@KeruboSk At least 2 that I can remember. My great grandmother, born in 1886 and great great uncle, her little brother, born in the 1890s. I drove myself to her funeral in 1988.

FAST FOOD IS GUILTY... OF OVERPRICED VALUE MEALS!!!!

Quote this with #ChilisFoodCourt & tell us how much you paid for your last overpriced fast food "value meal". We're picking 1,099 ppl & giving them a $20 gift card to Chili’s to try our new Big Crispy 3 For Me. rules ⬇️

I taste greatness! This is my #PepsiEntry for a chance to win $5K playing the @Pepsi#PepsiTasteWins jackpot! Tap below and post to enter to win yourself! U.S. res, 18+. Ends 2/8/26, 9:45pm ET. Rules: https://t.co/ERy7h3gblg

I’m in. This is my #PepsiEntry for a chance to win $1K playing the @Pepsi#PepsiTasteWins jackpot! Tap below and post to enter to win yourself! U.S. res, 18+. Ends 2/8/26, 9:45pm ET. Rules: https://t.co/ERy7h3gblg

This is a great new tool for anyone who is interested in using options in their investment plan. Combines with other Volland tools, it gives traders a clearer picture of the market.

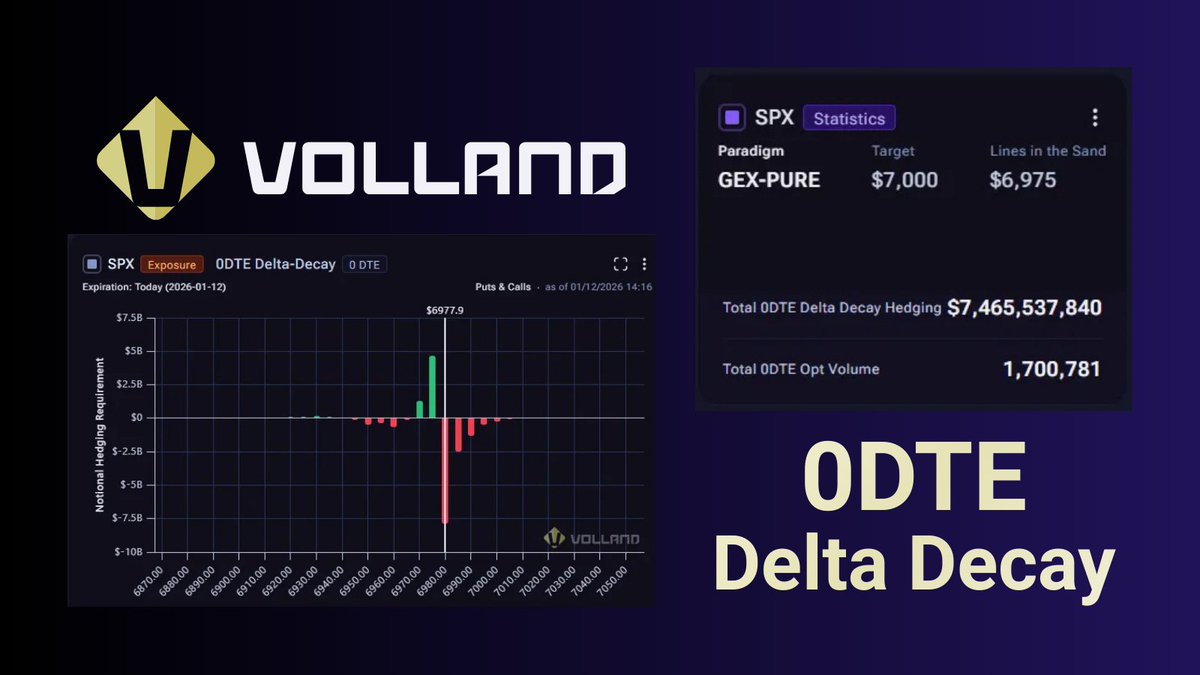

0DTE Delta Decay: Intraday Dealer Hedging Quantified

The final word on 0DTE hedging flows

When Cboe introduced daily options in $SPX, it forever changed market dynamics. Very swiftly, “0DTE” options became half of all SPX flow, but not at the expense of the other tenors. The result is that SPX option volume has been hitting daily volume all-time highs about as often as SPX itself.

With all of that volume comes different market dynamics. #0DTE options have been priced much differently than its higher tenor siblings, usually with much higher static IV and steeper skew. All of this created a dynamic that couldn’t be ignored, especially for the intraday trader.

While there are many flows that the need to be accounted for when intraday trading, considering that the margin of error is so small, the dealer hedging flow is critical. This is because options volumes are so high that the imbalance of the 0DTE dealer book must be taken into account. It was this failure that caused David Chau’s “Captain Condor” strategy to so remarkably blow up on Christmas Eve.

Volland saw these flows, and up until recently, attempted to signify this from the perspective of charm. We tried many ways to express that notional hedging more accurately, and we realized that we were deriving this with the incorrect terms. Notional charm was expressing delta notionals, when we wanted straight notional hedging but using the principles of delta expiration dynamics that vanna and charm express.

The new 0DTE Delta Decay widget completes what we set out to do with our work with charm.

Introducing 0DTE Delta Decay

The 0DTE Delta Decay widget is the only widget that swiftly and accurately shows the amount of notional delta that dealers need to hedge before expiration on the 0DTE tenor on a strike-by-strike basis.

If you need to know how much total hedging needs to be completed before the end of the day, Volland’s 0DTE widget has that total notional that needs to be hedged.

These widgets are available in all of Volland's 0DTE option offerings, including $SPY and $QQQ, which are needed for better timing and a full picture.