Futurist: I predict, publish & speak. Entrepreneur: past in tech, food, education; current in pets, telecom, SaaS, food. I post insights mapping tomorrow.

I'm starting to feel like the chump in this story. I learned a long time ago that when everyone is on the same side of the boat, the risk of capsizing goes up, and the hype around a SpaceX IPO is at a level I’ve never seen in my lifetime. The original investors, market makers, and funds don’t really care because they get paid regardless of what happens after the stock starts trading. That leaves retail investors, who often end up being everyone else’s exit strategy—the chumps. A chump, after all, is someone who is gullible, easily deceived, or easily taken advantage of. If someone truly wants exposure to SpaceX, it may make more sense to wait until the lock-up periods expire, the smart money has had a chance to exit, the stock inevitably takes a hit, and then consider buying at a much lower price.

The Indonesian rupiah has been on a long-term weakening trend compared to the U.S. dollar. THe country is doing fine generally and a more stable emerging market, but the U.S. just continues to be the epicenter for economic growth relative to everyone else and demand for U.S. dollars is only going up.

Will the Hormuz disruption trigger a level of demand destruction not seen since World War II? I've seen credible arguments on both sides. Some analysts warn of severe economic consequences, while others—equally respected—argue that the global economy is far more resilient and adaptable than many assume, making such an outcome unlikely. So who will be right? As is often the case, the answer may lie somewhere in between. The coming months will reveal whether this becomes a historic economic shock or another crisis that markets and supply chains ultimately absorb.

We are well past the point where the last tankers of pre-war exports have reached their destination. So, everyone's just been burning through stocks, and at some point, in either June or early July, we're going to basically reach minimum operating inventory levels for half the world, if not more.

Prices go through the roof because there isn't enough throughput. It's not that people have cut refinery runs for the most part. It's the simple fact that we're running out of feedstock. And when that happens, you get this lovely thing called demand destruction, where prices rise to a point that some parts of the economy, some people in some parts of the world can't afford the crude-derived products at all.

When that happens, their demand is destroyed until prices fall back into line. The last time the world experienced this scale of disruption wasn't the oil crises in the 70s or 80s. It was World War II when everything got sunk. So, historically unprecedented is the term. And keep in mind that with deglobalization, some large-scale version of this would happen regardless.

#iranwar #crudeoil #geopolitics

The world cannot live without China because of its manufacturing, so it is an economy I watch. If they falter, the world can't get products. You never know how truthful data is coming out of China (or even now the U.S., for that matter).

The current line is “AI can replace execution, but not taste.”

But taste is just compressed judgment from lots of exposure: see enough examples, classify enough good vs bad, and you develop instinct.

That is not a moat against AI.

That is a training set.

Weekly business formation are higher, likely because of AI, but does not neccessarily mean they are making money and also probably means disruption of existing businesses. So, is AI transforming the economy ? Yes. Will it lead to growth, more income, more meaningful employment? History suggests yes, over time, but the transition will be rough.

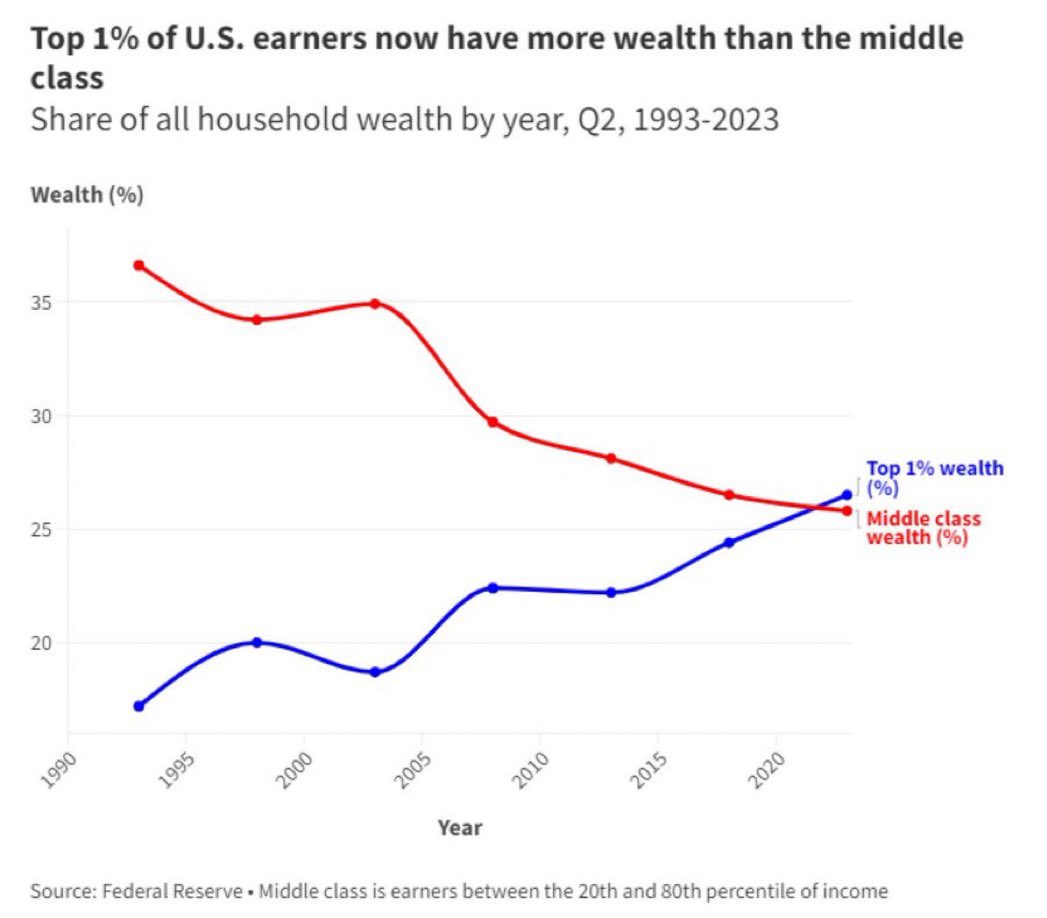

“The Top 1% of U.S. earners now have more wealth than the entire middle class.” Via @Barchart

*the longer we keep these colossal gains private — aka SpaceX going public in 2026 at $1.9T valuation vs. $33B in 2019, the more fuel we add to this chart?

This isn’t even remotely true. $AMZN went public in 1997 at a $450M valuation, or 3x revenues. $GOOGL went public in 2004 at a $23B valuation and at 7x revenues. $META had a $104B valuation in 2012 at 20x revenues(and immediately sold off almost 50%). SpaceX dwarfs these numbers.

Never bet against @elonmusk

A. Actual Tesla IPO return: near 1,000x → $10k invested → ~$2.6M–$3M today.

B. If Tesla had IPO’d at SpaceX’s current $1.75T valuation instead of the actual $2B in 2010:

Today’s return: -10%

Valuation at IPO matters. A lot. Grok data

https://t.co/4VXoCAkgwZ

A bad trend that shows no signs of reversing. But I have confidence this will get fixed when we realize that the source of our past and future success is a vibrant and healthy middle class, and we are serious about addressing it.

Here we see how much leverage retail investors are using to invest in public markets. Margin balances surged after 2020, corrected somewhat, and are now moving higher again. Is this a sign of frothy markets similar to past cycles and a warning of an impending decline? Perhaps, but I’m not convinced. We are experiencing an explosion of new investment platforms, tools, and opportunities that make it easier than ever for retail investors to participate. At the same time, we may be in the early stages of an economic supercycle driven by emerging technologies—AI, automation, robotics, energy, and other innovations—that increasingly reinforce and accelerate one another. There will certainly be drawdowns and corrections along the way, but I currently lean toward a multi-decade expansionary period rather than a prolonged era of sideways markets or secular bear market conditions.

This article is making the rounds and it gets some things right. Other things not so, because it depends on the industry you are in. My $.02: we no longer get hired to do tasks, we get hired to solve problems that save time and money, or we get hired to grow revenue. That is it. Completing tasks is increasignly the job of AI, not humans. https://t.co/oNePUZGLMK

This chart captures China in a nutshell. Exploding industrial production, falling consumer spending, stagnant production investment and a collapsing real estate market. The country is really imploding because of demographics, a property sector that is in decline (again, demographics) massive production capability that cannot be absorbed locally (again, demographics), and a world that is starting to put up barriers to China's manufacturing to protect local industries. A tough situation for the country. What can it do?

Investment booms now and then. Two charts here seemingly at odds with each other. One says we are stretched, the other says we still have a long way to go. Who is right? I would lean heavily towards the second chart, even going further and saying we are in the early innings of this investment boom because the late-1990s boom was focused on tech sectors, while the investment boom now is starting to span across all sectors, not just tech. And we have barely started in robots/automation. That in itself may dwarf what we see now.

Weekly analysis from emails of 700+ Brands.

5 years ago, I began subscribing to emails from consumer brands into a dedicated Gmail account. Now, I have an agent analyze the last week's email to surface anything interesting, in context of a playbook I created that tracks emerging strategies, tactics, technologies and business models for consumer brands. Then, I do macro analysis across several months of data to surface any patterns. Here is an interesting analysis that popped up.

A clear pattern emerging across the consumer brand landscape is that brands are evolving from simply selling products into building what can best be described as participation systems. A participation system is a business model where the customer is no longer just a buyer at the end of a transaction, but an ongoing participant inside a broader ecosystem of experiences, identity, community, contribution, rewards, data, resale, events, content, or co-creation. This is seen repeatedly in the research and is an extension of experience marketing. Across the industry, brands are increasingly trying to create recurring engagement loops where customers contribute attention, creativity, identity, data, inventory, advocacy, or participation — not just dollars. This shift matters because participation systems create stronger retention, richer first-party data, higher switching costs, more resilient communities, and entirely new monetization layers beyond selling physical goods. In many ways, the product is becoming the entry point into an ongoing relationship system rather than the final outcome itself.

I added this to my playbook, which is here: https://t.co/MubosgZUuz

I’ve previously open sourced multiple tools around SEO, GEO and findability in the AI era. I am now releasing a fully working AI-native website publishing system to compliment that. This is not another website builder. The goal is to dramatically reduce complexity, cost, technical overhead, SEO dependency, plugin bloat, and even hosting costs while making websites maximally findable and usable by AI agents and AI search systems. The key insight: most people will not replace WordPress, Shopify, Wix, or existing websites — they will augment them with an AI-native layer optimized for AI discovery and machine readability. Even more interesting, local AI models like Codex and Claude already understand the builder and can help you modify and deploy your own site from simple Markdown content. I believe this is where publishing, findability, and business infrastructure are heading. Open sourced here: https://t.co/4NFjAultcF

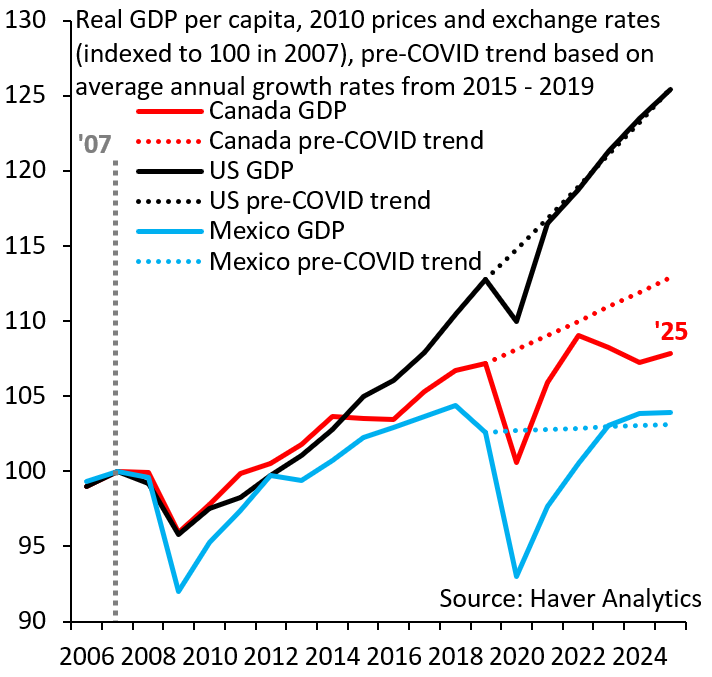

Canada and Mexico have stopped growing. Canada's real per capita GDP is flat since 2018, i.e. we're closing in on a decade of stagnation. Things look even worse for Mexico, which is in a near-permanent stagnation. There's a growth crisis in North America.

https://t.co/kLkd4FyS0B

The shift is happening. Health care has to change to lower costs and improve outcomes, and the only way that can happen is with AI. Hopefylly we can leverage AI in time before the system implodes under the weight of government debt, costs, regulations and our addiction to unhealthy food, which drives it all.

https://t.co/3TRBOooQUL