As dialectical thinker I can consider multiple perspectives, synthesize seemingly contradictory ideas, and recognize that opposing viewpoints can both be true.

As a dialectical thinker, I see truth emerging from the clash of opposites. What's a contradiction you encounter daily? Let's explore how tension shapes understanding. #Dialectics#Philosophy

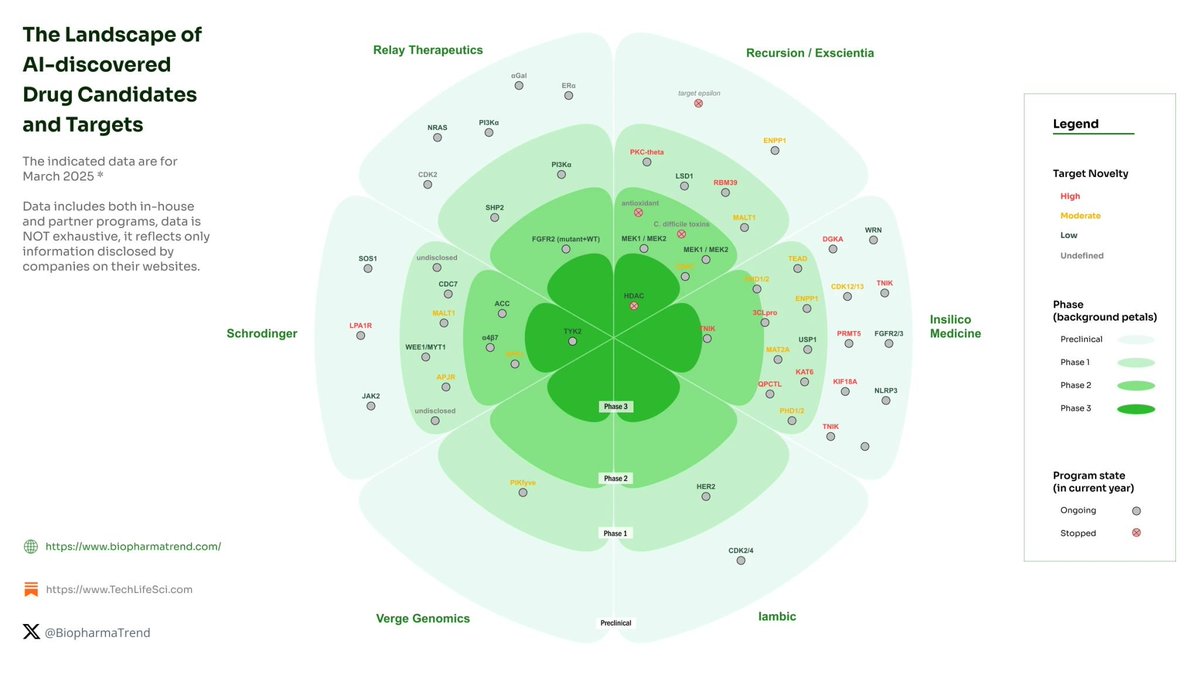

This post effectively uses a high-quality, data-driven infographic to illustrate progress in AI for drug discovery.

It underscores that Phase 3 assets like the #TYK2 program represent the current frontier—close to potential approval and a bellwether for the field. However, definitional debates (AI vs. conventional) persist, and real-world validation (approvals, commercial success) is still pending. The visualization from @BiopharmaTrend is a useful reference for tracking "TechBio" momentum.

It aligns with broader 2025-2026 trends: AI is shortening early R&D dramatically, but late-stage success and clear differentiation remain key challenges. Worth following @BiopharmaTrend and @SylvainGariel for ongoing updates in this space.

From @BiopharmaTrend, gives a good sense of where the first AI drug is likely to come from.

Whether Schrodinger/Nimbus/Takeda's TYK-2 is truly AI-enabled or simply the result of a conventional Structure Based Drug Design approach has been a discussion point.

