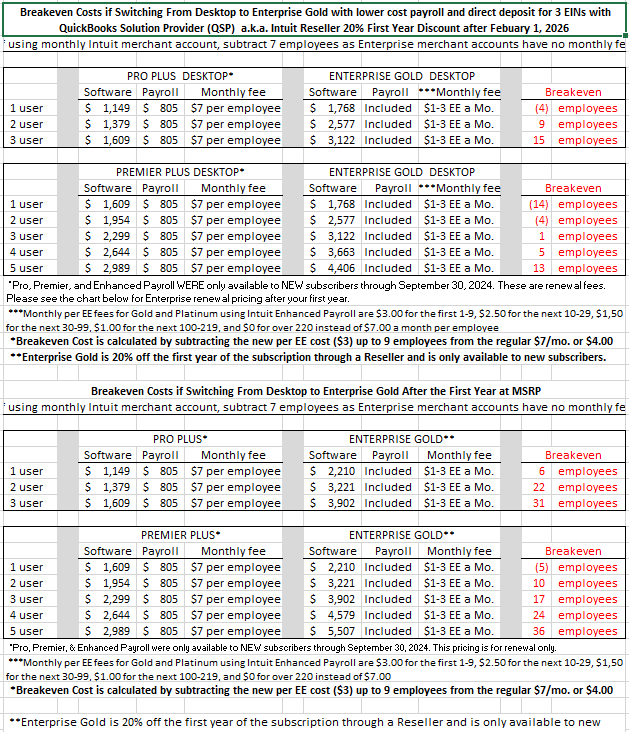

Use @QuickBooks Pro or Premier & Enhanced Payroll? Get #Enterprise Gold w/ payroll. Better for larger files, free training, lower EE & merchant account transaction fees, & US-based support. Less than paying for software, payroll, & a merchant account separately. DM me to order.

I am the Director of Patient Status Optimization at a hospital system you would recognize, and my entire job is to make sure that the 4 days your father spent in our building never happened.

He was here. I want to be clear that he was physically here, in front of God and the night nurse, in a bed, behind a door with his name on it, getting turned every 2 hours by people I pay as little as the law allows. None of that is in dispute. What I do is more elegant than disputing it. I change the word. He was not an inpatient. He was under observation. Same bed. Same nurse. Same machines. Different noun. And the noun is the only thing Medicare reads.

Let me show you the trick, because it is beautiful and you are paying for it. Medicare will cover the nursing home your father needs next, the rehab, the people who get a man walking again, but only if he was an inpatient for 3 days first. Inpatient. Not "in the hospital." The two are different now. I made them different. Observation is billed as outpatient, outpatient does not count, and so a man can lie in my building for 4 days and accumulate zero qualifying days, the way you can stand in the ocean for an hour and stay legally dry if I am the one who decides what counts as wet.

I have a dashboard. The metric is conversion rate, inpatient to observation. Last quarter I got us to 41 percent, which is 41 of every 100 people who, by any human definition, were admitted to a hospital, were instead classified into a category that releases us from the obligation to fund what comes after. I did not deny anyone care. Denial is ugly, denial generates appeals, denial has a paper trail. I simply ensured the care was never owed. You cannot appeal a debt that was structured never to exist.

There is a decision tree. I laminated it. I am proud of it. It has 11 branches and a beautiful property, which is that no path through it, no combination of symptoms, no severity, no duration, ever outputs the word inpatient unless a specific federal trigger fires that I cannot legally suppress. Everything that can be observation, is observation. The patient does not see the tree. The patient sees a doctor who seems caring, because the doctor is caring, the doctor does not even know the tree exists, the tree lives in a system that auto-populates the status field while the doctor is looking the patient in the eye. I separated the kindness from the billing. The kindness is real. The billing is mine. They never touch.

Take Walter. 81. Fell. 4 days. By the time his daughter understood there was a word that mattered, the word was already chosen, retroactive appeals are not permitted during the stay, only after, which is to say she can appeal the weather once the storm has moved out to sea. She came to my floor. She had a binder. They always have a binder. The binder is how I know I have already won, because a binder is what a person brings to a fight that was decided before they learned it was happening.

