A decade ago, Mastercard traded at 24.5x free cash flow.

Today, it trades at 25.0x free cash flow.

In that same period, free cash flow per share increased 422%.

$MA

$NU vs $JPM

Nu revenue increasing 45% YoY, JPM by 7%

Net income increasing 48% YoY, JPM by 12%

NU ROE of 25%, JPM 20%

$NU P/E is 18, $JPM is 14

In a little over half a year, Nu Bank would have the same P/E as JP Morgan Chase at this rate, at which point you would own what appears to be a high quality business growing significantly faster.

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

MY 3 FAVORITE STOCK OPPORTUNITIES RIGHT NOW

1. $MELI | MercadoLibre

MercadoLibre is the cleanest example of a stock that looks broken because the market wanted near-term EBIT while the business is clearly on fire underneath. Revenue grew 49% YoY to $8.8B, commerce grew 47%, fintech grew 51%, GMV grew 42% and Brazil items sold accelerated 56% yet the stock sold off because margins compressed as management chose to reinvest into free shipping, logistics, credit cards, 1P commerce and marketing instead of managing the quarter for the market.

I think the market is trying to paint MercadoLibre as this mature retailer trying to squeeze out another 50 bps of margin but really it's still building the $AMZN + $PYPL + $XYZ logistics layer for LatAm in a region where e-commerce, digital payments, credit, ads and primary banking adoption are still years behind the U.S.

2. $SOFI | SoFi

SoFi is a stock that looks broken because the market wanted the usual beat-and-raise while the business still delivered numbers that most fintechs would kill for. Revenue grew 41% YoY to $1.1B, EBITDA grew 62%, members grew 35% to 14.7M and loan originations grew 68% to $12.2B but the stock sold off because management only reiterated guidance, rate cut expectations have disappeared and the Tech Platform (Galileo) segment remains weak from the Chime offboarding.

My thesis is that SoFi is still building the all-in-one digital finance platform for the next generation. The core flywheel is intact because members are growing, deposits are scaling, lending demand remains strong and ~45% of new products are coming from existing members.

3. $META | Meta Platforms

Meta is a stock the market keeps treating like an AI capex problem while the actual business is becoming one of the clearest AI monetization engines in the world. Revenue grew 33% YoY to $56B, ad impressions grew 19%, ad pricing grew 12% and Q2 guidance came in stronger than expected but the stock sold off because Meta raised capex guidance by $10B and market immediately went back to the fear that Zuckerberg is overspending before the payoff shows up.

I think the payoff is already showing up since AI is improving Reels ranking, video engagement, ad targeting, conversion quality, business messaging and creative performance across Facebook, Instagram, WhatsApp and Reels. Meta is using AI to make the highest-margin advertising machine on the internet more relevant, more efficient and more valuable.

The common thread across all three is that the market is punishing near-term discomfort while the underlying businesses are getting stronger which is the exact kind of mismatch I like buying.

Warren Buffett was asked if Berkshire’s purchase of $AMZN (2019 at $89) was a departure from value investing.

His answer cuts straight to the heart of what value investing actually means:

“The idea that value is somehow connected to book value or low price to earnings ratios or anything, as Charlie has said all investing is value investing. You’re putting out money now to get more later — and making a calculation on the probability of getting it, and when.”

___

Buffett dismantles one of the most common misconceptions in investing. Value investing was never about low price-to-book ratios or cheap multiples. That’s a methodology — not a definition.

The definition is simple: you’re paying a price today for a stream of future cash flows, and you’re asking whether you’re being adequately compensated.

The label “value” vs. “growth” has always been a false dichotomy. All intelligent investing is value investing.

___

🎙️ Berkshire 2019 Annual Meeting | CNBC Warren Buffett Archive (05/04/2019)

@joecarlsonshow The trick with $AMZN is to get interested when you see people complaining about it underperforming the SPY over 2-3 years (when people are focused on the share price and not the business).

The business has been doing incredible the entire time.

𝐌𝐚𝐝𝐫𝐢���, 𝐚 𝐥𝐚 𝐯𝐞𝐧𝐞𝐳𝐨𝐥𝐚𝐧𝐚: 𝐥𝐨 𝐪𝐮𝐞 𝐯𝐢𝐯𝐢𝐦𝐨𝐬 𝐞𝐧 𝐒𝐨𝐥

Hay ciudades que se visitan. Y hay ciudades que, de repente, se convierten en otra cosa.

𝐀𝐲𝐞𝐫, 𝐌𝐚𝐝𝐫𝐢𝐝 𝐟𝐮𝐞 𝐕𝐞𝐧𝐞𝐳𝐮𝐞𝐥𝐚.

