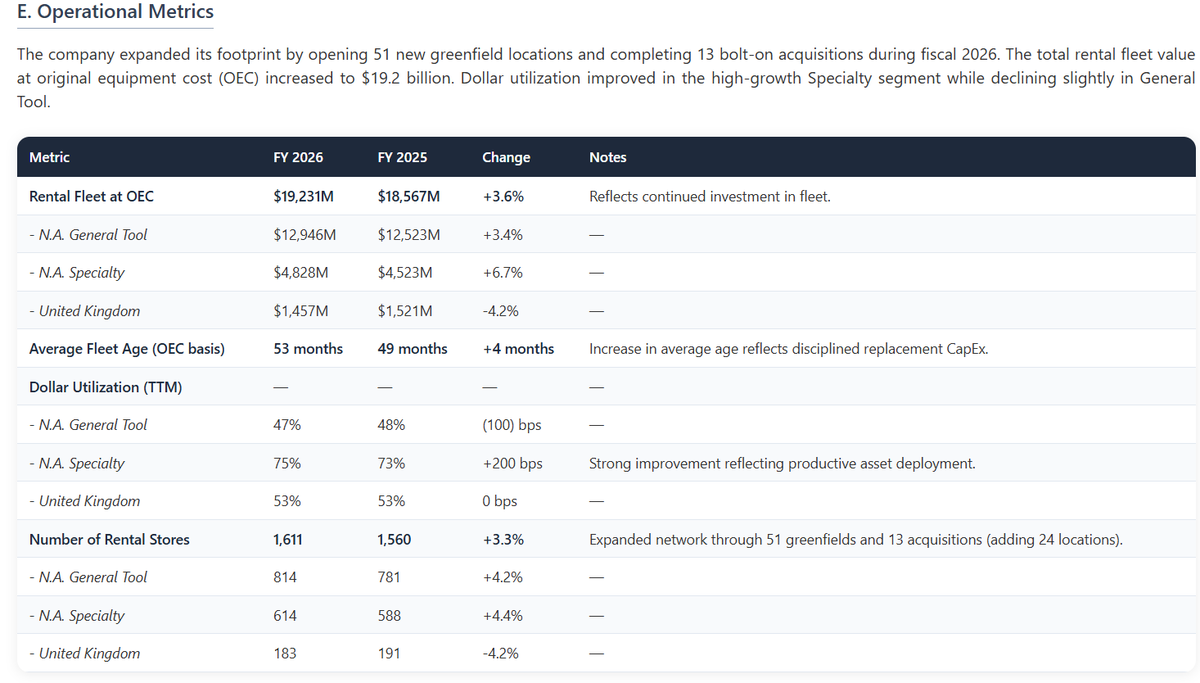

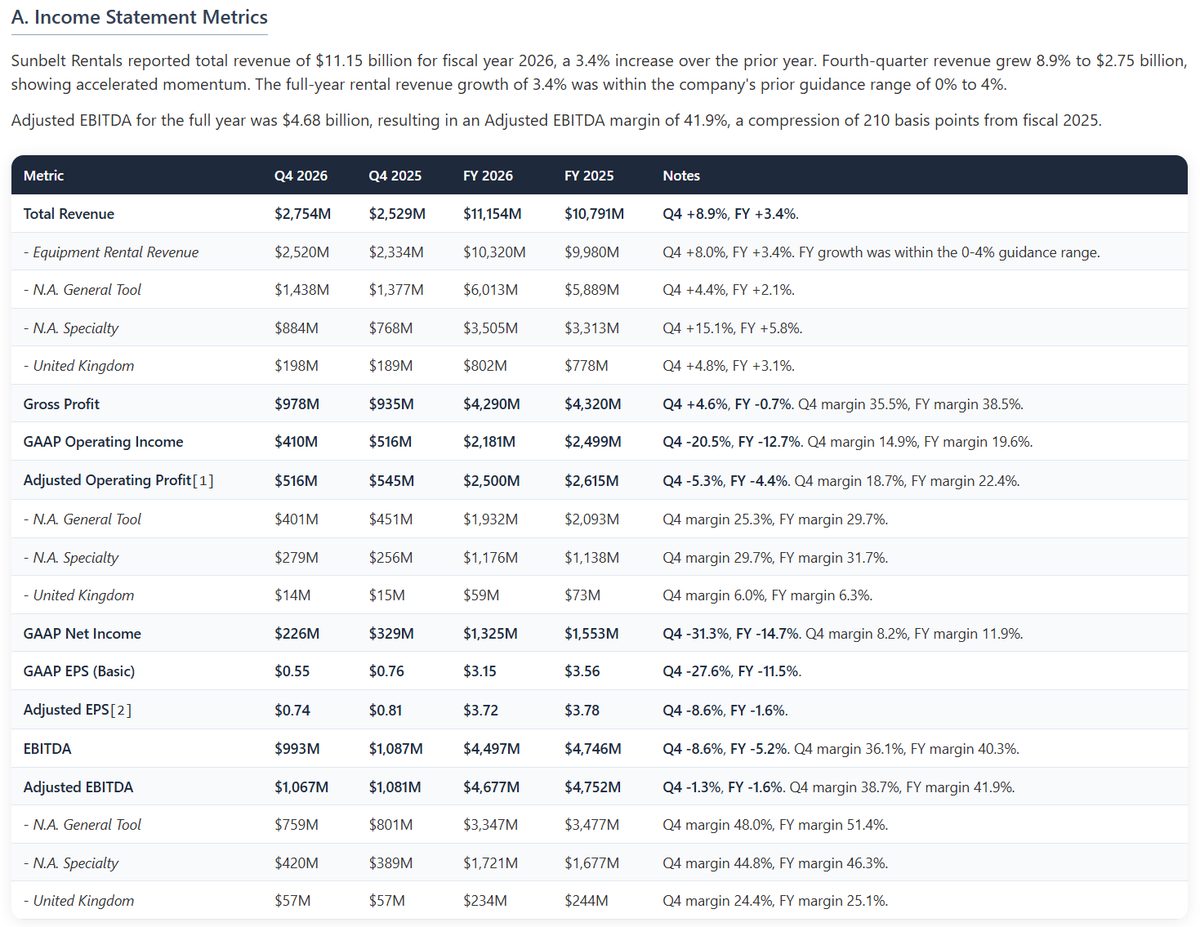

$SUNB Sunbelt Rentals reported an acceleration in Q4 FY2026, with total revenue growing 8.9% YoY, bringing full-year growth to 3.4% to $11.15 billion. The primary challenge remains profitability, as the full-year adjusted EBITDA margin compressed 210 basis points to 41.9%. Management attributed this to a revenue mix shift toward lower-margin Specialty and ancillary services, costs to reposition fleet for growth, and lapping a $28 million receivables provision reversal from the prior year.

The company introduced FY2027 guidance for 5-8% rental revenue growth but projects broadly flat adjusted EBITDA margins, with improvement weighted to the second half of the year. Growth is underpinned by a significant expansion in the awarded