Everyone sees ₹52,000 Cr for defence

I’m looking at who supplies these systems

This DAC approval is mainly for:

• Electronic warfare

• Air defence

• Missiles

• Surveillance systems

• Radars, sensors and guidance

That’s why I’m watching BEL, BDL, Data Patterns, Astra Microwave and Paras Defence more closely than the broader defence sector

Headlines move prices. Procurement creates winners

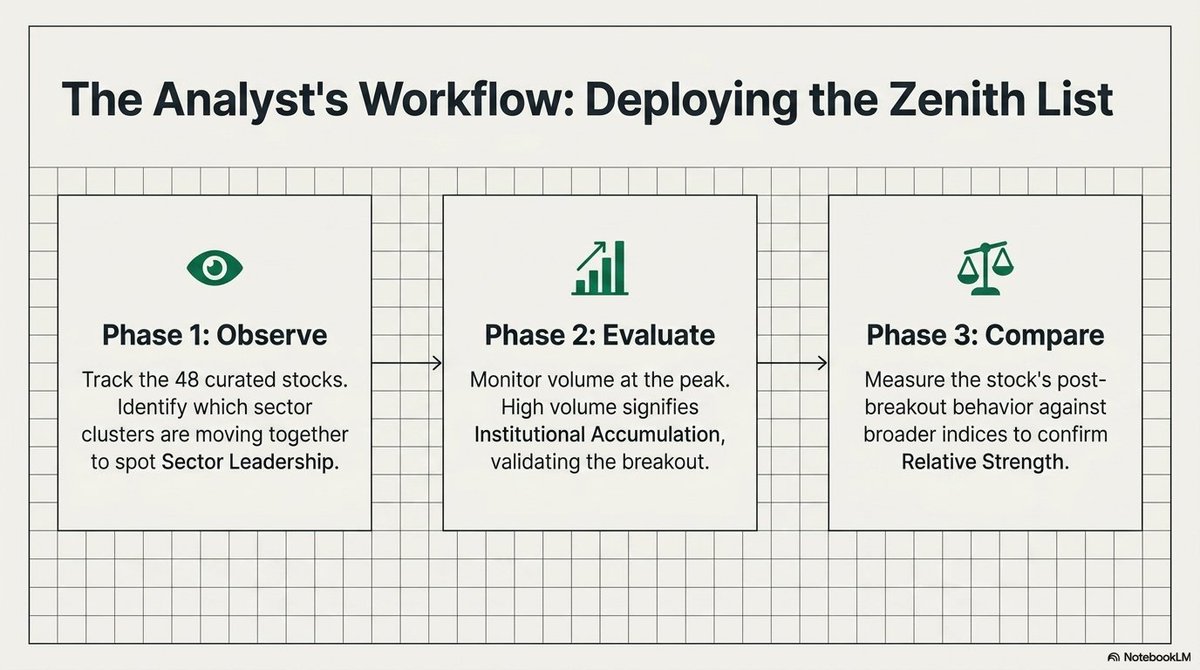

45 HIGH-QUALITY STOCKS AT OR NEAR ALL-TIME HIGH LEVELS TO STUDY & TRACK 🔥🔥🔥

▪ SPARC

▪ Timex Group

▪ Kernex Microsystems

▪ Emmvee Photovoltaic Power

▪ TIPCO Engineering

▪ Sedemac Mechatronics

▪ Afcom Holdings

▪ Cupid

▪ Cemindia Projects

▪ Neetu Yoshi

▪ Acutaas Chemicals

▪ Bajaj Consumer Care

▪ SKM Egg Products

▪ Schneider Electric Infra

▪ Aditya Infotech

▪ Uttssav CZ Gold Jewels

▪ R R Kabel

▪ Sky Gold & Diamonds

▪ Shivalik Bimetal Controls

▪ Shreeji Shipping Global

▪ KMC Speciality Hospitals

▪ Thangamayil Jewellery

▪ Data Patterns

▪ Shri Ahimsa Naturals

▪ Welspun Corp

▪ ADF Foods

▪ Premier Explosives

▪ Black Box

▪ KSH International

▪ VA Tech Wabag

▪ GNG Electronics

▪ Astra Microwave Products

▪ Bharat Seats

▪ Avalon Technologies

▪ Modern Insulators

▪ Park Medi World

▪ Ramco Systems

▪ SBC Exports

▪ Laurus Labs

▪ Lloyds Engineering Works

▪ BLS E-Services

▪ Bliss GVS Pharma

▪ Rashi Peripherals

▪ Syrma SGS Technology

▪ Sanghvi Movers

▪ Jay Bharat Maruti

▪ Knowledge Marine

▪ Indiabulls Enterprises

Stocks trading at or near their all-time highs often indicate strong institutional participation, positive business momentum, improving fundamentals, and sustained buying interest.

