Roth/MKM Initiates $OUST at Buy, PT $75

Analyst comments: "We believe Ouster is poised to outgrow the broader sensor market with advanced lidar and stereoscopic camera offerings that enable an AI-compute/software-based perception platform. We expect firm pricing and revenue growth driven by increased physical AI autonomy adoption to propel the company toward cash flow breakeven toward the end of CY27.

OUST is a unified sensing and perception platform vendor targeting emerging physical AI applications across mobility, industrial automation, visual inspection, smart infrastructure, and robotics. With a comprehensive product offering and capability, we expect the company to evolve into a physical AI solutions vendor that can adapt its offering based on customer needs. OUST’s market traction has the potential to proceed in a manner similar to a physical-AI-based solutions platform across manufacturing, smart infrastructure, and mobility."

Analyst: Suji Desilva

Last night, I attended @ousterlidar ‘s rev8 tech talk, their first notable public appearance since their $OUST SPAC IPO. Here are some things I learned:

1. Expect them to be more vocal about partnerships and new client wins, NDA/stealth mode is over. I suspect there also has been a change in the legal terms surrounding this disclosure with the rev8 iteration

2. Ouster has been learning a lot about working with the department of war to secure military contracts, since their BlueUAS approval. They have ongoing talks with Army, Navy, Airforce, etc, the sales team has been busy traveling, and obtaining security clearance and speaking the language is important.

3. Im incredibly bullish on their drone partnerships- I expect a proliferation of drones not just for surveillance, but increasingly for counterUAS (Argus) and increasingly in drone vs drone warfare. Recall that there are ethical complications for targeting people, but drone vs drone warfare is already here. $OUST is working with Anduril, Rheinmetall, and every country is already looking to see how they can deploy a combination of drones and humanoids to decrease human operators. The LTV of supporting a US marine is well in excess of $1M. Forget exoskeletons, save money and heartbreak with robots.

4. The developer community is growing and they have a nice GitHub resource center- they are willing to work with startups for full turn key solutions, and also agree to let the companies own the data, which is super important in some fields where there are privacy concerns. In other places, their entire SDK is open source and we should expect more communal data and premade onboarding tools to reduce the friction to “hello world”.

5. I continue to see their biggest bottleneck as the lack of qualified lidar engineer operators at the client level to handle larger Fortune 500 company deployments. This will ease over time as the sector and technology grows. The reason why ITS has been so successful is that there is an embedded group of nerds and engineers who work on behalf of the DoTs and can onboard and retrofit legacy camera solutions. This is massively profitable and I love the SaaS/r&m/long term sticky contracts with good margins.

6. Right now for retail/security usage, their customers are still learning about the technology and it’s about getting in front of the right people with the right narrative and vision, vs geeking out on hardware. Here I think rev8 makes the biggest difference, as native color is an emotional and foundational light switch in front of an investment committee. It’s easy for ppl to now see the vision of what Ouster can do.

7. A lot of speculation about insider sales, most notably from Mark Frichtl the CTO. He was absent at the event, which I found notable, but I maintain that the preplanned sales we now see from recent 144 filings from him, Cyrille and others represents a 2025 year where many long time insiders finally broke even and achieve some type of meaningful liquidity event. SF is not a cheap place to live!

8. The event was 1/3 ouster employees, some developers and prospects (I spoke to someone from $TMUS ) who has been talking to Ouster. Unfortunately I was probably one of 3-4 investors, so for what it’s worth the company is still in stealth mode from a capital markets visibility standpoint. Probably better that they don’t know how excited and bullish the retail community is on their story.

9. $HSAI and the Chinese competitors will remain in auto, where the multinationals have to play nice with China. Increasingly outside of auto, there is a bigger geopolitical push for secure supply chains and made in America. Compared to last year when more customers were in startup mode, I think as they achieve scale and think about volume $OUST is a no brainer. There is a reason why we haven’t seen $MVIS, $AEVA, or $INVZ will real sales volumes- you can’t trick people into buying an inferior lidar product!

