oTFY is now live on @solana 🚀

$200M in trade-finance RWAs, fully composable within DeFi, built as high-grade collateral in Solana's lending markets. The asset is no longer a passive on-chain receipt. It becomes working capital inside a living financial system.

So it sounds like no verdict on money laundering (gov't could possibly re-prosecute). Guilty on conspiracy to transmit money, and not guilty on conspiracy to evade sanctions.

Happy about 1 and 3. The money transmission charge was inappropriate from the start and the way the legal rulings went down last winter may have doomed the outcome with a jury that can only find facts. This needs to be appealed, and Coin Center will do everything to make sure the judge gets the law right the next time around.

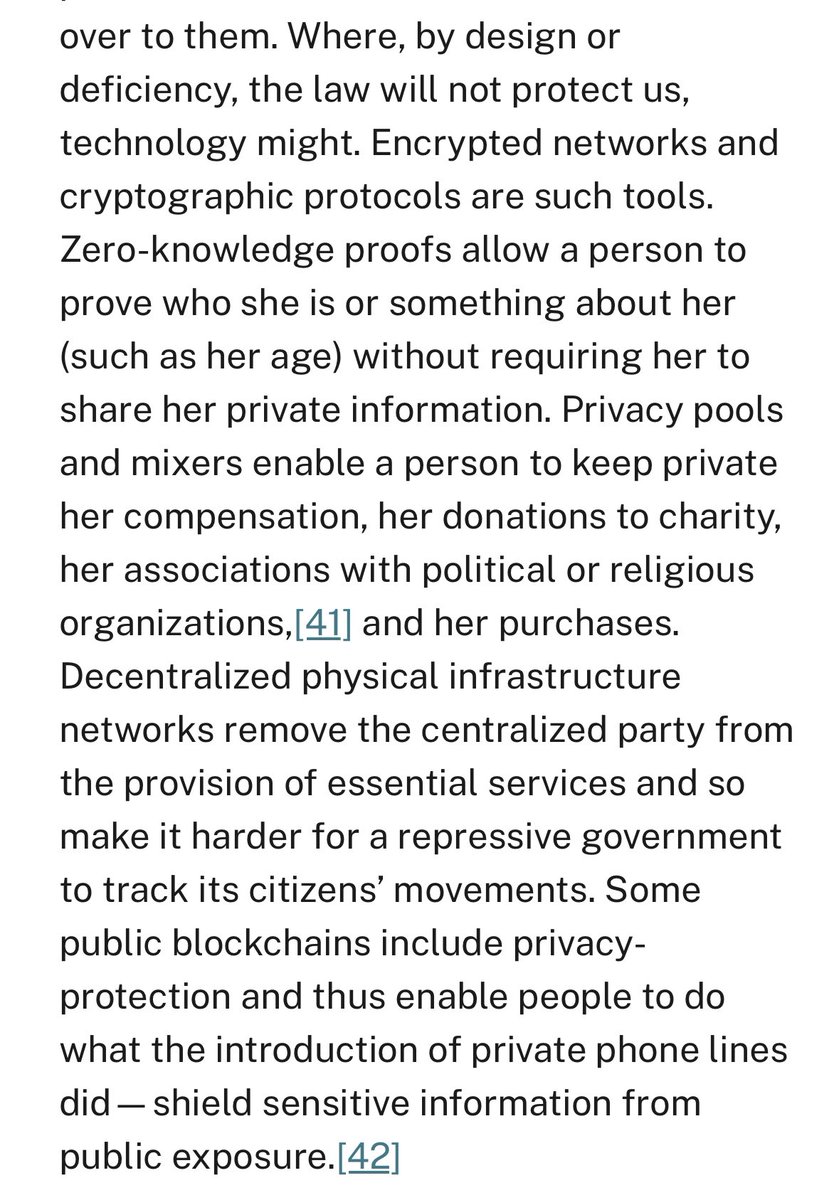

SEC Commissioner @HesterPeirce delivered an amazing speech today on financial privacy, which included references to Phil Zimmermann’s Pretty Good Privacy (PGP) and Eric Hughes’ A Cypherpunk’s Manifesto.