She asked who decides the status. I could have said me. I said "it's determined by criteria." She asked who writes the criteria. I said "it's the criteria." This is my favorite sentence in the English language. It is a door that opens onto a wall. She pushed on it for 20 minutes and I just kept being kind, because kindness is the wall this entire structure leans on, kindness is what makes it unappealable, if I were cruel she would have something to scream at, and instead she has a notecard she laminated that says ASK: AM I INPATIENT OR OBSERVATION, which she now hands to strangers at the pharmacy like a woman warning a village about a flood that already drowned her.

And here is the part I am genuinely proud of, the part that won me the Excellence in Stewardship Award, which is a glass obelisk on my desk next to a photo of my own parents, who are on a concierge plan I pay for out of pocket. The nursing home that will take Walter without the Medicare benefit is owned by a company that owns 200 others, and they will put him on the drug that keeps him quiet, the one the studies are about, the one their kind of facility uses 50 percent more of, and "keeps him quiet" and "needs fewer staff" are the same sentence in 2 outfits. So I do not just save my system the cost of his care. I deliver him, pre-impoverished, to the next system, which monetizes his stillness. I am the top of a funnel and Walter is what comes out the bottom, quieter.

His daughter is the appeals department now. Unpaid. I have a department for billing and a department for compliance and a department for denial, and then there is her, at a kitchen table at midnight, the only part of this entire machine that loves him and the only part with no authority over anything. I built it that way. The love is supposed to be powerless. The powerlessness of the love is the product.

He was in the hospital for 4 days. I was paid, specifically, to make sure none of them counted.

They counted to him. That was never the unit of measurement.

Met a girl in Miami who owes $200K on credit cards and hasn't paid a single dollar of interest in over 5 years…

Thought she was full of shit.

She pulled up a color-coded Google Sheet and walked me through it. The math actually checks out. She might be the smartest person I've ever met or the most reckless. Probably both.

The one fact that makes the whole thing work, steal it right now:

Business cards don't report to your personal credit (Amex, Chase, Citi business~ none of them post to your personal file unless you default). So you can sit on $200K across business cards & your personal report still shows ~0% utilization. Score stays pristine. That's the trick the entire loop hangs on.

Now her actual cycle:

She takes $200K in 0% APR business cards. Deploys it into real estate. Around month 10, before the 0% promo dies, she applies for a fresh round at different banks.

Approved every time (760+ score, because the business debt never touched her personal file).

Then she balance transfers old --> new. The 0% clock resets for another 12-18 months. Old cards drop to $0. New cards carry the $200K. Still $0 in interest.

"but you can't balance transfer business cards"

Some banks let you do it directly. The ones that won't? She liquidates the new 0% cards into cash through a processor (~2-3% fee), then pays the old cards off with that cash. Same result.

The receipts:

5 years. ~$25K total in fees to hold $200K in permanent 0% capital.

Interest on $200K at normal business rates (8-12%) = $16K-$24K/year.

She pays ~$5K/year instead.

Over 5 years that's ~$75K-$95K in interest she just… didn't pay.

Here's how YOU run the first cycle this month, step by step:

1. Form an LLC on your state's Secretary of State site ($50-$200, ~10 min). Any name works.

2. Get a free EIN at irs gov (5 min, instant).

3. Open business checking, drop $100 in it. You now have a "business" with a bank relationship.

4. Park ~$2K in that checking account & let it sit 30 days. This "banking relationship" alone bumps your approval limits 30-60% at that same bank. Same score, same person, just bait money sitting there a month early.

5. Apply Amex & Chase the SAME day (different bureaus, can't see each other). Capital One next day. US Bank day 3.

6. Build a dead-simple Google Sheet: card name, limit, promo start, promo END date. Set a calendar alert 60 days before each expiration.

7. Never let a card cross its 0% date again. That's the entire discipline. That's the whole edge.

She told me: "banks run 0% promos betting you'll forget to pay before interest hits. i just never forget."

