Building stablecoin infrastructure for financial inclusion | CEO @Haraka_xyz | Writing about behavioral econ in fintech, UBI, and emerging market payments | Ex:

Today we are shutting down the Bondy app and winding @Haraka_xyz down.

We started Haraka with a mission to bring financial access to people around the world marginalized by the traditional financial system. We advanced that mission over the last two years by giving loans to farmers in rural Ghana, credit scores to shopkeepers in Nairobi, and access to dollar savings accounts to freelancers in Nigeria.

We gave it everything we had, and while we didn't find the path to scale, we're grateful for every person who joined us on this ride. The mission lives on. Thank you.

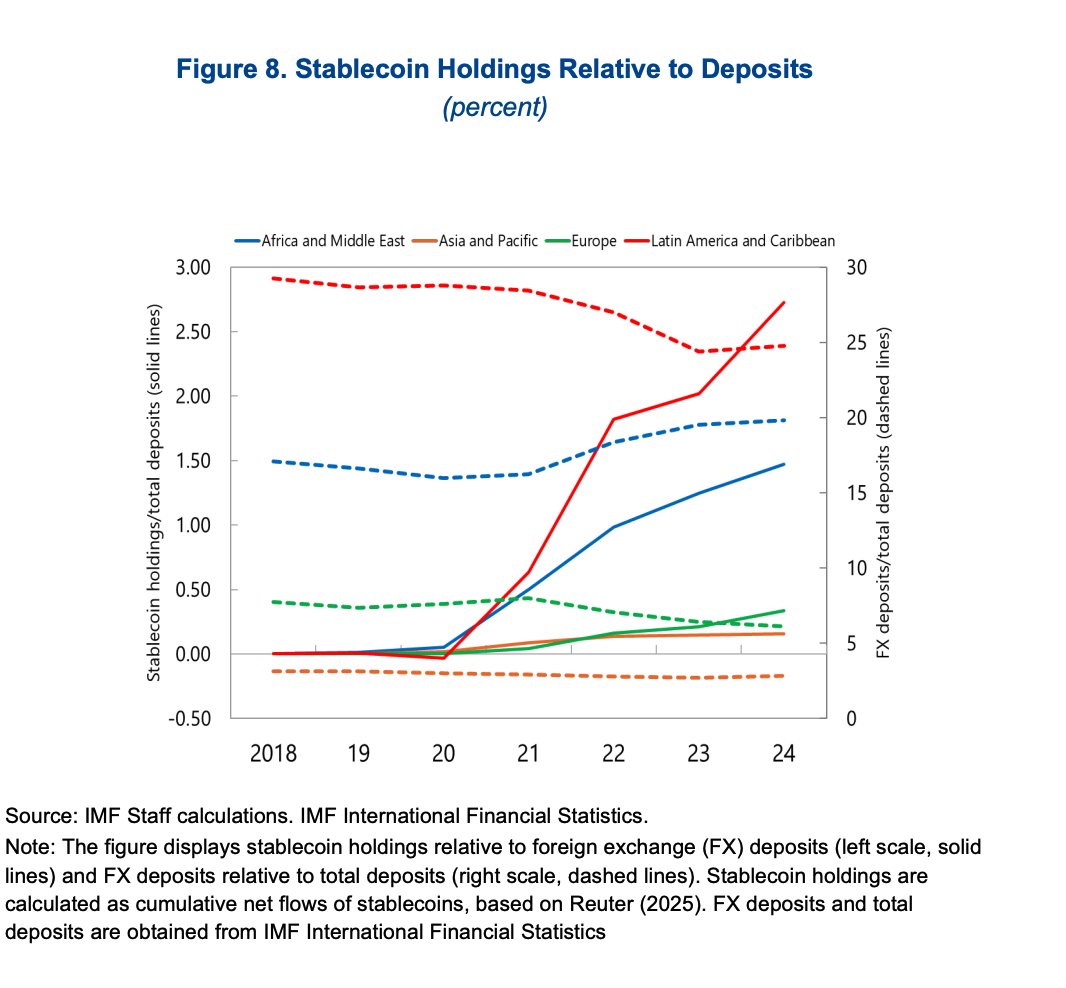

Interesting to see hard data behind what we know to be anecdotally true: LATAM and Africa are rotating into stablecoins as a way to hold foreign currency deposits.

Shame this only goes to 2024 - anyone know of data thru 2026?

Every screen. Every flow. Every pixel. The @Haraka_xyz brand. The Bondy rebrand. The logo. The UI. The social media. The component library. The onboarding. The dev handoffs across two markets. One designer. In the hands of 10,000+ users.

This International Women's Day we're highlighting the women powering Bondy. Starting with @just_i_m_a, our product designer and the person responsible for literally everything you've ever seen from us. Jack of all trades when it comes to design. Master of all.

And we're live! After months of work - excited to introduce a fresh and redesigned Bondy.

We built Bondy for a new generation of hustlers who earn globally but spend locally, with a bunch of added features that makes that experience seamless.

You can just open a USD account that earns 10%.

You can just spend locally without thinking about FX. You can just do things.

Now live in Nigeria 🇳🇬 and Kenya 🇰🇪

Sign up at https://t.co/6TiE8PdDnD

Anyone surprised that retail stablecoin adoption is higher in Nairobi than New York?

"Among respondents, a higher proportion own stablecoins in low and middle-income economies (60%) than in high-income ones (45%), with Africa leading at 79%" - https://t.co/WbYPjSsaKe

The mother of adoption is necessity.

Tokenization is the next step in a long, consistent evolution of financial markets toward greater speed, reach, ubiquity, and portability.

Stablecoins proved that blockchain infrastructure can operate at scale for core financial assets. Securities are next. They remain constrained by legacy settlement, fragmented ownership records, and layers of intermediaries that are no longer necessary.

@SuperstateInc is built around this transition. By combining an SEC-registered transfer agent with native blockchain infrastructure, it enables securities to move onchain without changing their legal form or regulatory treatment.

The result is not just faster settlement, but a fundamentally different market structure: real-time ownership, programmable corporate actions, and direct issuer-investor relationships.

I don't know who needs to hear this.

If presented currency options (local or home) when using your credit card abroad, always choose local.

https://t.co/GpRXYY8yGN

@Haraka_xyz

We partnered with @MCSocialVenture to test reputation-based lending + stablecoin credit with women’s savings groups in Ghana. Join us to hear what worked.

Nov 25 | 4 PM EAT / 9 AM ET

Register: https://t.co/5RpQL2QyIT

Access to credit is the biggest barrier for micro-entrepreneurs in emerging markets—especially women & informal workers left out by banks.

We’re joining a live convo next week to share what actually works from our DeFi pilots in Colombia, Ghana & Cameroon.

Real-World DeFi: Lessons Driving Financial Access

🗓️ Tue Nov 25

⏰ 4pm EAT | 8am Colombia | 9am ET

@quipulatam@FreeWillLe@Haraka_xyz@REasy + Njeri Muhia MCV @MCSocialVenture on building trust, low-tech usability & how to reach the excluded.

👉 https://t.co/HRb1TnvuaQ

Let me tell you a secret everyone in emerging markets already knows: the dollar never has one price.

Multiple markets, multiple rates, one reality. Onchain FX fixes this