Your agent is only as good as the data it can reach.

drillr is the MCP for fundamental stock research — one server, any client that speaks the protocol. Ask in plain English, get real data back instantly.

SEC filings, analyst signals, fundamentals & valuations — plus alt-data the screens don't have. 10,000+ tickers, one call.

SpaceX just filed to go public. Everyone's resharing the headline.

We pointed our agent at drillr and asked the better question — which listed companies does it ripple to?

One query mapped every name exposed: its rivals, its backers, and the supply chain that quietly bills it. The kind of companies you'd never have screened for.

$RKLB $GOOGL $RTX

PYPL beat. Stock fell -7.74%.

This morning: down another -0.39%. No bounce.

This is the 4th consecutive PYPL earnings day to close red. The Street has 0 Buy ratings out of 8. P/E is 8.69x.

The cheapest cash cow in payments doesn't bottom on beats. Here's why.

$PYPL

AMD just guided +32% next quarter.

The OpenAI ramp isn't in that number.

It's sitting in 3 footnotes — penny warrant, +$3.9B unconditional commitments, $4.4B WIP — none of which roll into reported revenue until H2 2026.

$AMD $NVDA $AVGO

OpenAI just missed revenue + user targets (per WSJ yesterday). CFO Sarah Friar warned capex may outpace revenue. AI-linked names sold off — $ORCL closed -4% (intraday -7%), $AMD /$AVGO -4% on the news.

