It’s not rocket science why $TSLA +28% in the last week vs NDX +4%: 1/ Elon’s all-hands meeting was a big success, with Elon conveying vision, confidence, energy, and calm to the troops; 2/ It’s clear from credit card data that TSLA orders (and specifically deposits) have not been impacted by Elon’s politics and DOGE activities, despite what MSM says; 3/ China TSLA weekly insured registrations have had two strong back-to-back weeks (YTD highs), and TSLA China 1Q registrations are now just -0.6% behind last year’s 1Q; 4/ The gorgeous new Model Y is ramping production quickly, which should lead to UPWARD FY ‘25 delivery revisions as we start 2Q (now 1,903K +1.6% YoY; was 2,078K +10.6% YoY at Y.E.).

In today’s pre-mkt summary for Subscribers: $TSLA China weekly insured registrations hit 17.3K, a YTD high as refreshed Model Y production ramps higher; TSLA Europe Feb sales decline of -47% not relevant given severely limited Model Y inventory as TSLA changes over to new Model Y Juniper version; Trump invents a new economic weapon called secondary tariffs to punish any country that buys oil from Venezuela.

$TSLA sales in Europe declined by -47% during February, a second straight month of declines, due mainly to the absence of new Model Y inventory as TSLA changed over its best selling CUV to the Model Y Juniper. In China TSLA weekly insured registrations were 17.3K for the week of Mar 17-23, a new YTD high as refreshed Model Y production continued to ramp higher.

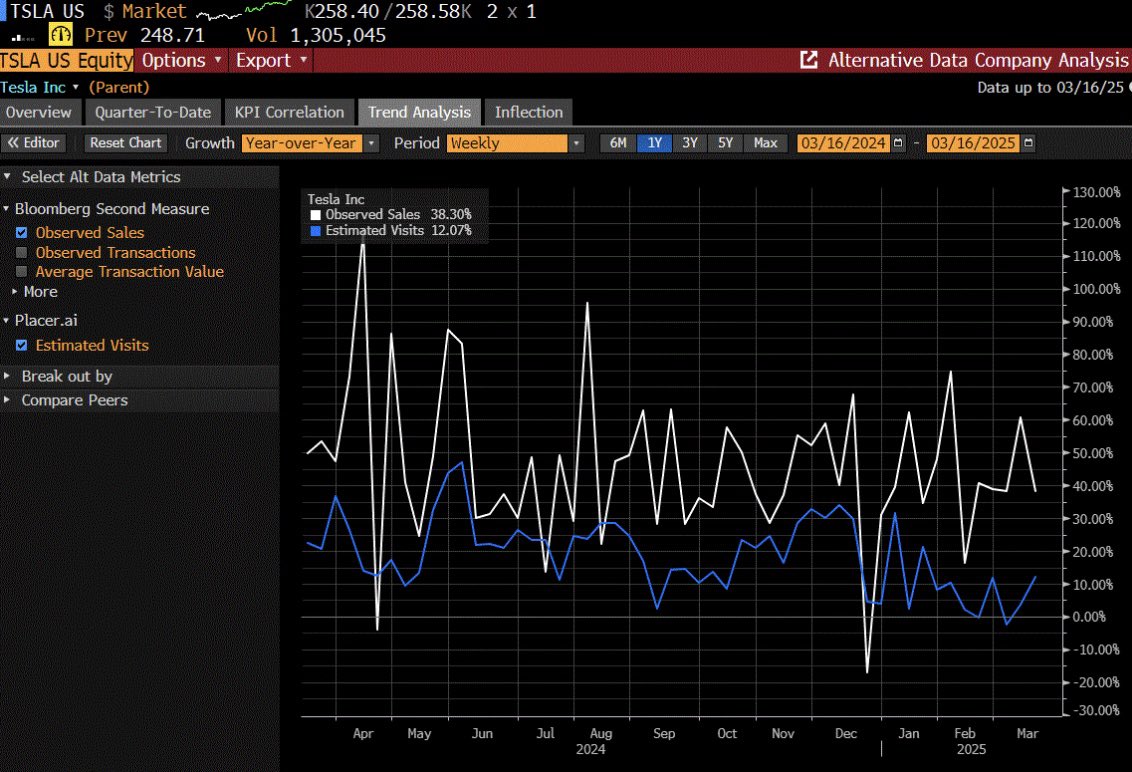

The sharp drop off in TSLA 1Q delivery ests that has pummeled TSLA shares so far in 2025 (TSLA -31%, NDX -4% YTD) is highly likely due to the changeover of the new Model Y Juniper and customers waiting for the new model rather than Elon’s political rhetoric and DOGE actions. In the U.S., third-party U.S. credit card data sourced from Bloomberg shows that weekly YoY orders through 3/16 have not changed much from a quarter earlier and daily orders through 3/16 are actually trending higher. Model 3 shipments are steady YoY even after normalizing for last year’s 1Q shipments by using the average over the year for the 2024/1Q period.

