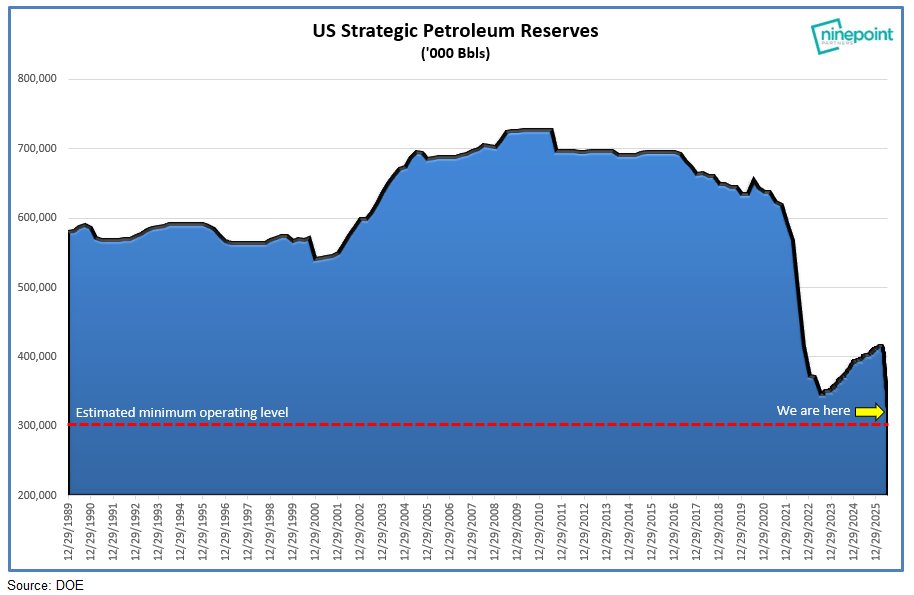

The US Strategic Petroleum Reserve is now ~19MM barrels away from estimated minimum operating levels. There very soon will no longer be a safety buffer to protect the world from further losses out of the Strait.

The greatest energy crisis of our lifetimes is not over yet! Yes there is a temporary glut from unsanctioned Iranian barrels + unlocked Strait vessels, but that is temporary. With inbound traffic 1/4 of normal, 8.6MM Bbl/d of still curtailed production, US SPR near operational minimums, and an inevitable return of Chinese buying, we believe the market is far too complacent: https://t.co/jrTcBGoyHT

Traffic through the Strait of Hormuz remains far from normal.

Only 62 ships transited the Strait on June 24. That was just 53% of the traffic recorded on the same day last year.

IRAN = CONTROLS THE STRAIT.

@hoje_no Quais eram os objetivos da guerra? 1 Deposição do regime político 2 Acabar com os mísseis balísticos 3 Acabar com o programa nuclear. Nada disso foi obtido. Vergonha de acordo. Não estou entrando no mérito da intervenção militar, apenas que o resultado foi vergonhoso

The Bloomberg Iran MOU contains the seeds of the next war.

Everyone is focused on Friday-- But what comes next is the key

After dissecting the agreement, I believe the next 60 days will become more dangerous—not less.

My new analysis at Escalation Trap Substack explains why: "Stage IV Begins?"

Trump: “The Deal with Iran is now complete… Strait of Hormuz OPEN TO ALL, US naval blockade lifted immediately.” Official signing Friday in Switzerland.

Market reaction was instant: Brent dropped to $84.88 (-3.2% on the day, -6% this week).

But the price is running months ahead of operational reality. 🧵

We are drawing inventories at unprecedented rates with no end in sight, and investors are the most bearish on oil in a decade...

I guess we need outright shortages for them to turn bullish.

@isaacrrr7 Como eu digo. Não se preocupem com Elon Musk ficando rico com o seu próprio dinheiro. Preocupem-se com políticos ficando ricos com o seu dinheiro.

@hajiyev_rashad Ok, now I understand. When you say buy, you mean sell. When you say sell, you mean buy. Great lol. Of course, one day you will be right but until there you will make a lot of people poorer.

Jeff Currie thinks we are sleepwalking into one of the biggest commodity shocks since Covid and the market is still pricing it like a headline risk instead of a physical crisis (Save this).

He calls it molecular contagion and last week, jet fuel shortages were concentrated in Singapore, where prices spiked to roughly 230 dollars a barrel.