mega-project pipeline, which more than doubled in Q4 to ~$25 billion. This momentum is intended to offset continued flat conditions in the local non-residential construction market.

Strategically, Sunbelt announced the $650 million acquisition of Reliant Asset Management (Aries), creating a new Modular Solutions specialty business to drive long-term growth. Despite margin pressure, the business model generated a record $2.06 billion in free cash flow, enabling $1.88 billion in shareholder returns. The company is leveraging structural growth drivers to navigate a mixed market, but the key focus remains on executing operational initiatives to stabilize margins against persistent mix headwinds.

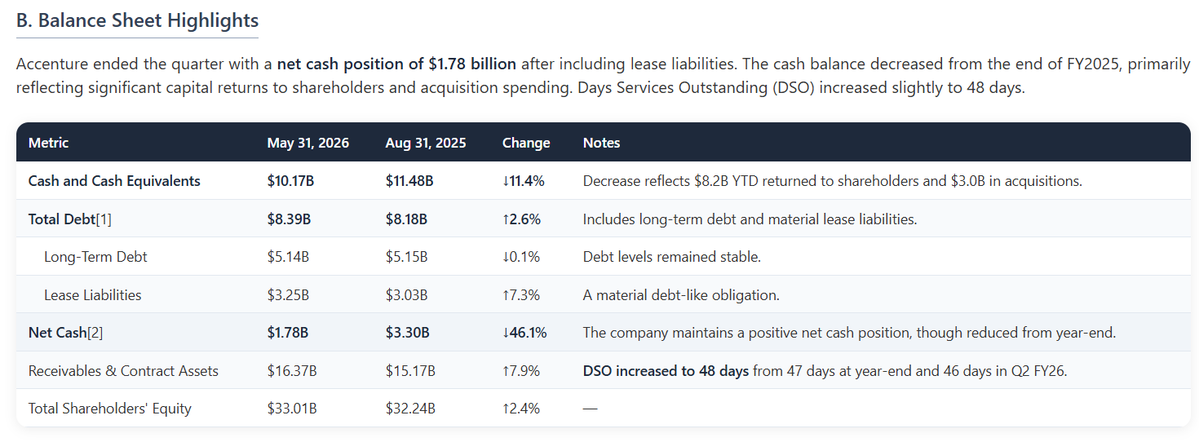

A big drawdown for $ACN today. Link to the report (no paywall) in the comment below.