While not every stock at an all-time high turns into a multibagger, many of the market's biggest wealth creators spend long periods making new highs after new highs.

Studying such stocks helps investors understand relative strength, sector leadership, institutional accumulation, and breakout behaviour, making them an excellent addition to any quality watchlist.

DISCLAIMER

The above list is shared purely for educational, learning, research, and tracking purposes. It is not a buy, sell, or hold recommendation. Please conduct your own research before making any investment decision.

Shivalik Bimetal Controls 795⚡

One of the most interesting businesses you’ve probably never looked at.

The company manufactures bimetal strips, shunt resistors and electrical contacts—small but mission-critical components used in EVs, smart meters, circuit breakers, industrial equipment and power systems.

Think of it this way: you don’t buy the engine, you buy the tiny component without which the engine won’t work.

As India spends more on electrification, smart grids, renewable energy and EVs, demand for these precision components keeps rising.

Recent numbers back the story:

📈 Revenue: ₹162.6 Cr (+22.8% YoY)

📈 Net Profit: ₹26.0 Cr (+23.7% YoY) (Moneycontrol)

This isn’t a flashy business. It’s a “pick-and-shovel” company supplying essential parts to multiple fast-growing industries.

If the execution continues, I believe this is the kind of stock that can quietly compound wealth over the next 12–24 months while most investors chase the popular names.

Schneider Electric Infrastructure

✅ Capacity Expansion Approval for Manufacturing Facility

Board approved capital expenditure increase from INR 138 Cr to INR 184 Cr for medium voltage unit expansion. Manufacturing capacity to rise from 180,000 to 250,000 units annually.

@DhawalDoshi5@MithunSarkari@Asset_Architect

Vishnu Chemical:

Vishnu Chemicals has commenced production from its new strontium carbonate plant.

This can be replacement for Rare earth minerals possibility.

Vishnu Chemicals also completed its acquisition of Chromium Mine in South Africa.

Technically charts also showing as great times ahead, at ATH.

#ReRatingStock

DEE Development Engineers

Founded in 1988, DEE is India's largest process piping player by installed

capacity and among the top 5 globally. It designs and manufactures

high-pressure piping systems, spools, fittings, and heavy fabrication for

Oil & Gas, Power, Petrochemicals, and Fertilizers across 27+ countries.

Listed on BSE (544198) and NSE (DEEDEV).

FY26 headline (Consolidated)

Revenue: ₹827 Cr to ₹1,142 Cr, up 38 percent

Op. EBITDA: ₹124 Cr to ₹189 Cr, up 53 percent (margin 15.0 to 16.6 percent)

PAT: ₹44 Cr to ₹77 Cr, up 77 percent

EPS (diluted): ₹6.60 to ₹11.14

Order book: ₹1,228 Cr to ₹1,940 Cr, up 58 percent in a single year

The core engine is firing

The piping business is where the real story sits.

Core revenue ₹1,086 Cr, up 46 percent.

Core Op. EBITDA ₹195 Cr, up 82 percent.

Core operating PBT went from ₹24 Cr in FY25 to ₹93 Cr in FY26.

This is operating leverage showing up in the P&L, not just the deck.

The backward-integration bet

Two capacity milestones landed in FY26:

1. Anjar pipe fabrication scaled to 30,000 MTPA, commissioned ahead of

schedule.

2. India's first Seamless Pipe Plant (7,000 MTPA) commenced commercial

production. This is a 100 percent import-dependent item domestically,

so this is genuine import substitution.

Both sit near Kandla and Mundra ports, cutting inland transport and transit

time. The margin thesis rests on how fast these ramp. Total installed

capacity now stands at 93,500 MTPA in piping and 32,400 MTPA in heavy

fabrication.

Order book quality

Closing order book ₹1,940 Cr, of which 94 percent is process piping and

60 percent is export. FY26 orders executed were around ₹1,158 Cr, so

book-to-bill sits near 1.7x on FY26 revenue. Fresh wins include a

USD 40 Mn+ LOI into global OEM supply chains, a ₹90 Cr windmill tower order,

and a Reservation Agreement reserving 60 percent of HRSG pipe spool capacity

with an international EPC at a minimum annual job value of US$ 15.27 Mn.

