La fábula de la ventana rota, formulada por Frédéric Bastiat, es una de las lecciones más simples y contundentes de la economía. La historia parte de una escena aparentemente menor: un niño rompe el vidrio de una tienda. De inmediato, algunos observadores dicen que no todo está perdido, porque ahora el vidriero tendrá trabajo, cobrará por reparar la ventana y ese dinero circulará en la economía. A primera vista, parece que el daño generó actividad. Parece que la destrucción produjo empleo. Parece incluso que el accidente trajo un beneficio.

Pero ahí aparece la verdadera enseñanza de Bastiat: no basta con mirar lo que se ve. Lo visible es el vidriero trabajando, el dinero cambiando de manos y la ventana reparada. Lo invisible es todo aquello que el comerciante ya no podrá hacer con ese dinero. Tal vez iba a comprar zapatos para su hijo, invertir en más mercadería, mejorar su local, pagar una deuda o ahorrar para crecer. Ese uso alternativo desaparece porque ahora el dinero debe destinarse a reparar algo que antes estaba sano. Por eso la sociedad no se enriqueció; simplemente volvió al punto de partida, pero con una oportunidad perdida.

La gran trampa está en confundir movimiento con riqueza. Que haya gasto no significa que haya progreso. Que alguien cobre no significa que la sociedad gane. Si romper ventanas fuera una fuente de prosperidad, entonces los países más ricos serían los más destruidos. Pero la realidad es exactamente la contraria: la riqueza nace de crear, producir, ahorrar, invertir y coordinar esfuerzos hacia fines más valiosos. La destrucción puede generar actividad, pero no genera riqueza neta; obliga a desviar recursos hacia la reparación de un daño.

Por eso esta fábula sigue siendo tan poderosa para entender la política económica. Muchos gobiernos justifican el gasto público, la obra innecesaria, la burocracia o la intervención estatal diciendo que “generan empleo” o “mueven la economía”. Pero Bastiat nos obliga a hacer la pregunta incómoda: ¿qué habría hecho la sociedad con esos recursos si no se los hubieran quitado? ¿Qué inversiones, consumos, emprendimientos, ahorros o mejoras quedaron invisibles porque el dinero fue absorbido por una decisión política?

La fábula de la ventana rota enseña que la economía no debe analizarse desde la emoción inmediata, sino desde las consecuencias completas. El buen economista no se queda con la primera imagen, con el aplauso fácil ni con el beneficio visible para un grupo particular. Mira también el costo oculto, la alternativa sacrificada y el daño que no aparece en la foto. Esa es la diferencia entre pensar en serio y caer en propaganda: ver no solo al vidriero cobrando, sino también al comerciante perdiendo aquello que ya no podrá construir.

In 458 BC, Rome was on the brink of collapse.

An invading army had trapped the Roman consul and his legion in a mountain pass. Panic spread through the city. The Senate did the only thing they could think of:

They sent messengers to find a 60-year-old farmer plowing his field.

His name was Lucius Quinctius Cincinnatus. He had once been a senator, then lost his fortune paying his son's bail. Now he worked his own four-acre plot just to feed his family.

When the Senate's envoys arrived, they found him sweating behind a plow. They asked him to put on his toga so they could deliver an official message.

The message: Rome was making him dictator. Absolute power. Total command of the army. No checks. No oversight. No term limit.

He accepted.

Within 16 days, Cincinnatus had raised an army, marched out, surrounded the enemy, and forced their surrender. The republic was saved.

He had legal authority to rule for six months. He could have stayed. He could have expanded his power. He could have done what every other ruler in human history did when handed unlimited control.

Instead, he resigned on day 16.

He took off the toga, walked back to his farm, and finished plowing the field he'd left half-done.

Twenty years later, when Rome faced another crisis, they called him back. He was 80 years old. He took command, crushed the conspiracy, and resigned again, this time after just 21 days.

He died poor. On his farm.

2,200 years later, when George Washington was offered a kingship after winning the American Revolution, he refused and went home to Mount Vernon. The reason he was hailed as "the American Cincinnatus" is because Europeans literally could not believe a man who had won would willingly give up power.

King George III, on hearing Washington would resign rather than rule, said: "If he does that, he will be the greatest man in the world."

The lesson isn't that Cincinnatus was humble.

The lesson is that for most of human history, the people most qualified to lead were the ones who didn't want to. And the moment a society starts rewarding those who chase power instead of those who flee from it is the moment the republic begins to die.

Cincinnati, Ohio is named after him.

Most people who live there have no idea why.

