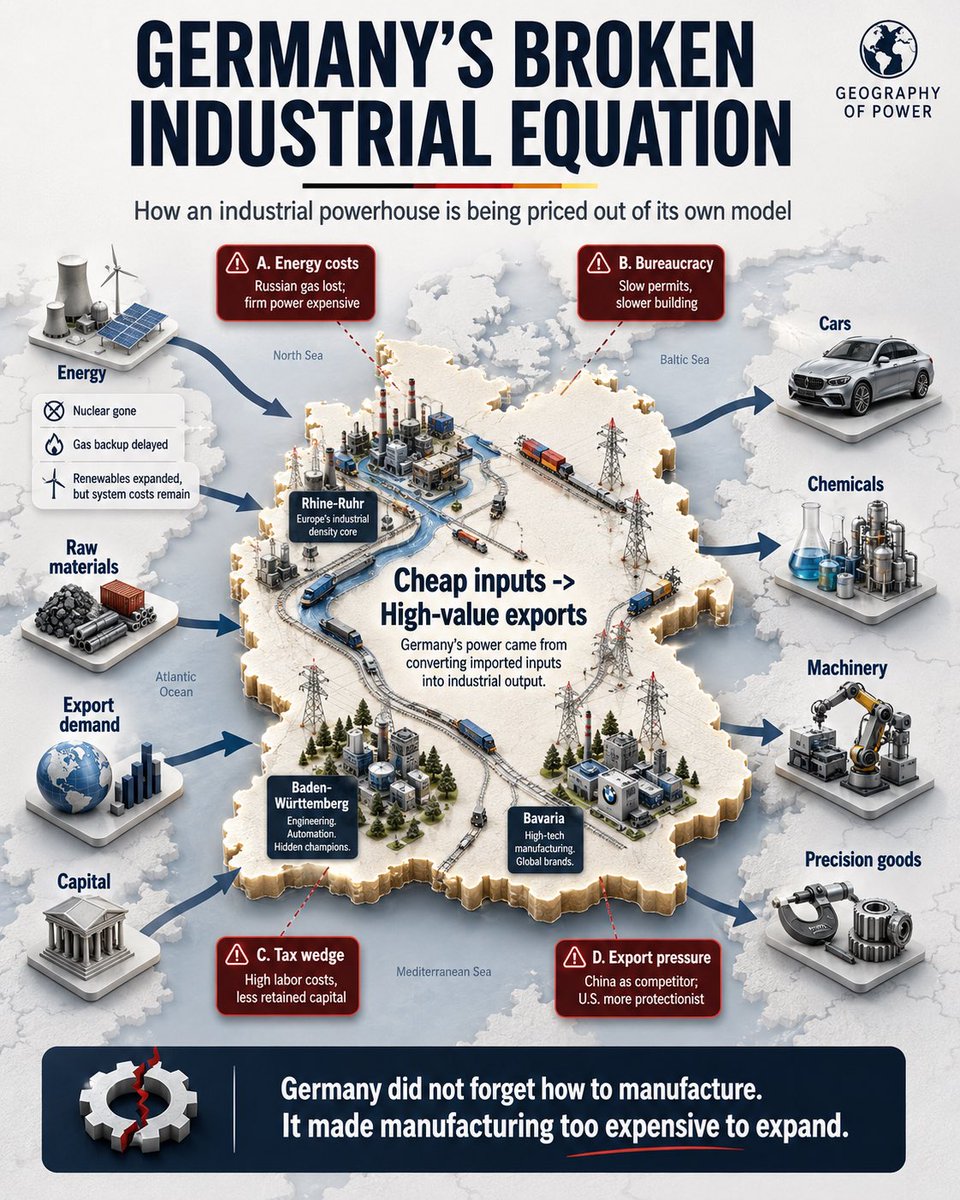

Germany Is Being Priced Out of Its Own Industrial Model

Germany did not lose its economic edge overnight. It lost it through decisions that looked manageable alone and damaging in sequence: cheap Russian gas taken for granted, nuclear shut down, coal scheduled for exit, backup capacity delayed, grids overloaded, permits slow, taxes high and bureaucracy expanding.

Germany was never a resource empire. It was a conversion machine. It imported energy, raw materials and components, ran them through dense industrial clusters, and exported cars, chemicals, machinery and precision goods. Its geography made it powerful: central Europe, Rhine corridors, ports, rail links, skilled labor and global markets. But that model needs reliable energy, fast infrastructure, skilled labor and retained capital.

Germany is weakening all four. Energy is the obvious wound. After 2022, Germany lost cheap Russian gas. But it had already reduced its strategic depth by exiting nuclear power. Wind and solar can be cheap in the right hour. That is not cheap industrial power across the year. A steel plant or chemical site runs on firm power, predictable prices, grid capacity and confidence. The mistake was sequencing. Nuclear exited. Coal is supposed to exit. Renewables expanded. But storage, grids, firm backup capacity and industrial price stability did not arrive in the right order. The planned gas plants are the quiet admission: the system still needs dispatchable power.

Bureaucracy is the second drag. Germany treats paperwork as harmless. It is not. Bureaucracy is time. Time is capital: delayed factories, grid connections, housing, data centers, rail upgrades and adaptation. Every government promises to cut red tape. Somehow the pile survives every funeral. German industry depends on coordination. Chemicals need power, water, rail, pipelines and permits. Cars need suppliers, testing rules, batteries, chips and export routes. Data centers need land, energy and cooling. A slow state lowers the operating speed of the machine.

Taxes and contributions add the next constraint. Germany has one of the highest gaps between what employers pay and what workers keep. That weakens incentives, raises hiring costs and compresses risk and reward. The state is large, but too much spending stabilizes the present instead of building the future. Defense spending is necessary. So is part of the welfare state. But neither automatically rebuilds productivity. Tanks do not solve grid bottlenecks. Subsidies do not replace permits. Welfare does not create cheap energy.

The export map has changed. China is no longer just a customer for German machinery and premium cars. It is a competitor in vehicles, batteries, solar, chemicals, robotics and industrial equipment. The United States is energy-rich, more protectionist and more willing to use industrial policy. Germany now sits between an energy-rich America and a scale-rich China. That is a brutal place for a high-cost exporter.

The weak critique is that Germany became lazy. It did not. The stronger critique is that Germany became institutionally anti-execution. It treats risk as scandal, profit as suspicion, industry as climate liability and bureaucracy as proof of seriousness. Germany still has brilliant engineers and world-class firms. But power rewards the ability to build. Germany asks industry to absorb expensive energy, regulatory overload, high labor costs, aging, weaker export markets, climate transformation and rising security costs — while still funding a large welfare state.

That is not a business cycle.

That is a geographic model under stress. Industrial powers rarely decline by forgetting how to build. They decline by making building too difficult.

@KimDotcom The uncomfortable question for Ukraine:

Can a state keep one of Europe’s largest territories if its young families, workers and future parents are abroad?

Borders matter.

But borders without people behind them are just cartography.

https://t.co/xIuoTv8rDg

Ukraine is not being replaced. Ukraine is running out of people.

The claim that Kyiv plans to “import” 4.5 million migrants is politically explosive. But as analysis, it is too crude.

The harder point is this: Ukraine is facing a classic geography-of-power problem.

A large state needs people to remain large.

Not symbolically.

Not emotionally.

Physically.

It needs soldiers, builders, engineers, nurses, teachers, drivers, electricians, farmers, taxpayers and parents.

Without them, territory becomes a burden.

Ukraine is not a compact city-state. It is one of Europe’s largest countries, with long borders, vast farmland, damaged industrial regions, ruined energy infrastructure, vulnerable cities and a reconstruction project that could last decades.

That is the geographic reality behind the migration debate.

Reuters has reported on Ukraine’s demographic strategy through 2040. The core issue is not first “replacement,” but whether a state battered by war, refugee flight, low birth rates and occupied territory can regain enough manpower to function. The strategy emphasizes refugee return, better infrastructure and family policy first. Immigration enters the picture if the labor market cannot be stabilized otherwise.