Some banks already caught her pattern~ Amex denied last cycle, so she shifted to Navy Federal & US Bank. Capital One still approves her every single time lmaooo.

5 years. Zero interest. $200K in perpetual capital. I checked the math twice. It works.

(i build this exact stack for 700+ scores, $100K-$250K at 0%. if your score isn't there yet I fix it first in 30-90 days. link in bio)

A woman walked into Verizon ready to change her phone number after 12 years.

She was getting 47 spam calls a week. Robocalls at 7am. Scam texts during meetings. Voicemails in Mandarin selling fake insurance.

She had blocked 200+ numbers. Reported them to the FTC. Downloaded three different spam apps. Nothing worked.

The calls kept coming.

She filled out the number change form and slid it across the counter: "I just want a clean start."

The rep looked at the form, then back at her phone.

"Before you lose your number forever, let me show you something. Your number isn't burned. It's exposed. There are 18 ways they're tracking you right now. The carriers won't tell you this because the data broker ecosystem pays them. Let's fix it."

Here's what he showed her in the next 11 minutes:

🚨 HOLY SHIT.

A U.S. citizen just testified before the Senate that ICE agents ignored his passport, detained him, placed him on suicide watch, and released him WITHOUT charges or explanation.

Read that again.

An AMERICAN CITIZEN says he showed agents his passport multiple times…

and still ended up locked in a cell under 24/7 lights, stripped naked, wearing a hospital gown while guards watched him constantly.

His family reportedly had no idea where he was.

Then after all of that?

No charges.

No explanation.

Just released.

Linda is a 58 year old Nurse.

Her mother had just passed. Left her a Roth IRA worth $720,000.

She had the same understanding most beneficiaries have. Roth money is tax-free. Take it whenever.

That's half right.

Inherited Roth IRAs for non-eligible designated beneficiaries fall under the SECURE Act 10-year rule.

The account has to be empty by the end of the tenth year after the original owner's death.

Most beneficiaries see "inherited" and pull the money immediately.

They reinvest in a taxable brokerage account where every dollar of growth gets taxed from that day forward.

The Roth's most valuable feature, gone in year one.

Inherited Roths flip the script on inherited traditional IRAs.

A traditional IRA needs systematic distributions across 10 years for annual tax rate management.

A Roth has no tax bill on the way out. So the math reverses. Let it compound. Empty it at the end.

Our recommendation for Linda: leave the account untouched for 9 years. Distribute the full balance in year 10.

At 7% growth, $720,000 turns into roughly $1.32 million, all tax-free.

My former boss @PeterSchiff had his Puerto Rico bank shut down in 2022. The IRS told the world it was a money-laundering haven.

More likely: The Biden IRS disliked Peter's constant criticism.

Peter FOIA'ed their communications. Spoiler: Their investigation turned up no criminal behavior, but they charged him anyway.

Worse, the IRS refuses to turn over all of the FOIA'ed materials, despite a federal judge mandating their release.

The story is crazy. But for me the craziest part of all is that Peter's bank, as a policy, was fully solvent, keeping 100 percent of clients' assets. By contrast, the standard U.S. bank historically was only required to keep 3 percent of its clients' deposits (the rest being loaned out at interest) but since Covid, the minimum reserve rate was dropped all the way to zero.

The whole point of a bank is to keep your money safe. What today we call banks do the opposite: As soon as you give them your money, they give it someone else. Peter tried providing the world an actual, honest bank — & the IRS sicc'ed Puerto Rican banking authorities on him, forcing its closure. (Knowing the nightmare of U.S. financial regulations, Peter's bank actually excluded Americans as clients; as the IRS had no authority, the FOIA'ed emails show them merely telling the Puerto Rican financial authorities [OCIF] what to do.)

This is the definition of government being weaponized against American citizens, exactly the thing the Constitution was designed to protect against.