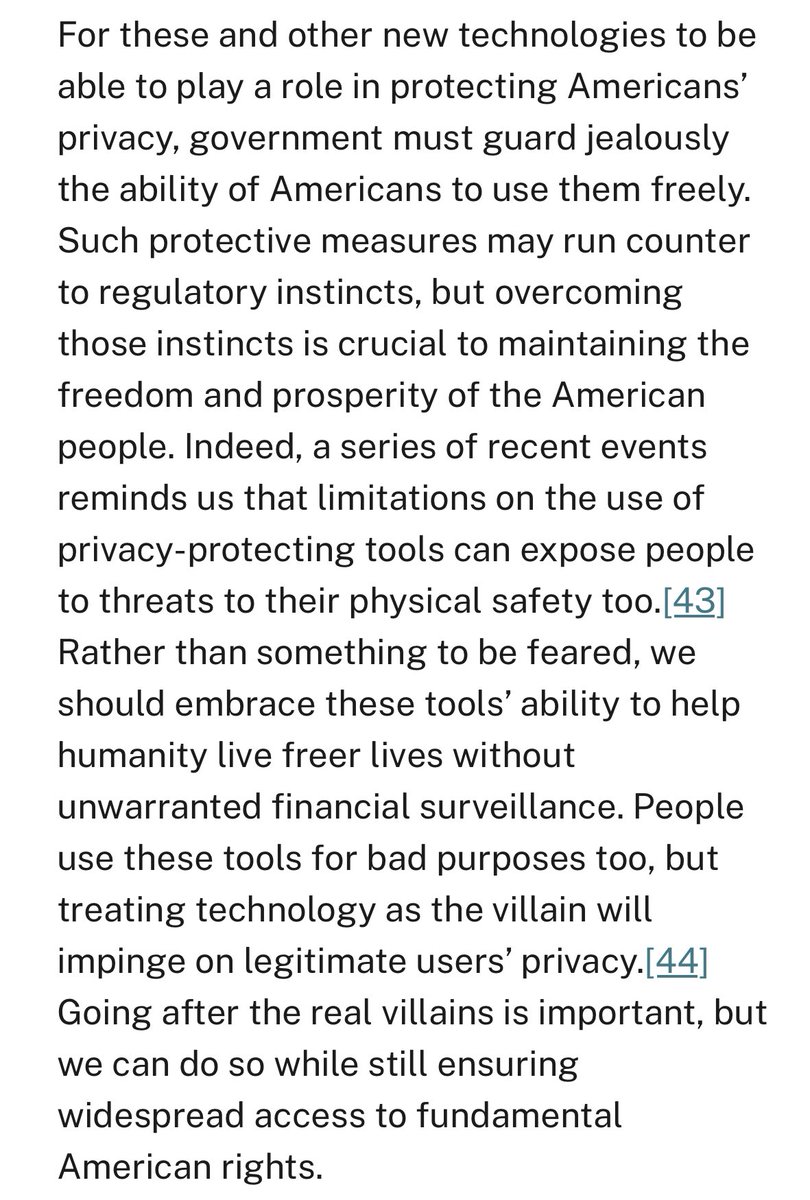

She stated: “Rather than something to be feared, we should embrace these tools’ ability to help humanity live freer lives without unwarranted financial surveillance. People use these tools for bad purposes too, but treating technology as the villain will impinge on legitimate users’ privacy.”

0/ On the topic of debunking factually incorrect takes, this thread from our friend Amanda Fischer at Bitter (a more accurate name these days, unfortunately) Markets hit my radar today.

This... is a mess.

Did a quick skim of the latest draft of the Digital Asset Market Clarity Act (aka the 'market structure bill'). I think this is the one.

People who have followed me know I have gone back and forth on different versions of this bill--initially liking it then hating it after the initial happy path for token clarity was made much narrower with many carveouts.

Since then, I have mostly reviewed and suggested changes in the background, working especially with @milesjennings and @SH_Brennan and @TheDRC_ who have been passionately engaged on the bill and done an amazing job surfacing issues from the broader cryptolaw community to the staffers drafting this bill. I don't have time to write a full analysis right now but at this point, my main concerns with prior drafts have been addressed & I can briefly summarize why/how:

-->tokens are not only exempted from being "investment contracts" under the bill, but also other kinds of securities ("notes", "profit participations") that could be claimed under other fuzzy-logic tests beyond Howey

-->@HesterPeirce 's 'safe harbor' notion is fleshed out into a full fundraising exemption (up $75M /year) for token sales of blockchain systems

-->only blockchain systems that will become 'mature' in four years qualify for the exemption, where ' maturity' is defined to track blockchain's core ethos of being open-source, decentralized, neutral, censorship-resistant, etc.

-->decentralized governance systems are recognized in the bill as a legitimate (and arguably almost necessary) part of a mature blockchain system, and will not typically be deemed to be legal persons, regulated issuers or license-requiring intermediaries--and such systems may include not only token voting, but also multisigs, councils, BORGs, etc., thus ensuring compatibility with other kinds of trust-minimization system designs beyond traditional "DAOs" (e.g., even single-sequencer L2 systems with security council checks/balances could be deemed 'mature', depending on their design & other factors)

-->there is recognition and protection of peer-to-peer transactions and private-key wallets

-->DeFi is largely carved-out from regulation, as are many ancillary activities related to blockchain such as validating, providing non-custodial DeFi web apps, etc.

The bill obviously is very complicated and of course will need a lot of post-passage work to interpret and create guidance & more specific rules around. It is not a cure-all--for example, we will have to trust the CFTC not to kill DeFi under preexisting law (swaps rules, leverage rules, etc.), which this act does not intrinsically address (though its carveouts for devs, webapps, etc. should be at least suggestive for what is appropriate in those other areas). Some may dislike that it gives special grandfathering rules for existing blockchains--Ripple and others will be able to 'get away with' retaining a much larger % of token ownership (50% vs. the otherwise applicable 20%) while nevertheless potentially being deemed 'mature'. And I'm sure there are other issues I'm overlooking--but that being said, I truly think this is as good as it will get, and also actually is just good, and we should pass it.

People keep asking me since days how to secure their systems and what the best strategy is. I will be very honest with you all as I'm always. If you want real security (and there will be never 100% security), it's not (just) about tools—it's about fucking mindset. At least 80% of it is pure paranoia. You and your team (can be a small DeFi project, can be a large CEX, ...) need to be paranoid as fuck. Drill it into them. Make it second nature. That's how you cut down risk, big time. The human factor is always the weakest link—no tech can _fully_ fix human fuck-ups. Sure, we'll kill blind signing, we'll upgrade our tools, but people will always be the problem. The only way to fix that? Train them to be fucking paranoid. There are no fucking shortcuts. If you have 900 employees, it's the leader's job to make sure all 900 are paranoid as fuck. You'll say that doesn't scale? Maybe not—but if you don't do it, you're effectively gambling with everything. And when shit goes wrong, the price you pay will be brutal.

again I must stress, I respect the hustle and skill that went into Solana & I understand the worldview & premises behind it & think there is some chance they could be correct, but it just has zero to do with what got me interested in crypto...which was self-sovereignty, censorship resistance, cyberanarchism, and dissidence... it's depressing to see one person after another capitulate & equate Solana's vs. Ethereum's tradeoffs to "competence" vs. "impractical idealism" etc., and of course it is always VCs leading this narrative ...The idealism is the entire fucking point, without it we might as well go back to servers. . .

Sony's L2 just showed us something wild about OP Stack censorship resistance:

Their attempt to block "unapproved" tokens spectacularly backfired in less than 24 hours after launch.

Here's exactly what went down 🧵

My watch has ended.

After five years as Kraken’s Chief Legal Officer, I’m passing on the reins to a successor.

I’ll stay close as a senior advisor. I’m going to help train up a successor and help to build a global advisory council for the company. I couldn’t be more proud of what we’ve achieved together as a team and I look forward to the next era of @krakenfx success.

Wait WHAT? Marco, WHY. And what's next? 👇

How Libra Was Killed.

I never shared this publicly before, but since @pmarca opened the floodgates on @joerogan’s pod, it feels appropriate to shed more light on this.

As a reminder, Libra (then Diem) was an advanced, high-performance, payments-centric blockchain paired with a stablecoin that we built with my team at @Meta. It would’ve solved global payments at scale. Prior to announcing the project, we spent months briefing key regulators in DC and abroad. We then announced the project in June 2019 alongside 28 companies. Two weeks later, I was called to testify in front of both the Senate Banking Committee and the House Financial Services Committee, which was the starting point of two years of nonstop work and changes to appease lawmakers and regulators.

By spring of 2021 (yes they slow played us at every step), we had addressed every last possible regulatory concern across financial crime, money laundering, consumer protection, reserve management, buffers, and so much more, and we were ready to launch.

We had worked on a slow rollout of a limited pilot that some members of the Fed’s Board of Governors were supportive of. At last, Chair Jay Powell was ready to let us move forward in a limited way. The story, as I heard it, is that Jay Powell was told by Treasury Secretary Janet Yellen at one of their biweekly meetings that allowing this project to move forward was “political suicide,” and she would not have his back if he let it happen. I wasn’t in the room when this conversation happened, so take these words with a grain of salt, but effectively this was the moment Libra was killed.

Shortly thereafter, the Fed organized calls with all the participating banks, and the Fed’s general counsel read a prepared statement to each of them, saying: “We can’t stop you from moving forward and launching, but we are not comfortable with you doing so.” And just like that, it was over.