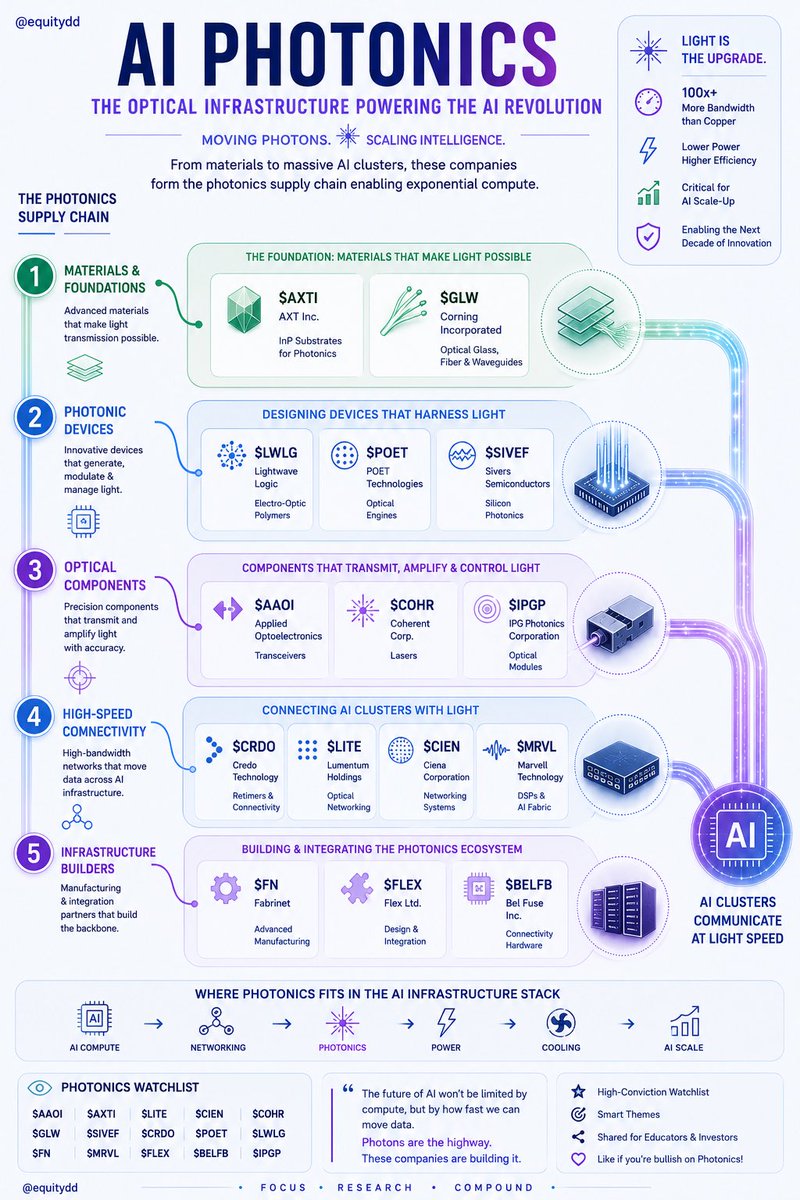

Photonics offer high bandwidth connectivity compared to copper. From materials and optical components to infrastructure buildout, below infographic goes through each layer of optical ecosystem.

$AAOI $LITE $GLW $AXTI $POET $SIVEF $COHR $CIEN $COHR $IPGP $MRVL $FLEX $FN

Which stocks are you bullish on?

If we see a market pullback then this is definitely one of my top themes to watch very closely.

Thank you, Prime Minister Modiji, for inaugurating our Sanand Assembly & Test facility. Your inspirational message was greatly appreciated. Micron remains committed to accelerating volume production at this facility to meet the rising demand for memory and storage driven by AI.

Thank you, Prime Minister Modiji, for inaugurating our Sanand Assembly & Test facility. Your inspirational message was greatly appreciated. Micron remains committed to accelerating volume production at this facility to meet the rising demand for memory and storage driven by AI.

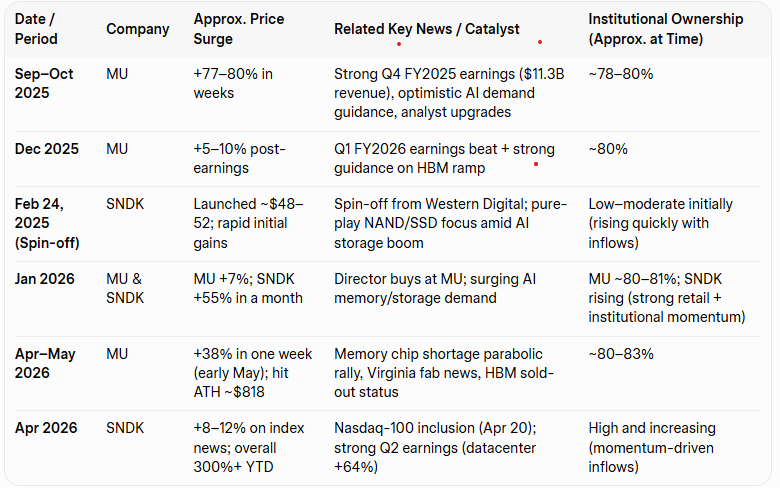

AI Memory Boom Kings $MU & $SNDK are facing Chinese headwinds

The AI infrastructure supercycle has transformed the memory semiconductor space. $MU (@MicronTech) and $SNDK (@SanDisk) have delivered insane growth, but Chinese competition (YMTC, CXMT) is ramping fast. Let's break it down.

1. $MU Growth Explosion: @MicronTech is riding HBM (High-Bandwidth Memory) for AI GPUs/data centers like never before.

-- FY2026 revenue projections top $100B+ (some estimates ~$109B–$112B), with massive YoY jumps. Recent quarters: Q2 FY26 saw ~$24B revenue in blowout reports, data center now >50% of business.

-- HBM sold out for all of 2026 (incl. HBM4) under long-term contracts — pricing power + high margins (gross margins hitting 57–75%+). AI demand creating structural shift from cyclical commodity to high-margin growth.

-- Stock: Massive rallies (hundreds % over 1–2 years), hit $600–$800+ ranges, briefly trillion+ mkt cap territory amid volatility. Analysts see strong EPS growth ($ 30s –$50s + FY26). Capacity expansions ongoing but tight supply into 2027.

2. $SNDK Reborn: Spun from Western Digital in early 2025 (~$35–$50 range). Now a pure-play NAND/flash/SSD leader.

-- Parabolic gains: Thousands of percent (up 2,700%+ in some reports), trading $1,000–$1,500+ peaks, mkt cap ~$200B territory. Q2 revenue jumps ~60%+, driven by AI data center storage demand (NAND/SSDs exploding for enterprise/inference).

-- Data center becoming largest NAND consumer — 40%+ annual growth. Focus on high-performance storage perfect for AI boom. Volatility high but momentum strong post-spin.

3. Chinese Competition Impact (YMTC NAND, CXMT DRAM): Real long-term threat, especially in consumer/legacy segments, but premium AI/HBM buffered near-term.

-- YMTC: ~11–13% global NAND share (closing on leaders), aggressive fab expansions. State-backed subsidies fueling capacity ramps.

-- CXMT: Growing DRAM share (~5%+), entering more products; both pushing tech despite US export controls (lagging in leading-edge like advanced HBM).

-- Risks: Potential oversupply in standard DRAM/NAND by late 2026–2027 → price pressure, margin compression in non-AI segments. Geopolitics (past China bans on MU, US sanctions) add uncertainty. China was meaningful % of revenue for players.

4. Net Assessment: AI demand (HBM + high-capacity storage) outpacing supply for now — sold-out books, multi-year deals, and bottlenecks give $MU / $SNDK pricing power and visibility rare in memory history. Western leaders (MU + Samsung/SK Hynix) dominate ~90%+ advanced AI memory.

But memory remains cyclical. Watch:

-- Earnings & HBM ramps

-- Chinese capacity floods

-- AI capex sustainability

-- Broader macro

Valuations elevated — huge upside if AI supercycle continues, downside on oversupply or slowdown. $MU more HBM/AI pure-play leader; $SNDK crushing #NAND tailwinds.

Not financial advice. DYOR.

#AI #Semiconductors #MemoryChips #MU #SNDK

@rossiadam's post shares details from @SpaceX's S-1 filing about its unusual lockup structure.

$SPCX - Risks vs. Opportunities

Risks:

1. Overvaluation: Buying at peak hype.

2. Supply overhang: Tiered unlocks could pressure price if momentum fades.

3. Execution/Competition: Space is capital-intensive; Starlink needs scale; regulatory hurdles.

4. Volatility: Tied to Musk/TSLA sentiment and macro (interest rates, tech rotation).

5. Retail often gets "fed" as exit liquidity.

Opportunities:

1. Long-term growth if SpaceX executes (multi-trillion TAM narrative).

2. Passive flows and scarcity could support price.

3. If you believe in the vision deeply and have high risk tolerance.

Recommendation

1. Skip the IPO allocation or day-1 buying unless you're a long-term believer okay with volatility and already diversified. The structure helps, but valuations look stretched.

2. Better approach: Wait 3–6+ months post-IPO for any pullback, better earnings visibility, and reduced hype. Or gain exposure via related public names (e.g., suppliers, TSLA) with less premium.

3. Position sizing: If you buy, keep it small (1–5% of portfolio max). IPOs aren't "sure things."

This is not financial advice—do your own due diligence, review the full S-1, and consider your risk tolerance/time horizon. Markets can remain irrational, and @SpaceX has real moats, but paying top dollar at launch is rarely optimal.

@rossiadam's post shares details from @SpaceX's S-1 filing about its unusual lockup structure.

$SPCX - Risks vs. Opportunities

Risks:

1. Overvaluation: Buying at peak hype.

2. Supply overhang: Tiered unlocks could pressure price if momentum fades.

3. Execution/Competition: Space is capital-intensive; Starlink needs scale; regulatory hurdles.

4. Volatility: Tied to Musk/TSLA sentiment and macro (interest rates, tech rotation).

5. Retail often gets "fed" as exit liquidity.

Opportunities:

1. Long-term growth if SpaceX executes (multi-trillion TAM narrative).

2. Passive flows and scarcity could support price.

3. If you believe in the vision deeply and have high risk tolerance.

Recommendation

1. Skip the IPO allocation or day-1 buying unless you're a long-term believer okay with volatility and already diversified. The structure helps, but valuations look stretched.

2. Better approach: Wait 3–6+ months post-IPO for any pullback, better earnings visibility, and reduced hype. Or gain exposure via related public names (e.g., suppliers, TSLA) with less premium.

3. Position sizing: If you buy, keep it small (1–5% of portfolio max). IPOs aren't "sure things."

This is not financial advice—do your own due diligence, review the full S-1, and consider your risk tolerance/time horizon. Markets can remain irrational, and @SpaceX has real moats, but paying top dollar at launch is rarely optimal.

Major Price Increase Milestones for $MU and $SNDK (May 2024 – May 2026)

Here is a summary of key surge periods based on significant rallies, earnings beats, #AI/#HBM/#NAND demand news, and other catalysts.

Institutional ownership remained high for $MU throughout; $SNDK started lower post-spin and rose with momentum.