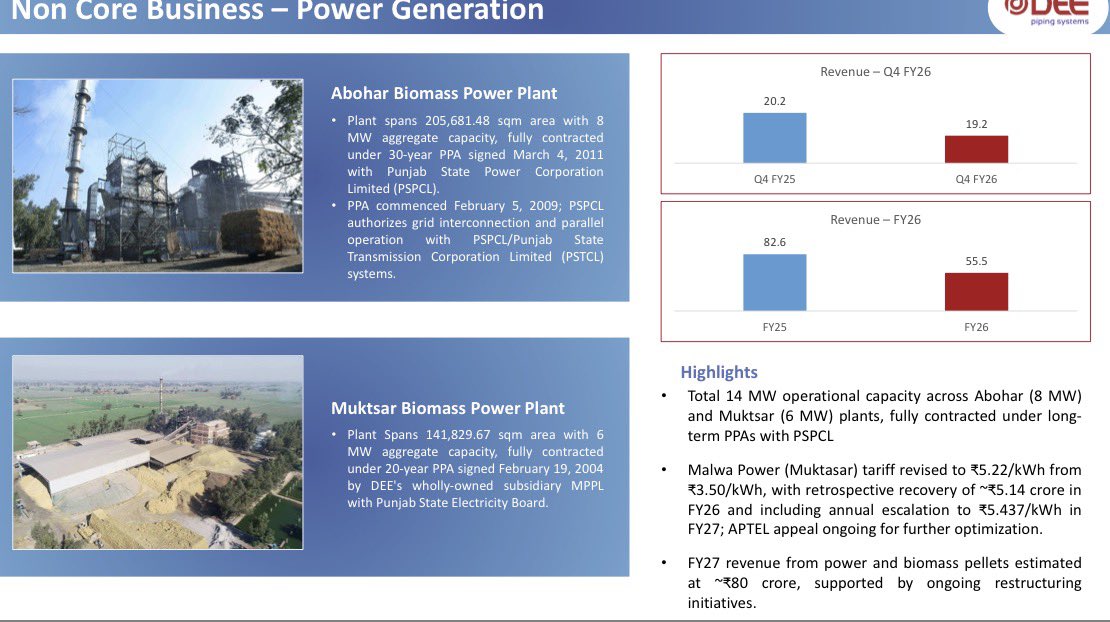

The honest part: the non-core drag

Power generation revenue fell from ₹82.6 Cr to ₹55.5 Cr, down around

33 percent, and the non-core segment carried an Op. EBITDA loss of ₹5.8 Cr

in FY26. The Malwa Power tariff revision (₹3.50 to ₹5.22 per kWh, with an

escalation to ₹5.437 in FY27 and a retrospective recovery of around ₹5.14 Cr)

helps, and management is pivoting to biomass pellets and evaluating housing

this under an InVIT. FY27 power plus pellets revenue is guided at around

₹80 Cr. Worth tracking whether the turnaround is real or optical.

Balance sheet reality

Debt to Equity: 0.73 to 0.89 (capex cycle still on).

Net Debt to EBITDA: 4.02x to 3.81x, elevated but improving.

ROCE: 8.2 to 9.8 percent. ROE: 7.0 to 9.1 percent.

Management flags the capex cycle as nearing completion and expects gradual

deleveraging as cash flows improve. This is the single biggest thing to

verify over the next few quarters.

The Q4 nuance

Q4 revenue ₹361.6 Cr, up 26 percent YoY, with Op. EBITDA margin recovering

to 18.2 percent QoQ. But Q4 PAT of ₹27.7 Cr was down 12.2 percent YoY,

driven by higher interest (up 34.5 percent) and depreciation, plus a

one-time labour code liability of ₹1.94 Cr. This is a leverage and one-off

story, not core weakness.

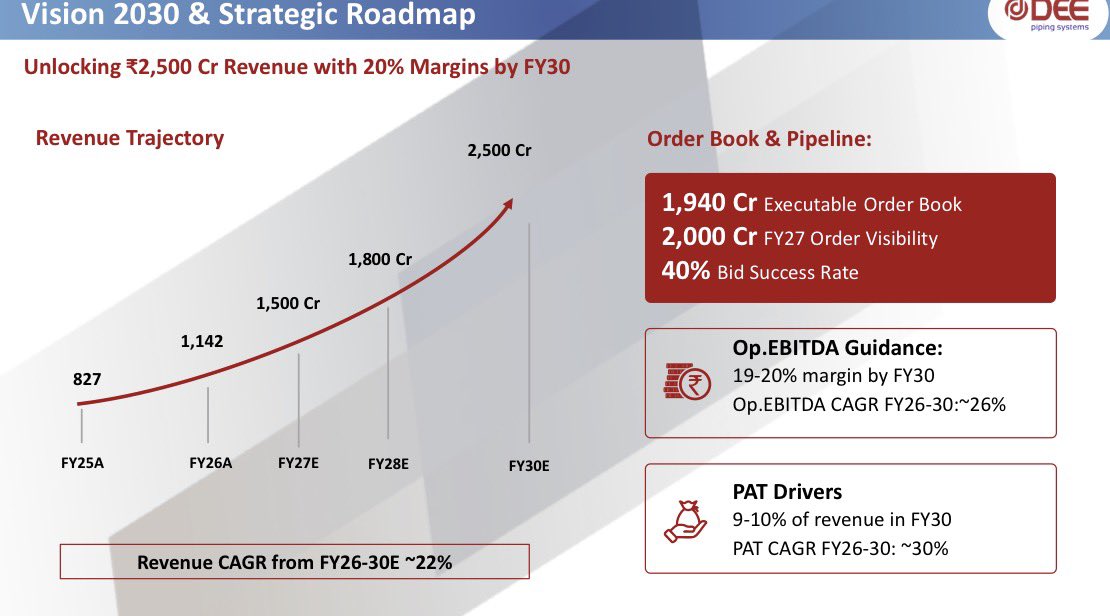

Vision 2030

Management is guiding to ₹2,500 Cr revenue at 20 percent margins by FY30,

a revenue CAGR of around 22 percent and PAT CAGR of around 30 percent, on

the back of thermal, refining, nuclear, data centre, and semiconductor

piping demand.

Strong topline and core-margin momentum, a completed backward-integration

build-out that could re-rate margins if utilisation ramps, high export-led

order visibility, offset by an elevated (though improving) leverage profile

and a non-core segment mid-turnaround. The thesis lives or dies on seamless

plant utilisation and deleveraging execution.

Trailing earnings put the stock at around 45x on FY26 EPS, so this is not a

cheap-on-trailing name. The multiple is a bet on the FY27 to FY30 ramp.

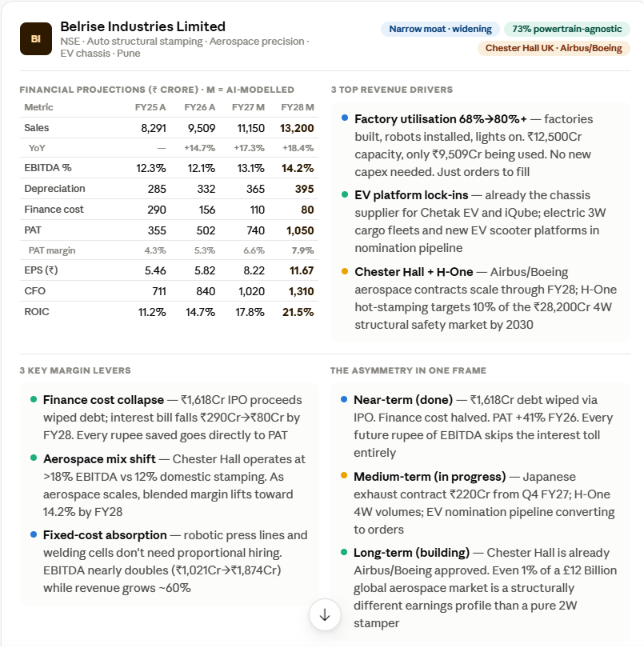

#BelriseIndustries#BELRISE

Everyone's debating ICE vs EV. Belrise Industries doesn't care who wins.

73% of its component lines supply the chassis, frame, and body — parts every vehicle needs regardless of what powers it. ICE or EV, the scooter still needs a skeleton.

But that's just the defensive moat. The asymmetry investors are actually betting on is a two-act play:

Act 1: ₹1,618 Crore of IPO money wiped out legacy debt — instantly freeing every incremental rupee of profit from interest payments. PAT surged 41% in one year on this single move alone.

Act 2: The same factory base that stamps chassis for Bajaj and TVS is now machining aircraft engine nacelles for Airbus — via Chester Hall UK — at >18% EBITDA margins vs 12% domestically.

The market is paying ~44x trailing earnings for this story. Is there enough in the order pipeline to justify it?

Business story

The story starts in 1988 as Badve Engineering — a metal stamping shop in Maharashtra making chassis brackets for India's booming two-wheeler industry.

First pivot: from parts maker to systems integrator. Instead of stamping individual components, Belrise became a single-source Tier-1 supplier — designing and delivering the entire integrated chassis assembly for Bajaj and TVS. This earned them a non-negotiable seat at the platform table for every new model launch.

