Weekly Earnings Brief #19 is out — $PD, and others.

$PD (Incident Response Software): Revenue up 1% YoY to $121M, but the real story is the cash machine: $41.2M free cash flow (34% margin), $444M cash, and a fresh $100M buyback at an EV/TTM FCF of 6.6x

Growth has flatlined, and net retention slipped to 97%. But new CEO + AI partnerships with Anthropic, Cursor, and LangChain look like a strategic reset. The bull case: PagerDuty becomes the orchestration layer for AI agents.

If you’d see value in a curated list of the most interesting smaller cap earnings reports, you’ll enjoy our weekly earnings recap briefings. Next one coming out tomorrow morning. We literally read hundreds of earnings press releases.

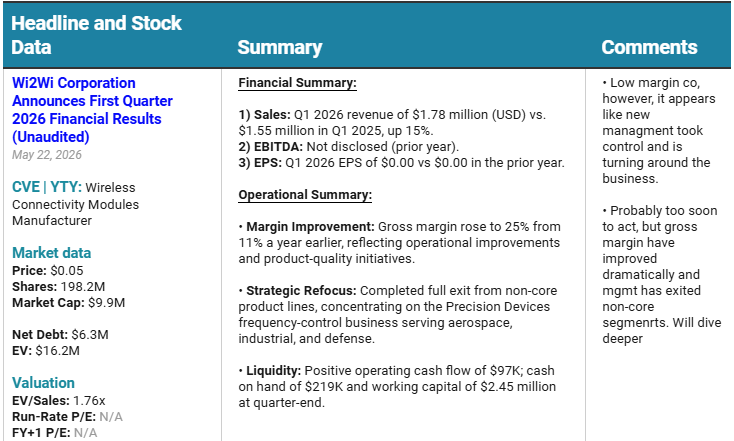

Weekly Earnings Brief #18 is out — $YTY.V, $TATT and others.

$YTY.V (Precision Frequency Control Devices) — Wi2Wi posted Q1 revenue up 15% YoY. Gross margin jumped from 11% to 25% as new management exited non-core product lines and focused on the precision devices business serving aerospace, industrial, and defense.

Q1 EBITDA of $122K and positive operating cash flow. Still early, but the turnaround signals are there: dramatic margin improvement, strategic refocus, and increasing defense exposure.

🔴 LIVE THIS THURSDAY (May 28)

- 10 small-cap picks in one session, 5 from @majgeoinvesting, 5 from @SebKrog

- Live on Substack. Open to everyone. Tickers named on stream.

🕐 Thursday, 12:30 PM ET

📍 Substack Live

Set a reminder 👇

🔴 LIVE THIS THURSDAY (May 28)

- 10 small-cap picks in one session, 5 from @majgeoinvesting, 5 from @SebKrog

- Live on Substack. Open to everyone. Tickers named on stream.

🕐 Thursday, 12:30 PM ET

📍 Substack Live

Set a reminder 👇

Weekly Earnings Brief #18 is out — $YTY.V, $TATT and others.

$YTY.V (Precision Frequency Control Devices) — Wi2Wi posted Q1 revenue up 15% YoY. Gross margin jumped from 11% to 25% as new management exited non-core product lines and focused on the precision devices business serving aerospace, industrial, and defense.

Q1 EBITDA of $122K and positive operating cash flow. Still early, but the turnaround signals are there: dramatic margin improvement, strategic refocus, and increasing defense exposure.

✅Peter Lynch popularizó el concepto de los “baggers”:

compañías capaces de multiplicarse varias veces desde el precio de compra inicial.

El problema es que los grandes baggers rara vez aparecen en las compañías más seguidas del mercado.

Suelen aparecer en small caps poco conocidas, fuera del consenso y con catalizadores reales.

Durante los últimos dos años, compañías presentes en Equity Small Caps FI como:

Anterix, PaySign, Helios Towers, Vox Royalty, LandBridge, Amerigo Resources, Andean Precious Metals, Tasmea, Talkspace, REV Group, AltynGold, Dundee Precious Metals, Hanza o ISS

han llegado a subir más de un +100% desde niveles de entrada del fondo.

Algunas de ellas ya no forman parte de la cartera tras materializar gran parte del valor.

Otras siguen actualmente en cartera.

Muchas eran prácticamente desconocidas para la mayoría del mercado hace pocos meses o años.

Porque para encontrar baggers primero hay que atreverse a mirar donde casi nadie mira.

Precisamente ese es el enfoque de Equity Small Caps FI.