Warren Buffett just warned that the US dollar could collapse and admitted he doesn't understand most of the stock market anymore.

95 years old, sitting on $380 billion in cash, and the first time watching from the sidelines instead of actively investing.

And what he revealed at this weekend's Berkshire shareholder meeting is genuinely concerning:

On the market, Buffett didn't hold back.

He compared it to "a church with a casino attached" and said the casino has never been more packed. On one-day options: "That is not investing. It's not speculating. It's gambling. Totally."

He pointed to the Avis short squeeze THIS WEEK. A rental car company that's been around for 50 years getting meme-squeezed in 2026. The same behavior that blew up retail traders with GameStop is back, except now it's hitting boring legacy companies with zero business being volatile.

"We have lots more regulation now, but people spend their time figuring out how to get around the rules rather than follow the rules."

That one sentence explains more about the current market than every CNBC segment combined.

When asked why he's hoarding $380 billion instead of investing it, Buffett said something no one expected:

"I understand fewer of the businesses as a percentage of the whole than I did 10 years ago. I have not learned new industries for some years. I'm not going to have an edge on a whole bunch of younger people that have actually grown up with it."

Think about what he's actually saying...

This is a man who made $140 billion by understanding businesses better than anyone alive. And he's telling you the current market is so detached from reality that even HE can't make sense of what's being valued and why.

He quoted IBM's Tom Watson Sr.: "I'm smart in spots and I stay around those spots."

In 60 years of managing money, he said MAYBE five were "really juicy." Five out of sixty. That means 92% of his career was spent WAITING while everyone else gambled. And he still ended up richer than all of them.

Then the conversation turned to inflation and that's where it gets really interesting:

Buffett said America is "not immune" from runaway inflation. He brought up countries that went bankrupt "six or seven times" in his lifetime.

Compared today to right before Volcker had to rescue the dollar, when Americans were borrowing at 12% to buy farmland earning 6% because they believed the dollar would disappear.

"Cash is trash" was the mentality.

Nebraska farmers collapsed

because of it. Entire communities wiped out not by a recession but by a BELIEF that the currency was dying. And Buffett sees that same energy building again.

Then someone asked the question everyone wanted answered: Do you see a crash coming?

"If you saw it coming, it wouldn't happen. The things people are talking about and thinking about? It's not going to happen. But there are things that can come out of the blue."

He compared it to the assassination of Archduke Franz Ferdinand in 1914 that triggered World War I. Nobody was discussing or anticipating it. But it changed the world overnight.

"That's particularly true now because of the things that can come out of the sky."

A 95yo man who has survived every crash, every war, every crisis of the last six decades just told you the market is a casino, the dollar isn't safe, and the real collapse will be something nobody sees coming.

$380 billion in cash is his answer because he believes things are about to get much worse.

Berkshire Hathaway's annual shareholder meeting just produced two moments worth paying attention to.

Greg Abel described compounding inflation at 8–9% as a "terrifying scenario." That is the person who will run the largest holding company in the world using the word terrifying — unprompted, on the record, in front of 40,000 shareholders.

The second moment is that Berkshire's cash position is now $397.4 billion. The company has been a net seller of equities for 14 consecutive quarters. They are not finding things worth buying. They are not deploying. They are holding T-bills at a scale that has no historical precedent for this firm.

The connection between those two data points is not a conspiracy. It is a balance sheet. If you believe inflation could reaccelerate to 8–9%, the correct positioning is exactly what Berkshire has done — liquidate equities priced on disinflationary assumptions, hold short duration instruments that reprice with rates, and wait. Cash earning 5% while inflation is 3.5% is not a great real return.

Cash earning 5% while inflation goes to 8% is a disaster — but it is a recoverable disaster. Equities priced at 22x earnings in an 8% inflation world are not.

Abel did not say inflation is going to 8–9%. He said it would be terrifying if it did.

That is a precise and deliberate distinction. But the cash pile says the optionality against that scenario is worth more to them right now than any asset they can find at current prices.

PCE is at 3.5%. Core PCE is 3.2%. Both are three year highs. Brent is at $119. Fertilizer exports through Hormuz have stopped. The people running the most patient capital allocation operation in history are sitting on $397 billion and calling high inflation terrifying.

What do you think they're seeing?

Un estudio psicográfico del equipo del economista Asdrúbal Oliveros (@aroliveros) junto a BAM Consulting revela que el consumidor venezolano de 2026 investiga más que nunca y todavía lleva en el ADN el amor por la comodidad: aunque el bolsillo no siempre lo permita.🧵

Just In: $BRK.B Berkshire's cash-to-total-assets ratio just hit its highest level since 2008.