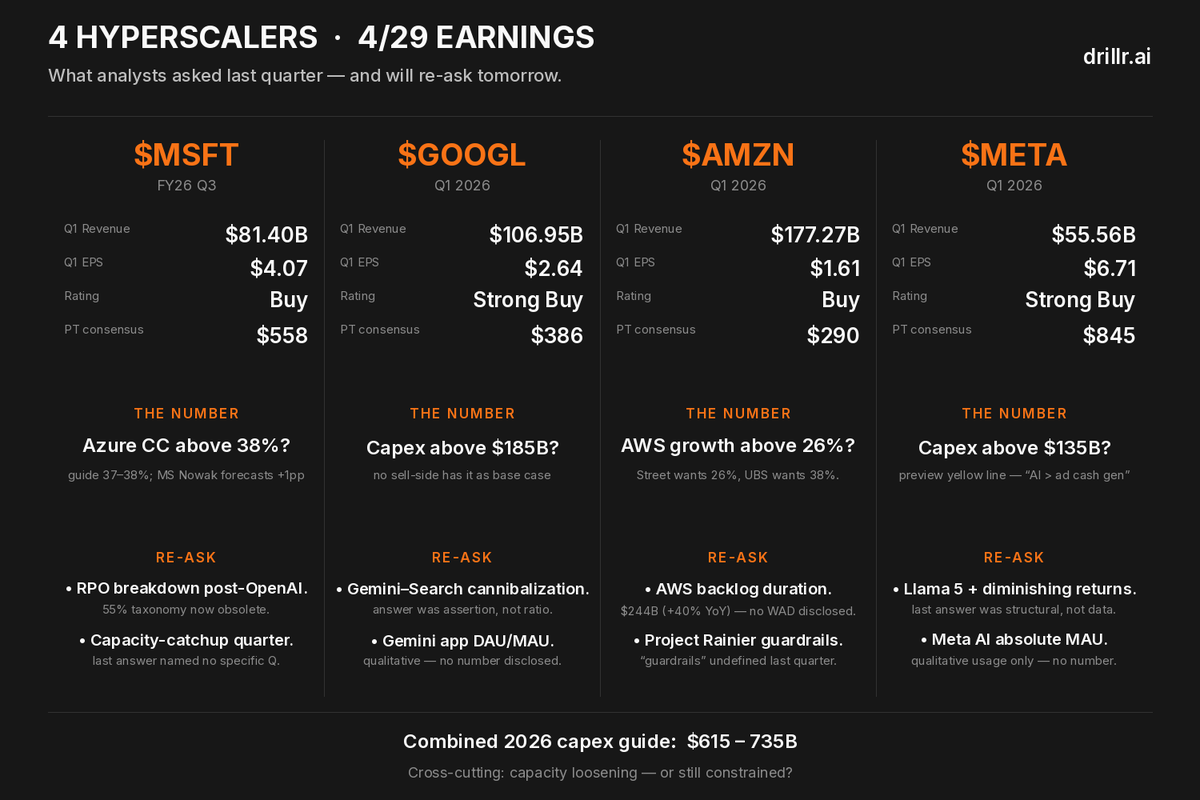

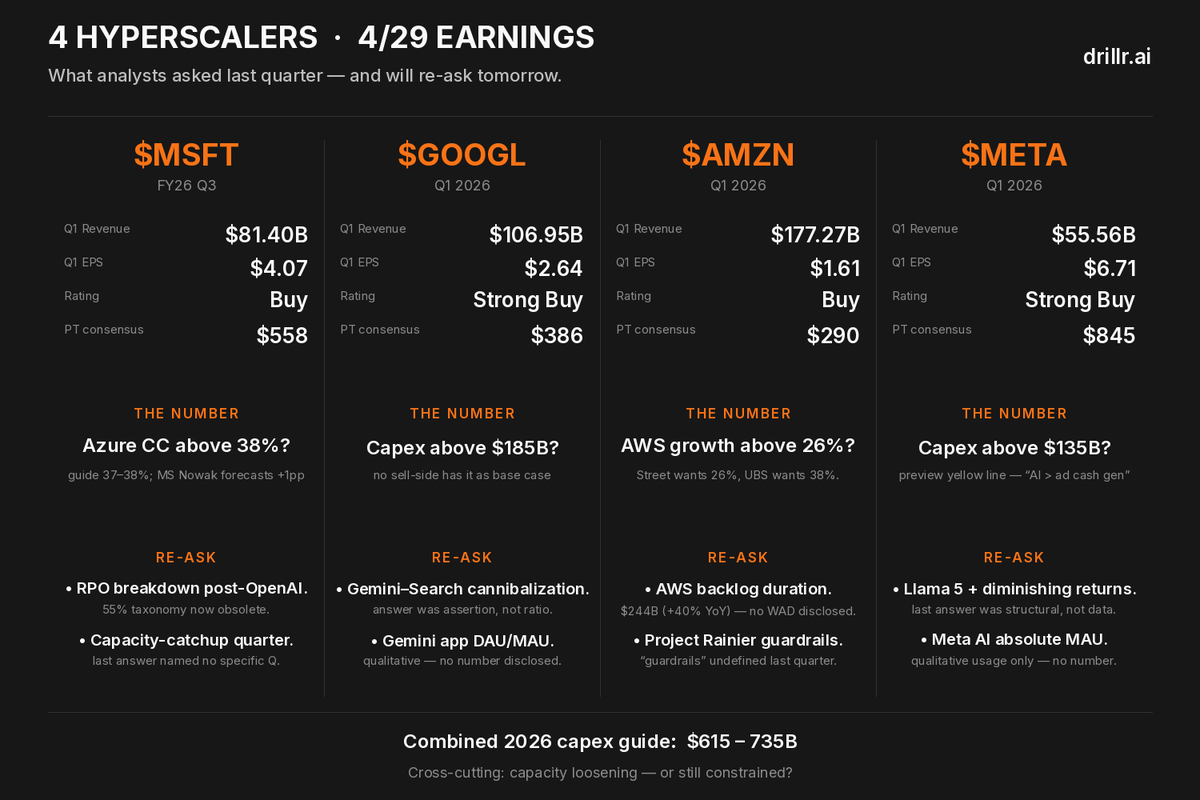

Tonight's 4 hyperscalers all report into this exact question: is the AI capex narrative sustainable, or is OpenAI's slowdown the first crack?

4 hours until the prints. The single-question scorecard — one for each company, on the KPI the market is most sensitive to:

$MSFT — Does Azure CC growth crack 39%?

Guide is 37-38%. Morgan Stanley's Brian Nowak openly forecasts ≥39%. Capacity loosening = growth ceiling lifts.

