$QXO, fin-twits most under covered gem, has dropped some news today.

The window for accumulating TopBuild votes is official closed.

@QXOInc vote is already locked in.

Regs got the all-clear.

And that means...the clock is officially on.

Proxy services are getting to work. I expect them to watch the price closely over the next 10 trading days.

So what's it gunna be? Price says no. Spread says yes.

Place your bets.

Patience is the super power.

It's a sparse community following this one on here, at least we've got random posts doing the deleted Houdini jig.

🍿🎬

Alright, here’s my $MU thesis:

In 100 years, Micron Technology invents time travel.

And right now, people from the future are coming back in time to buy the stock before it goes completely parabolic.

I don't know if we should aggressively ban it, I'm a libertarian if anything, though prefer not to fence identity in the first place.

I'd quicky address auto license requirements: they are far too liberal for the public good. I can't lean on a bad decision for a benchmark. The proof of this is in the actuarial tables: insurance, which is mandatory, is itself an admission that the license is not sufficient to keep society safe.

On gambling in your pocket: we have arguably run the highly permissive model, and @johnarnold's post is alluding to where we are in the feedback loop. Early results, pre-trial completion (good info to have if you trade biotechs) allow a society to prepare in real time. It doesn't have a standstill obligation with respect to early data.

In business, distribution is the bottleneck. It doesn't matter what you've got to sell or how good it is if you cant reach the customer. Smart phone ubiquity, combined with digital advertising, creates a heretofore non-existent distribution channel for a dangerous digital product. That's a reality that distinguishes the current arrangement from cars or other physical dangers like sex/drugs/rock&roll. It shouldn't be ignored.

The result is a different type of threat surface, and a different slope w/re the size and severity of the surface.

The game theory here also favors the value extracting party over the customer, and the extracting party has the ability to scale in an asset-light model. This is new threat territory. We've learned as much by experimenting on our youth over the last 15-20yrs. In fact, courts recently found in favor of plaintiffs V Meta/others with regard damages incurred from social platforms.

We don't always have to wait for the results. There's an argument to be made that maybe if we could go back in time and redo the social media experiment a different path would be chosen, right? At least its a "maybe".

Some differences in your samples worth noting:

Penny stocks are not part of the cultural fabric like sports, they are unfamiliar, old, and have proven not to be on an exponential threat path.

Lottery tickets are a tax on the poor, and those who failed to complete basic statistics. Also, observable growth path, moderate slope. Theoretically the money is recycled into education, not extracted for profit.

Neither penny stocks, nor lotto possess the illusion of control that sports gambling does.

Sex is good. Physically. Emotionally. Don't forget, mandatory for survival of species. Threat path of disease is stable, likewise addressed at the societal level. Sex education precedes sexual maturity/readiness.

Drugs/alcohol/tobacco. Health class, education precedes the gateway age. Threat path dynamic, large surface, fentanyl cxl/rpl alcohol. Vape cxl/rpl cigarettes. Society recognizes it's obligation to observe, adapt. The approach lives apart from laissez faire, invisible hand.

Consider automobiles: massive threat surface, biggest of any discussed. Society has accepted the threat. Nevertheless, drivers ed/driving school precedes auto-licensure. Rules, punishment, revocation. Threat path in decline as a result of efforts (LT), path in flux short term (cell phone distractions, other). Threat surface did not exist until about 100 yrs ago.

These are imperfect but deliberate attempts to address known life-challenges, best achieved during developmentally appropriate years. It is distinctly not arbitrary. It's not perfect, but that shouldn't prevent a village from trying.

As things change, we have a choice as a society to adapt or to ignore.

A recent example is low cost, battery powered, motors that have enabled a surge in micro-mobility devices. New rules do not exist for new products; it takes time to figure out what's best for the public interest and where/how/if to allocate resources most efficiently.

🎯I think the real answer here is that rapid changes to society with long duration effects require long term solutions that start with education. 🎯

The priest is the canary in the mine. The choice is ours to ignore it, logic it away, or accept that some short term actions may be beneficial while the impacts of the improved educational paradigm catch up over the long term.

I just spoke with Charles Schwab about the @SpaceX IPO. Schwab is one of a handful of brokerages selected by SpaceX to allocate IPO shares to retail investors.