$373B in cash. $373B on the sidelines.

Last time Warren Buffett hoarded cash like this:

• 2007 — before the financial crisis

• 2020 — before COVID crash

Great parting gift for Greg Able who took over Berkshire Hathaway as the CEO start of 2026.

🚨"El hombre moderno se encuentra en una situación terrible. Está perdidamente enamorado de la belleza de lo que construyó el viejo mundo, pero desprecia las creencias que lo inspiraron a construirlo". —Jeremey Wayne Tate

US Energy Secretary Chris Wright tells me he sees Venezuelan production up 30-40% by year-end from current level (that's ~270,000-360,000 b/d extra).

Last month, I wrote this @Opinion column suggesting there're "low hanging oil barrels" in Venezuela ⬇️���️

https://t.co/ptdquUaohr

RIP Robert Duvall (1931-2026)

Robert Duvall is undoubtedly one of the greatest actors of all time. His contribution to Cinema is immense.

He was a part of one of the most important periods of American Cinema & featured in many of the masterpieces, with "Apocalypse Now" (1979, Coppola) being one of them.

This is one of the most iconic lines in the History of Cinema. He will be missed by all.

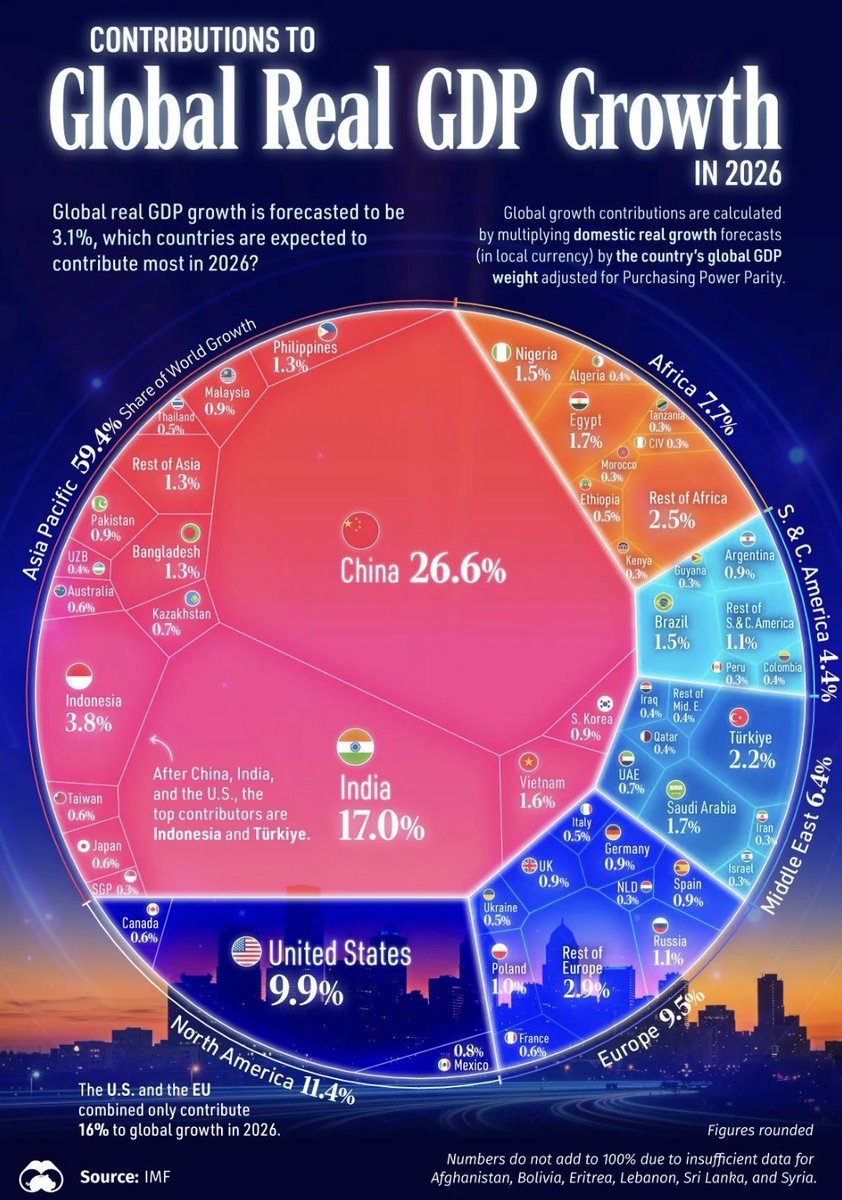

🌍Global growth in 2026🚀

🇨🇳#China alone drives 26.6% of global real GDP growth.

