We recently updated our Investor Relations site to enhance the experience for users.

Financial filings are quicker to find, quarterly results now include visual summaries alongside the reports, and more enhancements throughout.

Take a look: https://t.co/zXBEzgsapf

AI is not able to replace something as simple as a tax software, for now.

Remember it needs to be 100% accurate not 99%. The 1% error rate (or even 0.1%) destroys the business.

So far AI didn’t prove it can do that, but yeah maybe in 5-10 years, and the model is at risk… but that’s if INTU doesn’t perfect it themselves (more likely imo).

@dcurras1 I have a feeling that is why they chose to close the Imagine acquisition only in July (Q3).. so the numbers are clearer for a full quarter and to avoid the Q1 confusion.

$LMN.V @ 12x

Revenues on track. Margins to be optimized.

$CSU style reporting with a complete disregard to short-term focused shareholders

Other companies would definitely present you all the adjusted figures wrapped in a bow, but not this one.

Just wait for the numbers in the coming quarters.

What does the post-acquisition journey at Lumine actually look like?

To answer that, we're starting a new series, ‘After Acquisition,’ tracing a company’s experience at 1, 5, and 10 years. First up: a look at Incognito Software Systems, acquired over a decade ago.

In this video, Lumine Group Founder & CEO David Nyland and key figures from Incognito's journey reflect on the acquisition and what a decade of growth has looked like in practice.

Watch the first in our ‘After Acquisition’ series: https://t.co/o55EBTRXPR

Warren Buffett on Tim Cook, after the Apple CEO announced his upcoming retirement: “What he has done with Apple could not be done by anybody I’ve known.”

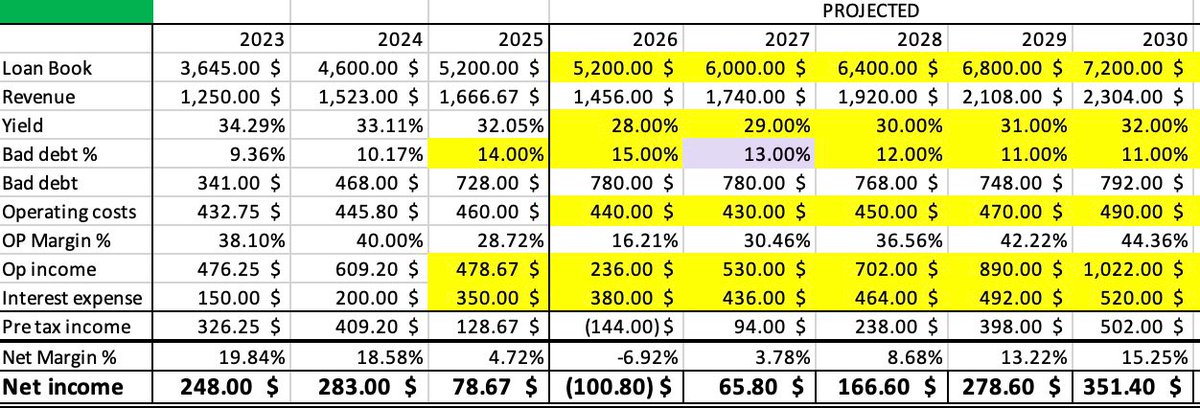

$GSY $GSY.TO ugly results but largely expected

The one big positive here supporting the turnaround thesis:

Net charge offs

Q1 guidance: 17.5% to 18.5%

Expected to decrease from 23.8% in the fourth quarter of 2025 to the mid-teens for full year 2026; improvement is expected as the year progresses.

..this means NCO’s are projected to end 2026 on a sub-14% run rate

= profits in 2027

Is there another example where CSU steps in to restructure the debt part as a minority shareholder ?

I agree with your analysis btw, also for adj ebitda.

I was thinking csu can pay down that debt and refinance from the mother company at low rates, and then assess the value csu would pay for the whole biz.

@WSB_redditor@andrew1corpora1@JustinvestToday Either you use EV, and net operating income, or market cap and net income.

Considering debt is pretty much permanent and used to generate revenues, I prefer to use net figures.