That does not make the issue harmless.

It makes it different.

Because labor migration is never just labor migration.

Germany learned this with the Gastarbeiter system. Postwar West Germany needed workers for industry, construction and growth. Recruitment agreements brought Italians, Turks, Greeks, Spaniards, Yugoslavs and others into the labor force.

The political assumption was simple: they work, then they leave.

The geographic reality was different: people who work need housing. People who live somewhere build families. Families build neighborhoods. Neighborhoods become society.

Temporary labor logic became permanent population geography.

That is not a moral judgment. It is a historical rule.

Russia knows the same rule. The Russian Empire used settlement policy to populate frontier and agricultural zones. This was not liberal multiculturalism. It was imperial spatial strategy. Empty land was weak land. Settled land became taxation, military depth and political control.

Modern Russia has its own version of the same contradiction. It needs migrant labor from Central Asia and elsewhere while its politics becomes more nationalist and suspicious of migration. The economy needs people. The rhetoric pretends demography can be ignored.

Ukraine now faces a harsher version of this problem.

Before 2022, Ukraine’s population was already shrinking. Since Russia’s full-scale invasion, the country has suffered deaths, injuries, mass refugee flight, occupied territory, falling births and permanent emigration. The longer Ukrainian women, children and young professionals live in Poland, Germany or Czechia, the less likely return becomes.

That is the real demographic tipping point.

At first, flight is an emergency.

After several years, it becomes a life plan.

Children enter new schools. Mothers find work. Families build routines. Languages are learned. Rental contracts are signed. Social networks form.

Exile becomes future.

For Ukraine, this is strategically dangerous because the country is not losing population in the abstract. It is losing exactly the people a country needs after war: young families, skilled workers, future parents and mobile professionals.

Ukraine’s reconstruction will not depend on money alone.

Money can buy concrete.

But money does not build a bridge if there are no builders.

Money does not repair a grid if there are no technicians.

Money does not defend a border if there are no reserves.

Money does not produce children if a generation settles abroad.

This is the cold logic of geography.

Ukraine does not simply need “more population.” It needs population in the right places, with the right skills, inside a state safe enough for people to stay.

That is where migration becomes a power issue.

If Ukraine attracts foreign workers, it may help stabilize construction, industry, agriculture and care work. But it will also reshape the country’s social map. Anyone who thinks millions of workers can be imported like machines and switched off later has not understood the 20th century.

The better strategy would be layered.

First: bring back the Ukrainian diaspora.

Second: keep young Ukrainians through security, housing, jobs and education.

Third: push automation and military-industrial productivity.

Fourth: use targeted, controlled migration where labor gaps cannot otherwise be filled.

That is not romantic.

It is state logic.

The weakest part of the “Great Replacement” narrative is that it mistakes pressure for intention. Ukraine does not need to be ideologically “replaced” in order to be demographically transformed. War, exile and low birth rates can break the old population structure by themselves. The labor market then demands a new one.

That is the sharper point.

Ukraine is not only fighting for land.

It is fighting over whether that land will still have enough people after the war to be held, farmed, rebuilt and defended.

A border is just a line if nobody lives behind it.

A factory is just a shell if nobody works inside it.

A village is just a dot on the map if no children are born there.

So the central question is not:

“Is Zelensky replacing Ukraine?”

The better question is:

“How does one of Europe’s largest states defend and rebuild itself when the people needed to do it are dead, displaced, occupied, unborn or already building lives elsewhere?”

This is not a conspiracy.

It is geography.

And geography is colder than propaganda.

The real story is not “replacement.”

It is manpower geography.

A large border state needs people to hold territory, rebuild infrastructure and sustain reserves. Ukraine’s map is enormous. Its available population is shrinking.

That gap is the strategic problem.

https://t.co/jaItMmSKzd

Ukraine is not being replaced. Ukraine is running out of people.

The claim that Kyiv plans to “import” 4.5 million migrants is politically explosive. But as analysis, it is too crude.

The harder point is this: Ukraine is facing a classic geography-of-power problem.

A large state needs people to remain large.

Not symbolically.

Not emotionally.

Physically.

It needs soldiers, builders, engineers, nurses, teachers, drivers, electricians, farmers, taxpayers and parents.

Without them, territory becomes a burden.

Ukraine is not a compact city-state. It is one of Europe’s largest countries, with long borders, vast farmland, damaged industrial regions, ruined energy infrastructure, vulnerable cities and a reconstruction project that could last decades.

That is the geographic reality behind the migration debate.

Reuters has reported on Ukraine’s demographic strategy through 2040. The core issue is not first “replacement,” but whether a state battered by war, refugee flight, low birth rates and occupied territory can regain enough manpower to function. The strategy emphasizes refugee return, better infrastructure and family policy first. Immigration enters the picture if the labor market cannot be stabilized otherwise.

That does not make the issue harmless.

It makes it different.

Because labor migration is never just labor migration.

Germany learned this with the Gastarbeiter system. Postwar West Germany needed workers for industry, construction and growth. Recruitment agreements brought Italians, Turks, Greeks, Spaniards, Yugoslavs and others into the labor force.

The political assumption was simple: they work, then they leave.

The geographic reality was different: people who work need housing. People who live somewhere build families. Families build neighborhoods. Neighborhoods become society.

Temporary labor logic became permanent population geography.

That is not a moral judgment. It is a historical rule.

Russia knows the same rule. The Russian Empire used settlement policy to populate frontier and agricultural zones. This was not liberal multiculturalism. It was imperial spatial strategy. Empty land was weak land. Settled land became taxation, military depth and political control.

Modern Russia has its own version of the same contradiction. It needs migrant labor from Central Asia and elsewhere while its politics becomes more nationalist and suspicious of migration. The economy needs people. The rhetoric pretends demography can be ignored.

Ukraine now faces a harsher version of this problem.

Before 2022, Ukraine’s population was already shrinking. Since Russia’s full-scale invasion, the country has suffered deaths, injuries, mass refugee flight, occupied territory, falling births and permanent emigration. The longer Ukrainian women, children and young professionals live in Poland, Germany or Czechia, the less likely return becomes.

That is the real demographic tipping point.

At first, flight is an emergency.

After several years, it becomes a life plan.

Children enter new schools. Mothers find work. Families build routines. Languages are learned. Rental contracts are signed. Social networks form.

Exile becomes future.

For Ukraine, this is strategically dangerous because the country is not losing population in the abstract. It is losing exactly the people a country needs after war: young families, skilled workers, future parents and mobile professionals.

Ukraine’s reconstruction will not depend on money alone.

Money can buy concrete.

But money does not build a bridge if there are no builders.

Money does not repair a grid if there are no technicians.

Money does not defend a border if there are no reserves.

Money does not produce children if a generation settles abroad.

This is the cold logic of geography.

Ukraine does not simply need “more population.” It needs population in the right places, with the right skills, inside a state safe enough for people to stay.

That is where migration becomes a power issue.

If Ukraine attracts foreign workers, it may help stabilize construction, industry, agriculture and care work. But it will also reshape the country’s social map. Anyone who thinks millions of workers can be imported like machines and switched off later has not understood the 20th century.

The better strategy would be layered.

First: bring back the Ukrainian diaspora.

Second: keep young Ukrainians through security, housing, jobs and education.

Third: push automation and military-industrial productivity.

Fourth: use targeted, controlled migration where labor gaps cannot otherwise be filled.

That is not romantic.

It is state logic.

The weakest part of the “Great Replacement” narrative is that it mistakes pressure for intention. Ukraine does not need to be ideologically “replaced” in order to be demographically transformed. War, exile and low birth rates can break the old population structure by themselves. The labor market then demands a new one.

That is the sharper point.

Ukraine is not only fighting for land.

It is fighting over whether that land will still have enough people after the war to be held, farmed, rebuilt and defended.

A border is just a line if nobody lives behind it.

A factory is just a shell if nobody works inside it.

A village is just a dot on the map if no children are born there.

So the central question is not:

“Is Zelensky replacing Ukraine?”

The better question is:

“How does one of Europe’s largest states defend and rebuild itself when the people needed to do it are dead, displaced, occupied, unborn or already building lives elsewhere?”

This is not a conspiracy.

It is geography.

And geography is colder than propaganda.

Ukraine is not being replaced. Ukraine is running out of people.

The claim that Kyiv plans to “import” 4.5 million migrants is politically explosive. But as analysis, it is too crude.

The harder point is this: Ukraine is facing a classic geography-of-power problem.

A large state needs people to remain large.

Not symbolically.

Not emotionally.

Physically.

It needs soldiers, builders, engineers, nurses, teachers, drivers, electricians, farmers, taxpayers and parents.

Without them, territory becomes a burden.

Ukraine is not a compact city-state. It is one of Europe’s largest countries, with long borders, vast farmland, damaged industrial regions, ruined energy infrastructure, vulnerable cities and a reconstruction project that could last decades.

That is the geographic reality behind the migration debate.

Reuters has reported on Ukraine’s demographic strategy through 2040. The core issue is not first “replacement,” but whether a state battered by war, refugee flight, low birth rates and occupied territory can regain enough manpower to function. The strategy emphasizes refugee return, better infrastructure and family policy first. Immigration enters the picture if the labor market cannot be stabilized otherwise.

That does not make the issue harmless.

It makes it different.

Because labor migration is never just labor migration.

Germany learned this with the Gastarbeiter system. Postwar West Germany needed workers for industry, construction and growth. Recruitment agreements brought Italians, Turks, Greeks, Spaniards, Yugoslavs and others into the labor force.

The political assumption was simple: they work, then they leave.

The geographic reality was different: people who work need housing. People who live somewhere build families. Families build neighborhoods. Neighborhoods become society.

Temporary labor logic became permanent population geography.

That is not a moral judgment. It is a historical rule.

Russia knows the same rule. The Russian Empire used settlement policy to populate frontier and agricultural zones. This was not liberal multiculturalism. It was imperial spatial strategy. Empty land was weak land. Settled land became taxation, military depth and political control.

Modern Russia has its own version of the same contradiction. It needs migrant labor from Central Asia and elsewhere while its politics becomes more nationalist and suspicious of migration. The economy needs people. The rhetoric pretends demography can be ignored.

Ukraine now faces a harsher version of this problem.

Before 2022, Ukraine’s population was already shrinking. Since Russia’s full-scale invasion, the country has suffered deaths, injuries, mass refugee flight, occupied territory, falling births and permanent emigration. The longer Ukrainian women, children and young professionals live in Poland, Germany or Czechia, the less likely return becomes.

That is the real demographic tipping point.

At first, flight is an emergency.

After several years, it becomes a life plan.

Children enter new schools. Mothers find work. Families build routines. Languages are learned. Rental contracts are signed. Social networks form.

Exile becomes future.

For Ukraine, this is strategically dangerous because the country is not losing population in the abstract. It is losing exactly the people a country needs after war: young families, skilled workers, future parents and mobile professionals.

Ukraine’s reconstruction will not depend on money alone.

Money can buy concrete.

But money does not build a bridge if there are no builders.

Money does not repair a grid if there are no technicians.

Money does not defend a border if there are no reserves.

Money does not produce children if a generation settles abroad.

This is the cold logic of geography.

Ukraine does not simply need “more population.” It needs population in the right places, with the right skills, inside a state safe enough for people to stay.

That is where migration becomes a power issue.

If Ukraine attracts foreign workers, it may help stabilize construction, industry, agriculture and care work. But it will also reshape the country’s social map. Anyone who thinks millions of workers can be imported like machines and switched off later has not understood the 20th century.

The better strategy would be layered.

First: bring back the Ukrainian diaspora.

Second: keep young Ukrainians through security, housing, jobs and education.

Third: push automation and military-industrial productivity.

Fourth: use targeted, controlled migration where labor gaps cannot otherwise be filled.

That is not romantic.

