🔥 Collecting on $GOOGL while holding LEAPS with PMCC

💥 04/07: LONG 5x Dec '26 $100 Calls @ $56.50 = $28,253

💰 05/05: SOLD 5x May 16 '25 $175 Calls @ $0.50 = +$246.65

🧼 05/16: CLOSED the short for $0.02

📌 Net premium banked 💸

📌 Core LEAPS now up +44%

📌 No assignment risk

📌 Theta did the work 😎

🧠 This is how you rent your calls while holding conviction.

Stack time (theta). Stack edge. Let the market pay you.

Three weeks ago I put together a full breakdown on $HON at $213.

It's $237 today. The thesis is playing out

.

What's changed since May 10:

- HON went from $213 → $237.86 — up 11.7% in 21 days

- June 29 spin date officially confirmed by Honeywell on Q1 earnings call.

- HON also announced the sale of its Warehouse and Workflow Solutions business to American Industrial Partners — additional portfolio cleanup not in the original article.

- June 3 Investor Day is in 3 days

- The chart shows HON back above the 200-day MA, momentum indicators all turning positive, and heavy volume accumulation in the $235–240 zone

Our base case was $266. Stock still has 12% to get there even after today's move. This is old school digging but it pays if you can tolerate thinking in years instead of days.

Full original report: https://t.co/Z5LWJAbZsh

$HON $HONA $GE $GEV -

Closed the $GOOGL Dec 18, 2026 $100/$290 call vertical.

Position:

+5 $100 calls

-5 $290 calls

Closing Date: 5-12-26

Sold $100 calls at $289.61

Bought back $290 calls at $112.18

Net spread exit: $177.43

Total proceeds: $88,705.35

Max possible value at expiration was $95,000, so this captured about 93.4% of max spread value.

There was only about $6,295 left to squeeze out, with the upside capped and a lot of capital tied up.

If I had managed the $290 calls better in March I may have been able work the trade for a little bit longer. However, this one did its job. Lock the win, free the capital, and look for the next asymmetric setup. Hard not to do something right with this kind of movement in a stock.

🔥 Collecting on $GOOGL while holding LEAPS with PMCC

💥 04/07: LONG 5x Dec '26 $100 Calls @ $56.50 = $28,253

💰 05/05: SOLD 5x May 16 '25 $175 Calls @ $0.50 = +$246.65

🧼 05/16: CLOSED the short for $0.02

📌 Net premium banked 💸

📌 Core LEAPS now up +44%

📌 No assignment risk

📌 Theta did the work 😎

🧠 This is how you rent your calls while holding conviction.

Stack time (theta). Stack edge. Let the market pay you.

UPDATE 09/03 — LEAPS/Rolling a 2 DTE position after Google blasted through our strikes.

📈 Core: 5× $GOOGL Dec ’26 $100C

• Day’s gain: +$9,550

• Total LEAPS gain: +$39,796.67

💵 Option “rent” Selling Covered Call (net, after fees): $3,729.93

➡️ Income-only ROC: 13.2% on $28,253.33

📊 Total ROIC (mark-to-market):

$39,796.67 (LEAPS) + $3,729.93 (income) = $43,526.60

➡️ +154.1% on initial $28,253.33 Since April 7th

Now short OCT17 $230 ITM Calls

Own great companies at value, let LEAPS run, collect and manage premium. 📬

$SPY $SPX $QQQ

$HON is trading at a 22% discount to what its parts are worth separately.

The spinoff is June 29. Two Investor Days before that — June 3 and June 11 — are when the discount starts closing.

Bear case sum-of-parts: $226. Base case: $266. Current price: $213.

The catch nobody is talking about: HONA launches with $16B in debt. That's why it's not a straight GE Vernova replay.

