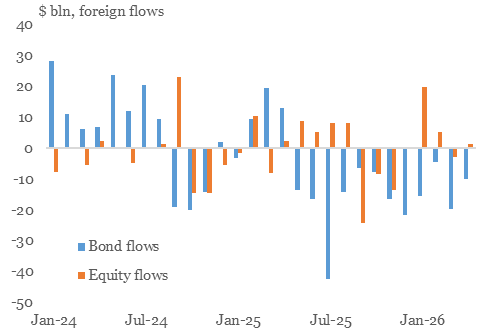

But foreign investors were still net sellers of Chinese bonds and equities in March-April. Chinese assets can be good candidates for hedging and diversifying risks. However, they have not become safe-haven assets in the eyes of global investors.

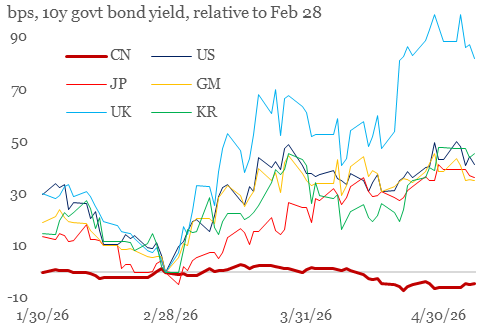

Chinese bonds, equities, and the currency held up well during the Iran shock, especially compared with many Asian peers. CGB yields fell, Chinese equities outperformed most regional markets, and the CNY was among the more stable major currencies.

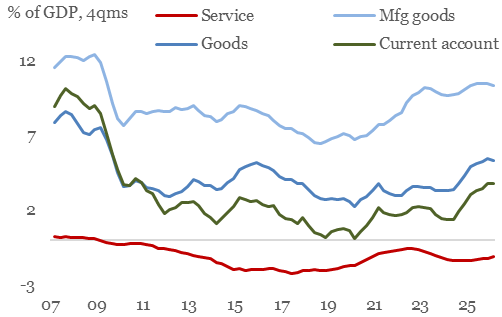

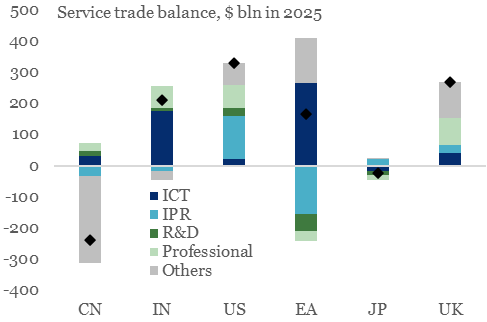

China’s goods surplus has become the focal point of the global trade debate, but the more interesting change may now be occurring in services.

Why China’s services trade matters for global imbalances https://t.co/tvGfeQVhW4 via @wef

For years, China’s large services deficit helped absorb some of the pressure generated by its manufacturing surplus. That offset, however, is becoming less reliable as China's service exports are likely to expand and the service deficit is likely to narrow.

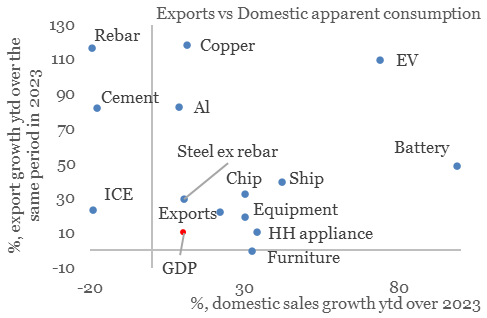

The strong export of copper, EVs, and batteries cannot be attributed to weak domestic demand. Their domestic sales have been strong over the past two years.

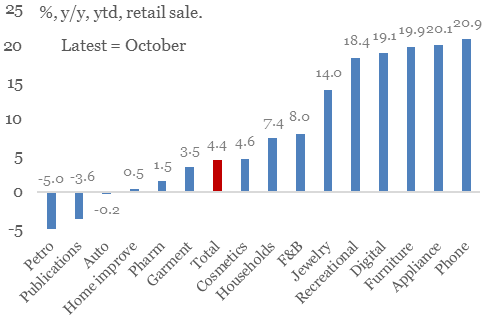

Did the weak Chinese household consumption channel excess output to the global market? Well, retail sales of consumer discretionary items were quite robust ytd, thanks to trade-in subsidies. Except for cars, the export growth of these consumer goods was modest in 2025.

Three examples of weak domestic sales but strong exports are rebar and cement, which suffered from plummeting construction and investment, and ICE cars, which domestic consumers are abandoning.

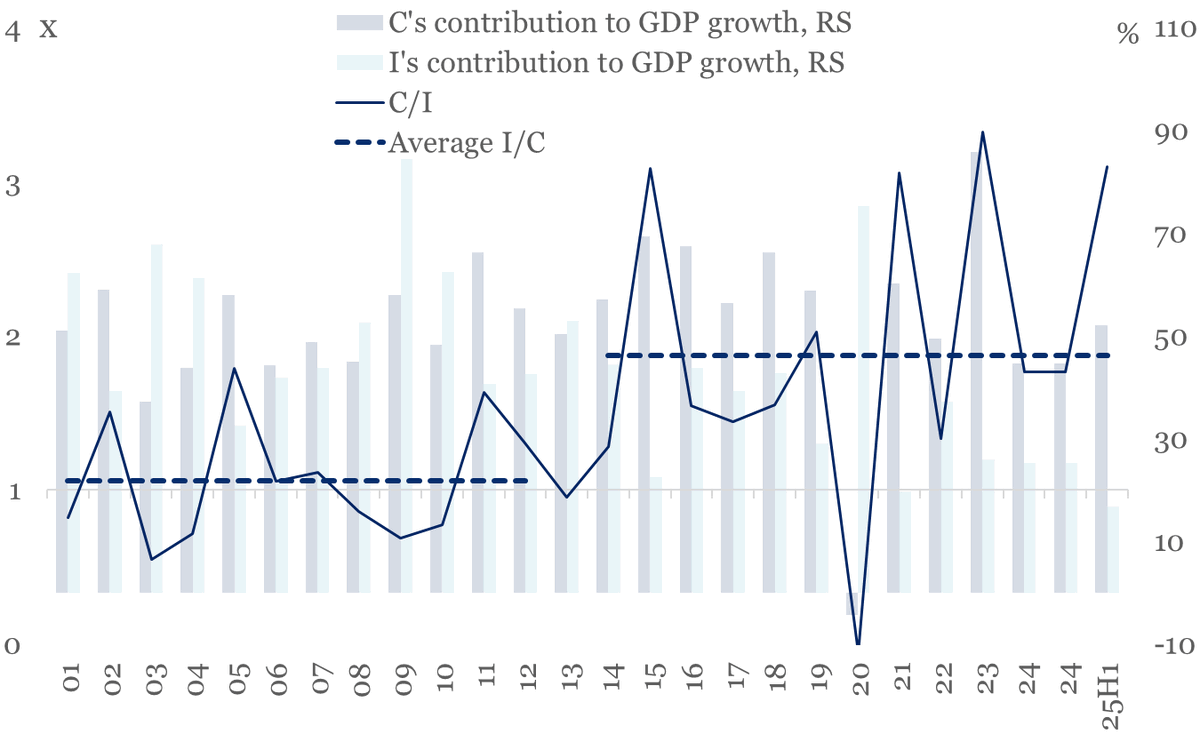

This resilience also cannot be explained by the “under-consumption & over-investment” narrative. In the first half of this year, consumption’s contribution (2.8 ppts) to GDP growth was three times that of capital formation (0.9 ppts).

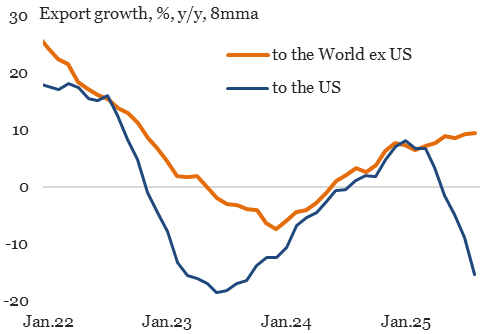

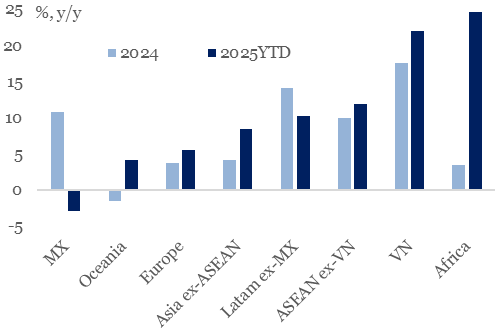

Excluding shipments to the US, China’s exports rose by 9.4% y/y in the first eight months of the year. The strength of exports to markets outside the US cannot be explained by front-loading or rerouting.