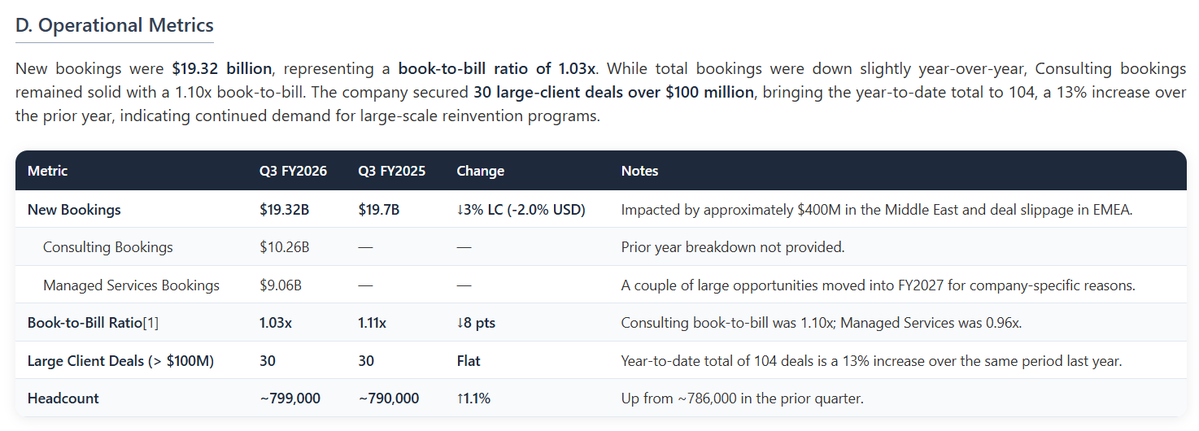

Accenture reported solid Q3 results with revenue of $18.72 billion, representing 3% growth in local currency that landed above the midpoint of guidance, along with 8.9% EPS growth. This performance, however, was tempered by newly materialized geopolitical headwinds. Management quantified a revenue impact of approximately $100 million and a sales impact of $400 million from the Middle East conflict, which also contributed to the slippage of large managed services deals into FY2027.

Reflecting the increased uncertainty, the company trimmed the top end of its full-year revenue growth outlook to 3% to 4% in local currency, down from a prior range of 3% to 5%. Management signaled that "more of the guided range is in play" for Q4, indicating a wider band of potential outcomes.

Concurrent with this near-term caution, Accenture announced its most significant strategic pivot of the year, nearly doubling its planned FY2026 acquisition spend to approximately $9 billion from $5 billion. This is driven by a major expansion into the Operational Technology (OT) security market through the acquisitions of Dragos, runZero, and NetRise, a move intended to create a new, platform-led growth engine.

The quarter highlights a dual narrative: while aggressively deploying capital to expand its addressable market and evolve its business model for long-term growth, Accenture now faces tangible near-term risks that are impacting current sales cycles and creating a more uncertain outlook.

