Bolivia is being read abroad as another EM reform story.

Subsidies. Protests. IMF. Lithium. Bonds. Investor patience.

All relevant.

But not enough.

The old political order lost the presidency, but it did not leave the operating system.

That is where the story turns darker.

Stuck in the Loop, Part IV

The Country They Keep Misreading

https://t.co/EXT71isLU5

No lo llamaría manipulación. Es una política cambiaria dirigida, con un indicador cuya composición cambió.

El “referencial” del BCB no es el paralelo. Se construye con operaciones reportadas por las entidades financieras. Desde abril, el BCB incluyó en el Valor Referencial de Compra operaciones que para las EIF representan posición en bancos corresponsales del exterior.

Eso es clave. El dato no solo mira operaciones con clientes en Bolivia, sino también una parte de la posición externa de los bancos. Y en paralelo el BCB ha venido empujando a la banca a reducir posiciones largas en moneda extranjera. Si cambia la muestra de operaciones y cambia el incentivo regulatorio sobre esas posiciones, el referencial puede moverse por diseño de política.

Se puede criticar la opacidad, el retraso en la publicación y la pérdida de comparabilidad de la serie. Pero llamarlo manipulación confunde el problema. Es administración cambiaria bajo escasez de divisas, con un indicador que mezcla mercado, regulación y posición externa bancaria.

Concuerdo. El MAS siempre fue una mezcla extraña de discurso revolucionario, corporativismo, culto al líder, presión sobre las instituciones y lógica de amigo/enemigo. Ahí entra la teoría de la herradura: los extremos terminan pareciéndose más entre sí de lo que admiten. Cambian las banderas, los símbolos y hasta el color del pelo del Joker, pero la intolerancia al disenso, la captura institucional y la lógica de poder terminan siendo demasiado similares.

Y cuando a eso se le suma ignorancia, populismo y falta de educación cívica, el incendio solo crece

Hey WSJ, this one needs sharper analysis.

This is not a right versus left story. That frame is too easy, too Washington, and honestly not very useful for understanding what is happening.

Rodrigo Paz was not elected as some right wing tribune with a Milei style mandate. He won because the previous model collapsed and people wanted MAS out. Dollars disappeared, fuel became scarce, reserves were drained, inflation came back, and the state kept pretending the exchange rate regime still worked long after the economy had already moved on.

That matters because Paz is not governing like a hard right reformer either. He is already offering bonos and cash transfer style measures, very à la Lula, to calm the streets and buy social peace. Maybe that is politically understandable. But it does not fit the story of a clean conservative wave being tested by left wing resistance.

Bolivia is much messier than that.

Paz inherited wreckage. Part of the old machinery is still inside the state. The street already knows how to veto adjustment. The financial system is increasingly tied to public sector risk. The dollar system fractured before the government admitted it had fractured. Subsidies became impossible before the state had a credible replacement.

So the protests are not simply anti right unrest. They are the first stress test of a weak government trying to stabilize a broken model while the old order still has enough power to block the country.

The Trump ally angle is also thin. Washington may like the optics around lithium, China and post MAS Bolivia. Markets do not price Miami summits. They price reserves, inflation, the parallel dollar, IMF sequencing, bank balance sheets, social unrest and whether the government can execute adjustment without the street becoming the real finance ministry.

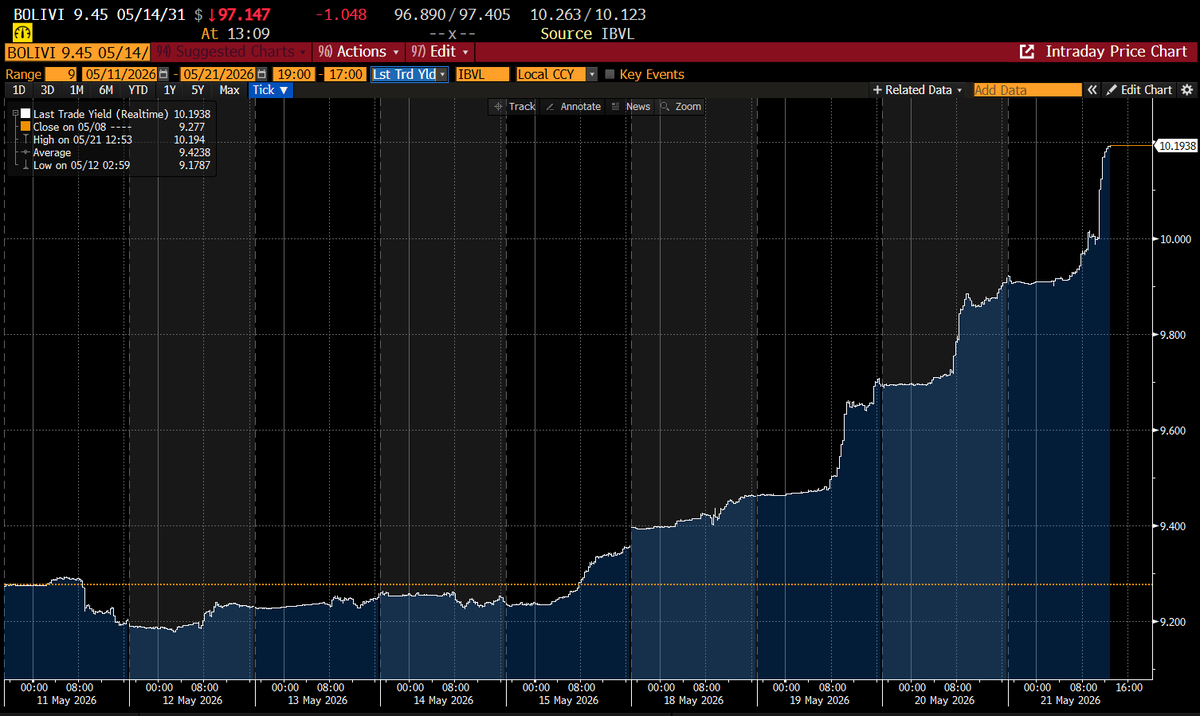

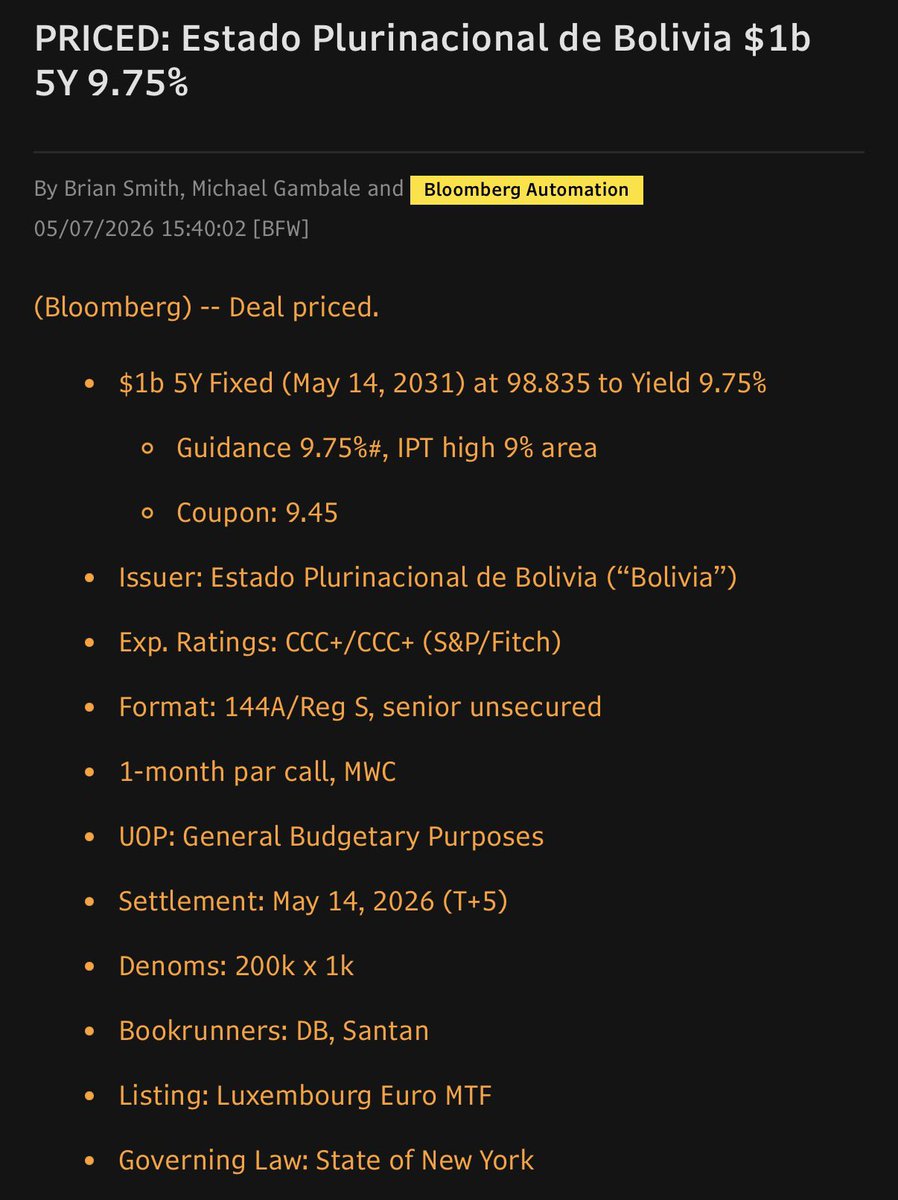

The new bond says the same thing. Bolivia regained market access, not market normalization. A USD 1 billion five year bond issued at a 9.75% yield and already trading closer to 10.3% is not a victory lap. It is a warning label.

This is not a conservative wave story. It is a state capacity story, an FX crisis story, a fiscal crisis story and a confidence crisis story.

Bolivia does not need better ideological labeling. It needs analysis that understands the machine that broke.

Yes. I would have waited.

The whole point of an IMF program is precisely to reassure the market before borrowing, not after. It gives investors a policy anchor, a financing envelope, conditionality, and some confidence that the adjustment path is not just political improvisation. That is how countries improve borrowing conditions.

Ecuador is the clean comparison. Market access improved after the IMF framework helped stabilize the story. Ghana and Egypt show the same basic logic in different settings. Once the Fund architecture is in place, investors may still demand a premium, but they are pricing a clearer policy framework rather than pure uncertainty.

Bolivia did the sequence backwards. It went to the market before the IMF package, so investors priced the uncertainty directly into the bond. That is why the result looks like access, but not normalization. A 9.45% yield, five year maturity, and almost immediate trading above 10% is not a clean vote of confidence. It is the market saying we will lend, but only if we are paid enough for the risk.

So yes, squarely. I would have waited for the IMF package first, then issued. Unless the government was under immediate cash pressure and had no choice, this looks like rushed prefunding at a high price.