This week the same pattern has shown up in Rotterdam at around 220 dollars and in Thailand, the Philippines, New Zealand, and Australia which means the dislocation has gone intercontinental.

In his words, there is no longer any meaningful spread between Singapore and Rotterdam, no spare barrels to re route, and no policy lever that can solve the problem in the short term.

Currie’s core point is brutally simple, you can print money, but you cannot print molecules.

The futures curve, the paper market is still trading around 100 dollars a barrel.

The physical market on the other side of the Strait of Hormuz is telling a completely different story, with Oman crude spiking to 173 dollars and Asia bound blends effectively clearing around 130 dollars a barrel.

Refined products like jet fuel and diesel are already spiraling north of 200 dollars a barrel in multiple hubs.

That is the tale of two markets he is talking about.

On one side you have screen prices that look volatile but manageable, helped by algorithmic trading, cross commodity hedging and the lingering belief that high prices fix high prices before anything breaks.

On the other side you have physical supply chains that are already breaking, tankers being diverted, refineries bidding against each other for the last uncommitted barrels, and regional shortages that cannot be solved with central bank liquidity.

US petroleum stockpiles are draining at a rapid pace:

Total US crude and petroleum product inventories fell -10.6 million barrels last week, to 1.57 billion barrels, the lowest since 2004, according to the EIA.

This was driven by commercial and government crude stocks, which fell -15.9 million barrels, the 2nd-largest weekly drop on record.

The drawdown comes as exports to Asia and Europe are surging, with global markets scrambling to replace lost Middle Eastern supplies.

Before the Iran War, US crude and petroleum product exports were ~3.0 million barrels per day. They are now up to 13.6 million barrels per day, the 2nd-highest reading on record.

Meanwhile, the Strategic Petroleum Reserve fell another -7.9 million barrels last week, now down -58 million barrels since the start of the war, to 357 million barrels, the lowest since January 2024.

The US is acting as the lender of last resort for global oil markets.

The US government is becoming increasingly dependent on private investors to finance its growing debt burden:

Privately held US Treasury debt maturing within 1 year is up to a record $8.3 trillion.

This figure has DOUBLED over the last 5 years, reflecting the government's growing reliance on short-term financing from private investors.

As more debt shifts into Treasury bills, a larger amount must be refinanced every year, leaving borrowing costs increasingly sensitive to interest rates and investor demand.

At the same time, foreign central banks are reducing their share of Treasury holdings, making private investors absorb a larger portion of new issuances.

As a result, the Treasury market is becoming increasingly dependent on investor demand and liquidity conditions rather than the stable long-term buyers that have traditionally anchored it.

With US public debt at an all-time high, even modest disruptions in funding markets could have an outsized impact on borrowing costs.

Treasury refinancing risks are intensifying.

Rick Rule: Very soon we will see oil shortages.

Rich countries will outbid poor countries... the rich will pay higher prices, the poor will have to deal with shortages.

But this doesn't mean rich countries won't face problems.

- Higher oil prices are a tax, driving liquidity out of markets

- Combine that with higher interest rates and you get a recipe for disaster

In this kind of market environment, having excess liquidity lets you sleep at night and gives you the opportunity to take advantage of a market correction.

Jeff Currie, former Goldman Sachs head of commodities and now at Kalo writing research, is watching a physical supply shock in the commodities market.

This is a tale of two markets.

Paper crude oil was sitting around $100 a barrel while physical crude being delivered into Asia was trading between $130-$170. Products like jet fuel were spiraling above $200.

The spread between paper and physical has completely disconnected.

On the physical side: a discount airline out of London Gatwick canceled all flights because they couldn't source fuel. The UK just took its last known kerosene shipment with no further arrivals scheduled. Singapore jet fuel spiked to $230 a barrel. Rotterdam hit $220. The shortage is now in Thailand, Philippines, New Zealand and Australia.

Currie called it "molecular contagion."

And here's the critical point: there is no policy fix for this. The supply shock is roughly equal in magnitude to the COVID demand shock. And we all watched what COVID did to global supply chains.

Currie's framing: the paper markets have disconnected from reality. When crude is trading at $100 on NYMEX but delivering into Asia at $130-170, someone is wrong. He thinks it's the paper market.

The mispricing window doesn't stay open forever.

For macro investors, this is exactly the kind of dislocation between financial prices and real-world supply chains that historically creates the biggest moves.