@star_okx ,Hi Star, for your information of our finding about Biance Platform system Failure on Oct.11.

Oct.11 Erroneous Liquidation Caused by Binance Platform System Failure Key Facts and Chronology Platform-Designated Anomaly Period: In a post-incident announcement, Biance identified the period from 05:36 to 06:16 Beijing Time on October 11, 2025, during which losses occurred due to specific collateral de-pegging, as "abnormal" and initiated a full compensation program.

Five-Pronged Technical Evidence Chain demonstrating Biance's System Failure

First Failure: Source Price Index Distortion During the "10.11 Event," the proportion of cryptocurrencies on Binance whose prices were more than 10% below the lowest prices on other exchanges was as high as 43%. In contrast, during the "5.19 Event," this figure was only 18.1%. Furthermore, the proportion of cryptocurrencies whose prices on Binance were more than 100% below the lowest prices on other exchanges reached 13% (involving 31 tokens) in the "10.11 Event." In the "5.19 Event," this extreme discrepancy was only 1.4%, involving just one token.

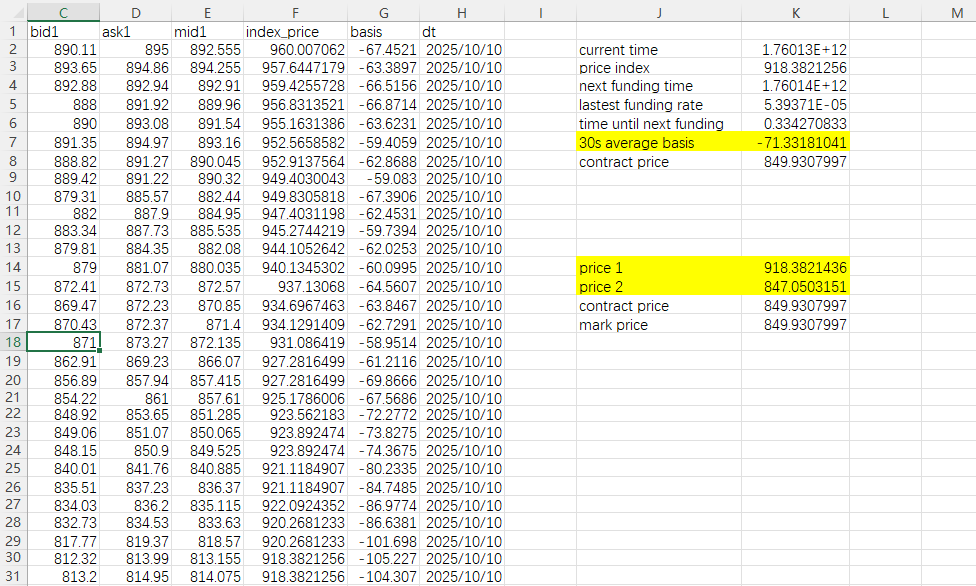

Second Failure: Risk Control Mechanism's Non-Response to Clear Alarms a.Many cases extreme negative funding (basis): The 30-second average basis corresponding to a relative basis rate of is less -10%. b. In financial derivatives markets, such a large and sustained negative basis rate is a definitive signal of completely paralyzed liquidity and price discovery mechanisms in the contract market, constituting a clear risk control alarm. c. Biance risk control system failed to initiate any circuit breaker, protective measures, or switch to an emergency pricing mode in response to this alarm. The system design contained a fatal flaw in its response to "isolated extreme basis rate anomalies."

Third Failure: Corroborating Evidence from Biance Own Risk Control Standards a. According to the Biance’s official rules, it has a deviation circuit breaker mechanism for single price source data: when a price deviates from the median price by more than 3%, the system forcibly intervenes, restricting that data to within ±3% of the median price b. This rule, established as an official standard, defines a 3% price deviation as an "abnormal" state requiring immediate intervention by its own technical system. c. In more than 43% cases, Binance's own spot price was significantly deviated, being more than 10% lower than the lowest price of other exchanges. Simultaneously, many cases "Basis Rate"—core to derivatives pricing—reached -10%, which is 3.3 times the aforementioned 3% spot deviation circuit breaker threshold. If even a 3% spot deviation necessitates forced correction, then a 10% funding basis rate anomaly should more strongly be judged as a severe failure of the overall market pricing mechanism. Yet, the system took no action.