🇮🇳#India adds 17%.

🇺🇸 US contributes 9.9%.

Asia = the engine.

China + India + US ≈ 54% of global growth.

US + EU combined? 16%.

This is the economic balance of power, already shifting.

-¿Qué os dan de comer a los hombres de Pittsburgh?

-Acero, y hornos de fundición tan calientes que un hombre olvida su miedo al infierno.

Diálogos fordianos... #fordianos

Tres (3) bancos de inversión hablan sobre el sector petrolero de Venezuela y su impacto global:

1. JP Morgan:

"Venezuela podría alcanzar, de forma realista, niveles de producción de 1,3 a 1,4 millones bd en dos años tras una transición política. Con nuevas inversiones y reformas institucionales importantes, la producción podría alcanzar los 2,5 millones bd en la próxima década. Actualmente, la producción petrolera del país ronda los 750 mil bd."

2. Goldman Sachs:

"Una producción venezolana potencialmente mayor a largo plazo incrementa aún más los riesgos a la baja para nuestro pronóstico del precio del petróleo para 2027 y años posteriores. Si bien Venezuela produjo aproximadamente 3 millones b/d en su punto máximo a mediados de la década de 2000 y posee las mayores reservas probadas de petróleo del mundo (aproximadamente una quinta parte de las reservas globales), creemos que cualquier recuperación de la producción probablemente será gradual y parcial, dado el deterioro de la infraestructura, y requerirá fuertes incentivos para una inversión sustancial en exploración y producción. Estimamos una baja de US$4/bl en nuestro pronóstico base del precio del petróleo Brent para 2030, de US$80/bl, en un escenario alcista donde la producción de crudo venezolano aumente a 2 millones b/d en 2030 (en comparación con nuestro escenario base de 0,9 millones b/d)."

3. ING:

"Por ahora, los acontecimientos del fin de semana no nos han llevado a cambiar nuestra perspectiva sobre el mercado petrolero para 2026. Seguimos esperando que un mercado bien abastecido influya en los precios y seguimos pronosticando que el Brent promediará 57 dólares por barril durante 2026. Mientras tanto, para 2027, existen riesgos a la baja para nuestro pronóstico de 62 dólares por barril si empezamos a ver aumentos significativos de la oferta de Venezuela, aunque mucho dependerá también de la respuesta de la OPEP+."

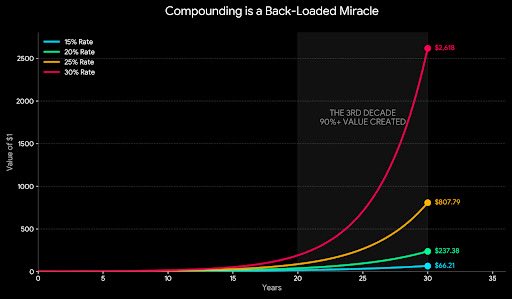

The power of compounding is widely understood. What’s underappreciated is when the value is actually created.

Compounding is continuous, but when you look at it in decade blocks, the pattern becomes obvious. Even moderate differences in the annual compounding rate are severely amplified over time. For instance, starting with $1:

At 15% annual compounding

10 years: $4.05

20 years: $16.37

30 years: $66.21

Last decade: 75.3% of the total value

At 20% annual compounding

10 years: $6.19

20 years: $38.34

30 years: $237.38

Last decade: 83.8% of the total value

At 25% annual compounding

10 years: $9.31

20 years: $86.74

30 years: $807.79

Last decade: 89.3% of the total value

At 30% annual compounding

30 years: $2,618

Last decade: 92.8% of the total value

A 2× difference in the rate (15% vs 30%) becomes nearly a 40× difference in outcomes over 30 years.

Compounding doesn’t add. It multiplies the entire base.

The first decade is impressive.

The second decade is extraordinary.

The last decade is unfathomable.

That’s when fortunes are made.

That’s why the ceiling matters. If the market size caps you early, compounding dies early. You need a category large enough to let it run for decades.

Once you see compounding this way, it permanently changes how you choose markets.

Health insurance, for instance, is roughly a $1.7T TAM in the U.S. alone. It may not be the sexiest space, but that’s one of the reasons I’m so excited about Curative Health long term.

What business today has a ceiling high enough to compound until 2056?