What Bloomberg Price Project (now covering 85% of the basket) is saying about May’s CPI. @tdurie95

Flagging:

-pickup in computer related goods (that memory chip and nand shortage)

-strong airfares

-accelerated inflation in sports equipment and major appliances (basically stuff that has high metal component—this may seem like tariffs pass through but is not)

And yet…

Core cpi close to the pace consistent with Fed’s 2% inflation target

How to square?

Weak recreation services inflation.

People are cutting back to gyms, clubs, streaming services, vets visits, dental visits….

SK Hynix to Raise Supplier Procurement Prices

SK Hynix, which posted record quarterly operating profit on the back of the high-bandwidth memory (HBM) boom, is reviewing plans to raise the prices it pays its suppliers. Expectations are growing for a so-called "trickle-down effect," in which the profits earned by large corporations flow through to their partners.

According to industry sources on the 10th, SK Hynix recently requested "price adjustment review materials" (documentation justifying price increases) from multiple equipment suppliers (tier-1 vendors) across the board. Some equipment makers are understood to have used this as grounds to request price increases in the range of 3–4%.

While price renegotiations do occasionally occur for materials and components with high cost volatility, extending this to equipment suppliers is seen as unusual. For materials companies, raw material costs (chemicals, gases, wafers, copper, etc.) account for a large share of the supply price (30–70%), and international commodity price movements can be tracked directly and clearly, making cost-linked pricing relatively easy to apply.

Equipment makers, by contrast, have cost structures dominated by fixed costs, development expenses, and technological capability, making it difficult to apply a simple "raw materials went up, so raise our price" logic. In fact, the norm is the opposite: the initial supply price is the highest, and roughly 10% is shaved off the supply price each time additional purchases are negotiated.

Tier-1 equipment vendor "Company A" is known to have recently supplied equipment to SK Hynix at higher prices than the previous year. Despite having had no price increases for the past five years or so, this year's negotiations went smoothly.

An equipment industry official said, "The recent semiconductor boom has been driven primarily by supply price increases stemming from the memory shortage, and apart from some new investments, materials/parts/equipment (sobujang) suppliers have seen no change in their prices — in some cases their profitability has actually deteriorated. On top of that, rising oil prices from the Iran war and the persistently weak won make price increases necessary."

The move by large corporations to raise equipment prices is interpreted as reflecting the fact that, amid the semiconductor supercycle, the delivery timelines and responsiveness of key equipment suppliers have an increasingly large impact on chip production plans.

SK Hynix set a new all-time quarterly record in Q1 this year with revenue of KRW 52.5 trillion, operating profit of KRW 37.6 trillion, and an operating margin of roughly 72%. Operating profit is forecast to grow sharply to the KRW 60–64 trillion level in Q2, compared with the seasonally weak Q1.

An SK Hynix official explained, "With raw material procurement burdens growing, supplier requests for price increases are on the rise. We will determine prices according to objective purchasing principles such as exchange rates and supply stability."

Some interpret the move as not unrelated to recent developments, including mounting political pressure on SK Hynix and Samsung Electronics to pursue "win-win cooperation" with their partners. The government has been ratcheting up the pressure, including reviewing plans to attract a Samsung Electronics semiconductor fab to the Honam region.

Over the last couple weeks, a hypothesis that I have come to feel more strongly about is this:

If market forces were allowed to run, the AI rally and boom will at least a couple it years the run.

The catalyst for a bust will come from a bipartisan political consensus to regulate AI in a form that smells like revenue sharing or something that has a whiff of nationalization.

The year would be 2028, when both Democrats and Republicans would try to outdo each other on who can come up with a stricter AI regulation proposal.

It took almost two decades for politicians to come to an agreement on the impact of the China shock.

The pace of convergence toward that bipartisan backlash for AI is happening much much faster.

Mythos invented its own language, then switched back to English to talk to humans

(AI safety researchers have been warning of this "Neuralese" risk for years. If AIs stop reasoning in English, we can't monitor their thoughts, which means we can't detect scheming.)