$GOOGL — Does Cloud growth crack 48%? Does capex hold at $185B?

Pichai literally said "capacity and supply chain" is what keeps him up. Higher capex = problem persists. Same capex + higher Cloud growth = constraint loosening.

$AMZN — Does AWS growth crack 26% (consensus)?

24% was 13-quarter high. Consensus 26%, UBS bull 38% — widest spread of the four. Below 26% = "13Q peak was the peak."

$META — Does capex hold at $135B? Multiple previews aligned on $135B as the yellow line — above it = "AI buildout already outpacing ad business cash generation." Breach extends the PT compression already underway in April.

The cross-company tell: combined 2026 capex guide is ~$615-735B. If any name raises capex tonight without a revenue raise, FCF compression narrative gets fresh fuel.

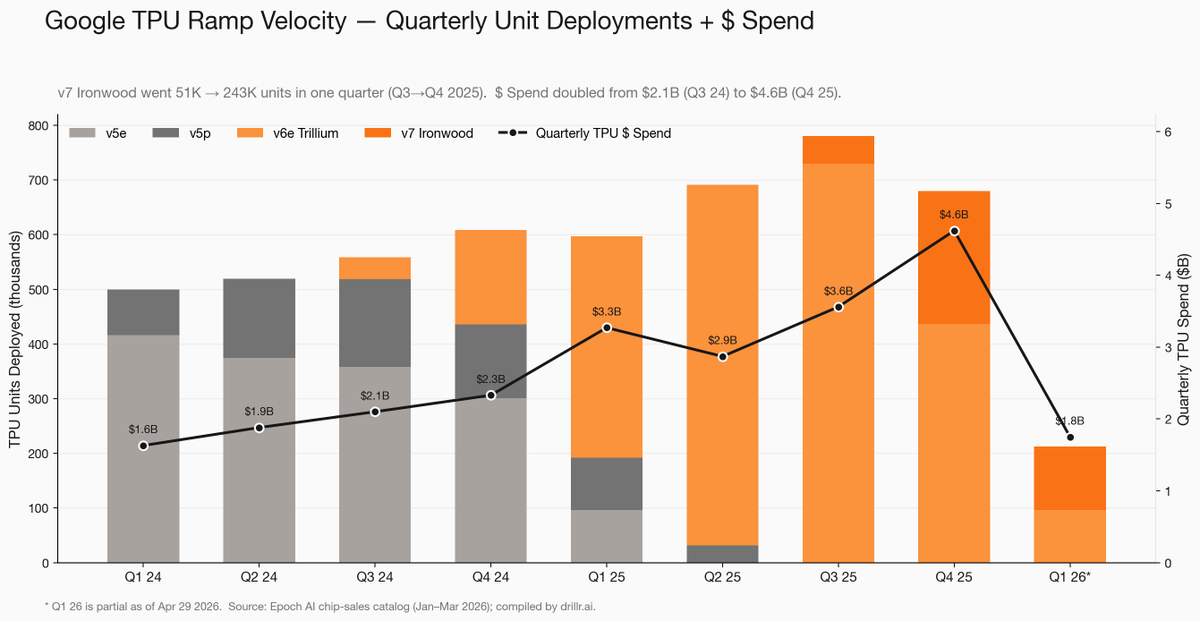

$GOOGL reports tonight. Everyone is asking about Cloud growth.

The question that's already been answered, in 3 separate filings nobody connected:

→ $AVGO Q1 FY26 8-K: Google TPU + Anthropic deal "supercharge revenue visibility." HSBC: Google TPU = 78% of AVGO's 2026 ASIC revenue ($22.1B), at $13K/chip vs $5K for other ASICs.

→ $MRVL FY25 Q4 10-Q Note 13 (filed Dec 3): $87 warrant to "a customer" for 1.0M shares, vesting on revenue milestones, 6-year term. Customer not named. Timing + Celestial Photonic Fabric (scale-up interconnect) + Google's 4/22 TPU 8 announcement = strong inference: customer is Google.

→ $CLS Q1 2026 print (yesterday): "preferred manufacturing partner" for Google TPU systems. 2026 revenue guide $17B (+37% YoY). Capacity expanded 5x. Google plans to deploy ~3.3M TPU units in 2026.

Tonight's question isn't only "will GOOGL beat?" — it's also:

The footnotes are the leading indicator. The second-order names already ran:

→ $CRDO +93% from 4/2 to 4/24. $ALAB +82% over the same window. Both gave back -7%/-8% on the OpenAI WSJ news Mon/Tue.

If GOOGL's print confirms the TPU trajectory tonight, the question stops being "who's next" — it becomes "is the second-order leg done, or does the print extend it?"

drillr lined up the 3 footnotes — same TPU build-out, 3 different SEC filings.

P.S. — the highest-conviction call in the layer map is $MU . Q2 FY26 10-Q (filed 3/19): gross margin 74% vs 37% YoY, revenue +196% YoY. Micron's own MD&A calls the HBM mix "structural." Bull case isn't a forecast — it's printed. fwd P/E 11.6x.

24h later: WSJ reports OpenAI missed revenue + user targets. $ORCL -4% close (intraday -7%), AI infra names sold off across the board.

The $250B Azure contract floor I flagged yesterday just turned into the most important question on tonight's $MSFT print:

The floor is contractual. OpenAI's actual demand is not.

What % of MSFT's $625B RPO is OpenAI? Hood's answer tonight is the highest-information disclosure of the year.

@amitisinvesting For everyone showing up at 4PM ET tomorrow 👇

If any one raises capex tomorrow without a

corresponding revenue raise, FCF compression

gets fresh fuel.

If revenue raises along with capex, demand

is real.

Per-name watchlist ↓

Worth noting POET's own 20-F has warned about this every year since 2020 — risk factors literally say "customers may cancel POs without significant penalty." The cancellation right was always there in standard PO terms. MRVL didn't even need to invent the breach-of-confidentiality argument; it was a clean exit baked into the contract structure.

The trigger was the CFO interview. The cause was on file 5 months earlier.

MRVL's Dec 3, 2025 10-Q (Note 13): a warrant issued

to "a customer" — 1.0M shares at $87, vesting on

revenue milestones with MRVL's silicon photonics

over 5 years.

That customer is now equity-incentivized to ramp

MRVL's stack, not POET's. Cancellation was structural

— the CFO interview just pulled timing forward 1-3

quarters.

POET Technologies had its worst trading day on record yesterday.

→ Open: ~$14

→ Intraday low: $7.00

→ Close: $7.20

→ -47.4% on the day

The headline says "CFO blunder."

The actual story is in Marvell's 10-K Note 13 — filed 5 months ago.

When Marvell announced the Celestial acquisition on December 2, 2025, they ALSO issued a warrant to "a customer" for 1.0 million shares at $87, vesting on revenue milestones over 5 years.

That customer is now equity-incentivized to consume Marvell's photonic stack.

Why pay POET to ship optical engines into your product when triggering this warrant runs through Marvell's own silicon photonics engine?

POET losing this customer was structurally inevitable from the moment that warrant was signed. The CFO's Stocktwits interview was the trigger, not the cause.

Full breakdown — every filing date, the warrant math, the $0.3M revenue vs $5.5B integrated stack mismatch👇:

$POET $MRVL $NVDA

Yesterday $MSFT and OpenAI announced "the next phase" of their partnership.

MSFT plunged -5% intraday, then closed -0.37%.

That intraday → close shape is the tell: someone started reading the actual terms during the trading day.

We pulled MSFT's last 6 quarters of SEC filings on https://t.co/rF3DszrG2s.

The "exclusive" word disappeared from MSFT's own filings two filings ago. The $250B Azure contract has been booked in RPO since January 28. The AGI clause was already gone in the October Note 17.

Most of yesterday's "news" was already in MSFT's filings 6 months ago.

The market traded a surprise that wasn't a surprise.

Full breakdown — every disclosure timeline, the RPO walk, the AP-bound capex tell, the OpenAI HLBV math 👇: