Rolled forward and updated my $CSU.TO base case going into earnings after $TOI.V results

Expecting 15% YoY revenue growth ($11.6B), on $1.9B FCF2S (+28% YoY / 16% Margins - as reported) [though this understates Asseco contribution by ~US$30M]

Total capital deployed $1.5B excl Asseco or $1.9B incl Asseco (87% of FCF2S , still very soft deployment numbers). Putting the AI boogey aside, this is the most important question for me for 2026 - CAN MARK MILLER RIGHT THE DEPLOYMENT ENGINE AND TAKE ADVANTAGE OF THE BEST VALUATION MULTIPLES ENVIRONMENT FOR SAAS IN YEARS AND DEPLOY?

P/ 2025e FCF2S of ~19x is below historical ~25-40x. if acquisition momentum resumes in 2026, we can expect a re-rating to ~25x (35% return) + ~20-25% FCF2S growth type

It's so over, folks...

First Fable 5. Now GPT-5.6.

The Trump administration has reportedly asked OpenAI to stagger the release of GPT-5.6 over security concerns.

Sam Altman reportedly told staff that access to GPT-5.6 will be approved on a customer-by-customer basis.

At this rate, most of us aren't seeing GPT-5.6 anytime soon.

There's lots of chatter on "Why is Meta running a dystopian tracking experiment on thousands of its best engineers to generate AI training data, causing them all to leave?"

I think to answer this, you need a longer view of what has made Facebook successful (and not).

Apple, Microsoft, and Google all built their businesses on powerful technologies. Even after their initial famous breakthroughs (apple 2, BASIC compiler, pagerank), at least once a decade they achieved something else that greatly helped their core business (ipod, windows, gmail).

Facebook's story isn't like this. Their initial success wasn't technical, and their great achievements since then have largely been acquisitions. Their ads business was borrowed from Google, they almost missed mobile entirely, etc.

Think from Zuckerberg's perspective. Since the IPO in 2012 he's been flush with cash, but hasn't had a core, defensible edge in any technology. He has always tried to carve one out, e.g. the Facebook phone (to avoid being dependent on Google and Apple), or buying up all rival social networks.

He tried crypto (remember Libra?), robotics, and of course Oculus and VR/AR. So what's he supposed to do about AI?

His first try at LLMs didn't work, orienting FAIR and other research divisions to build open Llama models. They lacked the talent and mission, and there was too much infighting.

What would you do in Zuck's situation? The one thing you do have is a business generating ~$25B profit/year, and an army of tens of thousands of software engineers. You'd use them!

So his second try after Llama was turning money into AI. He bid for all the LLM talent at 10x normal wages for "Superintelligence", and bought Scale AI at some absurd price. That didn't seem to work.

His third try is using his other resource, his armies of good software engineers to generate a unique and defensible dataset.

Yes, it's dystopian (though the "gulag" thing... these people need to read their Solzhenitsyn). Yes, he probably will lose his best engineers. But you have to grudgingly respect his conviction and his willingness to use the resources he has. What else would you expect?

Prediction: Anthropic will not go public; they’ll raise the $100B+ or whatever they need by using Mythos to deploy capital through vehicles like Situational Awareness

That quote that $PDD “poor people’s time is not valuable” is from Pinduoduo’s founder, Colin Huang. He is quoting his mother. He is saying that even though he is super rich, his mom still seldom takes a taxi. His mom thinks her time isn’t valuable, or not valuable enough to take a taxi. So she usually takes buses.

And after I heard the quote, I started to understand why a lot of Pinduoduo’s platform design is like this. Let me give a few examples. Actually, in $SE, there are also a lot of things like this.

Pinduoduo’s most famous traffic/acquisition strategy is “砍一刀,” which is to let users invite others to chop down the price. It’s very annoying and time-consuming.

This kind of thing doesn’t work well in wealthy cities. People are less willing to bother someone just to get a very small gift. But it works perfectly for people in poor rural areas.

Another example is its DuoDuo Groceries logistics network. The group leaders who do the last-mile work get paid insanely low. Oftentimes, less than 0.05 per package. But the people that Pinduoduo is attracting aren’t the ones that see this as a job.

They are the housewives and the old people who feel like, “I can let Pinduoduo send my groceries to my house, and I will also get a little bit of extra money.”

The money that Pinduoduo pays the last-mile group leaders is way less than minimum wage. But for the people that Pinduoduo is attracting, their time doesn’t mean anything.

The third example is that, in DuoDuo Video, Pinduoduo’s short-video service, you can earn some money just by looking at the videos. The money is also obviously very little, but for the people who look at it, they would think it’s extra money. It’s fine to look at it!

This doesn’t make much sense in a wealthy country. So, there are very few services that provide this kind of service. But in China, both Douyin and Kuaishou have special versions of their apps for this kind of user. If I remember correctly, Facebook also has it in some countries.

Another interesting thing is that the “check-in” feature of eCommerce apps to earn cashback is also one of these initiatives, which is more popular in Western countries.

But all in all, when you look at Pinduoduo’s platform design and philosophy, “poor people’s time is not valuable” is one of the core design ideas in Pinduoduo’s operation. There are a lot more examples!

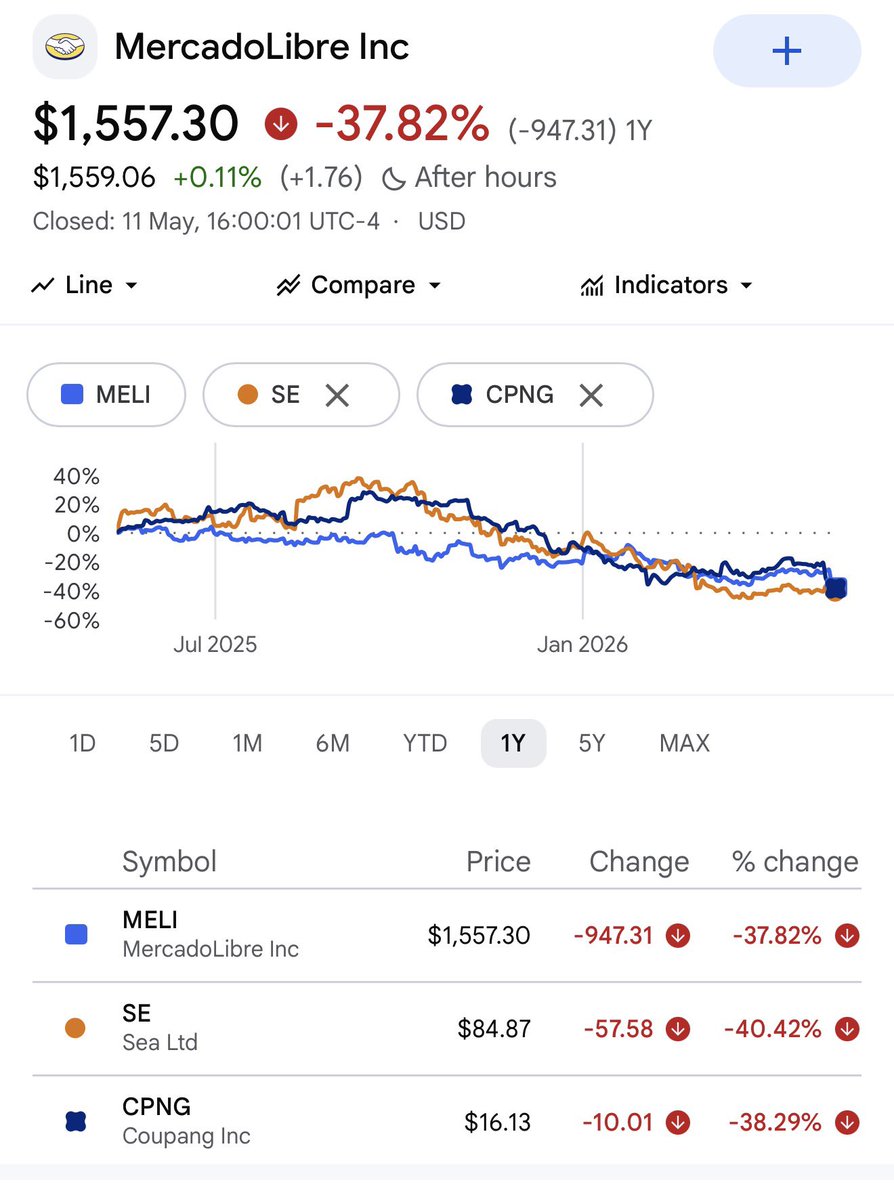

$CPNG, $SE, and $MELI, all major e-commerce and digital commerce platform companies, now share eerily similar charts and are each down roughly ~40% over the past 12 months, signaling there may be a much bigger problem with the sector than people currently understand.

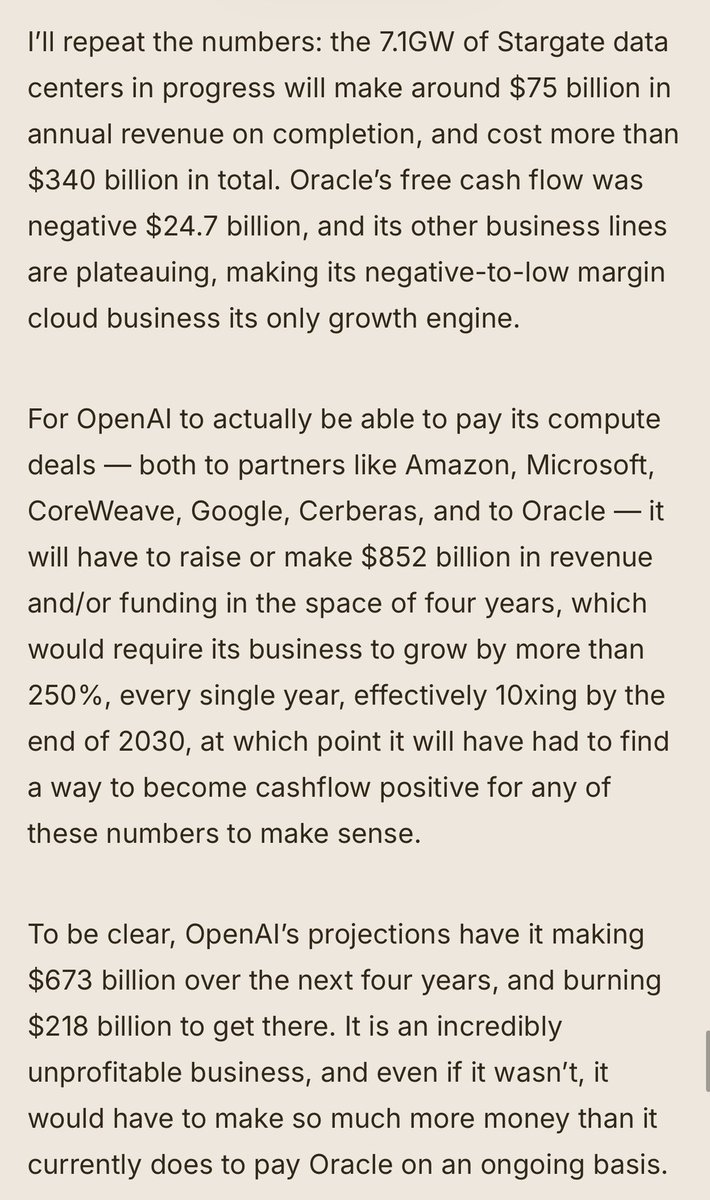

I don’t think people realize the ramifications of OpenAI’s revenue growth slowing. Oracle is building about $348bn in data centers and needs OpenAI to pay it $75bn a year in revenue to keep up with the costs. Ellison has bet everything on this.

https://t.co/kfIi6umbcS

@NicoperJES The thing about TEMS is management fucks with you. If you say you’re PEMS but you do TEMs best of both worlds.

$BRK brands itself as Permanent owner but nowadays is mostly a growthy fund no?

I tried refining about it four times… essentially put in all my articles as a pose starting point, then loaded up all the cos public filings, then asked it to write in my usual 3-4 heading frame work (history,recent history,risks and opps,valuation). The point being the prose was unreadable

![DigBabby's tweet photo. Rolled forward and updated my $CSU.TO base case going into earnings after $TOI.V results

Expecting 15% YoY revenue growth ($11.6B), on $1.9B FCF2S (+28% YoY / 16% Margins - as reported) [though this understates Asseco contribution by ~US$30M]

Total capital deployed $1.5B excl Asseco or $1.9B incl Asseco (87% of FCF2S , still very soft deployment numbers). Putting the AI boogey aside, this is the most important question for me for 2026 - CAN MARK MILLER RIGHT THE DEPLOYMENT ENGINE AND TAKE ADVANTAGE OF THE BEST VALUATION MULTIPLES ENVIRONMENT FOR SAAS IN YEARS AND DEPLOY?

P/ 2025e FCF2S of ~19x is below historical ~25-40x. if acquisition momentum resumes in 2026, we can expect a re-rating to ~25x (35% return) + ~20-25% FCF2S growth type](https://pbs.twimg.com/media/HCC9Xu-bkAAjdrk.png)