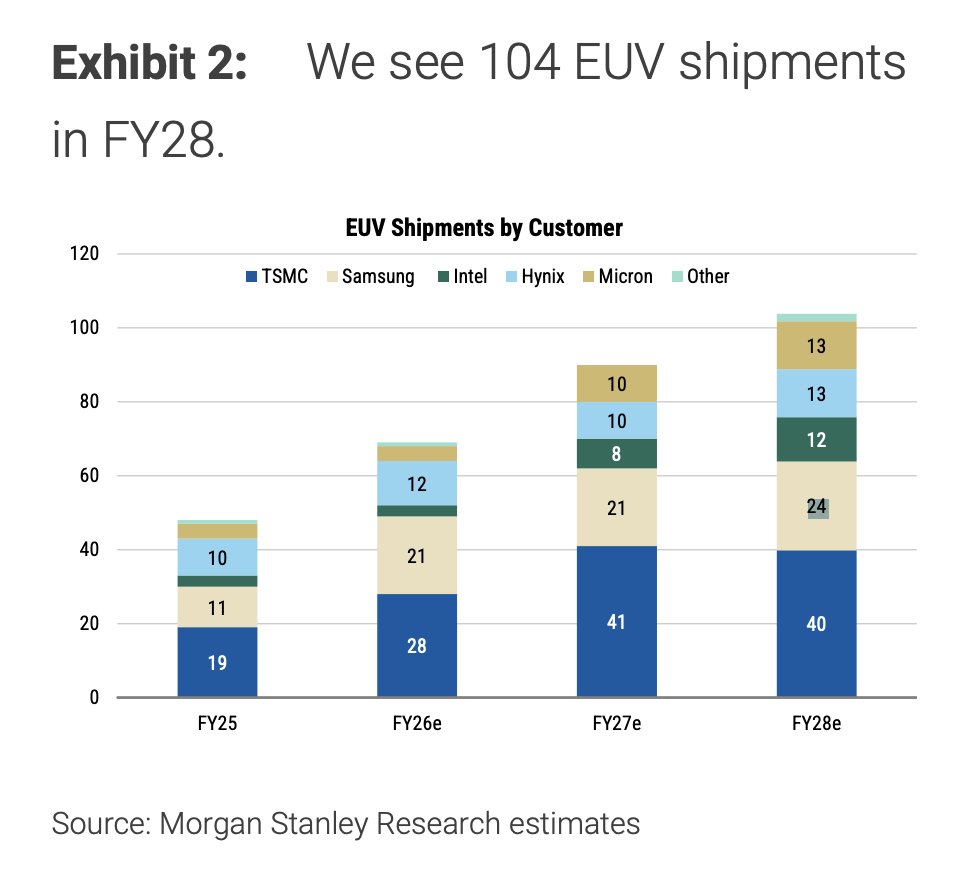

Both MSCO and JPM raising $ASML EUV ests today, '28 EUV units now at 104 and 105, respectively. Super bullish notes, upping ests and PTs, too. MSCO PT to €1,660 and JPM to €1,900 ($2,200)

JPM: "The Street is Behind the Curve: ‘27/’28 Numbers Need a Rewrite"

IBM shares jump as much as 15% in premarket trading after a video of President Donald Trump praising the company’s CEO and discussing the stock at a December event recirculated on social media over the weekend: BBG

Seaport analyst also not impressed with $NVDA keynote

"Nothing to write home about"

Summary: Nvidia had little new to offer at its Computex keynote. The headline event was the launch of their PC CPU line, but more noteworthy was their effort that future AI data centers would cost $80 billion per GW to build. As much as the company is executing at a solid pace, we see little to change their current trajectory.

F TIER KEYNOTEMAX: Jensen ComputeX presentation was one of the worst keynotes he has done. He announced nothing new on the AI datacenter side, and he only announced Windows on NVIDIA ARM CPU which the transition will not go work unlike Apple transition from x86 to M1 ARM.

The NVIDIA laptop chip is already delayed by 6 to 8 months from its original expected launch window. During development, the high-speed connection between the Nvidia and MediaTek parts caused so much interference that the video output was completely broken,

Laptop makers are reportedly being told definitely not let anyone turn them on or run benchmarks. That screams "immature hardware."