Second pivot: EV-proofing the business. When Bajaj launched Chetak EV and TVS expanded iQube, Belrise was already locked in as the chassis manufacturer. Electric drivetrain, same steel skeleton — zero revenue at risk.

Third pivot — the bold one: precision engineering for aerospace. In 2024, the company rebaptised itself Belrise Industries and acquired Chester Hall Precision Engineering (UK) — a certified Airbus and Boeing supplier machining components to tolerances thinner than 0.2 microns. Suddenly India's largest scooter chassis maker is also making thrust reversers for commercial jets.

The fourth move: acquiring H-One India's hot-stamping capabilities — unlocking ultra-high-strength crash structures for passenger cars and SUVs, doubling the domestic content-per-vehicle opportunity.

From a Pune stamping shop to a four-vertical global engineering platform in 36 years. That's the business story.

Moat:

Verdict: Narrow moat. Widening. Competitive advantage period of 5-10 years.

Four structural pillars — three rated Strong, one Moderate:

① Entry barriers are brutal. A new entrant needs ₹1,000-1,500 Crore of capex, then 2-3 years of OEM sourcing audits, then PPAP/PPQ clearances — before earning a single order. For aerospace (Chester Hall), add 3-5 years on Airbus/Boeing approved supplier lists. Nobody shortcuts this.

② Platform lock-in is near-absolute. Once tooling dies are customized for a vehicle platform, switching suppliers mid-lifecycle costs the OEM 6-12 months of downtime and multi-crore tooling rebuilds. Customer churn rate mid-lifecycle: virtually 0%.

③ Powertrain agnosticism is the structural insurance. 73% of component lines are body/frame focused — the part of the vehicle that never changes regardless of what powers it. Not one engine component. Not one injector. Zero ICE obsolescence risk.

④ Raw material cost edge: Moderate. Index-linked pass-through contracts absorb steel price spikes on a 1-quarter lag — protecting gross margins from commodity cycles. But Belrise doesn't control the steel price itself; it just passes it faster than competitors can.

Valuation & operational leverage:

The numbers (AI-modelled, directional only — compass not GPS):

FY26 A: Rev ₹9,509Cr | EBITDA 12.1% | PAT ₹502Cr | EPS ₹5.82 | ROIC 14.7%

FY27 E: Rev ₹11,150Cr | EBITDA 13.1% | PAT ₹740Cr | EPS ₹8.22 | ROIC 17.8%

FY28 E: Rev ₹13,200Cr | EBITDA 14.2% | PAT ₹1,050Cr | EPS ₹11.67 | ROIC 21.5%

Is there big operational leverage? Yes — and it's coming from two directions simultaneously. Finance cost collapsed from ₹290Cr (FY25) to ₹156Cr (FY26) to a projected ₹80Cr by FY28 as IPO proceeds cleared debt. And EBITDA absolute value nearly doubles (₹1,021Cr → ₹1,874Cr) while revenue grows ~60% — fixed robotic press lines and automated welding cells don't need proportional hiring.

EPS CAGR FY25-28: >44%. PAT nearly triples. On a relatively fixed share base.

Growth triggers:

✅ New Japanese auto major exhaust contract — ₹220Cr peak run-rate from Q4 FY27

✅ Chester Hall aerospace integration scaling to >18% EBITDA mix by FY28

✅ H-One hot-stamping unlocking 4W passenger car safety structures — market growing 11.4% CAGR

✅ Factory utilisation climbing from 68% → 80%+ on existing ₹12,500Cr capacity base

✅ Finance cost falling to ₹80Cr (0.6% of sales) — interest coverage >23x by FY28

Red flags:

⚠ Bajaj + TVS = heavy anchor client concentration — a demand slowdown in 2W hits utilisation directly

⚠ Chester Hall integration delay = near-term cost drag on consolidated margins

⚠ Pre-IPO income tax search (2021) — resolved but flags historic compliance patterns

⚠ Working capital cycle stretched to 65 days — improving but requires monitoring

Management quality & governance

Shrikant Badve (MD) has built this from a local toolroom to a ₹9,500Cr revenue global platform over three decades. The Chester Hall and H-One acquisitions were his strategic calls — and both have strategically sound logic (aerospace margins lift the consolidated blended EBITDA, hot-stamping unlocks 4W safety structures).

74.8% promoter holding, zero pledged shares. The IPO was a fresh issue — no OFS. The singular most important governance signal: management promised in the DRHP to use ₹1,618 Crore to pay down debt. They did exactly that. Finance costs dropped 46% in one year, directly producing the 41% PAT surge. Said it. Did it.

