Federal student loan eligibility is shifting from enrollment to outcomes.

via WSJ https://t.co/9sw1UR0fYZ

📅 Effective: July 1, 2026

🎓 Programs must show graduates earn:

• > High school graduates (BA & below)

• > Median bachelor’s earnings (master’s)

⏳ Measured 4 years after graduation

✅ Must pass 2 of 3 years

⚠️ ~3,200 programs (~690,000 borrowers) projected to fail.

💰 U.S. student debt: $1.7T.

https://t.co/tu8cXyOCQD

#nonprofit #college #studentloan #skills #productivity #University

https://t.co/0ilk3tFuws

The energy shock was cyclical for EU, but 𝐂𝐡𝐢𝐧𝐚’𝐬 𝐜𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐩𝐫𝐞𝐬𝐬𝐮𝐫𝐞 𝐢𝐬 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥.

Cheap Chinese exports, weaker Chinese demand, and persistent industrial overcapacity continue to weigh on Europe’s trade outlook. New trade deals help, but the eurozone still hasn’t found a clear path out of the dragon’s dungeon.

ht: TheEconomist WSJ EUCouncil CommerceGov #Tradewar

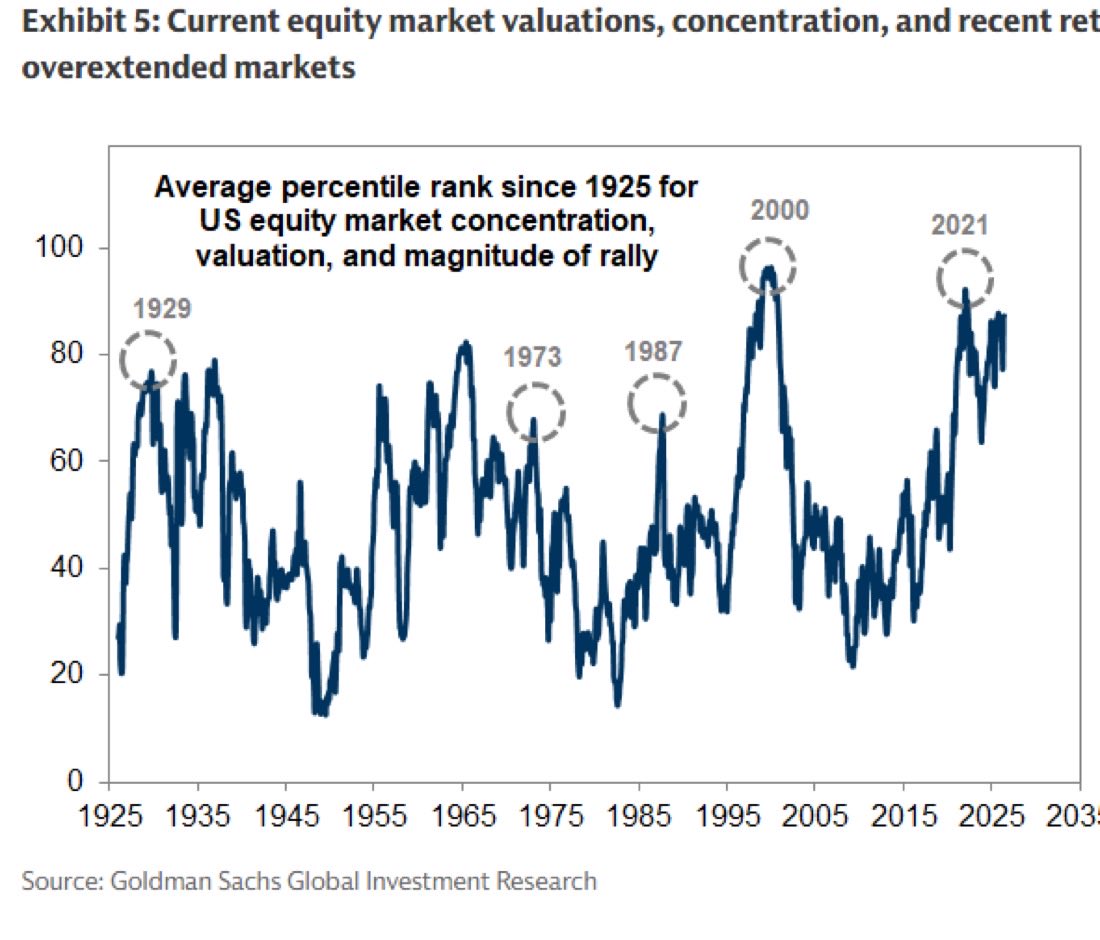

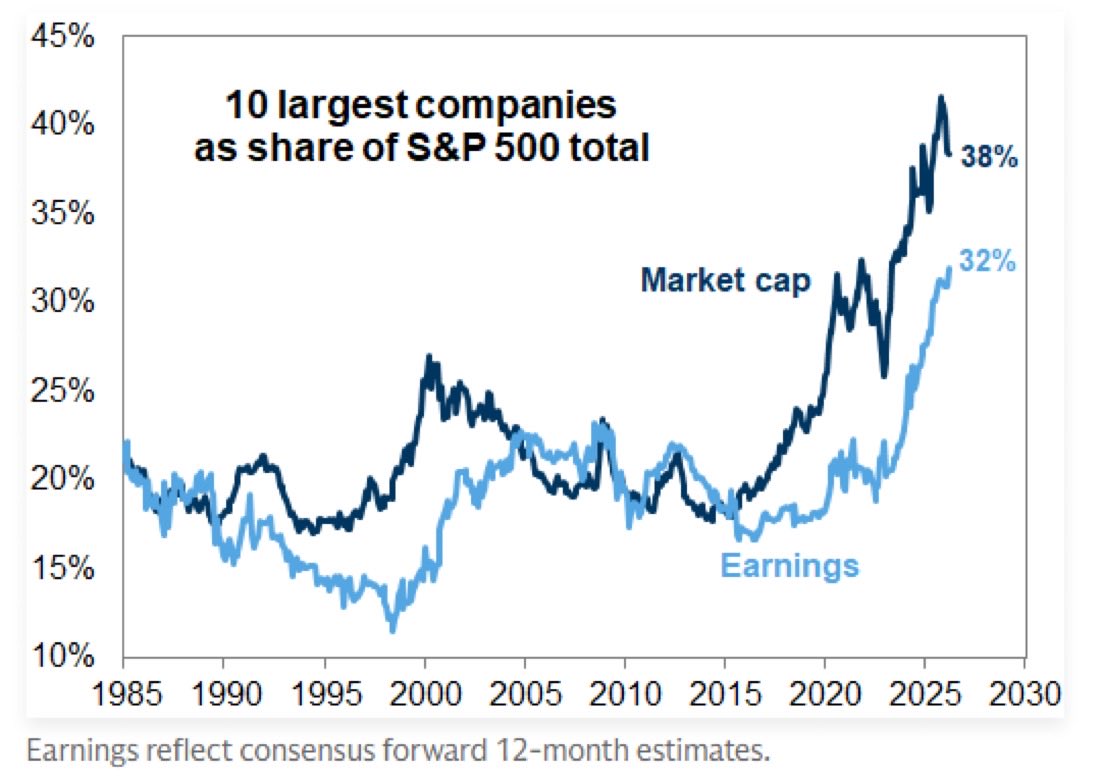

USA exceptionalism 🇺🇸

US GDP/cap sits ~2–3× major peers and the gap keeps widening; real GDP has out‑compounded Germany/UK/France for 200+ years; population scale inflected early and never converged; and even with China’s rise, the US still anchors ~35–40% of global defense spend with unmatched tech‑adjacent capability.

If the divergence isn’t cyclical, but structural, then what exactly is the mechanism that keeps reinforcing America’s long‑run outperformance?

ht:db/baml #investment #Vol #innovation #RiskManagement #Productivity

𝐅𝐞𝐝𝐞𝐫𝐚𝐥 𝐒𝐑𝐅 𝐜𝐚𝐩𝐚𝐜𝐢𝐭𝐲 𝐜𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 𝐢𝐧 𝐅𝐘𝟐𝟕 𝐬𝐢𝐠𝐧𝐚𝐥𝐬 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐭𝐢𝐠𝐡𝐭𝐞𝐧𝐢𝐧𝐠 𝐢𝐧 𝐥𝐨𝐰‑𝐜𝐨𝐬𝐭 𝐰𝐚𝐭𝐞𝐫‑𝐢𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐥𝐞𝐧𝐝𝐢𝐧𝐠. 𝐖𝐡𝐞𝐧 𝐰𝐢𝐥𝐥 𝐲𝐨𝐮 𝐬𝐞𝐞 𝐞𝐯𝐞𝐧 𝐡𝐢𝐠𝐡𝐞𝐫 𝐰𝐚𝐭𝐞𝐫 𝐛𝐢𝐥𝐥𝐬?