Full breakdown — multiples, management, buy now vs. wait for the dip: https://t.co/Z5LWJAcxhP

$HON $HONA $GE $GEV $SOLS

$CEG Put Ratio Spread — High ROC, Short Duration

+3x 285P

-3x 282.5P

-3x 280P

Exp: May 8 (9 DTE)

Net Credit: ~$855

Capital Required: $9,127

📊 Metrics

ROC: 9.37% (9 DTE)

Annualized: ~380%

PoP: ~85%+

Theta: +$100/day

📈 The Setup

$CEG ~305

All strikes stacked below price →

theta working immediately

Max Profit Zone:

👉 $1,605 between 280–282.5 at expiration

🧠 Why I Like It

• Elevated IV → rich premium

• Tight short strikes → accelerated decay

• Credit upfront → reduces cost basis

This is a premium harvest trade, not a prediction.

⚙️ Plan

Above 285:

→ Let it decay

→ Take profits early (50–80% maybe)

282.5–285:

→ Still profitable

→ Manage deltas / scale out

Below 280:

→ Roll down & out for credit

→ Re-center

⚠️ Risk

• Tail risk below 280

• Needs management if tested

💡 Summary

Short duration

Defined income window

Multiple ways to win

“When close counts.” 🎯

$NBIS trade closed ✅

The 5/1/26 1x2 put ratio spread expired for full credit.

Original position:

+3 94P

-6 90P

Only opened 1/2 size because I wanted room to add if NBIS pulled back further.

Original credit: $675

Capital required: $3,442

Final credit captured: 100%

Final ROC: 19.61%

Annualized ROC: 216.9%

Max profit on the structure was $1,875 if NBIS finished near $90, but the stock stayed strong enough that the puts expired worthless and the credit became the profit.

This is why I like the 1x2 put ratio spread:

It gives me a wide profit zone, positive theta, room to be wrong, and the chance to scale in if the stock pulls back.

Didn’t need the second half this time.

Base hit. Full credit. On to the next one.

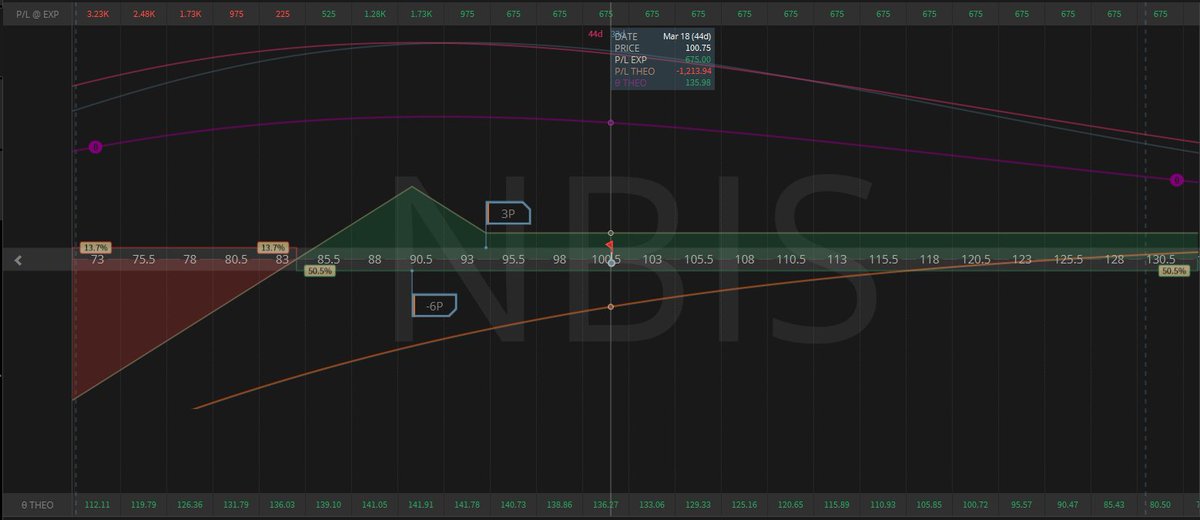

$NBIS Opened a 1x2 put ratio spread for 5/1/26 (33 DTE): Only placed 1/2 of the position - place the other 1/2 if the opportunity is given on further pullback.