Informe completo en Rankia:

https://t.co/hMMjCNA3WW

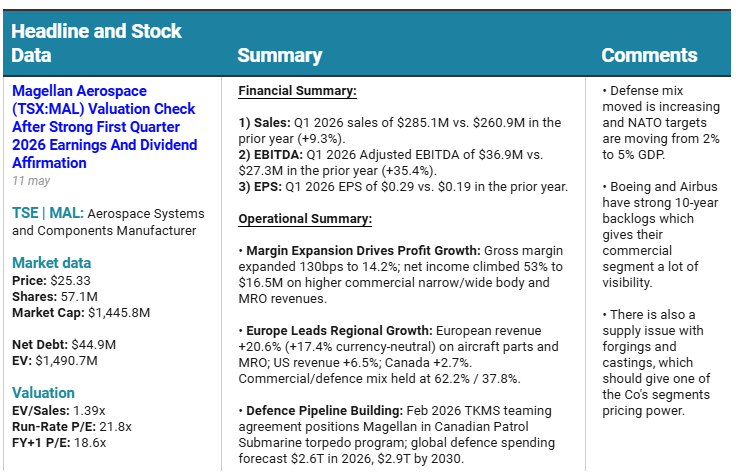

Weekly Earnings Brief #17 was published yesterday, featuringuring $MAL.TO, $FENC and others.

$MAL.TO (Aerospace Systems & Components): Magellan posted Q1 revenue up 9.3% YoY to 285M. Gross margin expanded 130bps to 14.2%, net income climbed 53% to 16.5M.

Defence mix is increasing as NATO targets move from 2% to 5% GDP. Boeing and Airbus have 10-year backlogs, giving the commercial segment strong visibility. Feb 2026 TKMS teaming agreement positions Magellan in Canada's Patrol Submarine torpedo program.

Global defence spending forecast: $2.6T in 2026, $2.9T by 2030.

@EPSMonitor $SIF Q1 earnings were completely under appreciated

• Aerospace theme with program funding accelerating

• Inflects to profitability after yrs of losses

• Aggressive backlog growth as sales grow

• Crazy operating leverage at the gross margin / OPEX level

• Run-Rate P/E = 10x

@Cyril955 Was definitely an interesting quarter. $KLYG had a one time revenue bump in the quarter, but the quarter shows what could happen if revenue takes a consistent step forward…

What's your favorite 🇺🇸🇨🇦Q1 2026 earnings report… so far, with shares under $60M, and profitable?

Tell us why in 5 bullets or less.

We’ll share and archive the results.

Please RT and like so we can get the idea flow going 🎉

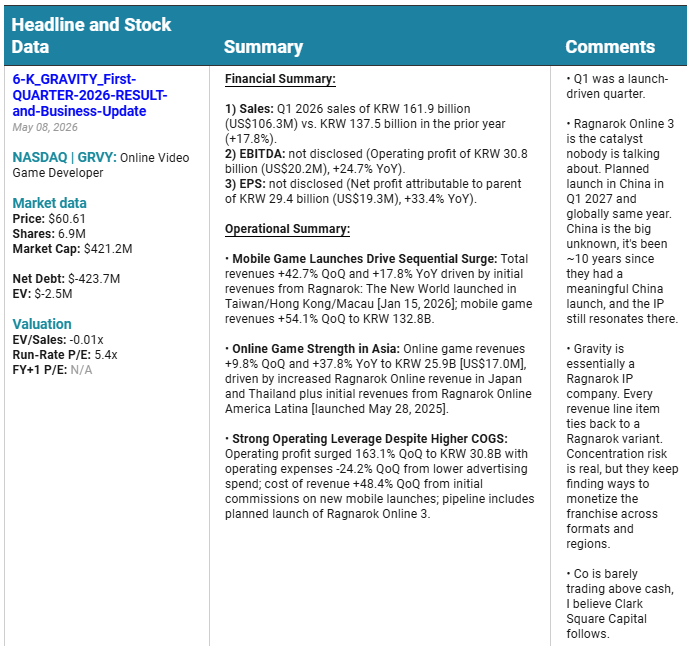

Weekly Earnings Brief #16 was published yesterday: $GRVY, $ACX.TO and others.

$GRVY Gravity (Online Video Game Developer) posted Q1 revenue up 42.7% QoQ and 17.8% YoY to KRW 161.9B ($106M). Operating profit surged 163% QoQ. Net profit up 33.4% YoY.

Ragnarok Online 3, planned for China launch in Q1 2027 and globally within 2027. It's been ~10 years since the IP had a meaningful China launch, and it still resonates there.

Stock is barely trading above cash, net cash of US$393M vs market cap of US$444M.

$ACFN Q1 2026 results were lackluster, and Q2 2026 will probably be a down quarter.

However, the AIO partnership is looking increasingly interesting. In the 10Q we got some interesting information about the software revenue split:

"The applicable share is initially 50%, and is reduced to 43% once cumulative amounts paid to AIO under this provision exceed $2.0 million, and further reduced to 34% once cumulative amounts paid exceed $4.0 million. Amounts due are to be calculated and remitted on a quarterly basis."

$ACFN Q1 2026 results were lackluster, and Q2 2026 will probably be a down quarter.

However, the AIO partnership is looking increasingly interesting. In the 10Q we got some interesting information about the software revenue split:

"The applicable share is initially 50%, and is reduced to 43% once cumulative amounts paid to AIO under this provision exceed $2.0 million, and further reduced to 34% once cumulative amounts paid exceed $4.0 million. Amounts due are to be calculated and remitted on a quarterly basis."