Fourth Failure: Post-Incident Rule Amendment as Evidence of Pre-Existing Risk Control Deficiencies a.We discovered that Biance has established a 1% deviation upper limit for BNB and few others on its official pages. The documented update date for this rule is November 28, 2025, which is after the occurrence of this case b. This timeline indicates that Biance, after this incident, urgently introduced an extremely strict (1%) deviation control rule specifically for BNB and BTC,ETH. This action has a clear "patch" nature, allowing a reasonable inference that its purpose was to prevent the recurrence of similar incidents. c. This post-hoc amendment strongly and conversely proves that on the day of the incident, for key assets like BNB, there was a lack of clear, effective risk control protection, or the existing rule thresholds were extremely unreasonable. Our loss occurred during a period of system vulnerability that Biance itself acknowledged required significantly enhanced risk control standards.

Fifth Failure: Erroneous Decision Output Based on Failed Data ("Garbage In, Garbage Out") a. Synthesizing points above, the operational state of Binance's Mark Price system at 10.11 can be summarized as "garbage in, garbage out": Core input data such as the "Price Index" and the "Funding Basis Rate" (-10% even worsre) received by the system were already severely distorted and had lost their market-representative function. b. The system ignored the comprehensive failure of the input data and mechanically executed the preset "middle-of-three-prices" formula, thereby outputting a Mark Price that was procedurally "compliant" but substantively completely distorted. c. Biance then used this Mark Price—calculated based on invalid premises—as the binding "fair price" to determine A lot of investors’ position ware insolvent and to execute the liquidation. The entire logical foundation of the liquidation operation was erroneous from the outset.

Summary of Core Legal Arguments Nature of Liability: Our losses did not originate from voluntarily assumed market volatility risk but ware directly caused by Biance’s failure to provide the basic guarantee of system reliability. Biance has an obligation to ensure its core pricing and risk control systems maintain functionality or safely trigger circuit breakers under extreme stress. 11. Direct Causation: The distorted Price Index and the extreme funding rate signaling market failure were the joint and necessary causes of the erroneous liquidation. Without this system failure, the liquidation would not have been triggered. Evidence from Biance Own Logic and Actions: a. Biance provision of full compensation for losses occurring after 05:36 is self-evidence that it recognizes the principle that losses caused by internal platform abnormal states should be borne by the platform. b. Biance post-incident establishment of a 1% deviation upper limit rule for BNB/btc/eth further acknowledges, conversely, the lack of risk control protection at the time of the incident. Many cases occurred at an earlier moment and is an earlier manifestation of the same system failure event, sharing the same nature of responsibility.

10月11日因币安平台系统故障导致的错误清算 关键事实与时间线 平台认定的异常时期:币安在事后公告中,将2025年10月11日北京时间05:36至06:16期间,因特定抵押品脱锚而发生损失的时间段定性为"异常",并启动了全额补偿方案。 证明币安系统故障的五重技术证据链

第一重故障:源价格指数扭曲 在"10.11事件"中,币安上价格低于其他交易所最低价超过10%的加密货币比例高达43%。相比之下,在"5.19事件"中,该比例仅为18.1%。 此外,在"10.11事件"中,币安上价格低于其他交易所最低价超过100%的加密货币比例达到了13%(涉及31个代币)。而在"5.19事件"中,如此极端的偏差仅为1.4%,仅涉及一个代币。

第二重故障:风控机制对明确警报无响应 a. 出现多例极端负资金费率:相对资金费率对应的30秒平均基差低于-10%。 b. 在金融衍生品市场中,如此巨大且持续的负资金费率是合约市场流动性及价格发现机制完全瘫痪的确切信号,构成明确的风控警报。 c. 币安风控系统对此警报未能启动任何熔断、保护措施或切换至紧急定价模式。系统设计在对"孤立的极端资金费率异常"的响应上存在致命缺陷。