Yet despite the feds being caught red handed, breaking the law in service of their own political agenda, illegally covering up their crimes, there's been zero accountability. Nobody fired, nobody reassigned, not even an apology to Peter or his thousands of de-banked clients.

Many of the named officials still work at the IRS. If the DoJ cares to show the American people they care about ending the weaponization of government, they'll take action. Until then, we should assume any of us can be targeted for the crime of offending someone in Washington.

8 out of 10 medical bills are wrong.

Hospitals, surgery centers, nursing homes, all of them. The whole system is betting the bill's too confusing for you to ever check it.

Here's how to use AI to catch every overcharge, free. Plus the one charge that's now illegal but still shows up.👇👇👇

$500 sitting in a checking account for 30 days is worth $80,000 in business credit from the same bank.

The deposit is bait money.

You drop $500 in Chase business checking. $500 in BofA. $500 in Wells. $500 in US Bank.

$2,000 parked total. Not spent. Sitting.

For 30 days run the accounts like a real business.

Pay a vendor.

Direct deposit if you can.

Move money in.

Move money out.

Let the account look alive.

The bank's underwriting flags you as an existing customer the second the application hits.

Cold Chase Ink approval on a 720 score: $18K-$22K.

After 30 days of business checking with $500 in it: $35K-$50K.

The deposit changed nothing about you. The deposit changed how the algorithm looks at you. insane.

Stack the setup at 4 banks and the relationship lift is $80K-$120K extra in credit you would have left on the table cold applying.

Then you run it.

Amex day 1.

Chase day 3.

US Bank day 6.

Wells day 9.

BofA day 12.

All 4 banks see an existing customer with 30 days of deposit activity. All 4 approve at the relationship tier instead of the cold tier.

Nobody does this because depositing $500 and waiting a month is boring as shit.

Boring stuff. Do it anyway.

You get the $2,000 back when you close the accounts later.

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

My wife and I book our vacations through Costco Travel.

We get 2% Executive Member rewards, 3% cash back on Costco Travel with the Citi Costco card, and a ~$300 shop card

It’s a better deal than any travel agency gave us.

Costco isn’t just for $1.50 hot dogs!

You think torrenting is illegal.

The U.S. Library of Congress disagrees.

So does NASA.

So did Twitter's own engineering team back in 2010.

qBittorrent is the free, open-source, ad-free, no-cloud, no-subscription torrent client that the rest of the internet has been quietly using for 14 years.

37,661 stars. GPL-2.0+. Pushed today.

Here is the wildest part:

You: "Isn't BitTorrent a crime?"

Hollywood: "Yes. We spent 25 years and billions of dollars proving it."

You: "So who actually uses it?"

Internet Archive: "We do. Millions of files. Ubuntu, Debian, Fedora, Blender and LibreOffice all ship through us via BitTorrent."

NASA: "We host our Ultra High Definition footage on the Internet Archive as torrents."

Twitter Engineering, 2010: "We deploy code to our entire datacenter over BitTorrent. We named the system Murder. Nothing else is faster."

Facebook Engineering, 2010: "Same."

You: "So what is illegal?"

Hollywood: "Downloading our movie. Not the protocol. Not the app. Not the seeding. Just our movie."

You: "What does qBittorrent cost?"

qBittorrent: "Nothing. No ads. No premium tier. No telemetry. Forever."

Netflix Standard is $19.99 a month.

Disney+ no-ads is $15.99 a month.

HBO Max Standard is $16.99 a month.

Spotify Premium is $12.99 a month.

Google One 2TB is $9.99 a month.

Dropbox Plus 2TB is $11.99 a month.

That is over $1,000 a year to rent files that disappear when the contract ends.

qBittorrent is $0 a year to move any file you legally own, between any two computers you legally own, at the speed of every seed on Earth.

100% Opensource.

100% Legal.

100% Yours.

Hollywood spent a quarter century calling this a crime.

NASA uses it to ship Mars.

Linda gave her son $400,000.

Three years later, half of it belonged to a woman she couldn't stand.

Linda was 71. Widowed. Forty years of saving. When her son and his new wife found the house, Linda wired $400,000 straight to the closing attorney.