Bolivia reopened the door. But it paid to open it before the credibility anchor was fully in place.

I wrote the broader argument here

https://t.co/EcrmjwNgu0

Bolivia’s new 2031 bonds did not even get a honeymoon.

Issued at a 9.75% yield, they are already trading above 10.1%. That is the market’s way of saying the optimism around fresh external financing is conditional, fragile, and reversible.

The problem was never just access. It was credibility.

Bolivia managed to reopen the door, but investors are already asking whether the adjustment program behind that access is politically durable enough to matter. In a country still trapped between FX scarcity, fiscal stress, fuel subsidies, and weak governability, a new bond can

buy time.

It cannot buy confidence.

Partly true, but that is not enough.

U.S. Treasuries moved higher, yes. But Bolivia is not just repricing mechanically with the global rates backdrop. The new 2031 is moving worse than comparable frontier/high yield sovereigns like Ecuador and Egypt over the same window.

That is exactly the point. The market is not only pricing U.S. duration. It is pricing Bolivia risk.

A new bond issue proves market access. It does not prove credibility. And when a newly issued bond breaks above 10% almost immediately, the market is already telling you that the adjustment story has not been bought in full. Too early for a final verdict, yes. Not too early to see that the honeymoon was basically nonexistent.

Ministro, con respeto, La Paz lleva semanas sitiada por grupos violentos, bloqueadores y delincuentes mientras miles de familias pasan horas buscando comida, combustible o simplemente tratando de trabajar. La gente no está pidiendo discursos sobre paciencia. Está pidiendo que se aplique la ley.