One essential point is worth making here. There was no legal or regulatory angle left for the government or regulators to kill the project. It was 100% a political kill—one that was executed through intimidation of captive banking institutions. That was the hardest part of this story for me personally. Not that we had failed, but that America, this country I immigrated to and became a proud citizen of because of its rule of law and value system, behaved in such a way for political reasons. It was a very tough pill to swallow.

The bright side of the story, though, was the many learnings from this wild ride. By the end of the project, we had made so many concessions to get a thumbs-up that the whole design of the network became a Frankenstein of our initial ambitions.

We also learned the biggest lesson of all, which is that if you’re trying to build an open money grid for the world—eventually moving trillions of dollars a day, designed to be here 100 years from now—you have to build it on the most neutral, decentralized, unassailable network and asset, which, hands down, is Bitcoin.

And now this is what many of us who went through this scarring journey are building together at @Lightspark. And this time, we won’t stop until we get it done!

SDNY: Want to know if courts think you are doing unlicensed money transmission? Meh, go pay for a court transcript; it's not something we'll put down in writing.

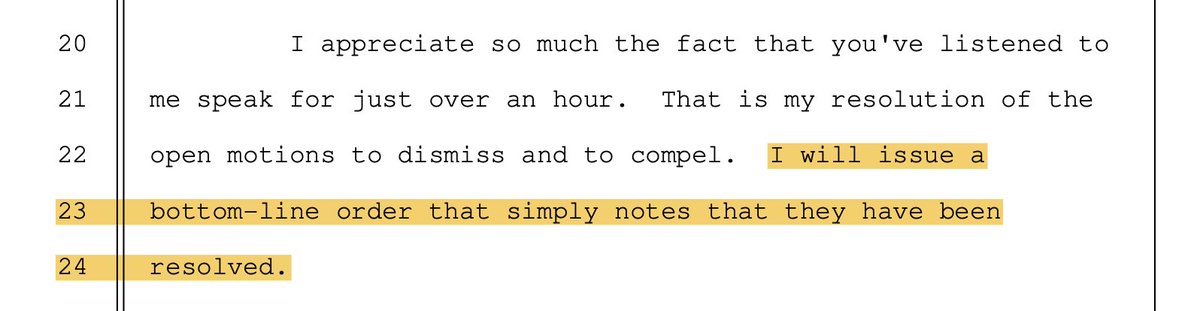

So, I'm working on an analysis of Judge Failla's disappointing ruling in Roman Storm's Tornado Cash case. One thing I can't get over is that she refused to even publish her reasoning in an opinion, choosing instead to read it orally on a hastily organized conference call and publish a "bottom-line" motion rejected order.

Official reasoning about highly consequential criminal liability for thousands of developers is not something that should be hidden from public view.

Can anyone think of a defensible reason for this obfuscation?

Put Pierce or Uyeda in charge of the SEC. They just get it. So reassuring to hear people who actually care about fostering capital formation at one of these hearings instead of Gensler's endless gaslighting.

so many of you will remember my reporting around "operation choke point 2.0" from the spring of 2023; TLDR, Biden's financial regulators, namely the Fed, FDIC, and OCC launched a crackdown on banks covering the crypto space...

Yesterday, the SEC announced the latest enforcement action against an NFT project - the social club @Flyfishclub

As Commissioners Peirce and Uyeda point out in their eloquent dissent titled "Omakase," the Flyfish settlement action "is just the latest dish that undermines trust in Chef SEC"

... and it smells fishy

The CFTC's action on Uniswap Labs has a problem. We don't learn anything from it.

The details released suggest that UL's crime could be as broad as merely publishing code, which is protected speech.

In settling they don't have to lay out their claims. No one learns what activities specifically trigger a CFTC action.

Today, the Federal Court for the Northern District of California ruled, as matter of law, that none of the tokens trading on Kraken are securities.

This is a significant win for Kraken, for the principle of clarity and for crypto users everywhere. It also confirms Kraken’s long-standing position that it does not list securities. 1/

yeah so there is a reason why prediction markets are heavily regulated (in fact basically prohibited) in the U.S.

whether that rule represents the right social cost/benefit analysis is very much an open question but let's not ignore the Black Mirror risks/downsides

this is also why I am a little more skeptical on switching all DAOs into a futurarchy governance model...adding a lot of regulatory risk to normal DAO governance and opening up a new frontier of extrinsic incentives...not saying it's bad, but I'm saying it's early and people only talk about the benefits not the risks...