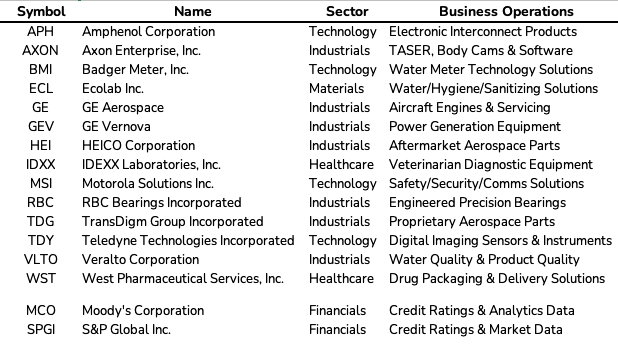

Searching for high-quality, durable businesses with robust competitive advantages, runways for growth, and a history of creating value for shareholders.

Here's the current state of the Durable Value Creators investable universe. Spent some time recently narrowing down the focus.

Primary themes include picks & shovels of secular trends, recurring revenue, razor-razorblade model, mission-critical, and/or relatively asset-light.

Any other companies/industries out there with similar dynamics to drug packaging ($WST $STVN) where there are volume tailwinds but also favorable mix shift? More biologics = higher spec, higher margin content.

Maybe semicap, such as rising litho intensity per chip? $ASML

@mxschumacher Do you find yourself using research mode and/or "thinking" for effort? I used to use the research mode more but found it's easier to steer the discussion just using thinking and have pivoted to preferring that... Unless I'm busy and want it to run research in the background.

Man I sure hope Claude is telling me accurate information, because I've either been learning a lot of good stuff lately or am being confidently mislead on various businesses and industry dynamics.

Looks like the AI "bubble" is that companies pushed AI spending too hard without results, which in turn overestimates AI company projections for customers and ARR. Everyone went too big too fast. The technology is real and beneficial, but potential has outrun productivity so far.

NEW: Amazon has reportedly scrapped its internal AI leaderboard as costs soared, with a senior executive telling staff: “don’t use AI just for the sake of using AI.”

HEICO Q2 earnings call summary and Q&A $HEI

Strong organic growth, raising operating margin guidance, and multi-year defense tailwind. Management argues newer generation aircraft with more expensive parts will create more PMA opportunity, not less.

@sal13836@CapstackCapital Not anymore. Not a bad company by any means but I already have a lot of industrials and aerospace in the portfolio/watchlist/universe.

@scaleadvantage Just seems irrational and wasteful to me. What business deliverables require that amount of additional resources per person to accomplish. Especially in the case of a business like Microsoft, where they already have an established ecosystem and extensive automation.

This seems kinda crazy to me. I don't know anyone at work using more than several hundred dollars worth of Claude tokens per month. Even with only using Opus and mostly using max effort I've still haven't hit the $500/mo mark using it most every day. What are these people doing?

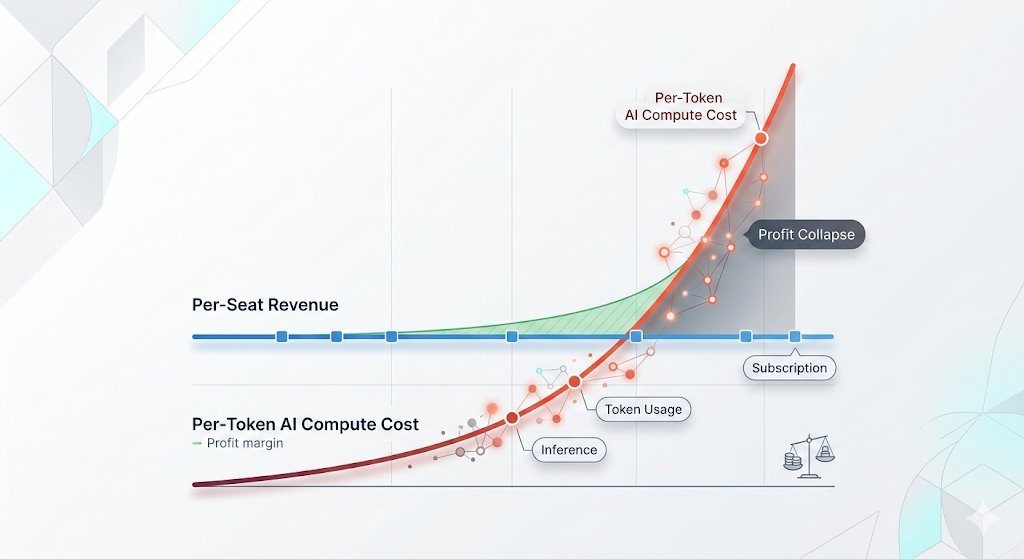

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

@sidecarcap They’re also one of the worst home builders in terms of quality of work. Ducking public appearances might be in management’s best interest, especially in the era of social media.

Or perhaps the alternative view is, maybe myself and the people around me aren't using AI enough... But I don't use AI just for the sake of using AI, must have a purpose or task in mind. Feels like some people are just setting tokens (and money) on fire for the sake of it.

@avalondrexmore I guess because buybacks give them more control over when that capital is deployed whereas a special dividend is a one time immediate departure of that cash. Plus makes a dent in the share count after SBC.

We see these posts every year now yet $NVDA revenue and profits continue to rip higher. Let's think for a second. In 2020 they spent $2.8B on R&D. This latest Q alone? $6.3B. TSMC makes all their chips so not much to spend on capex. What are they supposed to do besides return it?

$NVDA increasing their dividend is a very bad sign in my opinion. To me, it signals they don’t know what to do with the cash anymore.

Nobody owns NVIDIA to collect a 0.5% dividend.

"Just reinvest it" is a common argument. But R&D CAGR over the last 5 years is ~40%. They're pouring massive amounts into new projects. New projects take time to start and ramp up. They aren't a light switch you just flip on.

Dividends and buybacks are good in this situation.

@CapstackCapital@Krokodil_V@EndThePods Hey man, I really appreciate it and likewise the same to you. I've gone down several interesting rabbit holes after seeing some of your posts, most recently the missile supply chain stuff. MPTI is now a name on my radar, and there's a few others ones I'm learning about like ELMT.

@CapstackCapital@Krokodil_V@EndThePods Appreciate the tag. I've actually never looked at SOLS but you make a number of good points and it is the type of business that interests me.

Intriguing end market exposure with secular tailwinds, key input specialty materials for customers. I'll have to take a deeper look.

@returnoncap Agree with the overall idea, I've started a small basket of similar themes (but different names) in my own portfolio. Curious if you think $WST belongs in the group as well?

@fivepointscap That's fair. I just struggle with the incremental value that Meta gains off this level of spending, especially with costs for chips/memory/power right now. They obviously have more insight than me, just feels like their app ecosystem will still be here in 10 years either way.