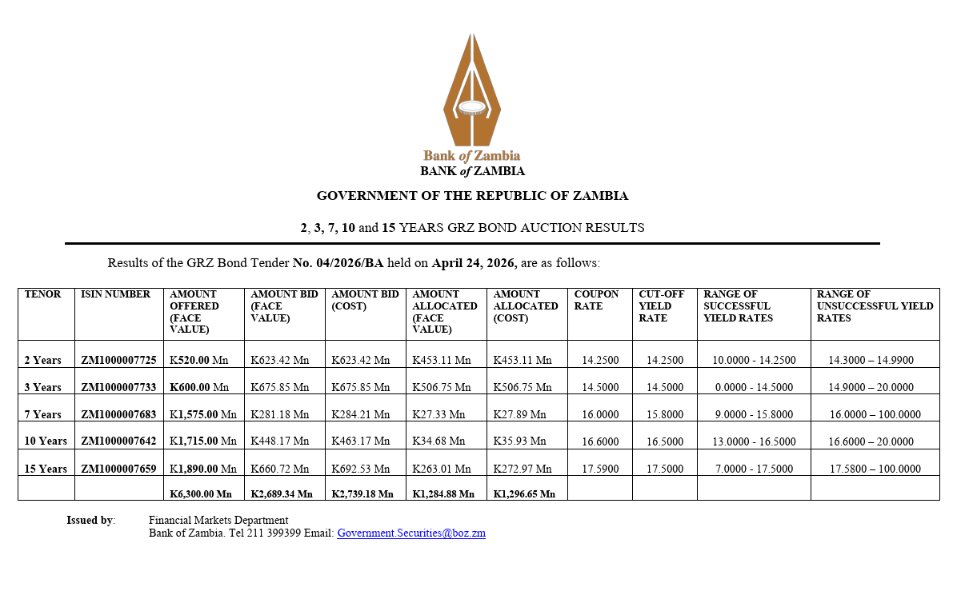

Zambia's April bond auction subscribed at 43 per cent.

GRZ offered ZMW6.3bn. The market bid ZMW2.7bn. Allocated: ZMW1.3bn. The 7-year drew ZMW281m against ZMW1.6bn offered. The long end did not show up.

In January, bids reached ZMW10.1bn. In February, ZMW21.3bn. Bond demand has fallen 87 per cent from the February peak.

The domestic borrowing programme targets ZMW106bn from securities this year. At end-Q1, ZMW75.8bn remained across nine months. April net financing so far, across two T-bill auctions and one bond auction, stands at approximately ZMW4.1bn against a required monthly run-rate of ZMW8.8bn. The shortfall is approximately ZMW4.8bn with one T-bill auction remaining, but T-bills offer just ZMW2.2bn per auction and are operating inside a corridor trap where three of four tenors offer insufficient compensation relative to the overnight interbank deposit floor.

The fiscal balance is already under pressure. Through February, the deficit reached K7.8bn against a full-year budget of K19.4bn. That is 40 per cent of the annual target consumed in two months. January alone ran K8.5bn, more than a quarter of the full-year allowance. February clawed back a small surplus of K674m, but only because expenditure pulled back sharply. Revenue underperformed in both months, with VAT 35 per cent below target through February, domestic VAT 78 per cent below in February alone, and grants effectively zero against a full-year budget of K12.1bn.

The fuel tax suspension costs ZMW3.3bn to ZMW4.6bn over its official three-month window. Pump prices are unlikely to rise ahead of the August election, extending the realistic window to six months and the fiscal cost to ZMW6.3bn to ZMW9.2bn. The 70 newly created constituencies, announced on 16 April and effective 15 May, will add to expenditure pressure. The fiscal cost of additional CDF allocations, staffing, and infrastructure has not yet been publicly quantified. Election-related spending more broadly is likely to intensify in the run-up to August.

Both April and May are light on bond maturities. Per Reuters, June carries ZMW14.6bn in total maturities, of which ZMW8.3bn in bonds. June's recycled cash should help, but the June auction now carries the weight of whatever April could not deliver, particularly because there is no bond auction in May.

We advised after the strong January and February auctions that it was early innings and that the half-year to June was the real test. Scaling the refinancing wall while securing strong fiscal performance required several things to align, with limited buffers for shocks. The shocks arrived. Yesterday's result confirmed the concern.

For the full analytical framework, see The 2026 Refinancing Wall, Domestic Market Absorption, Copper Output and the 2026 Royalty Arithmetic, Growth Without Diffusion, A Little Here a Little There, The Acid Test, and The Forecast Is Not the Evidence at Canary Compass.

A Norse flight departing from Harry Reid International at just the right angle, and let’s just say, the Sphere wasn’t too impressed about being woken up.

📸: @life.on.the.ramp

Your annual reminder of just how *ridiculous* Chelsea’s defence was in the 2004/05 season 😱

Bryan Mbeumo’s equaliser for Man Utd against Arsenal means Chelsea’s record of conceding only 15 goals in a single campaign can’t be beaten for another season!

Zambia’s 5.2B Dollar Reserves Milestone:

A Win Worth Celebrating, While We Stay Honest About The Road Ahead 🇿🇲 💪🏾

This started as a simple conversion with a friend (@OwenSichilima) on whether the headline reserves story is as strong as it sounds. Let me share where that conversation went.

First, the win. Zambia’s gross international reserves now stand at about $5.2 billion as at end September 2025, the highest level ever recorded and roughly 5.2 months of import cover. BoZ shows this is up from about $4.7 billion at end June.