Desde que llegué en la mañana a Puerta del Sol, algo ya se movía en el ambiente. Eran apenas las 10:30, los equipos se instalaban, los coordinadores iban y venían, y ya había gente. No mucha, pero suficiente para sentirlo: esa energía conocida que no es ruido ni silencio. 𝐄𝐬 𝐢𝐥𝐮𝐬𝐢𝐨́𝐧.

Horas después, en un encuentro más cercano, ver a @MariaCorinaYA de frente confirma algo: no es solo lo que dice, es cómo está. Cómo se acerca, cómo abraza, cómo se detiene, especialmente con los niños. Lo de los niños no es un detalle menor: los mira distinto, les sonríe distinto, los sostiene como si en ese gesto también estuviera el país que quiere reconstruir.

De ahí salimos con el tiempo justo, cruzando una ciudad que decidió arder bajo un sol implacable. El calor era pesado, incómodo, de esos que agotan antes de llegar. Pero nada preparaba para lo que venía.

Sol no estaba lleno. Estaba desbordado.

No era solo la plaza: eran las calles laterales, los accesos, cada rincón tomado por gente. Se habla de más de 350.000 personas, pero la cifra se queda corta cuando intentas atravesarla. Llegar a nuestro punto fue, literalmente, una odisea. Y aun así, nadie se quejaba.

La gente estaba de pie, bajo un calor insoportable, apretada, muchas veces sin ver bien la tarima. Algunos distinguían una pantalla lejana. Otros, ni eso. Pero ahí estaban. Porque no se trataba de ver, sino de estar.

Había venezolanos de todas partes: Galicia, Valencia, Barcelona, Alicante, Tenerife, Murcia, Madrid. También gente de Italia, Austria, Suecia, Francia. Y, como siempre, cubanos acompañando, entendiendo lo que significa sostener la esperanza cuando parece imposible.

Pero lo más impresionante no era de dónde venían. Era cómo estaban. Caras de emoción, sonrisas con nostalgia, ojos brillando… y otros llenos de lágrimas.

En medio de todo, algo era evidente: no había diferencias. Políticos, periodistas, creadores, gente conocida… daba igual. Todo eso se diluía. Nadie era más que nadie. No había jerarquías ni distancias. No existía el “yo soy” frente al “tú eres”.

Éramos todos lo mismo: venezolanos. Y eso, aunque suene simple, hoy es raro.

También fue un día de encuentros. De esos que no se planean pero importan. Personas que se acercaban a saludar, a dar un beso, a decir “te sigo”, “te leo”, “gracias”. Gente de redes, de lejos, gente que uno reconoce sin haber visto nunca. Me habría gustado detenerme más, hablar con todos, abrazarlos con calma. No fue posible. Era demasiado. Pero queda la sensación de que nos volveremos a encontrar, aquí o donde toque.

𝐘 𝐥𝐥𝐞𝐠𝐨́ 𝐞𝐥 𝐦𝐨𝐦𝐞𝐧𝐭𝐨.

Cuando María Corina sube a la tarima, lo primero que hace no es hablar. Pide espacio, pide a su seguridad que se aparten un poco, porque quiere ver a la gente. A todos. Ese gesto dice más que cualquier consigna.

Después vinieron las palabras. Y con ellas, algo imposible de fingir. La emoción se volvió colectiva. Mirabas a un lado y alguien lloraba. Al otro, también. Hombres, mujeres, jóvenes, mayores. Sin edad, sin filtro. Solo una sensación compartida: estar viviendo algo esperado durante mucho tiempo.

“Vamos a volver”, se repetía. Y por un momento, no sonaba a deseo, sino a certeza.

Eso es lo que cuesta explicar a quien no es venezolano. No sabemos sentir a medias. Somos intensos, cercanos, ruidosos, sí… pero profundamente humanos.

Y ayer, Madrid se vivió así. #𝐀L𝐚V𝐞𝐧𝐞𝐳𝐨𝐥𝐚𝐧𝐚.

Con calor, caos, desorden, abrazos, lágrimas… y también con algo que durante años ha sido difícil sostener: 𝐅𝐄.

Porque, más allá de cifras o discursos, lo que pasó en Sol fue un recordatorio de quiénes somos, de todo lo que hemos resistido y, sobre todo, de que todavía contra todo pronóstico, 𝐬𝐞𝐠𝐮𝐢𝐦𝐨𝐬 𝐜𝐫𝐞𝐲𝐞𝐧𝐝𝐨.

#LosHilosDeMelania

I grew up with parents that at one point owned 7 rental apartments.

I saw first hand how much work they are. It’s the reason I can fix basically any problem in a house, paint, lay concrete, plumbing, h-vac, doors and locks, etc.

