The private credit crisis is getting worse:

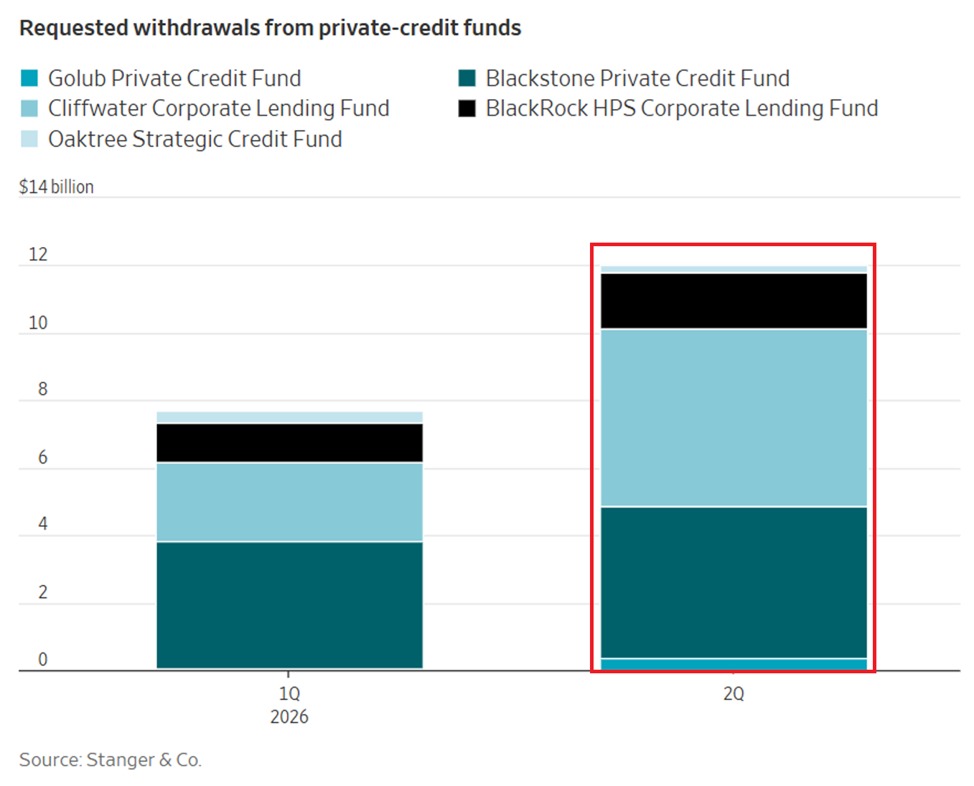

Investor withdrawal requests from large private credit funds has surged +$4.3 billion QoQ, or +56%, to $12 billion so far in Q2 2026.

The Cliffwater Corporate Lending Fund saw the largest increase in redemption requests, rising +$3.0 billion to $5.3 billion.

This was followed by the Blackstone Private Credit Fund's redemption increase of +$720 million, to $4.5 billion.

This comes as new sales of business development companies (BDCs), the primary vehicle for retail private credit investing, dropped -74% YoY in April, to just $1.6 billion, the lowest monthly total since May 2023.

In other words, far fewer retail investors are putting new money into private credit funds as confidence in the sector rapidly deteriorates.

Outflows are expected to continue, with capital projected to leave private credit funds over the next 1 to 2 years before slowing.

Stress in the private credit market is rising.

JP Morgan warns of $165,000,000,000 in global stocks selling in the next week.

The reason is rebalancing the portfolio, but it could be big enough to create a broader market correction.

China’s economic slowdown is deepening:

China’s retail sales fell -0.6% YoY in May, the largest monthly drop since the economy reopened after the pandemic in late 2022.

Furthermore, fixed-asset investment fell -4.1% YoY in the first 5 months of 2026, the largest decline since May 2020.

This follows the -1.6% YoY decrease posted in the first 4 months of the year.

Property investment led the contraction, plunging -16.2% YoY, compared with a -13.7% YoY slump in the January-April period.

China’s economy is showing several signs of weakness.