If you have an account with Schwab, here’s how to prepare for the SpaceX IPO:

1) You first need to opt into IPOs from the Trade > IPOs page on Schwab's website.

2) After you've opted in and the IPO shows on the page, you can submit an Indication of Interest. The indication of interest will be able to be submitted when the Roadshow period begins for the stock. This is currently expected to be early June.

3) You need to have minimum $100,000 in total balance to be eligible to participate in the SpaceX IPO share allocation.

Schwab still doesn't know how many shares will be allocated to their brokerage at this point since SpaceX will be the one to decide that in the coming weeks. Just be prepared to check back on the IPO section of Schwab's website. Additional info will come later.

Lastly, don’t be surprised if you receive fewer IPO shares than you requested (if any at all). Demand for the limited number of available IPO shares will almost certainly be extremely high, and these participating brokerages will only get a certain sized allocation of shares to offer to retail investors, so it'll likely be tough to accommodate everyone. The best thing you can do is to just be prepared.

Note: SpaceX specifically stated in their S-1 filing that any purchase of their Class A common stock in this offering through these platforms will be at the same IPO price, and at the same time, as any other purchases in this offering, including purchases by institutions and other large investors, which means any retail investors that are lucky enough to get allocated some SpaceX IPO shares will pay the same price as the big guys.

With the accompanying music to Nat King Cole's Christmas Song...

" @gnoble79 with eyes all aglow, will find it hard to sleep tonight"

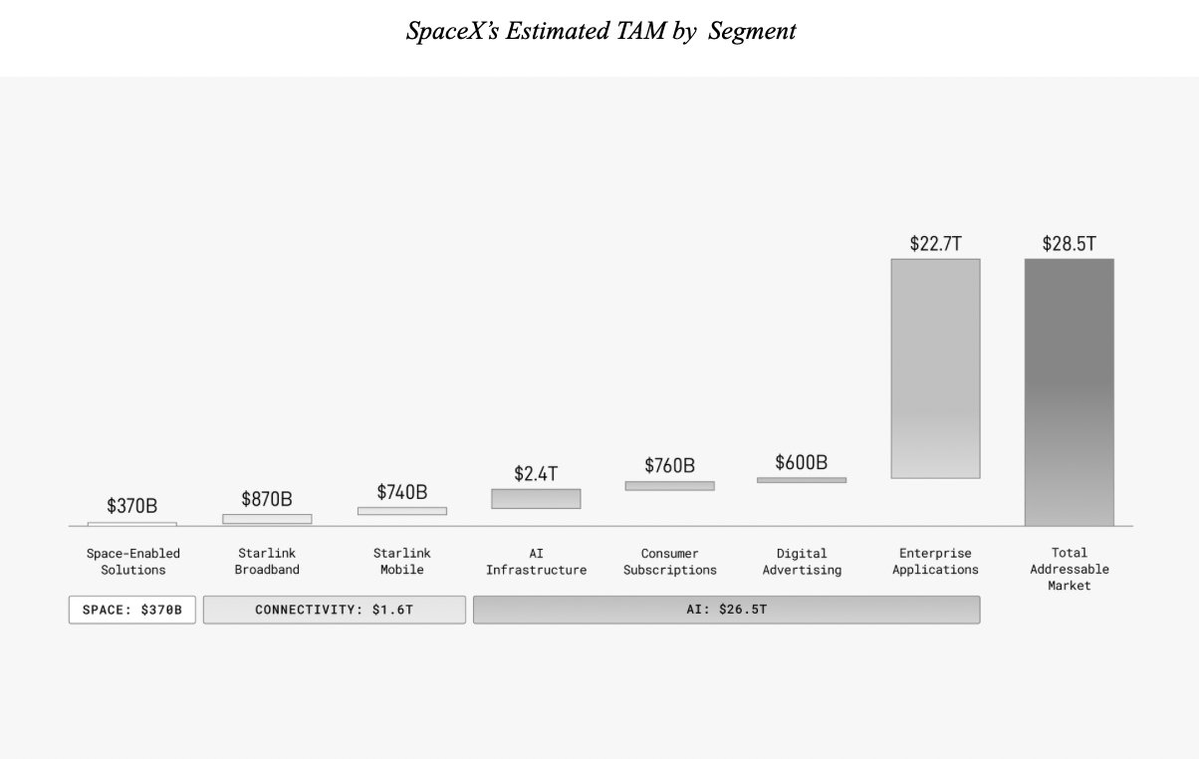

Is it possible for a superlative statement "most ridiculous isht in history" to also be an understatement?

SMH

🤦♂️

SpaceX wins the trophy for most ridiculous TAM analysis in public market history.

Saying your market is "$28.5 trillion" is the typa shit you see in F-tier startup pitch deck

Put another way, i don't think the short side of the trade has closed out and I don't think they've properly accounted for the fact that they over smashed the price so far as they are now at risk of racing the arb unwinds in the event of a NO-VOTE....that they caused by stop hunting the weak hands in an illiquid name that has no open market institutional support.

I think the smart risk-reducing move at this point is to buy as much $BLD and $QXO as they can get their hands on to accumulate voting power (vote in favor) and reduce net exposure (ie, lock in profits and call it a day).

This will crush the arb spread and take the mark price back to a more reasonable price level that accounts for a forward EBITDA run rate of $4B...because 7x is not the right number, and this deal is not value destructive.

Plenty of worthwhile $QXO observations in the last 48hrs. Not the least of which is a large compression of the merger arb yesterday which has retraced a bit this morning.

Odds of s snap back rally to $20 seem better than new lows. This makes p/c skew offsides atm.

FACT 1: There's going to be a massive push to close this deal from nearly a dozen angles.

FACT 2: stock pricing sub 18 is a threat to all but one of those stakeholders.

My thinking is they aren't going to tolerate that risk.

Of the dozen angles, the net short still wants QXO pricing here (or lower). But if there's a billion dollars of merge-arb pair on, that's 2B in unmanaged risk the moment a no-vote comes through. They can add to the pair, control more votes, influence outcome. Rational move. This compresses the spread.

What they can't do is make a recommendation in favor of the deal for the third parties, who influence decision making for the passive $BLD shareholders.

Those third parties will look at qxo common as currency and make an objective vote. A languishing stock price becomes a material risk, Glass Lewis and ISS have an obligation to be objective...not to prognosticate on future price of QXO. And there's no getting around the fact that since the deal announcement the broad market ($XHB, $ITB, SPHOME, etc) is down 15% while the deal currency $QXO is down 40%. It is not at all obvious to me that theses firms will be publishing thumb ups. @QXOInc knows this, they will be helping get the word out if reccos are in favor. If reccos are "against" QXO will just let them fallow.

In any event, at this point it is to the benefit of the merge-arb camp to help levitate the stock price. Higher priced currency makes the deal strong for the objective third pary, and the third party thumb up is what will ensure they complete their deal quickly, and avoid an unwind and/or additional weeks or months of borrow costs to hold the trade while folks argue about it until the outside date in January.

I think that the stock is thinly traded and vulnerable to short algos attempting to manipulate the price in the absence of anyone of consequence running QXO in a big long:short book. And when dilution is imminent (whether its good dilution like 2x ing EBITDA or bad like time warner AOL), the timing is right to deploy an attack. It's particularly risk manageable to orchestrate when theres an arbitrage gap because you can sell the acquirer and push everything lower, but if it doesnt work you have time to lean on buying the target stock and still break even.

That said, QXO has pretty good amount of industry coverage (all the ratings are basically buys with targets 25-40 territory) yet it's not a seasoned enough issue for a big relative value book to trade it. Think of how BofA placed $750M in one ticket on january at $23.80. Those guys "should" be buying it here. But they aren't active managers. They are chunky allocators. Long term holders, huge tickets, and GFYS if the price bounces around in the short term. Hate to say it but its true. And same for $APO and Temasek. But also they are restricted from buying in the open market anyway (its to prevent them, or anyone, from taking a stake that could become a control issue/headache for brad), and restricted from selling, so they are just stoic owners for now. But nobody is running 100M of long QXO against short 100M of ITB and balancing in and out as that spread breaths. For good reason, cause thing thing just whips , and theyd be carted.

Self fulfilling this is. If it whips, nobody actively trading L/S book. If nobody trading relative value, it whips.

But ultimately I think price rallies and the deal closes.

There's too many stakeholders in the room that want it to happen. Everyone wants to get paid, from the management on both teams, to the bankers, to merge arbs, to the visionaries, apollo, temasek, Morgan Stanley investment management, golly the list goes on and on.

Like I said, lots of risks.

But I perceive AI is a strength and opportunity for $QXO, not a threat. AI is a tool, he who uses it best derives the most from it.

That said, manufacturers cannot practically sell through to the job site, whether AI enabled or not. They would need to vertically integrate and assume role of distribution themselves. In order to provide value to the customer they'd need to then offer the entire menu that the customer expects, even the garbage items with terrible margins/turnover/economics. I don't see any manufacturers stepping up to the plate to do that.

On the flip, as a distributor QXO is already pumping the full menu to customers. The data of that inventory flow has a value which inures to the benefit of QXO. (Think of Costco/Kirkland.) Over time, the distributor gets to cherry pick the best economics and selectively integrate backwards up the ladder because they know exactly what the customer wants and they have the data relative to the customer's option-set (which they also have the data on). No manufacturer has this level of insight.

What does costco do? They cherry pick the best items for sale and vertically integrate. But they take it ones step better and they run asset-light. They dont actually manufacture the product and invest in P&E. Instead the use proprietary data to embed the best features that they already KNOW the customer demands and embed that into an own-branded product. And then they have someone else manufacture it and put Kirkland on the label. QXO will do this with select products over time, asset light, vertical-looking integration. They've said as much, slightly different words, but it's in Brad's remarks.

Deliver for the customer, Happy Customer. Sticky customer. more data. better service/offerings. happier customer. stickier customer. even more data. on and on. its a winning cycle.

key difference with $COST is that it's now a half trillion dollar company and doesn't have the opportunity to double it's EBITDA in a single transaction. but it's still trucking along. QXO is at an early point in its life cycle

Thesis on @QXOInc acquisition of TopBuild.

$QXO price ranges:

15-18: deal highly at at risk

18-20: deal at risk

20-22: deal likely

22-25: deal highly probable

Eyes on that arb spread.

Plenty of worthwhile $QXO observations in the last 48hrs. Not the least of which is a large compression of the merger arb yesterday which has retraced a bit this morning.

Odds of s snap back rally to $20 seem better than new lows. This makes p/c skew offsides atm.

FACT 1: There's going to be a massive push to close this deal from nearly a dozen angles.

FACT 2: stock pricing sub 18 is a threat to all but one of those stakeholders.

My thinking is they aren't going to tolerate that risk.

Of the dozen angles, the net short still wants QXO pricing here (or lower). But if there's a billion dollars of merge-arb pair on, that's 2B in unmanaged risk the moment a no-vote comes through. They can add to the pair, control more votes, influence outcome. Rational move. This compresses the spread.

What they can't do is make a recommendation in favor of the deal for the third parties, who influence decision making for the passive $BLD shareholders.

Those third parties will look at qxo common as currency and make an objective vote. A languishing stock price becomes a material risk, Glass Lewis and ISS have an obligation to be objective...not to prognosticate on future price of QXO. And there's no getting around the fact that since the deal announcement the broad market ($XHB, $ITB, SPHOME, etc) is down 15% while the deal currency $QXO is down 40%. It is not at all obvious to me that theses firms will be publishing thumb ups. @QXOInc knows this, they will be helping get the word out if reccos are in favor. If reccos are "against" QXO will just let them fallow.

In any event, at this point it is to the benefit of the merge-arb camp to help levitate the stock price. Higher priced currency makes the deal strong for the objective third pary, and the third party thumb up is what will ensure they complete their deal quickly, and avoid an unwind and/or additional weeks or months of borrow costs to hold the trade while folks argue about it until the outside date in January.

more sellers than buyers 😉

Never gets old, that one. But as funny as it is, it's the only true thing you have to go on.

Lots of reasons, read @LeoNelissen's recent write up for a pretty dispassionate coverage of it. If you want variables you've got rates, consumer spending, business environment, input costs, who's gunna eat the squeeze, merge arb, short attack, etc etc.

All candidates for root cause, but the known cause is more folks hitting the red sell button than the green one.

Voting machine first. Weighing machine last.

Right now my mind is more focused on all the stakeholders in the room and I think it is unquestionable that the deal is at risk if the stock price does not rise. And if that happens it blows up a massive merger-arb position. And seeing as this name tends to move around as the sands shift beneath our feet, I think the variance is going to continue and we get to watch the battle take place amongst the parties.