$TSLA China reported 17,400 insurad registrations for the week of Mar 17-23. This was the highest week so far this year, and included ~10,600 refreshed Model Y. As new Model Y production ramps up, overall China sales continue to stabilize. Through week 12, 1Q is -0.6% YoY and -34.5% QoQ. Sources: @piloly@Tslachan

$TSLA +10.5% today (vs NDX +2.2%) as investors starting to realize the decline in 1Q deliv estimates (from 459K on 1/1 to 400K today) are more due to lack of inventory of new refreshed Model Y than Elon’s political rhetoric and DOGE actions. From third party credit card data, we see that orders and specifically deposits don’t seem to be impacted by Tesla’s bad PR. Also, 1Q Model 3 delivs have so far been stable YoY.

With the refreshed Model Y supply shortage now easing, we should see a corresponding increase in TSLA 2Q deliv estimates over the next few weeks. We also believe tonight’s Chinese weekly insured registrations could top last week’s YTD high of 15.3K.

That said, it would be naive for us to argue that Elon Musk’s political rhetoric and actions have no impact on TSLA demand. Democrats are 2.5x as likely to buy an EV as Republicans, and when Elon backs a conservative political cause (e.g. endorses AfD party candidate in Germany) it’s going to impact TSLA demand given that Dems way overindex EV purchases.

A CEO’s job is to inspire their troops to greatness.

Jack Welch, former CEO of General Electric, emphasized that a leader’s role is to inspire and energize people, famously saying, “Good business leaders create a vision, articulate the vision, passionately own the vision, and relentlessly drive it to completion.” The idea of rallying "the troops" to achieve extraordinary results is a common thread in his speeches.

Based on that criteria, @elonmusk is a great CEO for $TSLA.

In today’s pre-mkt summary: President Trump shifts narrative to “targeted” tariffs; update on estimated TSLA deposits based on weekly and daily Bloomberg credit card data; why $TSLA continues to rally off its 3/10 bottom of $222.

Using $TSLA EV, energy and services profits alone one can justify $250/share in TSLA valuation (2030 Adj EPS $10.60 x 50x P/E = $530, discount back at 14.8% cost of equity (4% risk free rate, 6% equity risk premium, 1.8x TSLA beta = 14.8%) equals $250 ($530 / 1.148^5 = $265). So market is effectively putting zero value on robotaxi. Why do you think that is?

For those who have never managed a PR department before please see @GaryAndThe62949 ‘s recent post and understand that PR has a dual mandate: 1/ To hold media accountable through fact checking and 2/ To proactively shape overall perception and tell Tesla's story. https://t.co/lqpYpBscc2

Ultimately, the goal of PR is to maximize share of voice and the % of positive vs total stories about $TSLA. Today consumers hear one voice and it belongs to TSLA’s competitors (GM, F, VOW) setting the narrative through MSM because TSLA’s voice is nowhere to be found. If MSM is biased against TSLA, blame TSLA for not fielding a team.

$TSLA still not showing much degradation in order flow despite the recent spate of bad PR. Third party credit card data sourced from Bloomberg shows that daily YoY orders through 3/13 have not changed much from a quarter earlier and weekly orders through 3/9 are actually higher. While true that consumers pay cash (or finance with loans) to take delivery of new Teslas, credit cards are commonly used for the down payments.

Model 3 shipments still seem steady YoY even after normalizing for last year’s 1Q shipments by using the average over the year for the 2024/1Q period. If brand damage was severe as the MSM implies, wouldn’t Model 3 deliveries show deterioration? Our thesis remains that the drop off in TSLA 1Q YoY deliveries is due to limited Model Y inventories, which has caused buyers to delay taking deliveries until the new refreshed ModelY is available. We normalize M-3 shipments for last year’s 1Q because 2024/1Q M-3 shipments were low due to the M-3 Highland transition that started in China and Europe in 2023 4Q and impacted U.S. M-3 delivs in 2024 1Q.

Finally, TSLA China insured registrations show just a -4% 1Q YoY decline through 3/16, despite limited refreshed Model Y inventory in China and customers waiting for the updated version. We will get new TSLA China weekly registrations data through 3/23 on Monday night. We expect a weekly registrations of 16-18K after a quarterly best 15.3K registrations last week.

$TSLA now up +4% in a down market following last night’s @elonmusk X live stream to TSLA employees. Investors roundly cheered Elon’s vision, confidence, spirit, and calmness in praising employees for their efforts during the current media storm.