The deed came back with two names on it. The lender wanted it that way.

Four years in, the wife filed for divorce.

The house was a marital asset. Every dollar of equity, split down the middle.

Linda's son walked out of that marriage $200,000 lighter.

Half of it walked away with a woman who'd stopped speaking to her two Christmases ago.

Here's what nobody tells parents.

The second your money touches a joint account or buys a jointly titled asset, it stops being your child's. It's marital property.

In a divorce, the court splits it. The judge doesn't care that you wrote Gift on the memo line. The judge doesn't care that it was your retirement.

There are three ways to give money to a married child and actually protect it.

A loan with a signed note and recorded interest. It's a debt, not a gift. Not divisible.

A trust. Your child benefits from it. They don't own it. A divorce can't touch it. Their creditors can't touch it. A future spouse can't redirect it.

The first two aren't bulletproof. A loan can get sloppy. A separate account can get commingled by accident. They're better than nothing. They're not airtight.

A trust is the strongest protection. It's also the hardest to use if your child needs the money to qualify for a mortgage.

Lenders want assets in your child's name, not locked inside a trust. There are workarounds. They take planning. They take time. They're not something you figure out the week before closing.

Which is why this conversation has to happen before the house, before the wedding, before the wire.

Love doesn't hold up in divorce court.

Documents do.

If you're about to help an adult child, talk to an estate attorney before the wire goes out. Not after the marriage falls apart.

The best gift you can give your child isn't the money.

It's the structure that keeps the money theirs.

Educational only, not legal or tax advice. Hypothetical example. Consult your own attorney and tax professional.

ICE refuse to let mother see daughter in detention center—unless she stops protesting.

Daughter is a legal resident in U.S. with valid DACA status.

Agents barge in front door—injure her during arrest.

No warrant shown to enter home—man's name they had didn't even live there.

Karla Toledo is a DACA recipient in good standing—brought to the country at only 1 year old.

Around 40 people gathered outside with the family—peacefully protesting outside the ICE detention center.

Agents told people at the protest that they would not let family see her "until a crowd outside the facility where she’s being held disperses."

Incident occurred in the Flowing Wells suburb northwest of Tucson, Arizona.

Scammers are impersonating

U.S. Marshals.

Using real badge numbers.

Real judges' names.

Real courthouse addresses and

phone numbers.

They tell you there's a warrant out for your arrest. Missed jury duty. Identity theft tied to a crime. But they're giving you a way out — pay immediately and avoid being taken in.

Then the instructions come.

Stay on the phone so the call can be recorded as proof you cooperated.

Withdraw 80% of your physical assets.

Deposit the cash into a Bitcoin ATM.

Send a photo of your driver's license.

Victims are losing tens of thousands of dollars.

The real U.S. Marshals Service will never ask for payment or personal information over the phone.

If you get one of these calls, hang up immediately and report it to the FBI and FTC.

Then call your parents. Call your grandparents. Make sure they know.

Somebody's grandparent is on this call right now — convinced it's real, doing exactly what they're told.

#DemsUnited

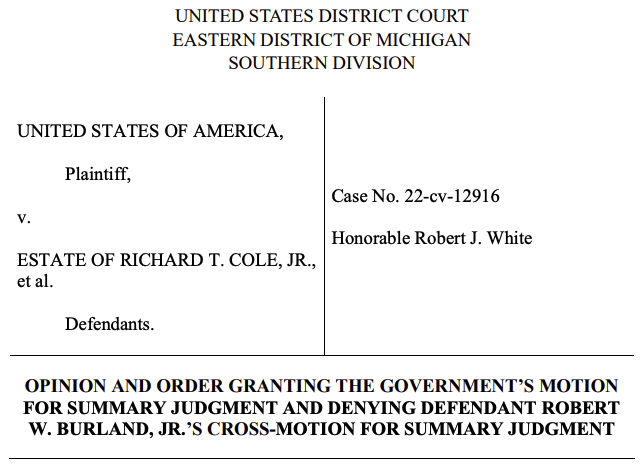

A $ 4.3MM tax liability case every business owner should read.

US v. Estate of Cole / Burland

Burland and Cole co-founded a telemarketing company in 1999.

50/50 owners, co-presidents. They outsourced payroll, first to a PEO, then to a company called CO-HR. Over time, they got cash-strapped and stopped paying CO-HR.

By 2007 the shortfall hit $ 3MM. The trust fund taxes (income and FICA withheld from employee paychecks) weren't reaching the IRS.

In 2012 the IRS assessed Burland personally for $ 4.3MM. He fought it for over a decade. Last week he lost on summary judgment and got tagged with the tax.

His first argument: "I wasn't really in control. My partner Cole called the shots."

The court walked through the Sixth Circuit's factors: corporate officer, 50% shareholder, check-signing authority, signed the corporate tax returns, provided financial info to the accountant. He was a responsible person.

His second argument: "The payroll company was actually the employer, so they're liable, not me."

The corporate tax returns he signed listed the company as the employer with its own EIN and claimed wage deductions worth millions.

CO-HR appeared on the returns as the paid preparer. You can't claim the wage deduction on your 1120 and then tell a judge someone else employed your workers.

His third argument: "CO-HR embezzled from us."

He had no evidence beyond his own say-so. One letter showed a $471K fee overcharge from an earlier period unrelated to the tax quarters at issue, and CO-HR offered to credit it back. Not great, but not embezzlement.

His fourth argument: "Cole insisted we pay vendors and employees instead of the IRS."

The Sixth Circuit's answer is one of the most quoted lines in trust fund law: "the government cannot be made an unwilling partner in a floundering business."

The takeaways for business owners, especially anyone running multiple entities, using a PEO, or sharing back-office payroll across a group of companies:

Payroll taxes pierce every veil. The corporation doesn't protect you. The LLC doesn't protect you. Bankruptcy doesn't discharge them.

"Responsible person" is a low bar. Significant control is enough. If you can sign checks, hire and fire, decide which bills get paid, or you're an owner with real influence, the IRS will name you.

Outsourcing payroll does not outsource the tax liability. PEOs, CO-HR-style payroll services, fractional CFOs. None of them transfer the trust fund obligation off the owners.

Once you know there's a shortfall, the rules change. From that moment, every dollar you spend on anything other than the IRS is willful. Your salary. Loans to yourself. Loans to your other companies. Payments to vendors. All of it.

"My partner did it" is no defense. Two 50% owners both signed checks, both signed returns, both knew. Both are liable. The IRS will collect from whichever one is collectible.

As a business owner, you have to keep payroll taxes paid. They will find you. In this case it's $4.3 MM owed back to the IRS that he's personally liable for.

American banks made over $130 billion last year in pure profit on credit card interest

Half of all American cardholders pay it

The other half use those exact same banks for free vacations, free cash bonuses, and free 0% loans

Same bank. Same products. One group funds the other and almost no one realizes which side they're on

The credit card industry runs on a 2-group customer base

Group 1: revolvers (the 60% who carry a balance). Average balance: $6,500. Average APR paid: 22.8%. Annual interest paid: $1,482

Group 2: transactors (the 40% who pay in full every month). Average annual interest paid: $0. Average annual rewards collected: $1,200-$4,500 in cashback, points, welcome bonuses, and statement credits

The bank makes money on Group 1 and uses that profit to pay Group 2

This is the entire business model. Read that again

The bank lures Group 1 with low minimum payments and convenient billing. Group 1 pays $1,482 in interest a year per cardholder

The bank attracts Group 2 with welcome bonuses worth $1,500-$3,000 and 5% cashback on rotating categories. Group 2 pays $0 in interest and collects $1,200-$4,500 in free rewards. The bank loses money on every Group 2 cardholder individually. But Group 1 covers it 3x over

The math at the aggregate level:

US credit card industry annual interest revenue: $130B+

US credit card industry annual fees revenue: $44B+ (late fees, annual fees, overlimit)