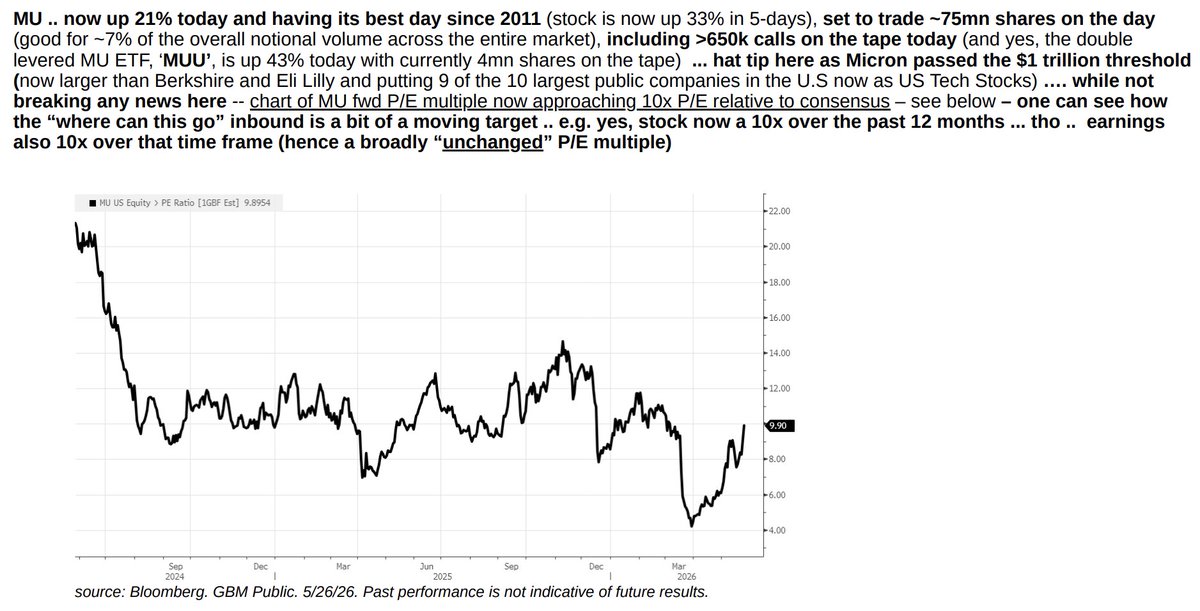

Hard to believe but some analysts are even raising a few concerns re $MU, while overall positive of course on the general developments in the sector. Raising $MU pt to $1100.

From Raymond James:

"We reiterate our Outperform rating on Micron and raise our price target to $1100 ahead of earnings later this month. Not surprisingly, in our recent travels, $MU has been among the most popular topics. While the share price and multiple continue to reach new highs, we note limited pushback among the investor base; there’s a general understanding that it really is “different this time.” Not only have all suppliers been more rational in capacity additions, the industry also has never seen a similar demand environment, with a significant (understatement of the year) investment being made by multiple customers at the same time."

Have to give props to Klein on $SMTC, great call yday, total fade and now trading down over 4%

“You make great money buying $SMTC on post earnings sell-offs, so keep that in mind”

$NVDA continues to be a funding short since earnings, from Cowen desk note:

"NVDA continues to trade squishy since negative T+1 reaction .. performance since May 15"

$NVDA continues to be a funding short since earnings, from Cowen desk note:

"NVDA continues to trade squishy since negative T+1 reaction .. performance since May 15"

Also, for the last 3 earnings, $NVDA has been sold off with stellar prints and guides, yday's event was great, but nothing spectacular in terms of expectations, might see some pressure again after running 40% into the print, and it has been a funding short name.

Barcs desk:

One doesn't have to agree with the analyst's controversial take here in $INTC $ALAB $SMTC, but if all three go from green to red on the opening bell, then you can't say there wasn't an oppy for a good trade, scoopy scoopy

Hearing Northland is downgrading $INTC:

Summary

Downgrading $INTC on valuation. INTC is making measurable progress in its turnaround, and we expect estimates to rise as demand for server CPUs picks up. However, we are modeling overall datacenter spending to decline in CY27 as hyperscalers become increasingly cash-strapped. Assuming INTC’s DC business grows by 40% in CY27, we get to an estimate of $3.20 and a P/E multiple of 38x the out-year. Even under this optimistic scenario, shares are expensive. We suspend our price target.

Hearing Northland is downgrading $INTC:

Summary

Downgrading $INTC on valuation. INTC is making measurable progress in its turnaround, and we expect estimates to rise as demand for server CPUs picks up. However, we are modeling overall datacenter spending to decline in CY27 as hyperscalers become increasingly cash-strapped. Assuming INTC’s DC business grows by 40% in CY27, we get to an estimate of $3.20 and a P/E multiple of 38x the out-year. Even under this optimistic scenario, shares are expensive. We suspend our price target.

Korean tech stocks going to get another leg higher. @DivesTech adding SK Hynix to his IVES AI 30 list.

"With this report, we are adding Datadog ($DDOG) and SK Hynix (000660.KS) to the IVES AI 30 list as core winners in the next phase of this AI Revolution with the memory super-cycle and AI observability themes front and center. We are removing Shopify ($SHOP) and Alibaba ($BABA) from the list."