第三重故障:币安自身风控标准提供的佐证 a. 根据币安官方规则,其对单一价格源数据设有偏差熔断机制:当某价格偏离中位数价格超过3%时,系统强制干预,将该数据限制在不超过中位数价格的±3%范围内。 b. 这一作为官方标准确立的规则,将3%的价格偏差定义为需要其自身技术系统立即干预的"异常"状态。 c. 而在超过43%的案例中,币安自身现货价格已严重偏差,低于其他交易所最低价超过10%。同时,多个案例中作为衍生品定价核心的"资金费率"达到了-10%,是上述3%现货偏差熔断阈值的3.3倍。若连3%的现货偏差都需强制修正,那么10%的资金费率异常更应该被判定为整体市场定价机制的严重失效。然而,系统未采取任何行动。

第四重故障:事后修改规则作为事前风控缺陷的证据 a. 我们发现,币安在其官方页面上为BNB等少数资产设定了1%的偏差上限。该规则记载的更新日期为2025年11月28日,是在本案发生之后。 b. 这一时间线表明,币安是在本次事件后,紧急为BNB、BTC、ETH等资产引入了极其严格(1%)的偏差控制规则。此举具有明显的"补丁"性质,可合理推断其目的是为防止类似事件再次发生。 c. 这种事后修正强烈且反向地证明了,在事发当日,对于BNB等关键资产,缺乏明确有效的风控保护,或现有规则阈值极不合理。我们的损失正发生在币安自身也承认需大幅加强风控标准的系统漏洞时期。

第五重故障:基于失效数据的错误决策输出("垃圾进,垃圾出") a. 综合以上几点,10.11事件中币安标记价格系统的运行状态可概括为"垃圾进,垃圾出":系统接收的"价格指数"、"资金费率"(-10%甚至更差)等核心输入数据已严重失真,丧失了市场代表性功能。 b. 系统无视输入数据的全面失效,机械地执行预设的"三价取中"公式,从而输出了一个程序上"合规"但实质上完全失真的标记价格。 c. 币安随后将这一基于无效前提计算出的标记价格,作为具有约束力的"公允价格",用以判定大量投资者的仓位已资不抵债并执行强平。整个强平操作的逻辑基础从一开始就是错误的。

核心法律论点摘要 责任性质:我们的损失并非源于自愿承担的市场波动风险,而是直接由币安未能提供系统可靠性的基本保障所导致。币安有义务确保其核心定价和风控系统在极端压力下保持功能或安全触发熔断。 直接因果关系:扭曲的价格指数和预示市场失效的极端资金费率,共同构成了错误强平的必要原因。若无此系统故障,强平不会被触发。 币安自身逻辑与行动提供的证据: a. 币安对05:36后发生的损失提供全额补偿,这本身就证明其认可因平台内部异常状态造成的损失应由平台承担的原则。 b. 币安事后为BNB/BTC/ETH设立1%偏差上限规则,进一步从反面承认了事发当时风险控制保护的缺失。众多案例发生得更早,是同一系统失效事件的更早表现,责任性质相同

@cz_binance@heyibinance@xiaomucrypto@hebi555@denny_x09118

@leonisdasnft

Oct.11 Erroneous Liquidation Caused by Binance Platform System Failure

Key Facts and Chronology

Platform-Designated Anomaly Period: In a post-incident announcement, Biance identified the period from 05:36 to 06:16 Beijing Time on October 11, 2025, during which losses occurred due to specific collateral de-pegging, as "abnormal" and initiated a full compensation program.

Five-Pronged Technical Evidence Chain Demonstrating Biance's System Failure

First Failure: Source Price Index Distortion

During the "10.11 Event," the proportion of cryptocurrencies on Binance whose prices were more than 10% below the lowest prices on other exchanges was as high as 43%. In contrast, during the "5.19 Event," this figure was only 18.1%.

Furthermore, the proportion of cryptocurrencies whose prices on Binance were more than 100% below the lowest prices on other exchanges reached 13% (involving 31 tokens) in the "10.11 Event." In the "5.19 Event," this extreme discrepancy was only 1.4%, involving just one token.