It is state logic.

The weakest part of the “Great Replacement” narrative is that it mistakes pressure for intention. Ukraine does not need to be ideologically “replaced” in order to be demographically transformed. War, exile and low birth rates can break the old population structure by themselves. The labor market then demands a new one.

That is the sharper point.

Ukraine is not only fighting for land.

It is fighting over whether that land will still have enough people after the war to be held, farmed, rebuilt and defended.

A border is just a line if nobody lives behind it.

A factory is just a shell if nobody works inside it.

A village is just a dot on the map if no children are born there.

So the central question is not:

“Is Zelensky replacing Ukraine?”

The better question is:

“How does one of Europe’s largest states defend and rebuild itself when the people needed to do it are dead, displaced, occupied, unborn or already building lives elsewhere?”

This is not a conspiracy.

It is geography.

And geography is colder than propaganda.

The Mars story gets the attention.

But the business logic is closer to ports, canals, telecom networks and toll roads: make a frontier reachable, serviceable and expensive for others to bypass.

SpaceX may be building the access map before the economy exists.

Full framework: https://t.co/2iyg1akSGi

SpaceX Is Not Selling Rockets. It Is Selling the First Toll Road to the Next Economy.

The SpaceX IPO is being discussed as a financial event.

That is already too small.

A normal company goes public because it wants capital, liquidity, index inclusion, prestige and a broader investor base. SpaceX is doing all of that. But underneath the IPO mechanics sits a much larger question: who gets to build the first privately controlled access system to the next economic geography?

Not the next app.

Not the next social network.

A new geography.

That is why the most important SpaceX story is not whether the company is valued at $1.5 trillion, $1.75 trillion or $2 trillion. The real question is whether SpaceX becomes the operating layer between Earth and the space economy: launch, satellite communications, orbital infrastructure, lunar logistics, resource access, energy systems, defense networks and eventually quasi-property rights beyond Earth.

That is not a rocket business.

That is a port empire.

1. The prospectus has to under-sell the frontier

IPO prospectuses are legal machines before they are marketing documents.

They are written to reduce liability. They list everything that can fail: rockets can explode, regulators can delay launches, Starship can miss milestones, AI infrastructure in orbit may never become commercially viable, Mars settlement may remain technically remote, and capital expenditure may consume cash faster than investors expect.

That is why the SpaceX filing sounds more cautious than the public Musk narrative.

Legally, this makes sense. Strategically, it hides the actual thesis.

Because the strongest SpaceX case is not that every futuristic line of business works. It is that all future space businesses depend on the same primitive layer: cheap, frequent, heavy, reliable access from Earth to orbit and beyond.

Every empire starts with movement.

Rivers. Roads. Ports. Canals. Railways. Shipping lanes. Air corridors. Fiber cables. Pipelines.

In space, the first equivalent is launch cadence.

2. Launch cadence is the first chokepoint

Geography creates power by creating bottlenecks.

The Bosporus matters because ships must pass through it. The Suez Canal matters because it compresses distance. Singapore matters because maritime Asia bends around it. Panama matters because geography forced trade through a narrow artificial cut.

Space has its own chokepoint: the gravity well.

For decades, the cost of moving mass out of Earth’s gravity kept space activity narrow, state-led and expensive. Satellites were valuable, but the operating environment was not yet an open industrial geography. It was more like an offshore oil platform: specialized, capital-intensive, hostile and limited to a few actors.

SpaceX’s central achievement is not that it launches rockets.

It made launch repeatable.

Falcon 9 created the operating rhythm. Starlink became the demand engine. Starship, if it works at scale, becomes the heavy transport system that turns orbit from a rare destination into a logistics zone.

That is why Starship failures do not automatically kill the thesis. Frontier infrastructure fails before it standardizes. Railways bankrupted investors. Canals ran over budget. Early aviation killed pilots. Undersea cables snapped. The important question is not whether the frontier is clean. It never is.

The question is whether one operator learns faster than the rest.

3. Starlink is not just internet. It is proof of orbital utility.

Starlink is usually described as satellite broadband.