Federal water‑infra spend rolls over hard as IIJA sunsets: annual SRF support drops from ~$10B during 2022–26 (IIJA‑boosted) back toward ~$3B in FY27 per OMB’s proposed 90% cut. The $12B annual gap equals ~20% of EPA’s estimated need, tightening capital flexibility for muni and IOU systems already facing rising replacement cycles and inflation‑linked project costs. Smaller muni systems show highest exposure as low‑cost SRF loan supply retrenches.

#water #infraatructure #investment ht:MCO

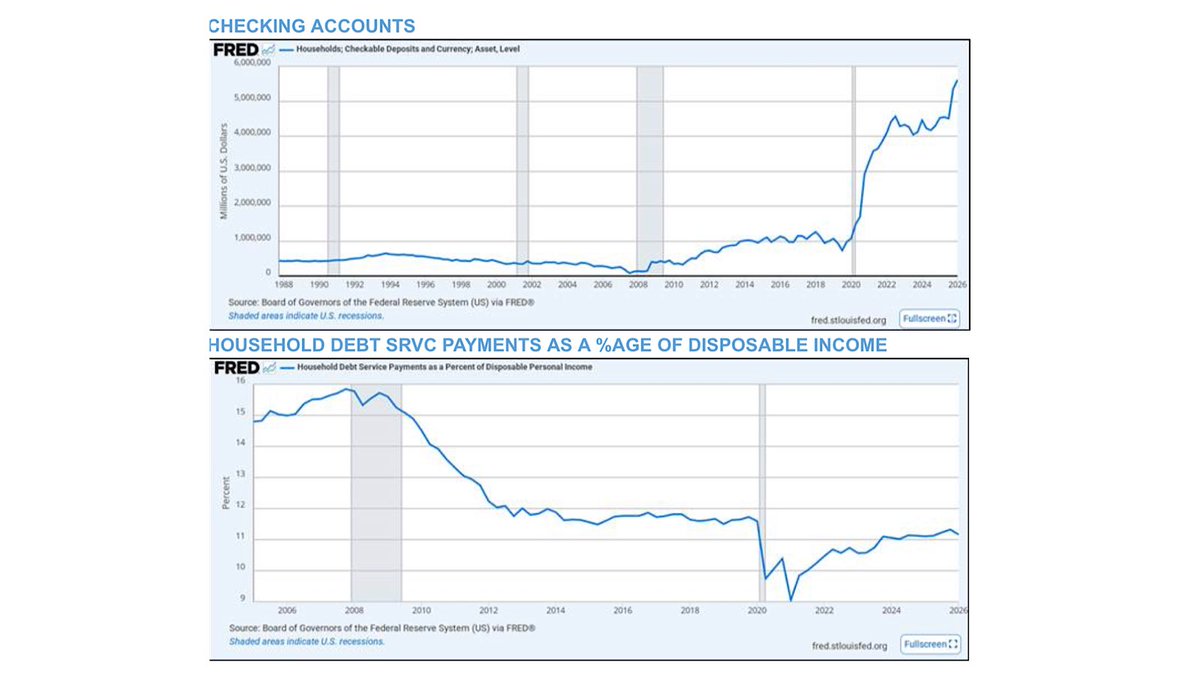

𝐏𝐮𝐛𝐥𝐢𝐜 𝐥𝐞𝐯𝐞𝐫𝐚𝐠𝐞 > 𝐩𝐫𝐢𝐯𝐚𝐭𝐞 𝐥𝐞𝐯𝐞𝐫𝐚𝐠𝐞.

Households de‑levered post‑GFC. Corporates re‑levered but stayed range‑bound. Uncle Sam absorbed the shock, and then kept going. Fiscal is now the balance‑sheet that does the work.