+3 94P

-6 90P

Stock: 100.75

Stats:

• Net credit: $675

• Capital required: $3,442

• ROC: 19.61%

• Annualized ROC: 216.9%

• Max profit: $1,875

• Max profit at: 90

• Breakeven: 83.75

• Net theta: +$42.96/day

This one has much better capital efficiency and a lot more juice than $AAPL, but it’s also the more aggressive trade and needs quicker management if price starts moving closer to the short strike.

Management plan:

• Above 94: let theta work

• If $NBIS drops into 93–91: start getting proactive

• I’d look to take off the 94/90 debit spread portion around $3.20 to $3.80

• Then manage the extra short 90s by rolling out/down for credit

• If needed, buy lower puts and turn it into a fly / broken wing fly. Look to add the second 1/2 of the position.

Higher return profile than the $AAPL setup, but definitely the one that can get hot faster if the tape weakens.

$NBIS update on my 5/1/26 1x2 put ratio spread

Position:

+3 94P

-6 90P

Stock: 144.89

DTE: 20

Current stats:

• Open P/L: +$570

• Original credit: $675

• Cost to close: about $105

• Credit captured: 84.4%

• Capital required: $3,442

• ROC so far: 16.6%

• Annualized ROC so far: 335.8%

• Net theta: +$14.19/day

• Net delta: +6

• Max profit: $1,875 at 90

• Breakeven: 83.75

$NBIS absolutely ripped higher and this ratio spread is now mostly a decay trade. Based on the current gain versus capital required and 18 days open, the annualized ROC is about 335.8%.

The short 90s are way OTM now, so the pressure has come way off this position.

Management plan:

• Above 94: let theta finish the job

• With only about $105 left to close, this is getting into don’t-overstay-it territory

• If price stays strong, I can let more premium come out

• If I want to clean up risk early, this is close to a very manageable exit

This one had more juice from the start, and now the move higher is doing exactly what I wanted.

$AAPL trade closed the best way possible — expired for full credit ✅

5/1/26 1x2 put ratio spread:

+4 230P

-8 225P

Original credit: $632

Final cost to close: $0

Credit captured: 100%

Capital required: $11,240

Final ROC: 5.62%

Annualized ROC from the 20 DTE update: ~102.6%

Stock stayed well above the 225 short puts, time did the work, and the ratio spread paid exactly how it was designed.

Patient trade. Defined plan. Full credit.

$AAPL 1x2 put ratio spread for 5/1/26 (33 DTE):

(In the red at the moment so it may require management) This is 1/2 of a full position. If management is needed then we will add the other 1/2 as part of the management process.

+4 230P

-8 225P

Stock: 248.67

Stats:

• Net credit: $632

• Capital required: $11,240

• ROC: 5.62%

• Annualized ROC: 62.2%

• Max profit: $2,632 (Only happens if the Shout Put is pegged at expiration)

• Max profit at: 225

• Breakeven: 218.42

• Net theta: +$43.71/day

Solid cushion, positive theta, and a much more textbook setup for how I like to run put ratio spreads.

Management plan:

• Above 230: let theta work

• If $AAPL drops into 228–226: watch the 230/225 vertical closely

• I’d look to take off the debit spread portion around $4.00 to $4.75

• After that, manage the extra short 225s by rolling out/down for credit

• If needed, convert the remaining risk into a fly / broken wing fly or add to the position and or look to take the stock.

Good managed trade. Not something I want to babysit into expiration if price starts pressing 225 fast.

$AAPL update on my 5/1/26 1x2 put ratio spread

Position:

+4 230P

-8 225P

Stock: 260.38

DTE: 20

Current stats:

• Open P/L: +$476

• Original credit: $632

• Cost to close: about $156

• Credit captured: 75.3%

• Capital required: $11,240

• ROC so far: 4.23%

• Annualized ROC so far: 85.9%

• Net theta: +$21.81/day

• Net delta: +14

• Max profit: $2,632 at 225

• Breakeven: 218.42

This trade keeps improving. Based on the current gain versus capital required and 18 days open, the annualized ROC is about 85.9%.

$AAPL is well above both strikes, the short 225s are safely OTM, and now this is mostly a time-decay trade.