Second Failure: Risk Control Mechanism's Non-Response to Clear Alarms

a.Many cases extreme negative funding (basis): The 30-second average basis corresponding to a relative basis rate of is less -10%.

b. In financial derivatives markets, such a large and sustained negative basis rate is a definitive signal of completely paralyzed liquidity and price discovery mechanisms in the contract market, constituting a clear risk control alarm.

c. Biance risk control system failed to initiate any circuit breaker, protective measures, or switch to an emergency pricing mode in response to this alarm. The system design contained a fatal flaw in its response to "isolated extreme basis rate anomalies."

Third Failure: Corroborating Evidence from Biance Own Risk Control Standards

a. According to the Biance’s official rules, it has a deviation circuit breaker mechanism for single price source data: when a price deviates from the median price by more than 3%, the system forcibly intervenes, restricting that data to within ±3% of the median price b. This rule, established as an official standard, defines a 3% price deviation as an "abnormal" state requiring immediate intervention by its own technical system.

c. In more than 43% cases, Binance's own spot price was significantly deviated, being more than 10% lower than the lowest price of other exchanges. Simultaneously, many cases "Basis Rate"—core to derivatives pricing—reached -10%, which is 3.3 times the aforementioned 3% spot deviation circuit breaker threshold. If even a 3% spot deviation necessitates forced correction, then a 10% funding basis rate anomaly should more strongly be judged as a severe failure of the overall market pricing mechanism. Yet, the system took no action.

Fourth Failure: Post-Incident Rule Amendment as Evidence of Pre-Existing Risk Control Deficiencies

a.We discovered that Biance has established a 1% deviation upper limit for BNB and few others on its official pages. The documented update date for this rule is November 28, 2025, which is after the occurrence of this case

b. This timeline indicates that Biance, after this incident, urgently introduced an extremely strict (1%) deviation control rule specifically for BNB and BTC,ETH. This action has a clear "patch" nature, allowing a reasonable inference that its purpose was to prevent the recurrence of similar incidents.

c. This post-hoc amendment strongly and conversely proves that on the day of the incident, for key assets like BNB, there was a lack of clear, effective risk control protection, or the existing rule thresholds were extremely unreasonable. Our loss occurred during a period of system vulnerability that Biance itself acknowledged required significantly enhanced risk control standards.

9. Fifth Failure: Erroneous Decision Output Based on Failed Data ("Garbage In, Garbage Out")

a. Synthesizing points above, the operational state of Binance's Mark Price system at 10.11 can be summarized as "garbage in, garbage out": Core input data such as the "Price Index" and the "Funding Basis Rate" (-10% even worsre) received by the system were already severely distorted and had lost their market-representative function.

b. The system ignored the comprehensive failure of the input data and mechanically executed the preset "middle-of-three-prices" formula, thereby outputting a Mark Price that was procedurally "compliant" but substantively completely distorted.

c. Biance then used this Mark Price—calculated based on invalid premises—as the binding "fair price" to determine A lot of investors’ position ware insolvent and to execute the liquidation. The entire logical foundation of the liquidation operation was erroneous from the outset.

Summary of Core Legal Arguments

Nature of Liability: Our losses did not originate from voluntarily assumed market volatility risk but ware directly caused by Biance’s failure to provide the basic guarantee of system reliability. Biance has an obligation to ensure its core pricing and risk control systems maintain functionality or safely trigger circuit breakers under extreme stress.

11. Direct Causation: The distorted Price Index and the extreme funding rate signaling market failure were the joint and necessary causes of the erroneous liquidation. Without this system failure, the liquidation would not have been triggered.

Evidence from Biance Own Logic and Actions:

a. Biance provision of full compensation for losses occurring after 05:36 is self-evidence that it recognizes the principle that losses caused by internal platform abnormal states should be borne by the platform.

b. Biance post-incident establishment of a 1% deviation upper limit rule for BNB/btc/eth further acknowledges, conversely, the lack of risk control protection at the time of the incident. Many cases occurred at an earlier moment and is an earlier manifestation of the same system failure event, sharing the same nature of responsibility.