Governance flags:

⚠ Income Tax search and seizure across Badve Group premises in 2021 — obligations subsequently settled but worth noting as a pattern in a fast-scaling family-led group

⚠ Pre-IPO entity structure was complex (Badve Polymers, Badve Engineering, multiple sub-entities) — corporate consolidation into Belrise improves transparency but historical RPTs require scrutiny

⚠ Cross-border integration of UK and French aerospace subsidiaries introduces jurisdictional governance complexity — audit committee bandwidth will be tested

⚠ Key operational knowledge concentrated in Shrikant Badve personally — succession planning not yet institutionalised

Order pipeline — does it justify ~44x P/E?

The core pipeline is structural, not project-based — and that's what makes it different from most capex stories.

Belrise doesn't have a project backlog. It has platform lifecycle allocations — multi-year, single-source contracts tied to the entire production run of a vehicle model. When Bajaj launches a new scooter platform for 5-7 years, Belrise is the chassis supplier for every unit. That's recurring, non-cancellable, and doesn't require re-tendering.

What's new and quantifiable:

→ Japanese auto major exhaust contract — execution from Q4 FY27, peak run-rate ₹220Cr annually

→ Chester Hall aerospace backlog — Airbus/Boeing sub-assembly orders extending into FY28-29

→ H-One 4W hot-stamping — targeting 10% market share in the ₹28,200Cr passenger car structural safety market by 2030 (currently at 4%)

→ EV platform nominations — already locked as chassis supplier for Chetak EV, iQube; new electric 3W cargo fleets in pipeline

Belrise's factories are running at only 68% capacity. The machines are already bought and paid for. Getting more orders to fill the remaining 32% costs almost nothing extra — but every rupee of that extra revenue goes almost directly to profit.

Watch Q4 FY27 for the Japanese exhaust contract revenue going live — first real test of execution velocity beyond the core anchor clients.

Closing thesis

So, are there real asymmetries to justify the ~44x valuation on an auto ancillary?

The near-term asymmetry was the balance sheet inflection: ₹1,618Cr of debt wiped in one move, finance cost halved, every incremental EBITDA rupee now flows directly to PAT without an interest toll. That move has already happened. PAT +41% in FY26 was the proof.

The long-term asymmetry is the precision engineering shift: the same factory culture that stamps a motorcycle chassis to 0.05mm tolerance is now machining aircraft nacelles to 0.0002mm for Airbus. If that aerospace division scales from <1% to even 1% of a £12 Billion global market — and Chester Hall is already an approved Airbus/Boeing supplier — that's a structurally different earnings profile than a pure 2W stamper.

The valuation doesn't require a miracle. It requires:

✅ Factory utilisation going from 68% → 80% on existing assets

✅ Chester Hall and H-One integrating into consolidated EBITDA above 14%

✅ The Japanese exhaust contract and new EV platform nominations converting on schedule

✅ Finance cost staying near zero as remaining debt pays down by FY28

It cracks if:

⚠ Bajaj or TVS volumes disappoint for 2+ consecutive quarters

⚠ Chester Hall integration drags cost overruns into FY28

⚠ India 2W demand cycle turns — Belrise has no consumer-facing cushion

Not a buy/sell call. AI-modelled numbers for directional perspective only. DYOR.

#LloydsMetals is one of those rare stories where the stock rally looks crazy…

until you see what has happened inside the business.

A few years back, this was largely an iron ore story.

Today, the company is slowly turning into a full metals platform:

Iron ore → pellets → DRI → steel → copper.

And the latest production update again shows that this is not just a PPT story anymore.