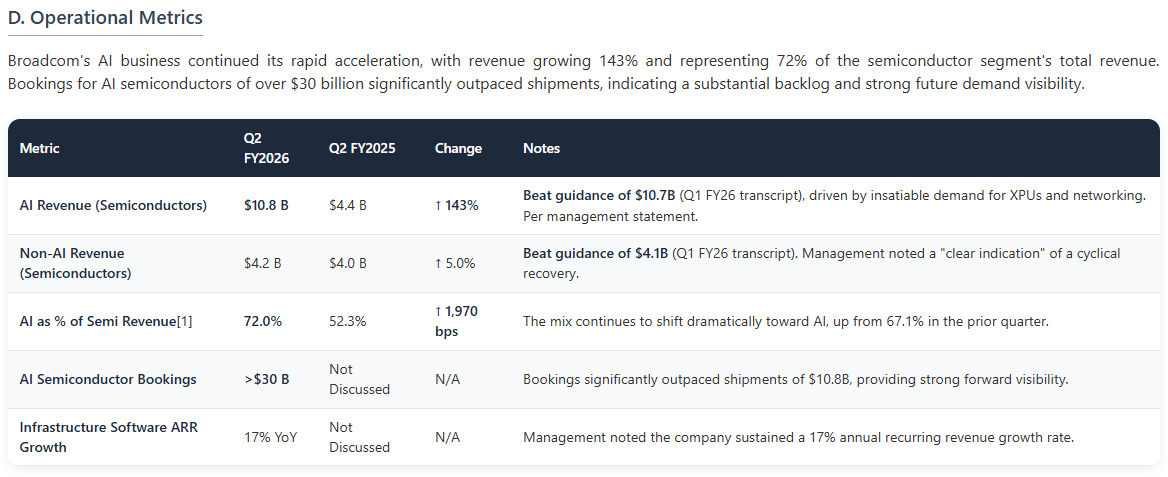

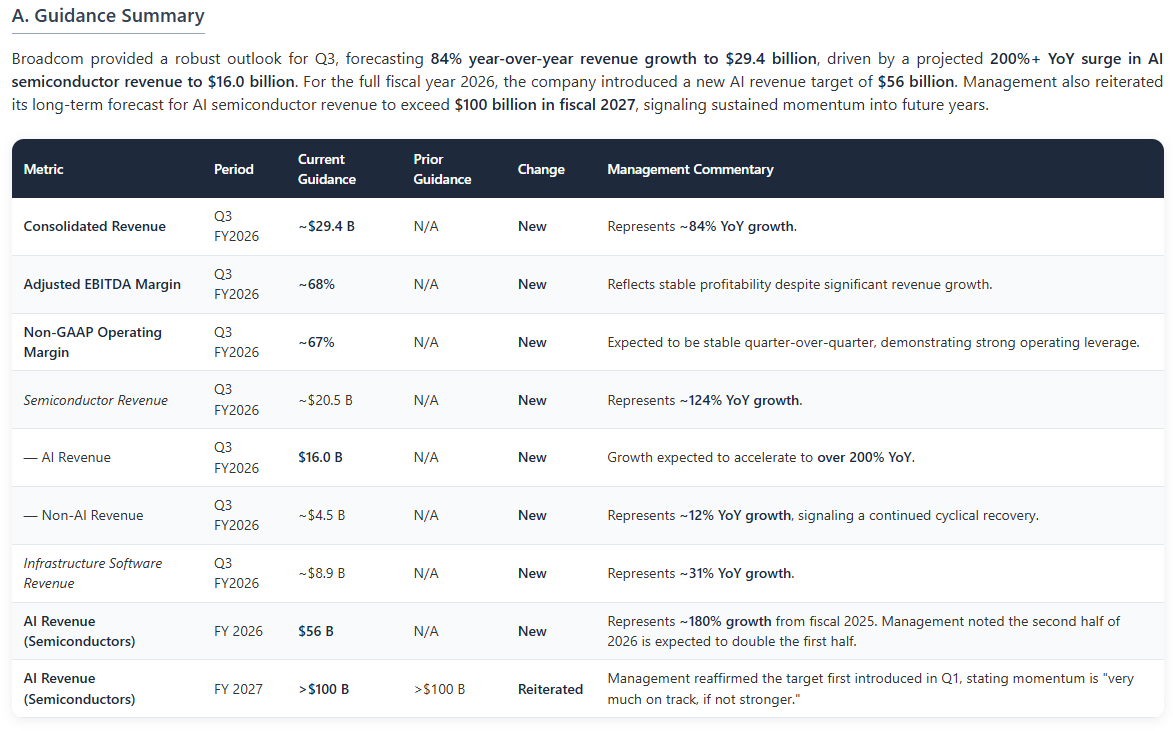

A good quarter by $AVGO, but guidance was clearly not good enough for the market's lofty expectations.

Broadcom reported record Q2 results and significantly upgraded its AI outlook, introducing a new full-year fiscal 2026 AI revenue target of $56 billion, a ~180% increase from the prior year. The company projects this momentum will accelerate, guiding for Q3 AI semiconductor revenue to surge over 200% year-over-year to $16.0 billion.

This forecast is supported by a substantial backlog, with AI semiconductor bookings exceeding $30 billion in the quarter, nearly triple the revenue shipped. Management also detailed new multi-year, multi-gigawatt agreements with core customers including Google, Anthropic, Meta, and OpenAI. To further secure this demand, Broadcom launched a new AI XPU Platform with partners Apollo and Blackstone to finance the deployment of over 20 gigawatts of compute capacity for key AI labs.

Concurrently, the non-AI semiconductor business showed clear signs of a "full cyclical recovery," with strong bookings supporting a forecast for accelerating growth.

The combination of a locked-in, multi-year AI demand trajectory, an innovative financing model to de-risk customer capital expenditures, and a recovering core business extends the company's visibility and solidifies its central role in the AI infrastructure build-out.

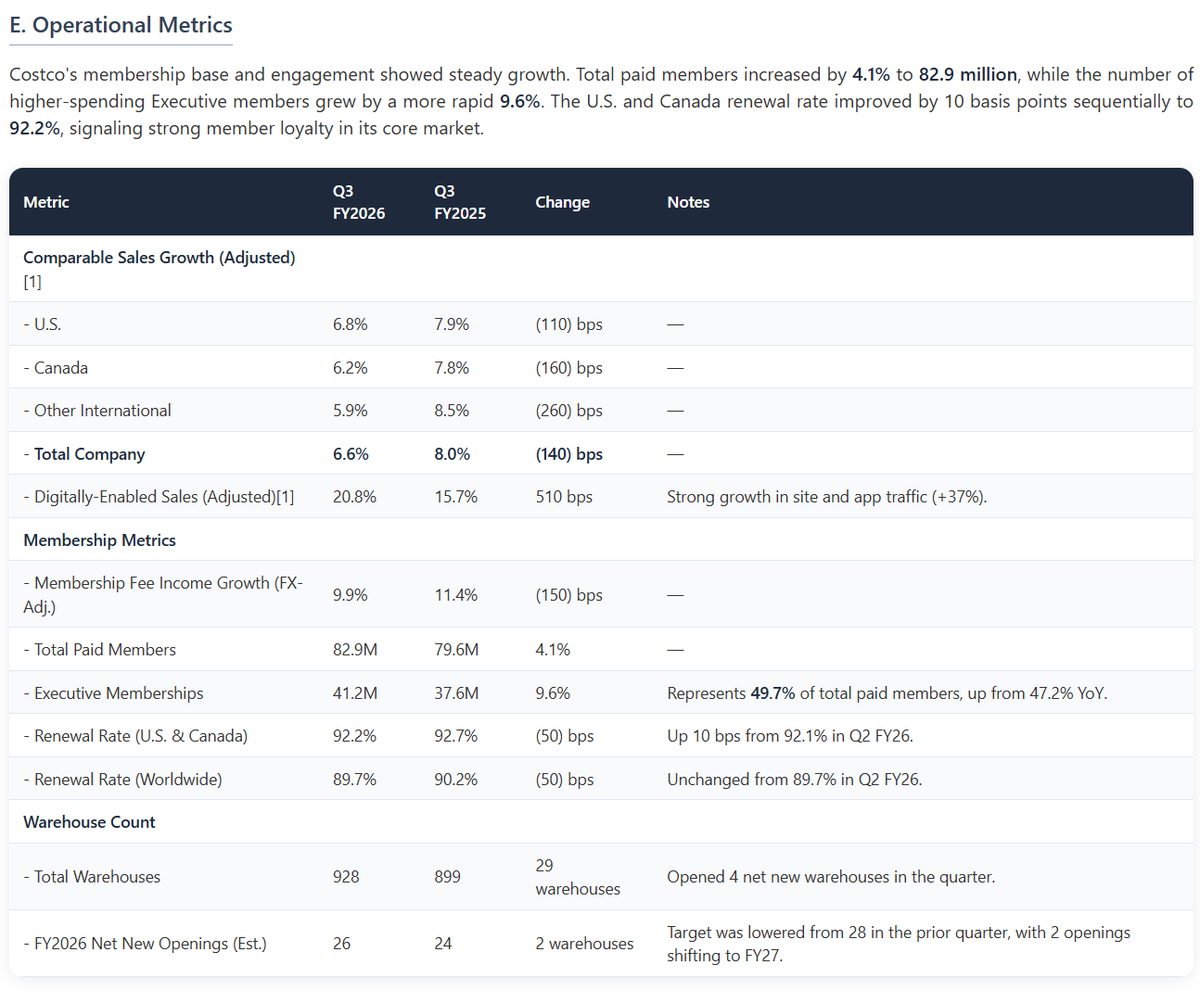

$COST Costco reported Q3 FY2026 results that demonstrated an acceleration in sales momentum, driven by its value proposition in a price-sensitive environment. The company delivered net sales of $69.15 billion, up 11.6% year-over-year, and diluted EPS of $4.93, a 15.2% increase. Total company adjusted comparable sales grew 6.6%, maintaining a consistent trend.

A primary driver was the company's fuel business, which saw record-breaking volumes as consumers reacted to higher gas prices. Management framed this not just as a sales boost but as a key catalyst for member loyalty, noting it drove many members to use Costco gas for the first time. This strength, along with significant market share gains in Pharmacy, propelled Ancillary business comps into the mid-20s.

The company's technology initiatives delivered quantifiable returns. Management highlighted that traffic from AI-driven search saw triple-digit growth and has the highest conversion rate of any channel. The core-on-core margin declined by 9 basis points, a move management characterized as a deliberate investment in member value rather than a reaction to competitive pressure.

Looking forward, the company slightly lowered its FY2026 net new warehouse opening target to 26 from 28. The results indicate that Costco is effectively using its pricing authority to capture market share, while its long-term investments in digital are beginning to yield material, high-quality growth, positioning it to capitalize on evolving consumer search behaviors.

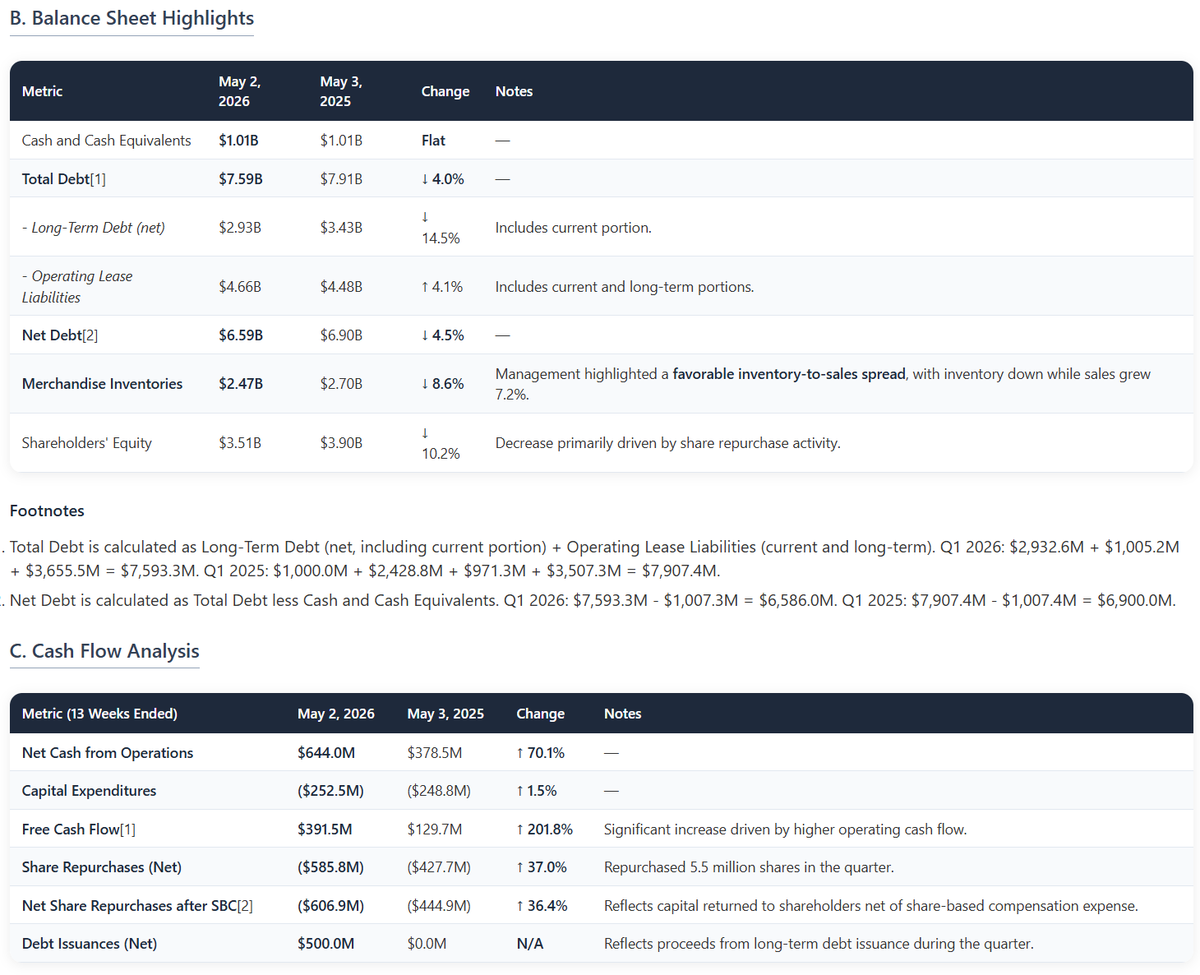

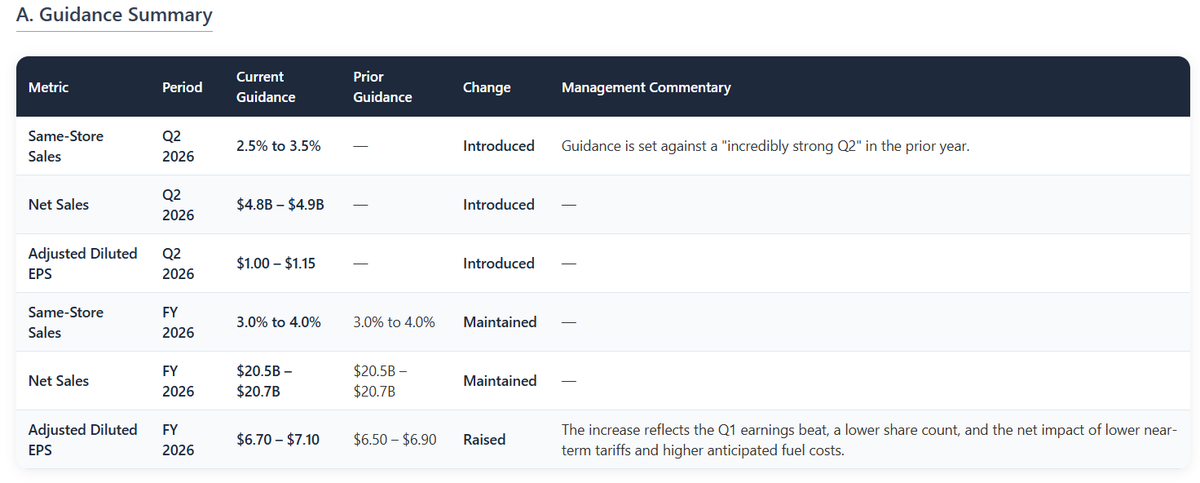

$DLTR Dollar Tree reported Q1 results that surpassed profit expectations, with adjusted EPS increasing 38.1% to $1.74, well ahead of its $1.45–$1.60 guidance. Net sales grew 7.2% to $5.0 billion, meeting the high end of the outlook. The outperformance was driven by strong operational execution, leading to a 120 basis point expansion in gross margin. Management highlighted a significant year-over-year improvement in shrink as the primary driver of the beat, stating their initiatives are beginning to “bend the curve” on losses.

The 3.5% same-store sales growth was fueled entirely by a 4.5% increase in average ticket, as comparable traffic remained negative with a 1.0% decline. However, the traffic trend showed a 20 basis point sequential improvement from Q4, which management cited as evidence of normalization following last year's pricing actions. Reflecting the strong start, the company raised its full-year adjusted EPS guidance to $6.70–$7.10 from $6.50–$6.90. Management framed this as a prudent update, using the Q1 beat to absorb the anticipated headwind of higher fuel costs for the remainder of the year.

The quarter serves as a proof point that the company's internal operational initiatives, particularly on shrink and inventory management, can drive significant profitability. This provides a buffer against macro headwinds, though the investment thesis now hinges on delivering the promised traffic recovery in the second half of the year.

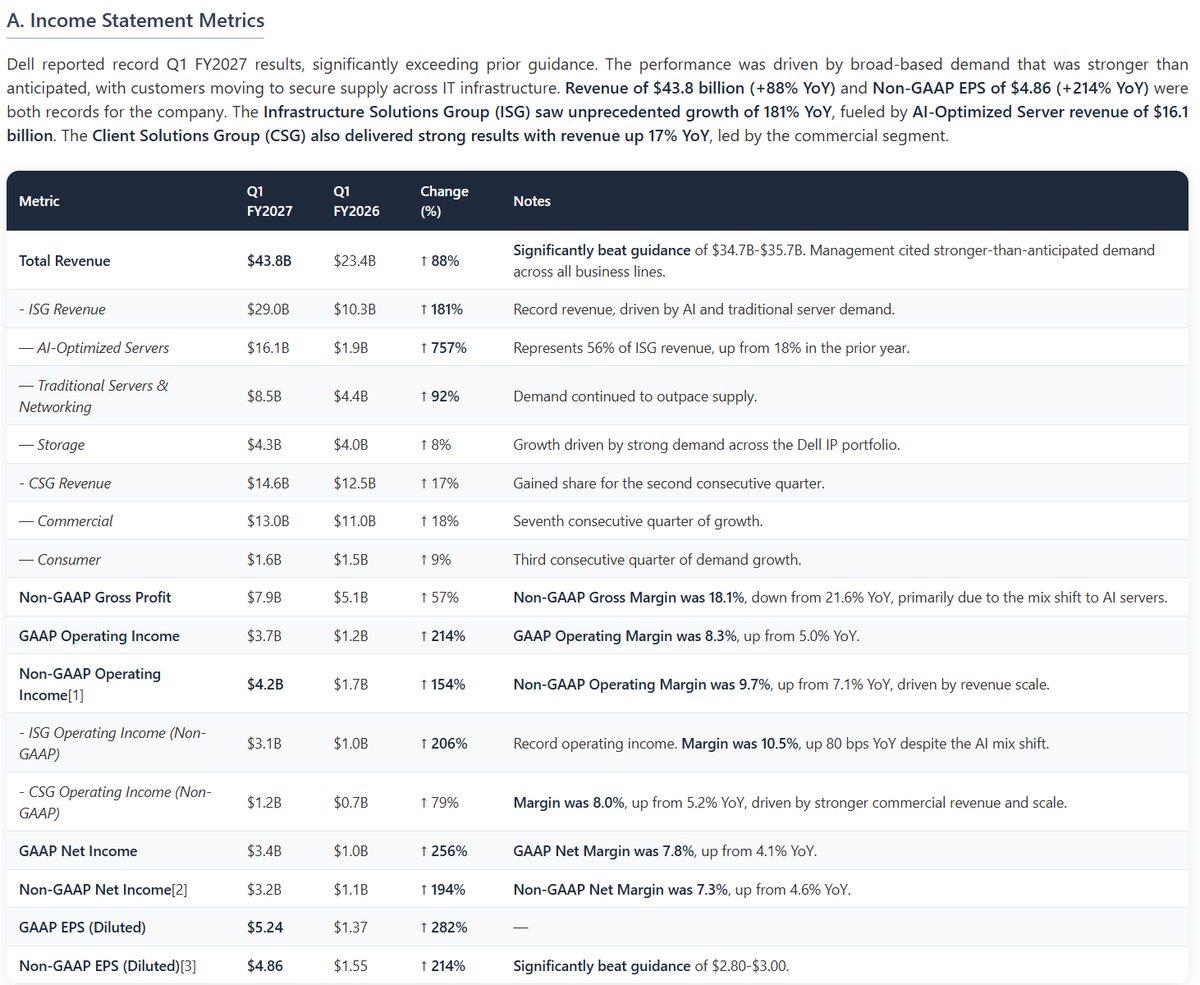

$DELL reported record Q1 FY2027 results that significantly surpassed prior guidance, driven by a broad-based demand surge management described as "different than historical." Revenue reached $43.8 billion (+88% YoY), with non-GAAP EPS of $4.86 (+214% YoY), as customers accelerated purchases to secure supply. This performance was fueled by $16.1 billion in AI-optimized server revenue and continued strength in traditional servers (+92% YoY) and commercial PCs (+18% YoY). The AI business momentum continued, with orders of $24.4 billion driving the ending backlog to a new record of $51.3 billion.

Reflecting this strength, Dell issued a massive upward revision to its full-year outlook, raising the midpoint of its FY2027 revenue guidance by $27 billion to $167 billion and non-GAAP EPS guidance by $5.00 to $17.90. Management introduced "agentic AI" as a new, TAM-expanding catalyst for its high-margin traditional server business.

The primary operational challenge is now navigating severe supply constraints, particularly in memory, with the outlook being explicitly supply-limited, not demand-limited. The results signal a potential structural reset in IT spending, with Dell's ability to secure components becoming the key determinant of its ability to capture the full extent of the market opportunity.