Risk Transfer

https://t.co/vjWN5P09NT

#consumer #debt #investment $

𝐔𝐭𝐢𝐥𝐢𝐭𝐢𝐞𝐬 𝐌&𝐀 𝐒𝐮𝐩𝐞𝐫𝐜𝐲𝐜𝐥𝐞 𝐃𝐞𝐞𝐩𝐞𝐧𝐬 𝐌𝐨𝐧𝐨𝐩𝐨𝐥𝐲 𝐏𝐨𝐰𝐞𝐫 𝐀𝐦𝐢𝐝 𝐀𝐈‑𝐃𝐫𝐢𝐯𝐞𝐧 𝐂𝐚𝐩𝐞𝐱 𝐒𝐮𝐫𝐠𝐞

Run by political bosses, the utilities M&A supercycle is making an already concentrated market even more monopolistic: $203.6B deals in 5mo ’26 (+40% vs all ’25). Data‑center capex $151.5B (2.2× YoY). Mega‑deals: NextEra–Dominion $112B, AES $33B. Utilities projecting 50–100% rev growth. Power costs +9% YoY → boom times for political‑lobbying consultants.

ht: FT #electricity #inflation #costofliving #mergers

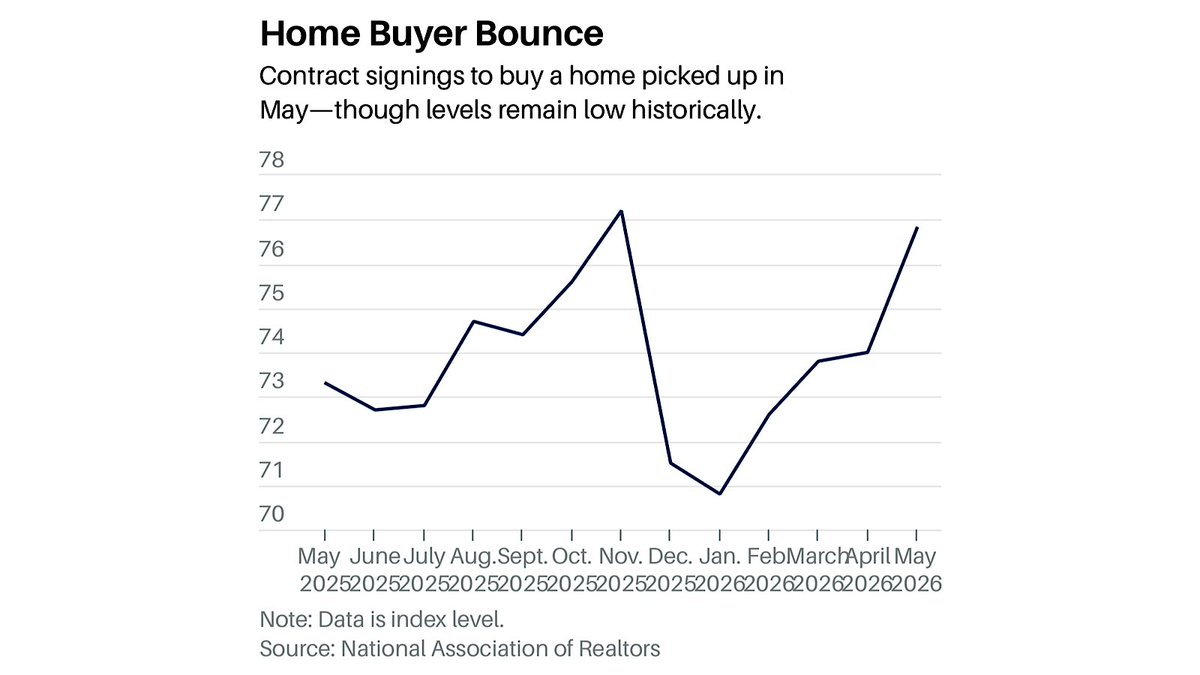

https://t.co/Qrsce9cMlX

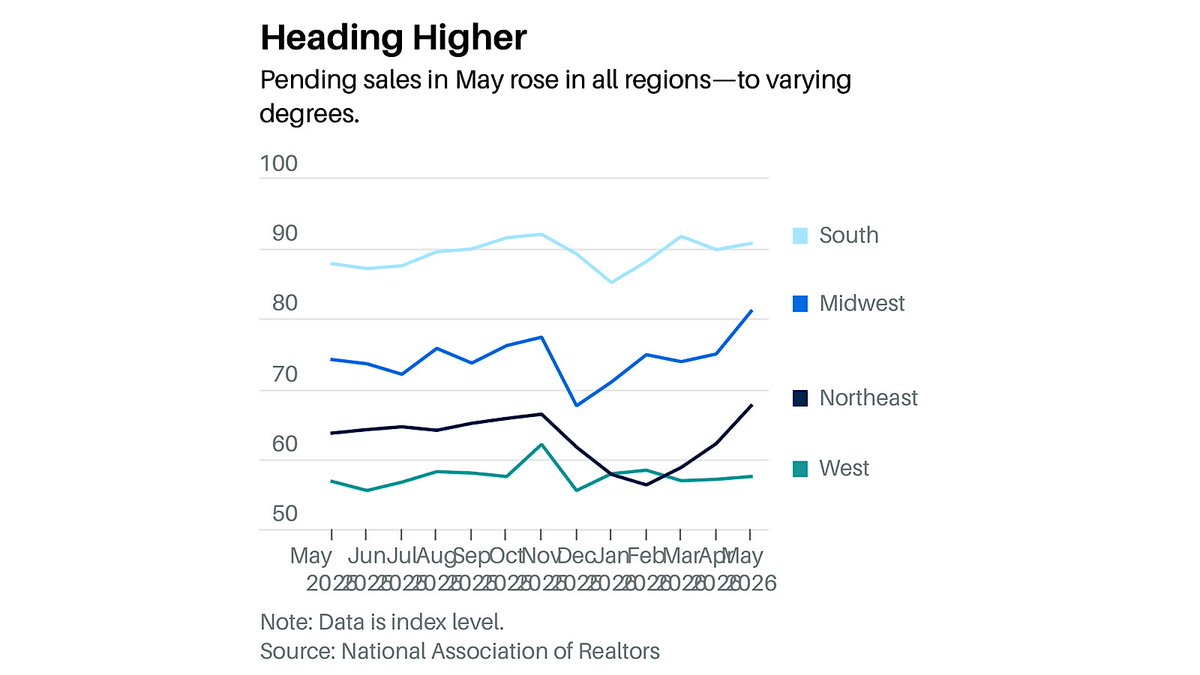

Short‑run: Case‑Shiller 20‑city up 0.9% YoY in April; buyer confidence rising (~⅓ vs 27% in 2025) even as high prices remain the top barrier. Pending sales and contract signings have bounced off winter lows, with 2026 activity running above 2025.

Long‑run: MBA’s demographic study signals a future supply overhang. 2025‑35 demand: 1.13M units/yr vs 12.6M expected construction.

Does the next decade’s housing demand really fall to about 802k units per year?

Net: ~23M units built vs ~19.4M needed. If builders don’t slow starts, and immigration stays status‑quo: supply > demand → national price pressure, softer household formation, and mortgage‑sector risk.

Chart @LoganMohtashami