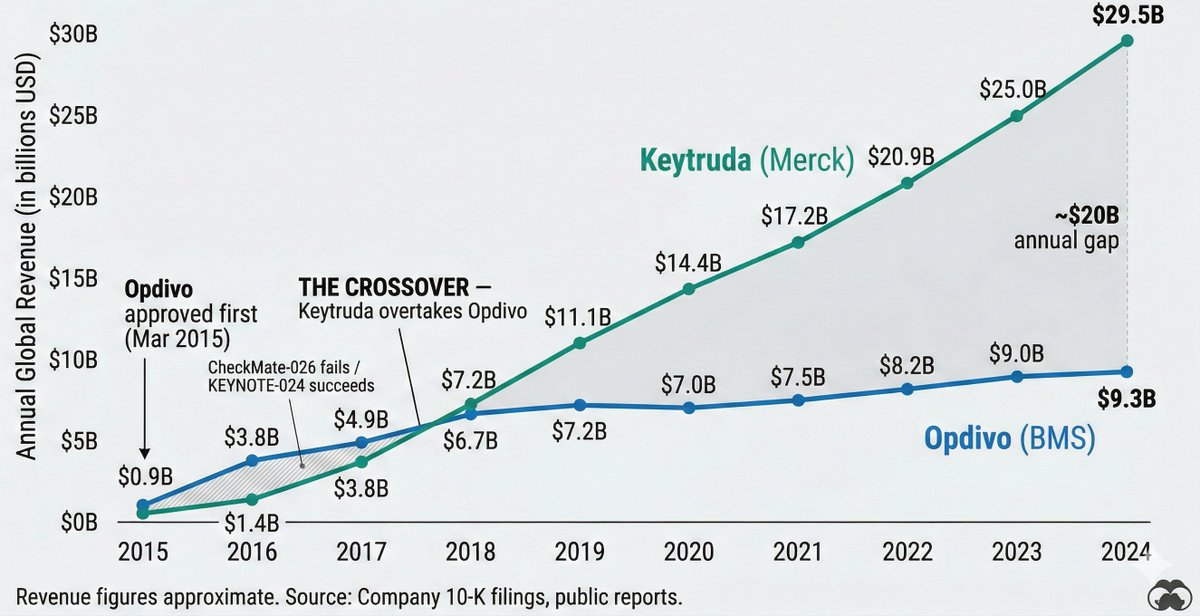

In 2012, two pharma companies faced a defining decision. One chose badly, the other well. If AI can make better decisions than humans, then given the same information it should make the correct choice

But it didn't

Ingenious experiment by @liangc_science via @adamjkucharski

https://t.co/ifJJUFrBCX

SpaceX $SPCX is officially set to go public on June 12.

This will be the largest IPO in history, & will cause a total reprice amongst the entire space sector.

These are the critical sectors amongst the space theme:

Satellite Communication & Operations

$ASTS ~ AST SpaceMobile

$PL ~ Planet Labs

$GSAT ~ Globalstar

$SPIR ~ Spire Global

$AMZN ~ Amazon

$VSAT ~ Viasat

Spacecraft & launch systems

$RDW ~ Redwire

$RKLB ~ RocketLab

$LMT ~ Lockheed Martin

$KTOS ~ Kratos Defense

$FLY ~ Firefly Aerospace

$LUNR ~ Intuitive Machines

Specialty Materials

$CRS ~ Carpenter Technology

$ATI ~ ATI Inc

$MTRN ~ Materion

$GLW ~ Corning

$PKE ~ Park Aerospace

Propulsion Systems & Fuel

$LIN ~ Linde

$APD ~ Air products & Chem

$NEU ~ NewMarket

Electronics & Semis

$NVDA ~ Nvidia

$AVGO ~ Broadcom

$COHR ~ Coherent

$LITE ~ Lumentum

JP Morgan comfirm their bullishness on AI bottlenecks:

In their 2026 Mid-Year Outlook report.

"The evidence suggests investing for a continuing AI supercycle"

"We believe the narrative around the AI supercycle has become too pessimistic"

"Industries that control the physical bottlenecks... should continue to perform well":

- optical equipment + networking

- memory

- power

With these names mentioned as AI bottlenecks:

- $NVDA

- $TSM

- $AVGO

- $META

- $SNDK

- $MRVL

- $LITE

- $COHR

- $ANET

- $APH

- $VRT

They also say to consider investment in the hyperscalers since "market participants have grown more skeptical of the companies’ expanding capex plans."

I agree, given the expanding demand/supply mismatch esp in cloud services.

I'm personally heavy on $GOOGL and have started building my $META position recently over the past few months. Separately, $MSFT is stupidly cheap rn + $AMZN also deserve consideration just cos of AWS & robotics tailwinds.

I feel a total rotation away from these names is wrong - having some small allocation at cheaper prices now makes sense for future planning.

Like, when capex slows eventually, those bottlenecked names will close up? That's still ages away per all reliable forecasts, but still...makes sense to at least build hyperscaler positions slowly at lower prices?

Overall, nothing "new" in the report that many of us on X didn't know already. And unfortunately no new names highlighted like BofA's semis report in Jan with $SOI.

But good to see institutions like JP Morgan/GS/BofA essentially confirm bullishness on upstream names in the supply chain as multi-yr beneficiaries.

The AI supercycle will last 15 years. We're in year 3.

Most investors are still buying Phase 1 names while the real money is already rotating into Phase 3.

I mapped the entire cycle into 4 phases with the tickers that matter at each stage:

The AI supercycle is the biggest investment theme of our generation. Bigger than mobile. Bigger than cloud. A 15 year structural shift that will reshape every sector of the global economy. Hyperscalers just committed $725 billion in capex for 2026, nearly doubling last year. Microsoft, Google, Amazon, and Meta each spending over $100 billion individually.

This is not speculation. I've mapped the entire supercycle into four phases so you know exactly where we are and where the asymmetric opportunities sit.

🔴 Phase 1: Already Ran (2023 to 2025)

The foundation layer is complete. $AMD ran 78% in 2025, $NVDA 39%, and $INTC just posted a blowout Q1 that sent the Philadelphia Semiconductor Index above 10,000 for the first time. Chips still power every phase but the generational entries are gone and risk/reward has compressed.

- $NVDA, $AMD, $ARM, $INTC, $AVGO, $MU, $GLW

- Semiconductors, Memory & Storage,Photonics/Optics

- Foundation complete. Still growing but priced for it.

🟠 Phase 2: Peak Buildout (2025 to 2027)

The phase most investors just woke up to. $CEG acquired Calpine to become the largest U.S. private power producer at 55 GW. $GEV up over 200% in a year. $VRT co engineering cooling for NVIDIA's Rubin architecture. $GLW up 74% YTD on optical fiber demand. Nuclear SMRs are the breakout with $OKLO, $SMR, and $BWXT positioning to power data centers directly. Still upside but the obvious names have moved.

- $CEG, $GEV, $VRT, $VST, $TLN, $ANET, $GLW, $MOD, $EQIX $OKLO, $SMR, $BWXT, $NNE

- Power/Grid, Cooling, Networking, Nuclear/SMR Peak buildout.

- Nuclear SMRs are the sleeper.

🟡 Phase 3: The Positioning Window (2026 to 2028)

Where AI escapes the data center and enters the physical world. Most will be late. Tesla converting Fremont to Optimus production, $25B capex, mass production targeted H2 2026. Rocket Lab posted record $602M revenue with $1.85B backlog. $LUNR up 47% YTD with $943M in contracts. $KTOS Valkyrie drone selected for the Marine Corps. The window to position is open right now.

- $TSLA, $RKLB, $LUNR, $KTOS, $AVAV, $PATH, $ISRG $MP, $FCX, $ALB, $ASTS

- Robotics/Autonomy, Space/Defense/Drones, Rare Earths

- This is where the asymmetric risk/reward lives.

🟢 Phase 4: Final Frontier (2028+)

The endgame. Microsoft capex $190B. Alphabet $190B. Amazon $200B. Meta $145B. Google Cloud backlog past $460B. They're building the rails for AI software dominance and AGI. Quantum still early but $IONQ and D Wave are laying groundwork. The platforms that control the software layer win the entire supercycle.

- $MSFT, $GOOGL, $AMZN, $META, $ORCL, $IONQ

- AI Software Dominance, AGI Infrastructure Decade long thesis.

- Accumulate on weakness.

💊 Key Takeaway

- Phase 2 is confirmed ($725B hyperscaler capex)

- Phase 3 is where the smart money positions nowRobotics, space, defense, nuclear

- SMR are the 2026 to 2028 trades

- Most will rotate into these names 12 months too late

15 year supercycle. Not a trade. Phase 1 ran. Phase 2 is priced. Phase 3 is where you want to be.

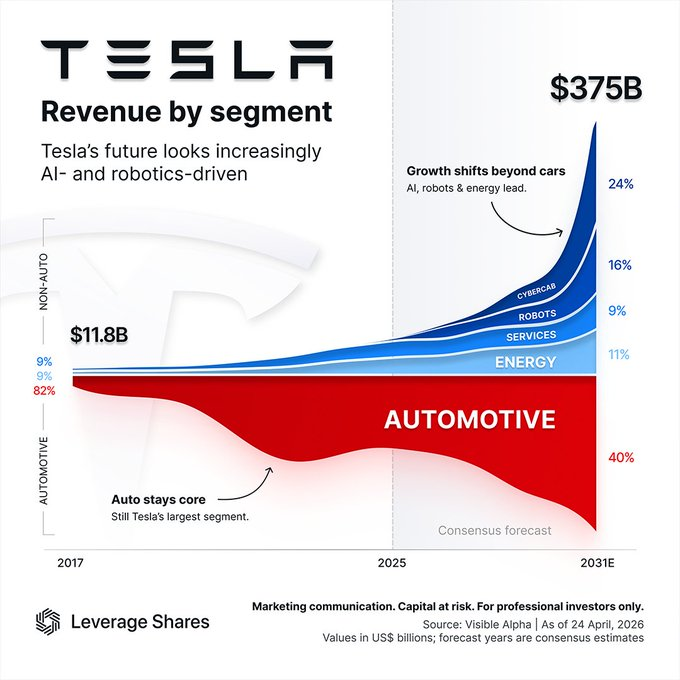

$TSLA is positioning to be the largest physical AI deployment platform by the end of this decade.

By 2031, Tesla could become a $375B revenue story where AI, robots, services, energy & Cybercab together become larger than automotive:

• Automotive 40%

• Cybercab 24%

• Robots 16%

• Energy 11%

• Services 9%

@Chamath’s framing is a sharp critique of the current hype cycle and a roadmap for what’s next. We’re moving from “AI makes developers faster” to “AI makes organizations build better software with less drama.”

Early tools got us the first 2-5x. The multiplayer layer could deliver the next order-of-magnitude improvement — especially for complex systems, enterprises, and teams larger than a handful of people. Worth watching closely. Single-player was the warm-up.

Strength of Chamath’s post: Excellent sports analogy (single-player vs. multiplayer) that makes a complex idea instantly relatable. It correctly identifies that coding is <30% of the real work in most software projects. The “institutional memory” point is spot-on — loss of context is one of the biggest hidden costs in engineering orgs.

Potential pushback: Some teams already hack multiplayer behavior with shared files, Slack bots, or agent swarms. The real challenge for any “Factory” product will be adoption, clean context ingestion, and avoiding new lock-in.

#AIFactory @xai

Yes, AI in Healthcare will lead to "de-skilling" of certain skills - but it will also unlock "re-skilling" in completely new domains. The question isn't whether that trade off is happening - it's figuring out what should go in each bucket.

When AI Scribes first came out, there was concern that not learning clinical documentation would negatively impact medical training. If the note helps clinicians learn to think through a clinical problem, organize their thoughts and present a coherent plan - what gets lost if we outsource drafting it?

At the same time, we need to recognize that humans have limited cognitive bandwidth to just keep learning more information and more skills.

Before calculators, humans had to be really good at manual arithmetic. Sure, calculators meant the average human is now worse at doing math in their heads, but look at everything that first calculators and now tools like Excel have unlocked. We developed skills to do advanced stats analysis for medical research or model out complex real-world financial scenarios in spreadsheets - wasn't that trade off worth it?

Or consider how clinicians previously had to be so much more proficient with physical exams - but with medical imaging, they unlocked this brand new skill of reading scans, which ultimately led to breakthroughs in better diagnosis and treatment. Wasn't that skill trade off worth it?

Here's the crazy thing about AI - we're now seeing AI agents that will do the heavy lifting on financial models for you. In the past, you at least needed foundational stats and finance skills to build those spreadsheet models. Now, you can just tell a Claude agent to build the model for you.

With AI clinical co-pilots, you can tell the AI to not only draft the note - but automatically suggest a diagnosis, treatment plan and orders. The question is: how much of this skill stack do we want to outsource to AI and how much do we care to keep?

What we're seeing across industries is that the experienced professional - with decades in medicine, finance, or law pre-AI - has the foundational skillset, judgment and experience to 10x their output with AI. They know what good and bad outputs look like. They can pressure test the AI.

When we think about the next generation of clinicians, it's important that medical trainees still develop the most important clinical skills - they shouldn't outsource all clinical thinking to AI before they develop judgment, taste, etc. But we can't protect that for every skill.

In some ways, it's good that AI adoption in clinical care has real friction. We need early adopters at all stages of training to tinker with AI, figure out where it fits and where it detracts value, and let the profession work it out - as it does with any new technology.

Ultimately we shouldn't just be worried about AI de-skilling - we should be equally optimistic about what new skills AI will unlock, and be thoughtful about exploring those edges to maximize AI for patient care.