10. Physical AI is here to stay. I’m LONG

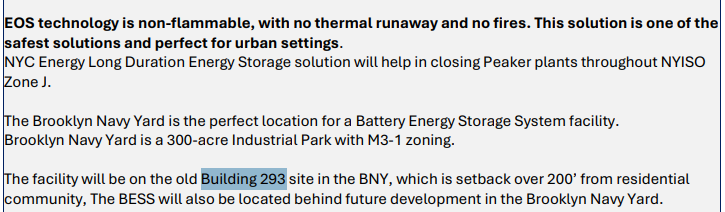

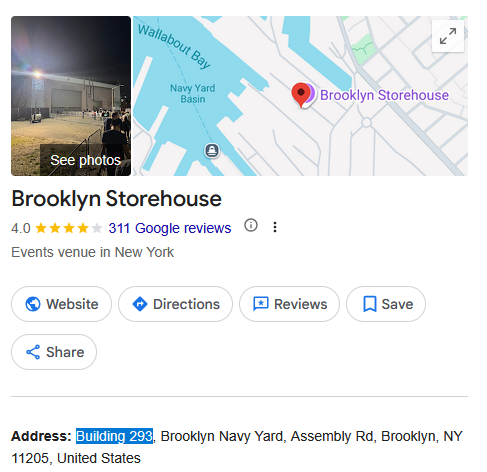

A massive win for $EOSE: The NYSERDA submission reveals a monumental 300MW/8hr (2.4GWh) zinc project at Brooklyn Navy Yard. Non-flammable zinc completely bypasses strict NYC lithium safety rules. A legendary urban validation & blockbuster revenue catalyst for Eos!

$OUST ARGUS Interception and Ouster Announce Strategic Agreement to Strengthen the Precision and Reliability of Counter-UAS Systems with Digital Lidar

(They will come - the partnerships - on a weekly basis now)

$OUST continues to establish itself as a key supplier for Physical AI.

Drones now, humanoid robotics next. Ouster’s lidar stack keeps showing up across autonomy, robotics, defense, and industrial AI applications - and this new ARGUS partnership is another step in that direction.

Just the beginning.

https://t.co/89NOAY4C7n

$OUST sometimes i can't help but laugh when I read "Ouster'll reach 100$ in 2030!"

It's like saying 2 years ago: Rocket Lab will reach 50$ in 2028!

Ouster at 400$ = 30B MC (if you assume a crazy 20% dilution!!)

I believe it will be way above 50B MC in 2030.

$OUST

I'm not a chart guy, but even to me this looks very sexy.

It reminds me of a certain space company I bought a couple of years ago that had a similar pattern, with a long consolidation phase before it started melting faces 👀

**OUST at 63x TTM sales (~$185M revenue) implies a ~$11.7B market cap, or roughly $183–184/share with ~63.7M shares outstanding.**

OUST deserves the higher multiple. It has ~9x AEVA’s revenue, 49% yoy growth, a much broader customer base (industrial/robotics/auto/defense), and a clearer path to profitability. AEVA’s valuation looks stretched on far smaller scale and execution risk.

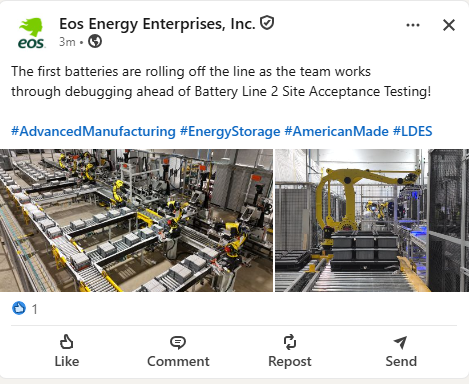

$EOSE for the price to move above 10$ and stay there, Joe just needs to do one thing: order line 2 (of the new building).

Thanks for your attention to this matter.