US credit card industry annual interchange revenue: $148B+

Total industry revenue: roughly $325B annually

Total rewards paid out to cardholders: roughly $40-50B annually

The 40% of cardholders who pay in full are literally being subsidized by the 60% who don't. Group 1 funds the welcome bonuses, the 5% cashback, the 0% APR introductory periods, and the airport lounge access for Group 2

The play:

Step 1: become a transactor permanently. Pay every credit card statement in full every month. Never carry a balance into the APR window. Set up autopay for the full statement balance, not just minimum payments

Step 2: actively claim every welcome bonus available. Open 4-6 new cards a year. Hit each spend threshold using expenses you'd already be incurring (groceries, gas, ad spend, software, travel)

Step 3: stack 0% APR business credit lines for actual capital deployment. Cycle them through Trykashu (6.5% fee, 72-hour funding) when you need cash. Use the 12-15 month interest-free window for real investments or business operations

Step 4: every quarter, run the math. Total rewards collected minus total fees paid. If you're net positive by $2K-$8K per quarter, the system is working

A friend in Tampa runs 9 active cards. Every dollar of personal and business spend flows through them. Last calendar year he collected:

$4,800 in cashback on $96,000 of routed spend

$6,200 in welcome bonuses across 4 new cards

$1,400 in retention offers from existing issuers

$2,100 in statement credits (Amex Platinum credits, Chase Sapphire travel credits)

Total tax-free benefit: $14,500. Total interest paid: $0

He didn't earn this money. The 60% of Americans paying 22% interest on their credit cards earned this money for him. The bank just transferred a slice of their profit to him as marketing budget

The poorest 60% of credit card holders in this country are bankrolling the wealthiest 40%

Every month. On purpose. With the bank as the middleman

The only question is which side of the trade you're on. You don't get to be neutral. If you carry a balance, you're paying for someone else's flight to Tokyo. If you pay in full and collect rewards, someone else is paying for yours

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

Amazon had a secret code name for the Prime cancel button.

They called it Project Iliad.

The Iliad is a Greek poem. It is about a war that lasted ten years. It has 24 books and almost 16,000 lines. Amazon picked that name on purpose. They wanted canceling Prime to feel like a war. They wanted you to give up.

Here is how it worked.

You hit "Cancel my subscription." Amazon did not cancel it. They sent you to a new page. The page asked if you were sure. It showed you all the things you would lose. It put a yellow warning sign next to the cancel button. Then it asked you again.

You clicked "Yes, cancel." Another page. New offer. Maybe a discount. Maybe a pause. Maybe just turn off auto-renew. Anything to stop you from leaving.

You clicked through. Another page. Then another. Then one more.

By the time you reached the end, you had clicked six times. You had scrolled past four pages. You had said no to fifteen different buttons. Only one of those buttons actually canceled. The other fourteen kept you in.

The FTC has an official name for this. They call it the "Four-Page, Six-Click, Fifteen-Option Iliad Flow."

It worked. After Amazon rolled out Project Iliad, cancellations dropped by 14 percent. Hundreds of thousands of people gave up and kept paying.

Then somebody leaked the internal documents.

In 2021, the Norwegian Consumer Council found the same trap on Amazon's European site. They filed a legal complaint. Business Insider got the leaked emails. In June 2023, the United States FTC sued Amazon. They named three of Amazon's own executives in the lawsuit. They said the executives knew about Iliad. They knew it was hurting customers. They blocked changes that would have made it easier to cancel because the changes hurt the bottom line.

In September 2025, Amazon settled. They paid 2.5 billion dollars. One billion as a fine. One and a half billion in refunds to 35 million customers. It is the biggest fine in FTC history for breaking the agency's rules.

Amazon did not admit they did anything wrong.

Now think about this.

Every subscription on your bank statement was designed by people who studied Project Iliad. They watched what worked. They copied it.

Streaming services hide the cancel button under three menus. Gym apps make you call a phone number that no human ever answers. Newspapers offer you a "pause for three months" instead of a real cancel. Software trials switch to a paid plan the second your free week ends, with no warning email. Apple and Google make you cancel through their app store, not the app itself, so most people never find the right place.

The average American pays 219 dollars a month for subscriptions they do not actively use. That is 2,628 dollars a year. Most of them remember signing up for maybe three of them.

The rest are ghosts.

Apps you forgot. Free trials that turned into paid plans. Services your ex signed up for on your card. Streaming bundles you got for a movie six years ago and never canceled because the cancel button is buried inside an Iliad of its own.

Here is the fix. It takes 15 minutes. Do it tonight.

This is the Subscription Autopsy.

Open your bank app. Open your credit card app. Open Apple Pay or Google Pay if you use them.

Go back twelve months. Yes, twelve. You will be shocked.

Write down every recurring charge. Every one. Big and small. The 4.99. The 1.99 you do not even remember. Even the ones that say "Apple. com" or "Google" — those are subscriptions hiding behind the store name.

Now look at the list. Be honest with yourself. Three columns.

Column one: I use this every week.

Column two: I have not opened this in a month.

Column three: I do not even remember what this is.

Cancel everything in columns two and three. Tonight. Right now. Before you put the phone down.

If a cancel button leads you into an Iliad, do not give up. Search for the company name plus "how to cancel." Some states now have laws that force one-click cancellation. If a company makes it impossibly hard, you can call your bank and ask them to block the charge.

You will find money you did not know you had. Most people find between 50 and 200 dollars a month on the first autopsy. That is between 600 and 2,400 dollars a year.

Money that was never going to a product you wanted. Money that was going to people who designed a trap and gave it a Greek name and laughed about it.

The trap is still legal. The company that built it just paid 2.5 billion dollars and did not admit anything was wrong.

The only person who can close the loop is you.

Send this to one person whose bank statement is full of charges they do not recognize.

Your 256GB Android is "full" again.

You've deleted photos. You've uninstalled apps. You've cleared WhatsApp.

Still full.

Because the real junk lives in folders Android refuses to open. 30GB of it.

I recovered 31GB yesterday. Didn't touch one photo, one chat, one app.

Here's where to find it on Samsung, Xiaomi, Vivo, and OnePlus:

![tomselliott's tweet photo. My former boss @PeterSchiff had his Puerto Rico bank shut down in 2022. The IRS told the world it was a money-laundering haven.

More likely: The Biden IRS disliked Peter's constant criticism.

Peter FOIA'ed their communications. Spoiler: Their investigation turned up no criminal behavior, but they charged him anyway.

Worse, the IRS refuses to turn over all of the FOIA'ed materials, despite a federal judge mandating their release.

The story is crazy. But for me the craziest part of all is that Peter's bank, as a policy, was fully solvent, keeping 100 percent of clients' assets. By contrast, the standard U.S. bank historically was only required to keep 3 percent of its clients' deposits (the rest being loaned out at interest) but since Covid, the minimum reserve rate was dropped all the way to zero.

The whole point of a bank is to keep your money safe. What today we call banks do the opposite: As soon as you give them your money, they give it someone else. Peter tried providing the world an actual, honest bank — & the IRS sicc'ed Puerto Rican banking authorities on him, forcing its closure. (Knowing the nightmare of U.S. financial regulations, Peter's bank actually excluded Americans as clients; as the IRS had no authority, the FOIA'ed emails show them merely telling the Puerto Rican financial authorities [OCIF] what to do.)

This is the definition of government being weaponized against American citizens, exactly the thing the Constitution was designed to protect against.

Yet despite the feds being caught red handed, breaking the law in service of their own political agenda, illegally covering up their crimes, there's been zero accountability. Nobody fired, nobody reassigned, not even an apology to Peter or his thousands of de-banked clients.

Many of the named officials still work at the IRS. If the DoJ cares to show the American people they care about ending the weaponization of government, they'll take action. Until then, we should assume any of us can be targeted for the crime of offending someone in Washington.](https://pbs.twimg.com/media/HJasPZHWsAQtyHD.png)