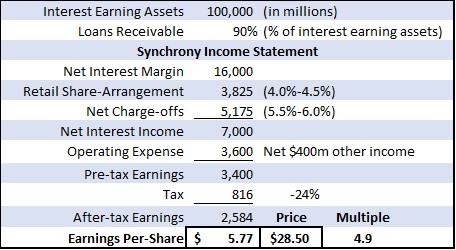

$SYF Quick pitch: bank that trades at 1.25x tangible book, has de minimis deposit flight risk, & targets (earns) a 28% return on tangible equity. While perennially discounted in relation to business quality, SYF is now exceptionally cheap (less than 5x earnings).

Alcohol is the new tobacco continues--Cuervo now off 70% over the last five years. What's wild is that it isn't even levered—lost 70% of its enterprise value since 2021.

Nu is more mature in its core market w/penetration at 60% of adult population, so heavy lifting is coming from newer & less proven foreign markets. Nu is also operating closer to peak efficiency, so additional operating leverage will only provide a modest tailwind to earnings.

$INTR has good visibility into another 300 bps of ROE expansion thru year-end. At this point, it will trade at 5.5x EPS & 4x FWD. It should also still be growing EPS at 35-40% per year. Combine this w/multiple expansion & co offers a 3-4 bag opportunity over the next few yrs.

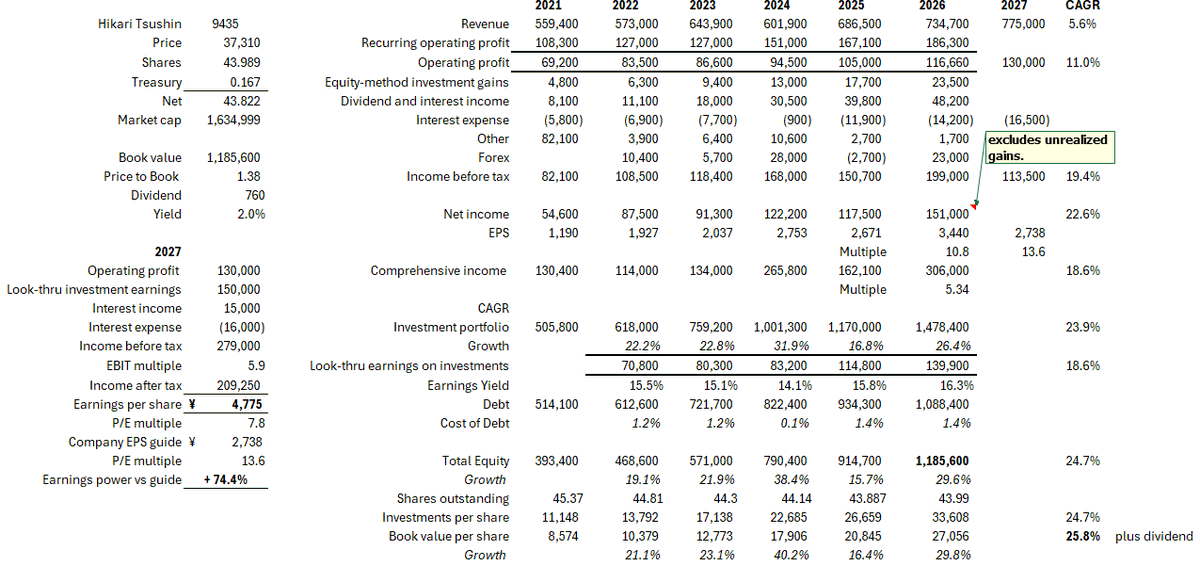

$9435 Hikari still a great way to play value in Japan. Just ran a 30% ROE & you can buy for 1.3x materially understated book. 27' ¥2,738 EPS guide is nonsensical. Co is operating biz + investments. Better framework: value like BRK:¥4,800 EPS, or 7.5x vs 13.6x based on guide. 1/n

Then to the extent that the CEO has investing skill, the investment portfolio return potentially runs higher than its look-thru earnings. Book value has continually benefitted from this: 15-year CAGR is 19% excluding dividends, 5-year CAGR is 28% when dividends are included.

A look-thru investment earnings figure of ¥150B for 2027 seems reasonable. Interest income mostly offsets interest expense. Effective tax rate is generally ~25% range. So, pay sub-8x EPS for a Japanese compounder run by an operator that actually understands capital allocation.

$ZTS has gone from trading at 10x premium to a 7x discount to Elanco in <2 yrs. Now valued on par w/ag. inputs co(Phibro) it sold low-margin feed additives business to. Cyclical & substituable low-margin additives vs branded pharma. @zoetis should fire Kristin Peck immediately.

Crazy that $Nu traded here at IPO in 2021. Business has grown 10x, model completely borne out w/near perfect execution--from loss-making to 30% ROE w/best efficiency ratio in industry, almost 3x the equity but still trades at 4.7x book.

$CLBT sub-$12 one of most intersting in SAAS space, IMO.$3B mkt cap, $534M cash-$2.4B EV. Rule of 50+ on ARR growth. $160M FCF TTM+ top-line growth 20%~$180M FCF 26, 7.5% yield on EV. Cash offsets stock comp. Spending 34% of rev. on S&M-steady-state lower if no credit for growth. Embedded w/slow-moving govt.

$SLM what multiple do you pay for dominant private student loan player w/a flat loan book running a 35%+ ROE w/a 33% efficiency ratio? Trades at 6.7x EPS. Quietly CAGR'd at 16% last 6 yrs w/market cap essentially unchanged. Sharecount ↓ by half—bought back another 6% in Q1.

$LYFT not cheap? $5.5B mkt cap, $750 M net cash, $4.75B EV. Just guided to 32% EBITDA growth in 2Q ($170M)--under 7x EV/EBITDA, no cash taxes, CAPEX low, buying stock. FCF figs ridiculously high (>$1B), but include stock-comp ($350M) & insurance reserves. Claim YOY share ↑(lie?)

DoubleU Games trying to take out minority shares of $DDI @ .5x EBITDA to EV. Suspect it gets a price bump or we see a challenge here. Minority protections in Korea fairly strong--expect appraisal rights to get exercised. Increased bid cheap b/c net cash still ~82% of EV @ $11.25

Howard Hughes $HHH is a long @ $63.50—existing business priced near depths of COVID lows, yet risk/reward profile of company has never been more attractive. 1/n

Mgmt expects ROE to reach high teens or better over time, driven by: continued improvement in expense ratio, removal of short-term pressure to write volume, & PSH’s mgmt. of Vantage's $2.8B investment portfolio.

Pershing argues pure-play specialty insurers w/similar ROEs trade >2x book value (I mostly agree). Achieving target ROE resets multiple (from sub-1.4x to >2x), layered on top of mid/high-teens book value growth= multi-year 25% IRR.