10月11日因币安平台系统故障导致的错误清算

关键事实与时间线

平台认定的异常时期:币安在事后公告中,将2025年10月11日北京时间05:36至06:16期间,因特定抵押品脱锚而发生损失的时间段定性为"异常",并启动了全额补偿方案。

证明币安系统故障的五重技术证据链

第一重故障:源价格指数扭曲

在"10.11事件"中,币安上价格低于其他交易所最低价超过10%的加密货币比例高达43%。相比之下,在"5.19事件"中,该比例仅为18.1%。

此外,在"10.11事件"中,币安上价格低于其他交易所最低价超过100%的加密货币比例达到了13%(涉及31个代币)。而在"5.19事件"中,如此极端的偏差仅为1.4%,仅涉及一个代币。

第二重故障:风控机制对明确警报无响应

a. 出现多例极端负资金费率:相对资金费率对应的30秒平均基差低于-10%。

b. 在金融衍生品市场中,如此巨大且持续的负资金费率是合约市场流动性及价格发现机制完全瘫痪的确切信号,构成明确的风控警报。

c. 币安风控系统对此警报未能启动任何熔断、保护措施或切换至紧急定价模式。系统设计在对"孤立的极端资金费率异常"的响应上存在致命缺陷。

第三重故障:币安自身风控标准提供的佐证

a. 根据币安官方规则,其对单一价格源数据设有偏差熔断机制:当某价格偏离中位数价格超过3%时,系统强制干预,将该数据限制在不超过中位数价格的±3%范围内。

b. 这一作为官方标准确立的规则,将3%的价格偏差定义为需要其自身技术系统立即干预的"异常"状态。

c. 而在超过43%的案例中,币安自身现货价格已严重偏差,低于其他交易所最低价超过10%。同时,多个案例中作为衍生品定价核心的"资金费率"达到了-10%,是上述3%现货偏差熔断阈值的3.3倍。若连3%的现货偏差都需强制修正,那么10%的资金费率异常更应该被判定为整体市场定价机制的严重失效。然而,系统未采取任何行动。

第四重故障:事后修改规则作为事前风控缺陷的证据

a. 我们发现,币安在其官方页面上为BNB等少数资产设定了1%的偏差上限。该规则记载的更新日期为2025年11月28日,是在本案发生之后。

b. 这一时间线表明,币安是在本次事件后,紧急为BNB、BTC、ETH等资产引入了极其严格(1%)的偏差控制规则。此举具有明显的"补丁"性质,可合理推断其目的是为防止类似事件再次发生。

c. 这种事后修正强烈且反向地证明了,在事发当日,对于BNB等关键资产,缺乏明确有效的风控保护,或现有规则阈值极不合理。我们的损失正发生在币安自身也承认需大幅加强风控标准的系统漏洞时期。

第五重故障:基于失效数据的错误决策输出("垃圾进,垃圾出")

a. 综合以上几点,10.11事件中币安标记价格系统的运行状态可概括为"垃圾进,垃圾出":系统接收的"价格指数"、"资金费率"(-10%甚至更差)等核心输入数据已严重失真,丧失了市场代表性功能。

b. 系统无视输入数据的全面失效,机械地执行预设的"三价取中"公式,从而输出了一个程序上"合规"但实质上完全失真的标记价格。

c. 币安随后将这一基于无效前提计算出的标记价格,作为具有约束力的"公允价格",用以判定大量投资者的仓位已资不抵债并执行强平。整个强平操作的逻辑基础从一开始就是错误的。

核心法律论点摘要

责任性质:我们的损失并非源于自愿承担的市场波动风险,而是直接由币安未能提供系统可靠性的基本保障所导致。币安有义务确保其核心定价和风控系统在极端压力下保持功能或安全触发熔断。

直接因果关系:扭曲的价格指数和预示市场失效的极端资金费率,共同构成了错误强平的必要原因。若无此系统故障,强平不会被触发。

币安自身逻辑与行动提供的证据:

a. 币安对05:36后发生的损失提供全额补偿,这本身就证明其认可因平台内部异常状态造成的损失应由平台承担的原则。

b. 币安事后为BNB/BTC/ETH设立1%偏差上限规则,进一步从反面承认了事发当时风险控制保护的缺失。众多案例发生得更早,是同一系统失效事件的更早表现,责任性质相同

@cz_binance@heyibinance@sisibinance@cz_binance@heyibinance Your promise:Please note that during extreme market conditions or deviations in price sources, which may lead to the Mark Price deviating from the Spot price, Binance will take additional protective measures. Which one price is more reliable in the case?