Pedimos que quienes destruyen, bloquean y aterrorizan a la población enfrenten consecuencias reales, pero en cambio el Gobierno habla de bonos, diálogo y cuotas de poder. Pedimos paz, pero se nos responde con más “aguantar”. Pedimos libertad para trabajar y producir, mientras el mismo Estado sigue protegiendo privilegios y regímenes especiales, incluso para sectores como los cooperativistas auríferos que continúan operando con niveles absurdamente bajos de tributación en medio de una crisis nacional.

La democracia no se defiende únicamente con declaraciones. Se defiende con Estado de derecho, instituciones fuertes, seguridad jurídica y respaldo al sector privado y a la ciudadanía que sostiene el país trabajando. Sin eso, hablar de democracia mientras la población vive paralizada y extorsionada pierde credibilidad rápidamente.

La Paz is tense before the IMF program has even arrived.

That is the warning. Bolivia has market access, but not stabilization. The streets are moving, inflation is still high, banks are hedging, and the old political machinery was never fully removed.

Stuck in the Loop Part 3: The Market Opened, the Streets Closed https://t.co/EcrmjwNgu0

If anything, Bolivia’s current crisis reflects how little structural reform has actually taken place. The current administration inherited a deeply fragile macro setup from MAS, but it has also failed to decisively dismantle the political and institutional networks that created the problem in the first place.

Many of the actors tied to the previous administration continue operating inside the state apparatus, while Evo Morales and the remnants of MAS still retain significant mobilization capacity. The recent protests are not evidence of an aggressive market reform shock. They are evidence of weak political maneuvering, delayed decisions, and a government that spent too long trying to coexist with forces actively working to destabilize it.

@g_espinoza Felicidades. Pregunta, por qué salir al mercado ahora antes de la confirmación de un programa con el Fondo? Teniendo el programa no ayudaría a bajar la tasa e incrementar el monto y tal vez el plazo?

Bolivia just issued USD 1bn in 5Y debt at 9.75%.

The signal is mixed.

Authorities are also seeking up to USD 3.3bn from the IMF. Normally, stressed sovereigns try to secure the IMF anchor first, then return to markets with lower uncertainty. Ecuador is the cleaner comparison: IMF framework first, stronger market access after.

Bolivia seems to be doing part of that sequence backwards.

Pricing also matters. The target was reportedly closer to 9%. Final yield came at 9.75%. Oversubscription helps the headline, but demand at a high coupon is not the same as restored confidence.

Then maturity. Five years is short. Côte d’Ivoire placed longer dated paper in 2024, including roughly 9Y and 13Y maturities. Ecuador also managed longer maturities once the IMF story was more anchored.

So yes, Bolivia reopened market access. But this still looks more like expensive bridge financing than clean normalization.

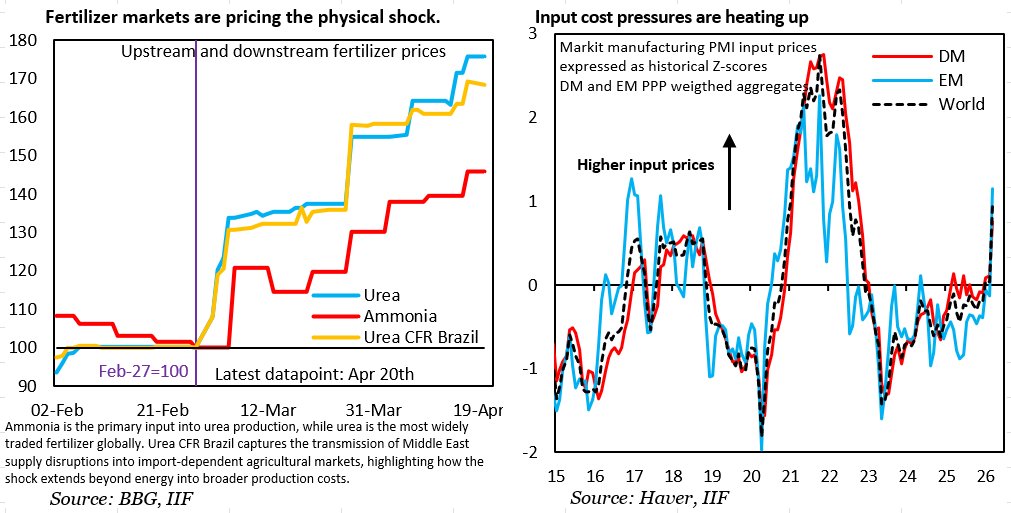

The key question is no longer just where oil settles. It is whether the shock is starting to spread into inputs, fertilizers, and supply chains more broadly.That is what looks increasingly likely.If so, the next phase is not really about relief. It is about transmission.And once that process gets going, inflation becomes much harder to bring down.