Management plan:

• Above 230: keep letting theta work

• If I can keep shrinking the close cost, I’ll stay patient

• If $AAPL falls back into 228–226, I’ll start watching the 230/225 vertical again

• Then I can peel the debit spread portion and manage the extra short 225s from there

This is what I want from a put ratio spread: cushion, decay, and less stress as time/premium comes off.

$SOLS update

Still acting well.

After building a base in the high 40s / low 50s, $SOLS made a strong trend move and is now pushing into the next overhead zone around 82–84.

What I’m watching now:

• 79–80 = first key area to hold

• 83–84 = near-term resistance / supply

• Above that, 87–88 opens up

• If it loses 79, I’d watch 76, then 72–73

The bigger picture still looks constructive:

higher lows, reclaim of the moving averages, and price pushing back toward the upper end of the volume profile.

Momentum has improved a lot, but it’s also getting more extended here, so I’d rather see consolidation or a clean hold of support than chase a vertical move.

Trend is still up.

Now it’s about whether $SOLS can turn this 79–80 area into support and build for the next leg. If there is a next leg. The idea for $SOLS was an AI Picks and Shovels play based on their products for liquid cooling in data centers.

SIDE NOTE: I started tracking the spinoff in April of 25. Tracking spinoffs is an old-school strategy that may not be all that glamours but it pays. I like tech and theme plays. $GEV PAID.

There is usually a small time when the new company bottoms and the asset managers reduce or adjust their holdings to realign their funds focus. I guess I could have bought $IREN at $6 but I may not be that smart.

💎 $SOLS (Solstice Advanced Materials) spun off from Honeywell ($HON). Most investors ignore spinoffs because they feel "old school" or boring.

Can anyone think of something that needs to run cooler and if noise cancelation was a by product it would be a huge plus?

$WULF covered call update

Position:

+10 Dec 17, 2027 4C

-10 May 1, 2026 20C

Stock: 18.90

Short call DTE: 20

Current stats:

• Net position open P/L: +$8,110

• LEAPS open P/L: +$8,550

• Short call open P/L: -$440

• Short call premium sold: $800

• Current short call value: about $1,240

• Net theta: +$37.99/day

• Net delta: +521

• Campaign ROC so far: 131.9%

• Annualized campaign ROC: 207.5%

$WULF has moved up hard, which is great for the LEAPS, but now the short 20C is starting to matter with the stock getting closer to the strike. Using the approximate net debit basis of $6,150 for the diagonal campaign, the annualized ROC is about 207.5%.

Management plan:

• Below 20: let theta work, but keep a close eye on it

• If $WULF keeps pressing through 20, I’ll decide whether to roll up and out for more credit

• If I still want more upside exposure, I’ll be more aggressive about rolling

• If I’m fine getting tighter on upside, I can let the short call do more of its job.

The LEAPS are doing the heavy lifting here. Now it’s about managing the short call without giving away too much upside. The only real downside is the option spreads are not as favorable as I would like.

$WULF is coiling. 🌪️

Technical: Price is compressing in a tight range ($12.50–$14.50) while volume dries up. This is textbook consolidation behavior. SMA is holding as the floor. The energy is building for a move back to $17+.

Fundamental: While the chart resets, the thesis gets stronger: 1️⃣ Nuclear Moat: Access to 24/7 zero-carbon power is the #1 bottleneck for AI. WULF has it. 2️⃣ The Pivot: Revenue is shifting from volatile Mining to stable AI Hosting (HPC). 3️⃣ Valuation: Still trading at a discount to $CORZ despite better power assets.

Reloading🔋⚛️

8/22/25 Entry with $4 DEC 17 2027 LEAPS (I should have just played the stock as the BID/ASK is unbearably wide and frustrating when you are writing short premium against them.)

$GOOGL $IREN $CRWV

@mikealfred I think the credit score is a marker of how you use credit. If you want a high score its more about knowing how to play the game than it is of assets or the lack there of. Interesting that was kind of the trigger in the previous post.