@cz_binance@heyibinance

As ecosystem pioneers, Binance should a set an example and prevent PnDs, by disabling funding rate on suspect tokens. Funding rate is based on relationship between spot and perp price > having a super majority control of available tiny float > easy to manipulate funding to manufacture short squeezes > preventing natural price discovery based on fundamentals. Look to $RIVER as an example. Same thing is happening to $LAB

https://t.co/R1TN04Iny2

1/ An investigation into the opaque private loans/OTC, unilateral vesting changes, market maker coordination, unknown float, and >95% supply control behind $LAB's recent pump to $6B FDV.

Here's why @LABtrade_ represents everything wrong with the current meta of retail extraction on major centralized exchanges.

CLOBs are not going to take us to the RWA promised land.

Today Hyperliquid owns the liquidity for a handful of RWA macro names. But outside the top 10 traded assets (which are ~90% of volume) liquidity falls off a cliff. When there's enough retail demand, order books can work. But "perps on everything" is a different problem, and TradFi solved it decades ago.

The answer isn't every venue rebuilding its own order book. That's not what Robinhood does, it's not what Schwab does, and it's not what DeFi should be doing either.

Building your own book for every asset means bootstrapping demand ticker by ticker, renting liquidity with subsidies, and ending up with thin markets that blow out 200x the moment news hits. It's like sucking the ocean of TradFi liquidity through a straw.

Variational skips all of it via the RFQ model. RFQ is how institutions like Dragonfly actually trade. In RFQ, dealers quote just-in-time and hedge on the primary venue as orders come in. This lets Variational mainline TradFi liquidity directly and mirror it on-chain. Margin in smart contracts, settlement in stablecoins, liquidity aggregated from the people who already trade on the biggest underlying markets, like the CME and NYSE.

It makes it permissionless to access the same depth and spreads the big boys get. With the cold start problem gone, new markets can ship at the speed of software.

By next year I expect RWA perps to be the biggest contract class on-chain, bigger than BTC and ETH perps combined. That's how crypto truly becomes the market for everything.

I believe the platform that wins that won't look like a traditional exchange.

Proud to lead Variational's $50M Series A.

Watch this space.

I respectfully disagree. Tokenized U.S. stocks will likely follow many of the same regulatory requirements as traditional brokerages. When you look at the largest yield-generating cryptocurrencies by market cap - USDT, USDC, ETH, and SOL come to mind. ETH and SOL generate yield because of staking. With tokenized stocks, I do not see staking, at least in the traditional sense, as a viable option.

USDT and USDC are able to generate ~3-4% APR for end users because they are backed by U.S. Treasuries. In most cases, for users to gain exposure to that yield, they generally must deposit into a DeFi protocol or a CEX earn program. AFAIK, Coinbase is the only major entity that allows users to simultaneously earn yield on USDC while still being able to freely trade it.

I only see meaningful yield for tokenized U.S. stocks coming from borrowing demand, with shorting being a major driver of that demand.

Undoubtedly, if tokenized U.S. stocks begin trading on blockchains, perpetual futures contracts will follow for a couple of reasons:

1. Since tokenized U.S. stocks will likely be more heavily regulated, most exchanges won't be able to offer spot trading. Perpetual futures, as always, will likely face fewer restrictions while also allowing higher leverage.

2. Perpetuals generate the most trading volume, and exchanges, ultimately, are profit-driven businesses.

As we saw with BTC lending APRs, the creation and maturation of perpetual futures significantly reduced its borrowing demand. I believe the same dynamic will eventually apply to tokenized equities as well.

On the bright side, I do agree that tokenized U.S. equities will bring significantly more liquidity into the blockchain ecosystem. A rising tide lifts all boats.

@cuntycakes123 Saw an excel ss, seed got in at 0.0035, 300x and pre-seed in at 0.00035 3000x. The funding in perps and OTC deals align with those numbers.

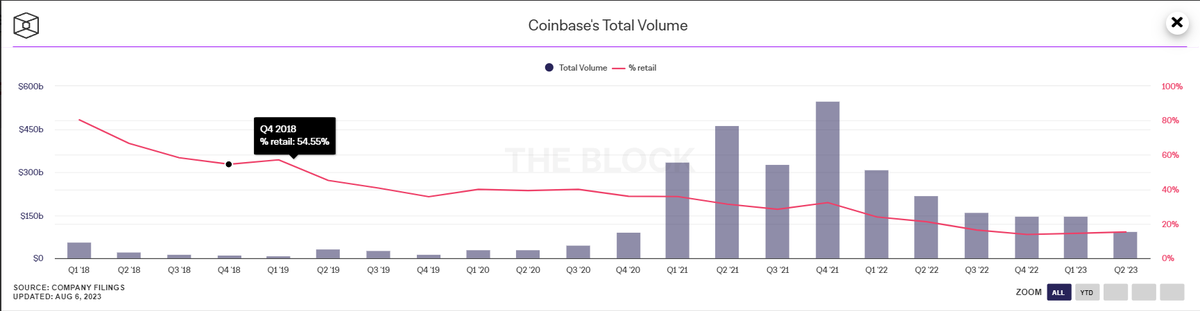

@RhoRider@El_Nicaman Using CB as it's #1 US by volume. Overall volume up a lot; q2 23 (93B) alone almost had as much as whole 2018 (100B). % retail is on decline.

@thebtcpainter@WatcherGuru I think majority of users who will use third party custodians will be very wealthy individuals or institutions for whom self-custody is more of a risk; regular CT plebs, self-custody is the norm

@noblemillions I can totally relate. Got liquidated for large % of NW because I neglected my physical and mental health. Stepping away to regroup thought and body definitely helped. Made back everything. Also got hit by FTX rug really bad so not much trading rn but that’s another story.