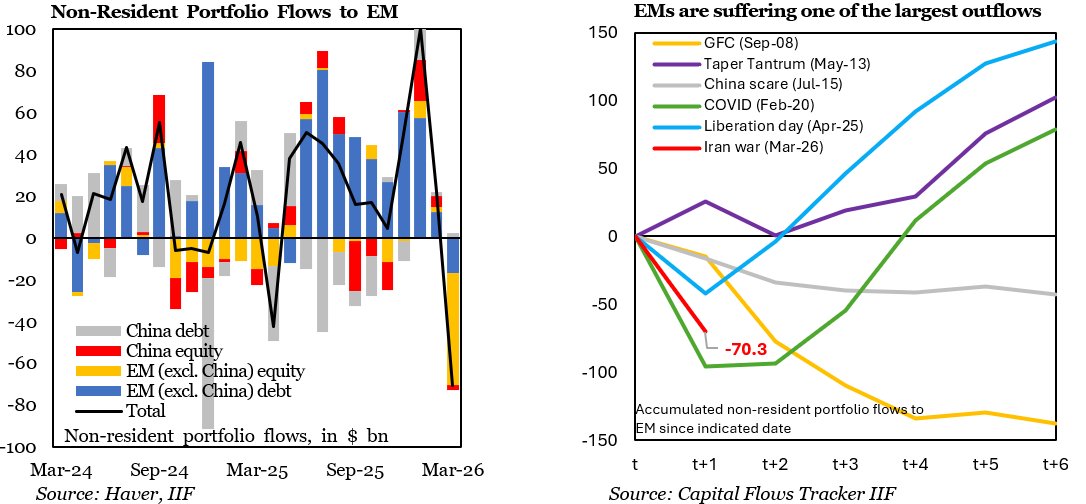

EM flows just had one of their worst months since the pandemic.

And it came in the first month of the Iran war.

March saw ~ $70 bn in outflows. Not a drift. A break.

So far this is an equity liquidation story, not a full funding stop. But that is how these episodes begin.

A truce may stabilize things.

But with this kind of on and off risk, the real shift is rising variance.

And that is where accidents happen.

The most dangerous moment in a stabilization is not the shock. It is the calm that follows.

Bolivia has lifted fuel subsidies. Protests are starting, the government is negotiating, and markets have already moved on. Spreads have compressed. Market access suddenly looks imaginable again.

That is exactly when bad sequencing becomes tempting.

In Stuck in the Loop, Part II, I look at why this moment feels like progress and why it is not. How market appetite can return before the macro regime is fixed. Why Bolivia’s debt composition matters more than the headline ratio. And why low reserves turn “going back to markets” into a much harder problem than it appears.

This is the second entry in a time-loop series on Bolivia’s recurring adjustment cycle. Same country. Different cast. The same structural trap around timing and escape.

The danger is not that Bolivia cannot borrow.

The danger is that it can.

Link below.

https://t.co/PpRppwPDCZ

Precisamente porque la Constitución es un sistema, no se le pueden inyectar definiciones que no contiene. Leerla como sistema no autoriza a convertir costumbres administrativas en reglas constitucionales ni a completar silencios con intuiciones políticas.

La interpretación sistemática exige coherencia entre lo que el texto dice y lo que deliberadamente no dice. El artículo 169 regula la ausencia. El 173 regula la autorización de viajes. Ninguno define la ausencia como territorial ni establece una pérdida automática del mando por salir del país. Un sistema constitucional no se construye agregando piezas que el texto no puso.

Decir “es un sistema” no responde a la pregunta central. Solo la evita. Y cuando el intercambio deja de producir argumentos nuevos y se reduce a repetir etiquetas generales, el debate se agota.