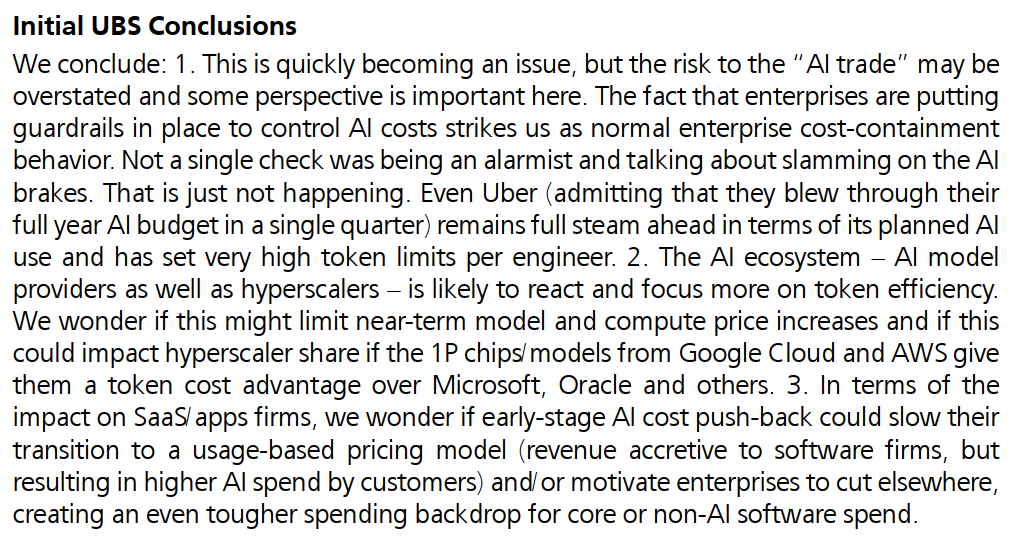

UBS has a long report out: "Token Costs – What Customers are Saying"

Companies are definitely feeling the higher bills, but the takeaway is that nobody’s actually slowing down AI use. They’re mostly just putting some guardrails in place and trimming spend in other areas while they keep rolling it out.

In conclusion, UBS saying Google Cloud and AWS could end up with a cost edge here because of their own chips and models. That might help them take some share from Microsoft and the others over time.

$GOOGL $AMZN $MSFT $ORCL

According to Al Jazeera, Iran’s deputy foreign minister has told them that they are not responsible for the downing of the AH-64 Apache helicopter earlier.

$ASTS yup. The market is completely asleep at the wheel not seeing TMobile is about to make a partnership with ASTS, especially after yesterday's video of SpaceX's CFO discussing going directly to the consumer and competing with MNOs, just weeks after TMobile joined ATT and Verizon in a proposed joint venture specifically for D2D connectivity. The signs couldn't be any clearer.

ASTS is on pace to have a monopoly with US MNOs, the most valuable mobile market in the world. Yet, Starlink has an implied market cap of $1T-$1.3T while ASTS is trading at $0.035T.

Yes, Starlink's implied market cap is heavily driven by their fixed broadband business, but the CFO said yesterday that connectivity's TAM is $1.6T a year or $0.740T a year for D2D/D2C.

There are only two dominant players in the D2D landscape: Starlink who is ultimately wanting to go directly to the consumer and will need low band spectrum to achieve that, and AST SpaceMobile who is working with MNOs. Effectively, a global duopoly is being made in a $740B TAM. Investors that want exposure can either pay $1T-$1.3T for Starlink Mobile or $35B for AST SpaceMobile.

It's really that simple.

*NFA

Not what you tend to see at the peaks. Again, doesn’t mean lows are in yet but you don’t see put volume spike to records at peaks, especially on the first pullback after a major breakout rally

$NQ_F The plan was to get long into the weekly EMA9, the only true first higher low after the incredible March breakouts. Coming into the first rejection target here.

Plan next: reject, revisit the low for acceptance, then make or break.

CPI coing - new plan before the bell.

BofA raises $NOK to €14.4 from €11, buy reiterated. The case: optical DCI leadership plus data center switch revenue building in H2.

I own $NOK and think it's the most interesting transformation to follow right now.

The advantage of $ASML not selling any high-NA tools is that capacity can be redirected towards selling much higher margin EUV tools. EPS will come in much higher than consensus is expecting. From JP Morgan: