MORGAN STANLEY WARNS US STOCKS MAY STRUGGLE TO HIT NEW HIGHS AS INVESTORS ROTATE OUT OF BIG TECH

Strategists at Morgan Stanley believe US equities could face difficulty reaching fresh record highs as investors rotate out of this year's top-performing technology stocks into other sectors. The shift could reduce the leadership of AI- and technology-driven mega-cap stocks that have powered much of the market's gains.

JPMORGAN: BUY THE CHIP STOCK DIP

JPMorgan says the recent pullback in semiconductor stocks is a buying opportunity, arguing the AI-driven chip cycle remains strong and meaningful new supply is unlikely before 2028.

The bank favors semiconductors over hyperscalers, expects global stocks to reach new highs in the second half of 2026, and sees market gains broadening beyond AI.

CEO of Samsung, Kim: “This year’s profit alone will exceed the cumulative profit generated over the 40 years since Samsung entered the semiconductor business.�� $DRAM $EWY $NVDA

Since Samsung officially committed to the semiconductor business in the early 1980s, it has navigated multiple major memory cycles (including the dot-com boom, the smartphone transition, and the 2017 cloud supercycle). The sheer pricing power of the 2026 AI boom means a single year of operations is on track to out-earn the net nominal profits of all those decades combined.

Samsung is expected to post a Q2 2026 operating profit of roughly 84.6 trillion to 86 trillion won ($55B to $56B) and over $200 billion for the year. If official preliminary earnings match these consensus figures, Samsung will surpass Nvidia's Q1 operating profit ($53.54 billion) to become the single most profitable corporate enterprise on Earth for the quarter.

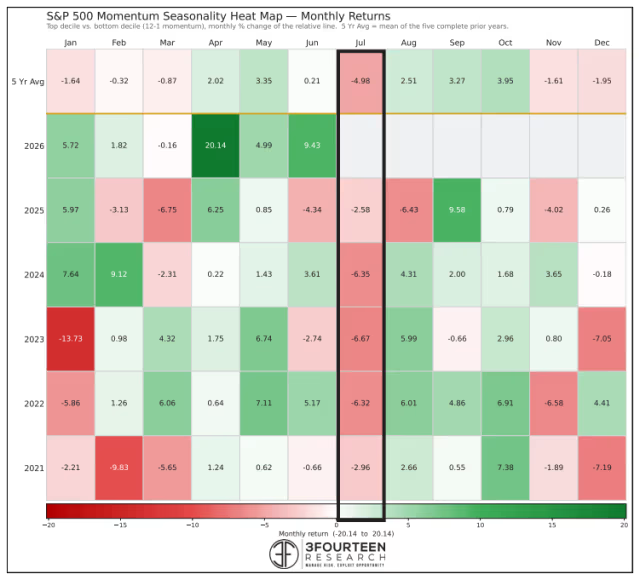

While you very likely have seen the chart from @WarrenPies (first chart) showing how the momentum factor is seasonally weak in July (Warren actually called for a potential "violent rotation" away from momentum which arguably we've seen with the Invesco S&P 500 Momentum ETF $SPMO down 6.6% this month), but the MarketWatch article also covers where he thinks investors might rotate that momentum money.

From the article:

"Pies expects that investors taking profits from the run-up in chips stocks may find opportunities this month in oversold equities tied to the 'quality factor' — particularly those in the relatively “disjointed” pocket of beaten-down stocks with momentum scores in the bottom 10% of the S&P 500."

“Quality has become synonymous with potential AI disruption,” he said — explaining that AI is generally viewed as having the potential power to destroy the competitive “business moat” associated with quality companies.

Warren also says to keep an eye on correlations which are near decade lows (second chart).

“Internal correlations drop as a bull market ages,” according to Pies. So “once you have really low correlations, some people might start looking for a top signal,” he said — although for now, “I think that’s a little premature,” he added. But he cautioned that “fragility comes back if correlations start to get closer to the norm.”

Last week showed continued capital rotation out of semi stocks as short-dated options dominate major indices. Learn more in our weekly newsletter: https://t.co/JTqUGT327s

Morgan Stanley: "Arguments that AI will be disinflationary and lead to lower policy rates should be re-examined and possibly rejected. First, the state of the business cycle will dominate. Second, the disinflationary effect is one of many; more productivity should also mean more demand, both through consumption and investment spending. Finally, faster productivity growth means higher equilibrium interest rates – r*, as economists say – further confounding the case for rate cuts. The simple argument is almost surely wrong."

The AI infrastructure buildout is entering a new phase:

US tech companies are committing to spend a record $850 billion on data center leases over the next several years.

This marks a +$570 billion YoY increase, or +204%, and +$200 billion QoQ increase, or +31%.

Meta, $META, added the most in Q1 2026, committing +$79 billion in new leases, a +76% QoQ increase, bringing its total to ~$183 billion.

At the same time, Microsoft, $MSFT, added +$41 billion, a +26% QoQ increase, bringing its total to ~$197 billion.

Oracle leads with the largest total commitments at ~$250 billion, having already secured many of the key sites needed to fulfill its contract with OpenAI.

Tech companies are doubling down on AI.

"The scale of China's oil demand collapse has been so dramatic that Chinese policymakers are reportedly examining whether this historic slump reflects a temporary response to elevated global prices or a more structural shift in consumption patterns." - JPM

Nice article from MarketWatch (based on an interview from last week). I discussed our call for a momentum unwind and how that has played out early in July.

https://t.co/4b79Pk8eDK

Is the AI infrastructure trade running out of steam?

JPMorgan: Data Center Watch report says not even close.

Worth bookmarking if you're tracking the AI capex debate.

Token usage, GPU leasing rates, and DRAM prices continue to rise. JPM noted in its latest 'Data Center Watch' report that large model usage continues to expand rapidly, token spending has reaccelerated, GPU leasing prices in the non-hyperscale cloud market are still rising, and DRAM spot prices remain strong.

> LLM token : June volume +70% MoM (vs May's 33%, April's 5%). YoY growth hit 20x, above May's 12x and April's 15x. Token spending also rebounded, +70% MoM and 16x YoY, snapping the prior two months' slowdown.

> Unit economics: Token usage and revenue are diverging. Falling model prices haven't dented market revenue - price erosion is slowing while usage growth outruns the cuts. This is the number that decides if AI commercialization actually works.

> Country wars: US models (OpenAI, Anthropic, Google, xAI) fell to 35% of OpenRouter token share, down from 46% in May and 56% in April - even as their volume grew 30% MoM and 8x YoY. Chinese/low-cost models (DeepSeek, MiniMax, MiMo, GLM) are eating share in cost-sensitive use cases: dev workflows, startups, agent coding.

> Rental prices: A100 at $1.63/GPU-hour (+6.3% MoM, 5th straight monthly rise). H100 at $2.72 (+3.7% MoM, 7th straight month up). B200 at $5.33 (+2.7% MoM).

> Memory: AI server DRAM demand is pulling supply from conventional DRAM. Three straight months of modest price declines suggest NAND tightness is easing - but prices are still up 5x+ YoY, so the industry hasn't hit supply abundance yet.

Which number surprises you more: token growth reaccelerating to 20x YoY, or GPU rental rates still climbing after 5-7 straight monthly increases?

Repost this if you're tired of the "AI capex is slowing" take this report has the actual numbers on it.

DeepSeek is hiking prices: Under new pricing, peak hour costs for its V4 Pro will rose to 12 yuan (US$1.77) for every million output tokens from the standard rate of 6 yuan during non-peak time

Doing this so fast after its 75% price cut in May signals major market share gains

The NASDAQ is 97.5% correlated to total global liquidity.

It has almost nothing to do with earnings or how good the companies are, and everything to do with how much money the world's central banks are printing.

The small slice that liquidity doesn't explain is the NASDAQ's own adoption curve sitting on top.

This is why everyone keeps saying equities are expensive. They're using a measure that stopped working the moment we started debasing currency. A high valuation doesn't really tell you a company is doing well anymore, it tells you how much money has been printed.

This is the heart of my Everything Code framework. Once you understand that liquidity is the key driver of all asset prices, the market stops behaving like a mystery and starts running like clockwork.