https://t.co/sBAjWODllT

#RMBS #realtor #realestete #housing #cre

Major indices green with the Dow clearing 52k for the first time.

Semis revision breadth pressing historical ceilings; SOX maintains correlation with SIL’s lead. WTI breaks structural levels and screens oversold on RSI.

ht MarketWatch #materials#oott#energysecurity $sox #AI #investor #riskarb

Isn’t @kevinschaul’s point at WPO essentially this, that these AI tools are failing to present truly neutral representations of nuanced policy debates, on average?

Neutrality ≠ vagueness.

Neutrality ≠ corporate PR tone.

Neutrality ≠ “both-sides-ism” that avoids substance.

Neutrality is structured clarity. Buffett’s joke was about fake independence, boards filled with people who look neutral but have no real ability to challenge management. That’s not “cXo of nothing,” and it’s not the Buffett-style “independent director who has no qualifications except doesn’t burp.” It’s actual intellectual work.

Isn’t a lot of AI “neutrality” today just performative balance without any real analytical competence?

OpenAI AnthropicAI CNBC #AI #

✅ #Hospital margins keep ripping: YTD 8.3% in Apr‑26 vs 7.4% in Mar‑26 as rev +8% y/y > exp +7%; OP +8%, IP +5%, labor +4%, non‑labor +9%, with payer‑mix deterioration still the drag.

#healthcare#HealthInsurance ht:baml

https://t.co/ctov8gZTqk