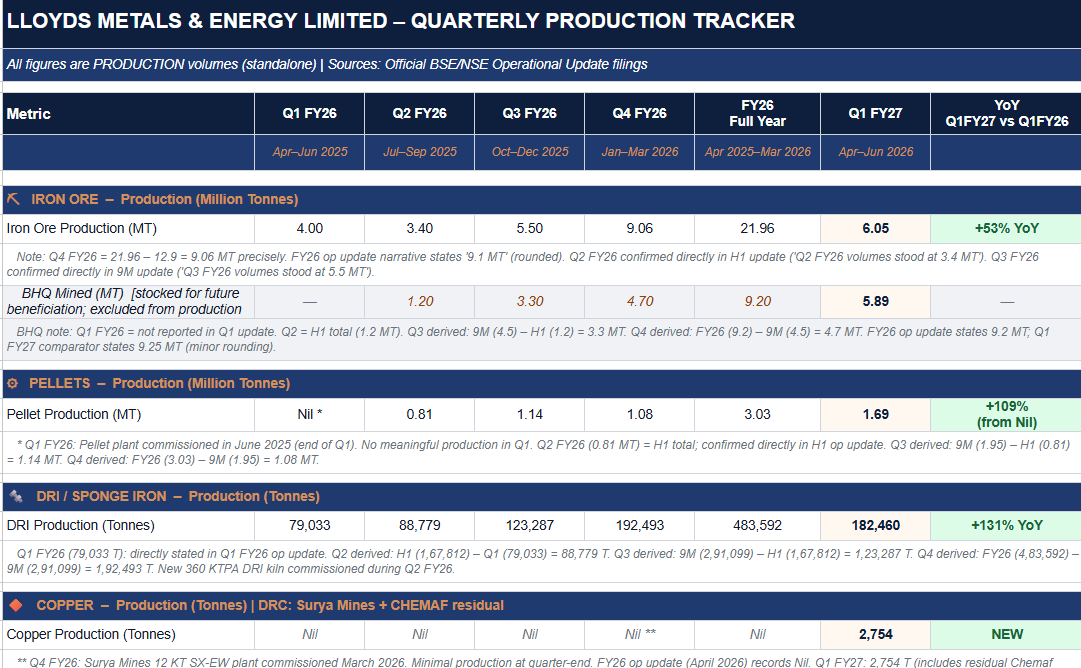

The scale-up is now visible

Q1 FY27 production was strong across key divisions.

Iron ore was up 53% YoY.

Pellets were up 109% YoY.

DRI / sponge iron was up 131% YoY.

Copper also started contributing.

So the growth is not coming from one lucky segment.

The base business is scaling, and new verticals are slowly entering the numbers.

The most interesting part is the operating leverage

This is where the story becomes crazy.

FY24 standalone sales were around ₹6,575 Cr.

In Q4 FY26 alone, Lloyds did almost ₹5,000 Cr revenue.

Basically, what earlier looked like an annual scale is now close to becoming a quarterly run-rate.

Same with profits.

FY25 full-year PAT was around ₹1,451 Cr.

Q4 FY26 PAT alone was ₹1,066 Cr.

This is what happens when mining, pellets and DRI start working together.

This did not happen overnight

The management has quietly done the hard work in the background.

Mines were scaled.

Pellet capacity came up.

DRI expanded.

Slurry pipeline started reducing logistics cost.

Copper entered through DRC.

Steel is the next leg.

The market usually sees the result at the end.

But the real story was built during the capex phase.

The capex is massive

Lloyds has spent aggressively over FY24-FY26.

FY26 alone saw more than ₹8,000 Cr of capex.

That is not small.

This is not a company just trying to benefit from higher iron ore prices.

It is trying to build a larger integrated metals ecosystem.

If done well, every step of the value chain can add margin, control and scale.

FY27 becomes the proof year

The company has guided for higher volumes in iron ore, pellets, DRI and copper.

Pellets should see a much bigger full-year contribution.

DRI should scale further.

Copper is still early, but it opens a completely different optionality.

And steel commissioning will be the next big thing to track.

So FY27 is less about announcements. It is about conversion.

Capex has to convert into production.

Production has to convert into margins.

Margins have to convert into cash flows.

The shareholder question is different now

After such a big rally, the question is no longer:

“Is Lloyds a good business?”

The real question is:

“Can the company keep executing fast enough to justify the valuation?”

Because expectations are now high, every quarter will matter.

Volumes, margins, debt, project timelines and copper execution will be watched closely.

The simple view

Lloyds Metals has gone from being a mining story to becoming a transformation story.

If management keeps delivering, this can become one of India’s most interesting integrated metals platforms.

If execution slips, the stock can punish quickly because a lot of future growth is already getting priced in.

That is the beauty and risk of such stories.

Big opportunity, big execution ask.

Worth tracking closely, but not blindly chasing.

Not a recommendation.

Panacea : note..if you don't keep on journaling your investment with pen and diary you won't map in your brain

Multiple engine growth trigger

Phase 3 trial or final stage almost done on many single shot doeses + africa revenue opportunities

Bigger demand = bigger problem solving= bigger chances of market cap expansion

Not momentum

Not timing

We need to spend time over creeze

@UrsRafeek@LnprCapital Thank you so much. I was just flagging the inefficiency here, why make someones life harder by doing inverse things.

I appreciate the account a lot, but the information is redundant without stocks name

I believe Cable & Wires is one of the biggest beneficiaries of the CAPEX cycle over the next 3–5 years.