At the same time, preliminary data show the current account moved from a deficit of about $0.5 billion dollars in Q2 to a small surplus of about $0.03 billion in Q3, around 0.4% of GDP. Exports grew faster than imports, helped by higher copper earnings and non-traditional exports like maize, electrical cables, cement and gemstones.

On the rating side, the story is just as clear. On 21 November, S&P moved Zambia from Selective Default to CCC+ with a stable outlook. On 28 November, Fitch moved us from Restricted Default to B- with a stable outlook. After almost 5 years in default territory, we are back in the B family. Around $12.7 billion of the roughly $13.5 billion external debt in scope has now been treated or agreed in principle, close to 94% coverage.

So yes, there is something real to celebrate here. Debt restructuring, fiscal adjustment and tighter monetary policy have rebuilt buffers and restored credibility. That lowers the fear premium, improves access for syndications in mining, energy and infrastructure, and gives the private sector a better starting point. Positivity matters because it feeds into spreads and behaviour.

Now for the part where people say, “Here comes Dean the party pooper.” 😅

The point is not to pour cold water. It is to explain what sits behind the $5.2 billion so that we keep our optimism honest.

Gross International Reserves (GIR) are the full stock of qualifying foreign assets on the BoZ balance sheet. They support the currency, help pay external obligations and provide a buffer against shocks. On that measure, $5.2 billion is historic and good for sentiment.

Net International Reserves (NIR) are tougher. NIR takes that same pool, then subtracts short-term foreign currency liabilities, IMF credits and other restricted balances, including required foreign currency reserves that commercial banks must hold. In plain language, NIR is the part of reserves you can use in a crisis without immediately creating another problem.

Why does that distinction matter?

Because gross reserves can grow in 2 very different ways:

1. Through foreign exchange earned surpluses. Exports and services outpacing imports and income payments, giving you a positive current account and a healthier overall balance of payments.

2. Through programme disbursements, project loans, changes in statutory reserve requirements and other liability-linked flows that lift the headline stock today but carry obligations tomorrow.

Both routes show up in the gross number. Only the first really deepens resilience.

If you read the BoZ November presentation closely, they are very clear on what drove the jump from about 4.7 billion to about 5.2 billion dollars in quarter 3. The build up mainly came from:

a) IMF ECF disbursement of about $191 million

b) Project related receipts

c) Net increases in foreign currency statutory reserve deposits

d) BoZ purchases of foreign exchange (mining-tax-related)

e) Interest earnings on reserves

f) Gold purchases of about 186.6 kilograms (worth $21.5 million), taking total holdings to just over 3,051.3 kilograms

None of that is a problem. In fact, this is exactly how an IMF supported programme is designed. You take pain on the fiscal and monetary side, and in return official flows and projects help rebuild buffers while you repair the plumbing of the economy.

The nuance is simple. We are not yet looking at a story that is fully driven by clean export surpluses. Fitch itself still expects a current account deficit of around 2% of GDP in 2025, only moving to small surpluses from 2026 onward as reforms deepen. At the same time, the IMF Fifth Review shows that by end March 2025 Zambia had already missed the NIR indicative target by around $65 million, together with indicative targets on non-mining revenue and arrears clearance, largely because BoZ had to sell more foreign exchange for energy imports and to avoid disorderly currency moves.

So the picture today looks like this.

Gross reserves are at a record high and now backed by an improving current account after a difficult first half. Part of the Q3 build up reflects real strength in exports and reduced profit outflows. Another part is mechanical and liability-linked, coming from programme money, project flows and higher foreign currency reserve requirements (FCY deposits increased to $4.23 billion at the end of Q3 from $4.04bn at the end of Q2, increasing GIR by around $48.5 million).

That does not cancel the progress. It simply tells you what kind of progress it is.

Liability-linked reserves are not free. You can use them to defend the currency or pay import bills, but then you have to think hard about what happens when:

a) The loans that boosted reserves fall due

b) The statutory reserve framework changes

c) Project owners start to draw down their balances

d) Programme disbursements slow or stop

If you have already spent those balances, you meet the next shock with thinner buffers. That is why NIR is monitored separately, and why central banks (internally) and the IMF place weight on it.

So where do I land.

First truth. Zambia has earned this celebration. The exit from default, the rating upgrades and the record gross reserves are not public relations theatre. They reflect real work by technocrats and policy makers who have taken difficult decisions under pressure. People are right to feel encouraged. Confidence changes behaviour and, over time, lowers our risk premium.

Second truth. The window is still fragile. A meaningful share of the reserves story remains liability-driven. Net usable reserves and the deeper external position need to catch up with the headline. Dedollarisation, and deeper export diversification are still projects in front of us, not achievements behind us.

Some will still call that party pooping. I see it differently.

I want the party. I want people to feel that Zambia is rising, because belief does shape outcomes. I also want everyone to get home. Vibes are allowed. Structure is non-negotiable.

So we celebrate the $5.2 billion as a genuine milestone.

Then we get back to work and make sure that the next time we cheer a record reserves level, it is driven much more by organic surpluses in goods, services and income, and much less by programme flows, projects and statutory mechanics.

That is the road from borrowed buffers to earned buffers.

Structure before sentiment.

I run every day for 30 minutes, if I miss a day I add 30 minutes to the next day.

This has truly been a game changer, tomorrow I’m supposed to run for 3 weeks.