From my Subscribers’ feed last night:

In Musk’s speech to employees, he covered a myriad of topics: Model Y this year will repeat last year’s accomplishment of being the world's best-selling vehicle. He talked of significant improvements in FSD unsupervised autonomy and his vision that FSD will be ultimately 10 times safer than a human driver.

Musk painted a vision of a future he called sustainable abundance, which is likely to become TSLA’s mission statement. “A future where you can have any good or service you want at will.” He reiterated that TSLA would build 5,000 Optimus humanoid robots this year; and 50,000 in 2026, and increasing 10x per year after that. He said that Optimus will be the biggest product of all time by far: “10 times bigger than the next biggest product ever made.” He insisted that Tesla is the only company that can build intelligent humanoid robots at scale.

Elon told employees to "hang onto their stock" and empathized what it must feel like to be a Tesla employee: “If you read the news, it feels like Armageddon. I can't walk past a TV without seeing a Tesla on fire…. I understand if you don't want to buy our product, but you don't have to burn it down, that's a bit unreasonable.” Musk painted a picture of Tesla as the company of choice for people to work for, with lots of opportunity for upward mobility. He ended with “One thing is for sure - the future is going to be very interesting."

We continue to believe $TSLA bottomed last Monday at $222, and will move higher once Elon gives up his DOGE responsibilities and returns as TSLA CEO full-time. Other positive catalysts include the continued ramp of refreshed Model Y, the new $25K-30K EV due out at end of 2Q, and Austin unsupervised autonomy test market in 3Q. We believe the reduction of 1Q deliv ests (now 400K vs 468K at year-end) is fully discounted in TSLA’s stock price.

In today’s pre-mkt summary for Subscribers: Elon’s $TSLA employee update streamed live last night on X; $FDX and $NKE both gave downbeat guidance with earnings, adding to the uncertainty of Trump’s trade war, with reciprocal tariffs set to go into effect April 2; expect additional volatility today in the form of so-called triple witching, with simultaneous expiration of three types of derivatives contracts — stock options, stock index futures, and stock index options — all on the same day. This event occurs four times a year, on the third Friday of March, June, September, and December.

$NKE -4.6% AH (no position) after giving a dismal 4Q outlook as new CEO Elliott Hill reset revenue and gross margin expectations lower while re-focusing Nike’s marketing message on the athlete.

3Q actuals:

- Rev $11.27B (-9% YoY) vs $11.03B (-11% YoY) est

- Gross margin 41.5% vs 41.9% est

- EPS $.54 vs $.28 est

- Repurchased just $499M shares vs $1,050M avg over the past 4 qtrs.

4Q guidance:

- Revs mid-teens decline vs -12% exp

- Gross margin -400bp to -500bp vs -340bp exp

FY’26 (starts June 2025):

- Same 4Q headwinds continuing into FY’26 (vs WS rev 0% est growth, gross margins expected to grow 80bp in FY’26)

- Digital traffic double digit declines vs direct to consumer rev growth -1.5% exp

$TSLA brand may be tainted until unsupervised autonomy goes live, given lack of PR to change the narrative. In the end, the best product will win. Refreshed Model Y production ramp should boost TSLA brand equity - understated and gorgeous, 327 mile range, superior technology, great value for the money. Cybertruck brand may be history given its impossible-to-miss presence and an obvious target for haters. @elonmusk needs to finish at DOGE and return to TSLA.

Top question I’m getting: Why does the $TSLA brand even matter if TSLA’s valuation is more about robotaxi and humanoid robots than Tesla EVs?

No disrespect but TSLA is in the business of selling EVs, unsupervised autonomy, and ultimately humanoid robots to consumers. Brand is critical to consumers’ trust, and if Elon’s political rhetoric and DOGE activities are hurting that brand and leading to acts of hate against owners of Tesla vehicles and stores, Elon (and Trump) need to formulate a plan to stop the hatred to protect the current EV brand. Second, TSLA needs to invest in the marketing skills needed to sell unsupervised autonomy and humanoid robots in the future.

As of 2024 4Q, 81% of TSLA profits came from the EV business, with just 2% of that 81% from FSD purchase and rentals. By 2030, assuming a 25% take rate, we estimate 78% of TSLA profits from EVs with 10% from FSD purchase and rentals. So persuading and delighting consumers is as critical as manufacturing and operational expertise.

You are joking right? $TSLA recall costs are one-time costs and rounding error to the P&L. Even if the cost to fix was $500 per, that’s a one-time EPS hit of <$.01/share.

In my pre-mkt summary for Subscribers: Fed holds rates steady; new dot plot indicates 2 rate cuts this year totaling 50bp, and signals decelerating economic growth and modestly higher inflation; $TSLA data shows M-3 1Q delivs stable and no degradation in credit card orders for Tesla despite brand taint, suggesting limited new refreshed M-Y availability was bigger factor in reduced TSLA 1Q delivery estimates.