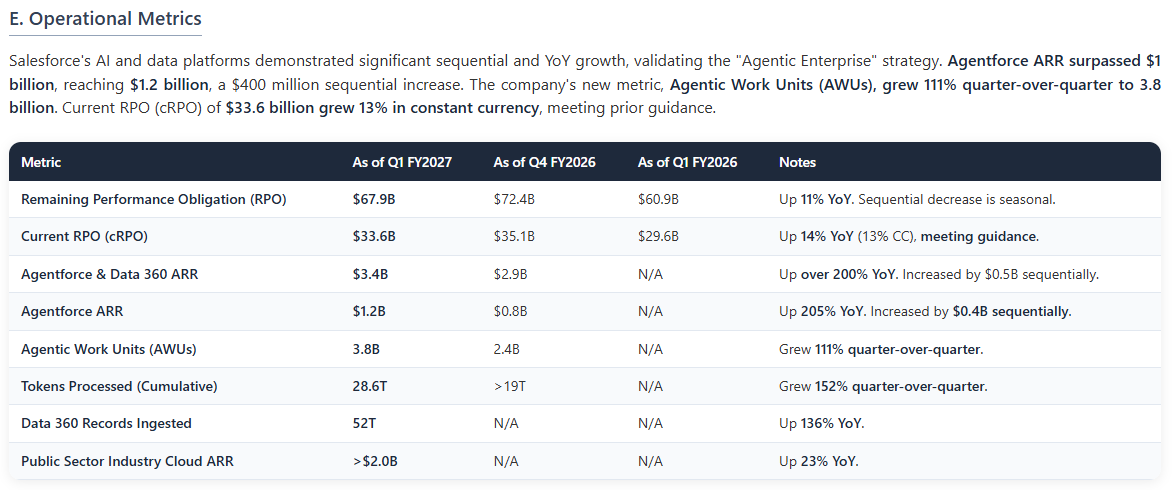

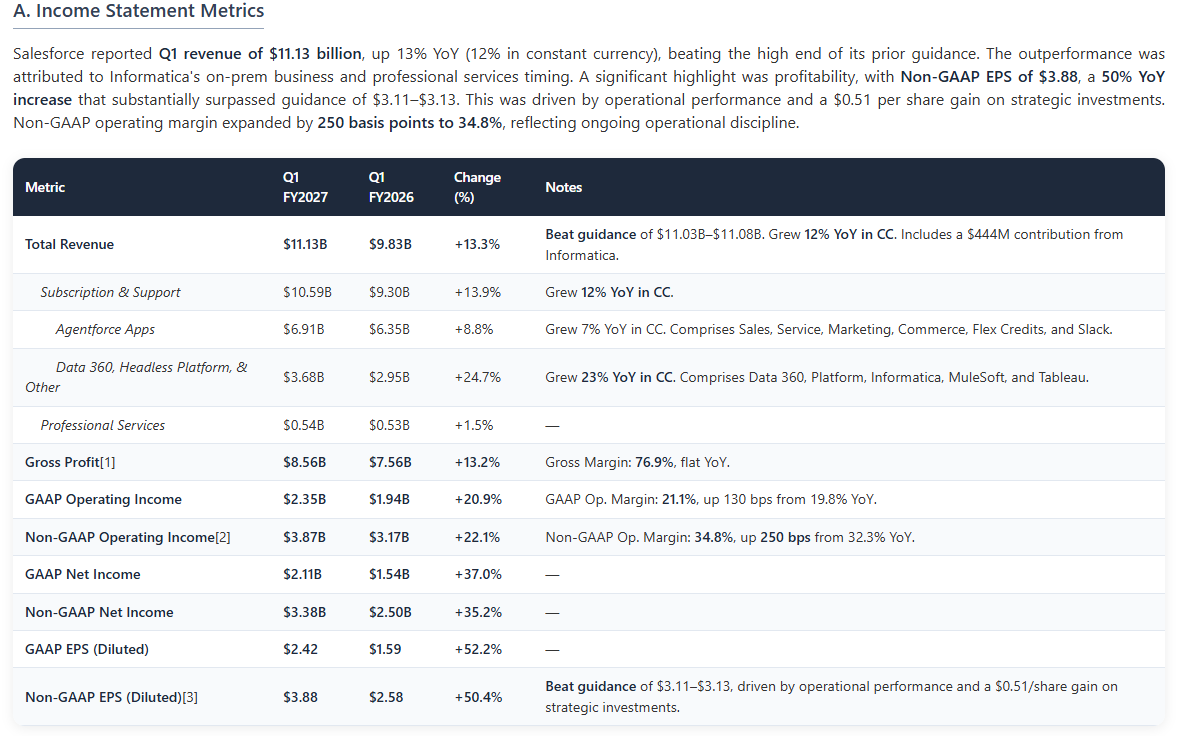

$CRM Salesforce reported Q1 results that beat top and bottom-line guidance, with revenue reaching $11.13 billion (+13% YoY) and non-GAAP EPS surging to $3.88 (+50% YoY), well ahead of the $3.11-$3.13 consensus. The quarter was defined by accelerating momentum in its AI platforms and an aggressive shift in capital allocation.

The company’s “Agentic Enterprise” strategy showed significant traction, as Agentforce ARR surpassed the $1 billion milestone to reach $1.2 billion, a $400 million sequential increase, and cumulative tokens processed grew 152% QoQ. However, this was set against a backdrop where Current RPO grew 13% in constant currency, meeting but not exceeding guidance for the second consecutive quarter. Management addressed this by reaffirming its confidence in a second-half organic revenue reacceleration, citing strong net-new AOV growth as a leading indicator.

Strategically, Salesforce executed a $25 billion accelerated share repurchase (ASR), funded by $24.8 billion in new debt. This move led to a significant raise in full-year non-GAAP EPS guidance but also resulted in a reduction of the full-year free cash flow growth forecast to 4-5% from 9-10% previously, due to higher interest expense. The results present a clear picture of a company leveraging its AI momentum and balance sheet to drive shareholder returns, while the market awaits proof of a broader reacceleration in its core business.

What level of CPU utilization does this represent?

In my experience, the source of the high time spent is the IO, not the CPU crunching data. CPU utilization tends to be very low because it's just waiting most of the time for the data. When the data arrives, usage spikes very briefly (< a few seconds) and then settles back down again quickly.

Curious to hear what other people's experience has been on this. What is the actual CPU utilization when running agentic tasks?

Excited to share a preview of what's cooking on the site. Financial data for US companies in both standardized and as-reported formats, with full auditability to the filing.

Thinking of keeping this as a free feature.

Any thoughts?