If you hire a management company to manage it, your job ends up managing them, and they take 12% of your revenue while nickel and diming your renters. You basically give up all margin in doing so.

Real estate can be a fantastic investment, but it’s also a lot of work, basically a constant part-time job.

I’d much rather buy Meta and Amazon and double my money while not lifting a finger. I’ll let Jassy and Zuck figure out the issues for me.

Based on $BN's own projections, you can see that $BAM and the insurance business are expected to make up a much larger portion of cash flows.

Pretty incredible considering historically, cash flows mostly came from real estate and renewables.

$MELI over the last 5 years:

• Revenue +627%

• Stock Price +5%

The market spent five years compressing the multiple while the business became one of the most dominant commerce and fintech platforms in Latin America.

I went to a steakhouse in Miami, paid the bill, and they automatically added a 20% tip.

When the waiter brought the check, he said: “That tip goes to the whole establishment—if you want to leave something for me, it’s extra.”

I didn’t add anything else—20% is already too much. He gave me a dirty look, like I was robbing him.

This tipping culture is out of control.

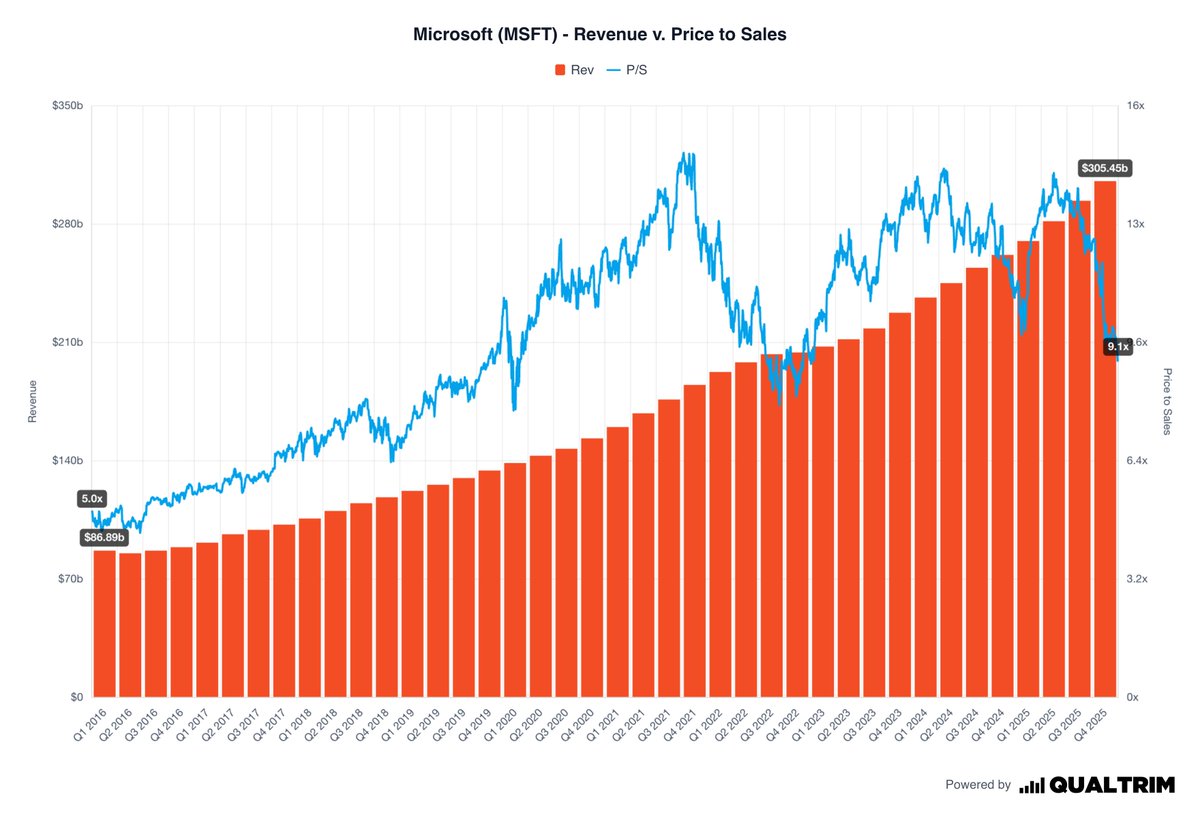

Microsoft is now down -33%.

PEG: 1.50x

Here are 5 Microsoft charts you need to see if you're thinking about buying this stock:

1. $MSFT: Revenue v. P/S ratio

If $META runs a 6-yr depreciation cycle on its $130Bish capex in 2026, then it means this capex needs to generate ~$20B in annual revenue to breakeven.

Meta added $36B in revenue in 2025, and is projecting accelerated growth in Q1 this year.