BREAKING: In new Form 425, GameStop Corp. increases eBay common stock holdings with additional 1,652,819 shares, bringing ownership of auction giant to 9.35%. 🚨 $GME

BREAKING: EBAY insider Boone Cornelius reported an open-market SALE of 31,100 shares of eBay common stock for $3,411,359.

The "Chief People Officer" (🤣🤣) and "Diversity, Equity and Inclusion (DEI) initiatives Officer" now has net $10.7M of common stock sales and a whopping $0 worth of purchases.

PATHETIC. $GME

Ryan Cohen/GameStop won't cross 15% ownership in $EBAY due to Section 203 Delaware limitations for +15% ownership

I believe Proposal 4 + a proxy fight is the best path to get into the board of eBay and effectuate leadership changes and the eventual M&A with $GME 👇

$gme will squeeze hard and fast in the coming days / weeks. 🚨

Picture 1 speaks for itself. Breakout today or tomorrow.

Picture 2 is HUGE, i never seen the bollinger bands so tight!

So tight means a HUGE move is coming very soon on the weekly!

This means Ryan Cohen can now legally convert GameStop’s derivative exposure into a 9% physical equity stake with full voting rights. 🤯

If eBay shareholders approve Proposal 4 on June 17, reaching just 10% ownership would allow us to bypass the board entirely and directly petition shareholders for a vote on an acquisition. 👀

$GME

eBay shareholder meeting - 10% special meeting threshold passes

GameStop shareholder meeting - share authorization increase passes (comp package too)

GameStop acquires 10% notional ownership, then exercises options

GameStop calls special meeting, which they could trigger by themselves

GameStop forces a vote on the half cash half stock offer to acquire eBay, it will pass

5 steps. That’s it. Checkmate ♟️

BREAKING: In brand new exclusive interview with Barron’s Ryan Cohen says $GME still wants to buy eBay, rips their BoD 🚨.

“I want to own eBay,” Cohen says. “I want to own it for the long term. It’s a great business that’s been poorly managed.”

On rejected offer: “It’s not surprising. We presented a highly credible offer, and it’s exactly what you would expect from a professional board and management team that’s not aligned with shareholders. So, it’s par for the course.”

GameStop Just Dropped a Nuclear Catalyst yesterday for the Mother of All Short Squeezes Bigger Than 2021:

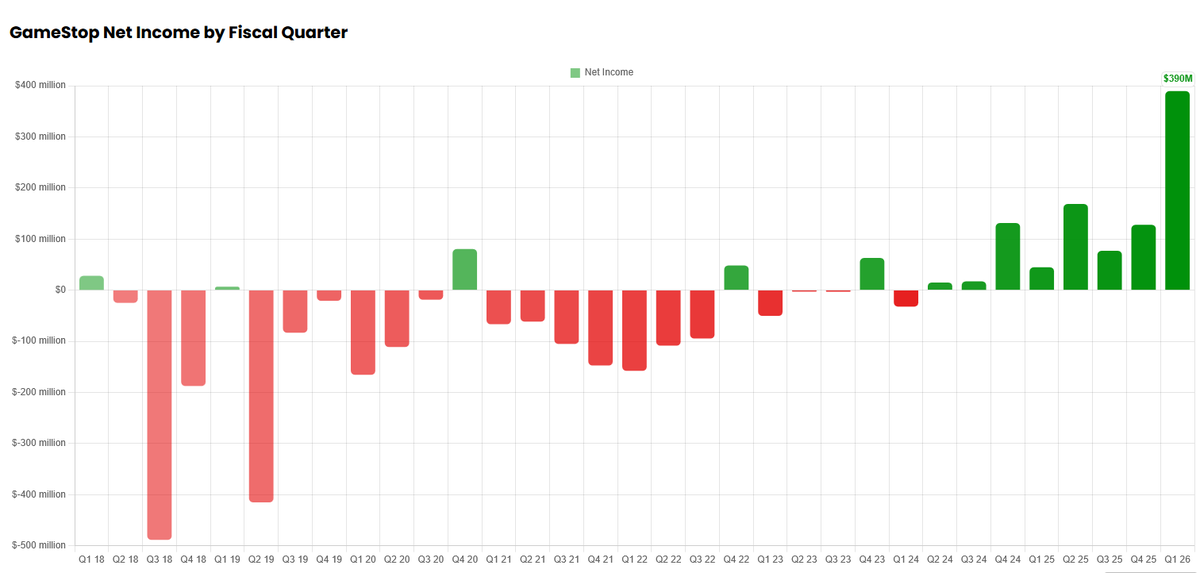

GameStop ($GME) released its Q1 2026 earnings yesterday, and the numbers are historic:

•Record quarterly net income: $389.6 million – the highest in company history.0

•Net sales: $835.3 million, up 14% YoY, led by strong collectibles growth.0

•Operating income: $143.3 million – another all-time high for Q1.