Hasta aquí llego. No por falta de interés, sino porque ya no hay nuevos argumentos jurídicos sobre la mesa.

El argumento confunde planos que no son equivalentes. La suplencia de un ministro es derecho administrativo ordinario. La suplencia del Presidente es derecho constitucional. Pretender que ambos operan bajo la misma lógica es un error de categoría.

Que en la administración pública la suplencia formal sea la práctica regular no dice nada sobre cómo se define la ausencia constitucional del Jefe de Estado. Los ministros no concentran titularidad de poder político originario. El Presidente sí. Por eso la Constitución dedica un artículo específico, el 169, a regular su ausencia. Y ese artículo, otra vez, no define la ausencia como territorial ni automática por viaje.

Invocar un decreto de suplencia ministerial para “probar” que la ausencia presidencial opera ipso iure es un salto lógico injustificado. La regularidad administrativa no crea regla constitucional. Menos aún cuando el propio texto constitucional no usa el criterio geográfico que se le quiere imponer.

Tampoco hay ningún “subterfugio” en distinguir entre ausencia funcional y ausencia territorial. Eso no es improvisación, es precisamente lo que la Constitución permite cuando no cierra el concepto. Si la CPE hubiera querido que todo viaje active suplencia automática, lo habría dicho expresamente. No lo hizo.

Decir que esta distinción “desnaturaliza” el orden institucional es invertir el problema. Lo que desnaturaliza el orden constitucional es leer en la Constitución lo que no dice para forzar una conclusión previa.

El artículo 169 activa la suplencia cuando hay ausencia constitucional. El debate es qué constituye esa ausencia. Repetir que “opera ipso iure” no resuelve nada, porque presupone justamente lo que está en discusión. Es razonamiento circular.

La práctica administrativa puede ser consistente, pero no sustituye la interpretación constitucional. Y en este caso, la Constitución no convierte cada viaje en una ausencia automática, por más que durante años se haya actuado como si lo hiciera.

Decir que el artículo 173 “define” la ausencia como territorial es una lectura incorrecta del texto. El art. 173 no define ausencia ni regula la suplencia presidencial. Regula otra cosa: la autorización política para que el Presidente salga del territorio nacional por misión oficial, fijando un umbral temporal. Eso es control legislativo del viaje, no definición constitucional de ausencia.

La norma que regula la ausencia y la sustitución es el artículo 169. Y el 169 no califica la ausencia como territorial, no habla de fronteras ni establece que salir del país active automáticamente la suplencia. Vincular 173 y 169 como si uno cerrara el significado del otro es una inferencia que el texto no hace.

Que el Presidente requiera autorización para ausentarse más de cierto número de días no implica que, una vez autorizado, pierda el ejercicio del mando. Son planos distintos: uno es control político del desplazamiento, el otro es titularidad del poder. La CPE no dice en ningún lado que autorizar un viaje equivalga a declarar ausencia constitucional.

Tampoco se trata de “importar modelos extranjeros por decreto”. La comparación regional sirve para mostrar que la idea de un mando estrictamente territorial no es una regla inherente al presidencialismo, sino una elección interpretativa local. Y si ese límite geográfico fuera estructural en la CPE, estaría escrito. No lo está.

La Constitución habla de ausencia e impedimento, no de pasaportes ni de coordenadas. Convertir una norma de autorización de viajes en una cláusula de pérdida automática del mando es una sobrelectura, no una exigencia constitucional.

Llamar “tontería” a una interpretación constitucional no la convierte en violación. Si es flagrante, debería ser fácil señalar qué artículo dice explícitamente lo contrario. Y no lo es, porque el artículo 169 no define ausencia ni equipara viaje con impedimento.

Decir “violación de la CPE” sin identificar una prohibición textual es retórica, no derecho. Es indignación sustituyendo análisis.

Además, esto no es un invento local. En Argentina, Chile, Colombia, México o Estados Unidos, los presidentes gobiernan desde el exterior sin que nadie hable de quiebre del Estado de derecho. Si eso fuera liberalismo cínico, medio continente estaría en falta permanente.

Criticar al sistema judicial boliviano es legítimo. Pero usar esa crítica para cerrar cualquier debate interpretativo es confundir diagnóstico estructural con el caso concreto. Cuando todo es “flagrante”, nada lo es.