Power Transmission, Renewable Energy, EVs and Data Centers all have one thing in common.

They all need to carry electricity.

That can only be done through cables and wires.

But the industry is much more than just one product.

There are Optical Fibre Cables, Magnet Winding Wires, LT Cables, HT Cables and EHV Cables. Each serves different end markets, and some companies specialize in niche, high-value products with strong entry barriers.

This opportunity is also not limited to India.

The US, Europe and many other countries are investing heavily in grid modernisation, renewable energy and data centre infrastructure, creating a structural demand tailwind for the sector.

One thing to be cautious about is execution, especially for EPC companies.

In EPC businesses, a large order book alone doesn't create shareholder value. Execution is what matters. Cost overruns, project delays or disruptions—particularly in government projects—can materially impact profitability.

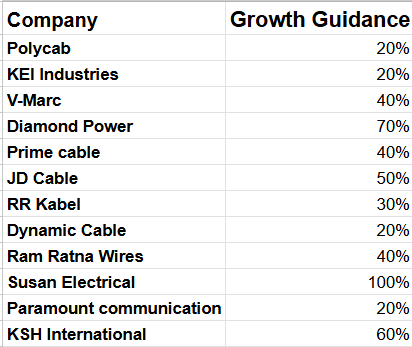

Over the past few months, I've studied multiple Cable & Wire companies, analysed their business models, growth drivers and management guidance.

I've compiled my key learnings along with each company's growth outlook. For companies that did not provide explicit guidance, I've mentioned the recent growth rate instead.

Hope you find it useful.

KSH International:

https://t.co/VsXmmLaXj4

Paramount communication:

https://t.co/oMR4typCIs

Polycab:

https://t.co/HXadsubkEy

KEI Industries:

https://t.co/wyWbANZYJ3

Dynamic Cable:

https://t.co/tO1soixBAo

RR Kable:

https://t.co/imRouSpezH

Ram Ratna Wires:

https://t.co/Ed351BOifu

Prime Cable:

https://t.co/rqPMhKzsLG

JD Cables:

https://t.co/r8OKsbv1Zo

Susan Electricals:

https://t.co/IAjyI8UQGE

Diamond Power:

https://t.co/Ta48Hfr22z

V-Marc:

https://t.co/8ClyY3hcYR

"Why is India spending money on space when we still have problems on Earth?"

A few years ago, a reporter even went so far as asking a former ISRO chief:

"What's in it for the farmers?"

These are the type of questions that get asked every time ISRO launches a mission.

I guess people just assumed that:

Money spent on space disappears into space.

But history suggests the exact opposite.

A few years ago, ISRO engineers used technology originally developed for rockets to create a low-cost heart assist device called Left Ventricular Assist Device (LVAD)

For patients suffering from severe heart failure, the device can help pump blood when the heart itself struggles to do so.

Think about that for a moment.

A technology born inside India's space programme found a second life inside a hospital.

This is where most people misunderstand the economics of a space programme.

The rocket is visible.

The ecosystem it creates is not.

And that is often where the real value gets created.

This isn't an isolated example.

ISRO's space programme has contributed to smart prosthetic limbs, medical technologies and numerous technology transfers to Indian industry.

My favourite example is Hydrophobic silica aerogel.

Originally developed for cryogenic rocket systems, the same material can also be used in winter clothing and boots for soldiers stationed in places like Siachen.

Technology built to protect rockets.

Later helped protect human beings.

And this isn't unique to India.

The CMOS image sensor inside billions of smartphones traces its origins to efforts to build smaller and more efficient imaging systems for advanced applications, including space missions.

Digital image-processing technologies developed for space exploration also found applications in medical imaging as well.

This pattern repeats across every major space programme.

To reach space, you are forced to solve some of the hardest engineering problems known to mankind:

• Materials

• Electronics

• Sensors

• Computing

• Manufacturing

Once those capabilities are built, they rarely remain confined to space.

They spread throughout the economy.

Entire industries emerge.

Skeptics often ask:

"What is the return on investment from a space mission?"

Perhaps a better question is:

"What technologies would never have existed if we had never attempted the mission in the first place?"

And from an investor's perspective, this may be the most important insight of all.

The largest economic value created by a space programme often doesn't come from the launch itself.

It comes from the ecosystem of materials, electronics, sensors and manufacturing capabilities that the programme forces a country to develop.

The rocket is visible.

The ecosystem it creates is not.

That ecosystem is precisely what we're trying to understand in our upcoming webinar on India's Space Revolution.

Because the future of the space sector may not be decided only by who launches rockets.

It may be decided by who builds everything underneath them.

Registration link in comments !