•Massive liquidity: $9.7 billion in cash, marketable securities, digital assets, and related items.

But the real fireworks? The Board unanimously approved a $2 billion discretionary share repurchase program through June 2029, replacing the old 2019 authorization.

Why This Sets Up a Squeeze Far Larger Than 2021?

1. Share Buybacks + Shrinking Float = Rocket Fuel: Buybacks directly reduce the number of shares available in the market. With GME already sitting on a fortress balance sheet and generating real profits, aggressive repurchases can remove tens of millions of shares over time. Fewer shares outstanding means any buying pressure (from shorts covering, retail, or institutions) has an outsized impact on price. In 2021, the squeeze was fueled by extreme short interest on a larger float. Today, buybacks act as a structural tailwind that shorts cannot ignore.

2. Fundamentals Have Flipped the Narrative: 2021 was largely a short-interest + retail momentum story against a turnaround company. Now? GME is profitable, cash-rich, and strategically active (see the eBay acquisition proposal). Record earnings and a buyback signal confidence from management under Ryan Cohen. Shorts betting on bankruptcy or endless dilution are staring at a fundamentally different company – one that can sustain higher valuations and punish holdouts.17

3. Short Interest Still Looms Large While exact current figures fluctuate, GME remains one of the most heavily shorted names on the market with persistent high borrow costs and synthetic share dynamics debated since 2021. Even at lower reported percentages than the 140%+ peak in 2021, the combination of reduced float (via buybacks) and any positive catalyst can create a feedback loop: rising price → margin calls → forced covering → even higher prices.

4. The 2021 Playbook, But With Better Ammo

•Stronger balance sheet = no dilution fears.

•Proven profitability = institutional FOMO potential.

•Retail community more experienced and diamond-handed.

•Options market gamma exposure can still amplify moves explosively.

A $2B buyback authorization isn’t just capital return – it’s a declaration of war on undervaluation and a direct mechanism to tighten supply. If management deploys even a portion at opportune times, it starves the short side while rewarding longs.

This isn’t hopium. It’s math: higher profits + massive cash + aggressive buybacks + unresolved short overhang = asymmetric upside with squeeze potential that dwarfs 2021’s setup.

The bear thesis is dead. GameStop is transforming, and the market is only beginning to price it in.

Load up, hold tight, and buckle up. The squeeze isn’t a meme anymore – it’s balance-sheet backed. 💎🙌

Not financial advice. DYOR. Markets are volatile.

THIS IS INSANE🚨

����1,426% increase in Operating Income

🚨769% increase in Net Income

🚨Almost $1/sh net income in FIRST Q

🚨$2B Share Repurchase APPROVED

GAMESTOP ANNOUNCES HIGHEST NET INCOME ⬇️ $GME

BREAKING🚨 GAMESTOP SHORT SELLER FOUND GUILTY OF SECURITIES FRAUD

The short-selling manipulators are going down

Like 👍 if you think Ken Griffin, Doug Cifu, and Charles Gasparino should be investigated next

So theoretically if $GME initiates a $2B share buyback at the bottom & price then goes above $32…

Warrants get exercised & the company raises $1.9B back? But issues less new shares than they bought back?

I sure would hate to be short right about now 😈

Ryan Cohen is playing chess and until you realize this nothing will make sense.

The $EBAY proposal was the spearhead. Half cash, half stock. Some might even say dilution.

To block the acquisition, $GME needs to be priced low - requiring more stock to finance the deal.

Enter… the buyback + Q1 earnings announcement.

This is the curveball.

To prevent the buybacks, price must be high. To prevent the $EBAY acquisition, price must be low.

This pits two sides of the trade against each other.

In the end, Ryan and shareholders are rewarded - regardless of the outcome.

Anyways, whats an exit strategy?