That description is accurate and insufficient.

Starlink proves that orbital infrastructure can become a mass-market utility. Once space infrastructure serves millions of terrestrial users, orbit stops being symbolic. It becomes part of daily economic life.

That matters because every frontier becomes investable only after it develops utilities.

The American West needed railroads, telegraph lines, water rights, forts, surveys and land registries. Maritime empires needed ports, coaling stations, dry docks, naval protection, charts and insurance. The internet needed fiber, data centers, protocols, browsers, payments and cloud infrastructure.

Outer space will be no different.

Before lunar industry, there must be energy. Before asteroid mining, there must be transport. Before orbital manufacturing, there must be docking, robotics, debris management, maintenance, power, insurance and predictable rules. Before Mars settlement, there must be a supply chain that can survive distance, radiation, equipment failure and political pressure on Earth.

SpaceX is dangerous to competitors because it is not building one piece of this chain.

It is trying to integrate the chain.

4. The property question is bigger than “owning the Moon”

The most provocative claim in the source article is that SpaceX could become the largest real estate story in history.

That is directionally interesting, but the cleaner frame is this:

The first space real estate will not be romantic land ownership. It will be infrastructure real estate.

No serious investor needs a decorative certificate for ten acres of Mars.

What matters is income-producing control over useful locations and systems: landing zones, power sites, orbital platforms, lunar logistics nodes, communication relays, fuel depots, radiation-shielded habitats, regolith-processing facilities, water-ice access corridors and high-value orbital slots.

On Earth, the most valuable real estate is often not empty land. It is the port. The airport. The logistics park. The railway terminal. The data center with grid access. The pipeline corridor. The fiber landing station. The warehouse cluster beside a highway interchange.

Space will follow the same logic.

A future “space REIT” may not own the Moon. It may own leases, operating rights, energy systems, habitats, docking infrastructure or resource-processing facilities that generate cash flow.

Finance does not need romance.

Finance needs enforceable income.

5. Law follows logistics more often than it leads it

The Outer Space Treaty blocks national sovereignty claims over celestial bodies. That matters. It prevents a crude repetition of old imperial flag-planting.

But it does not settle every commercial question.

Private companies operate through states. States license launches. States supervise national companies. Some national laws already recognize rights over extracted resources without claiming sovereignty over the celestial body itself.

That distinction is where the future will be fought.

Not “Who owns Mars?”

But:

Who may extract water ice?

Who may protect a landing zone?

Who may exclude others from a dangerous operating area?

Who gets priority access to a lunar power ridge?

Who insures damage between two private actors?

Who arbitrates interference between mining operations?

Who licenses orbital compute platforms?

Who controls military-use communications infrastructure?

The first property regime in space will likely be a patchwork of safety zones, licenses, contracts, insurance rules, bilateral agreements and de facto operational control.

That sounds boring.

It is how frontiers become markets.

6. The bear case is real

There is a serious objection.

SpaceX may be mixing too many speculative futures into one investment story: launch, broadband, AI, defense networks, orbital data centers, Moon logistics, Mars settlement, asteroid mining and off-world industry.

That is not a small risk. Frontier finance has always produced hallucination.

Railways produced fortunes and frauds. The internet produced Amazon and https://t.co/x49hFrX76I. Shale produced energy abundance and bankruptcies. Space capitalism will do the same.

So the right analysis is not “believe everything.”

The right analysis is hierarchy.

Cash-flow layer: Starlink and launch services.

Strategic layer: defense, communications, orbital logistics.

Cost-reduction layer: reusable heavy launch.

Option layer: orbital AI, lunar industry, asteroid mining, Mars settlement.

The IPO should not be judged as if all layers are equally mature.

They are not.

7. The real SpaceX thesis

The market will price SpaceX as a company.

History may judge it as infrastructure.

If SpaceX succeeds, it will not merely be the firm that made rockets reusable or sold broadband from orbit. It will be the company that made space commercially legible: reachable, serviceable, insurable, financeable and eventually ownable in practice, if not in the old territorial sense.

That is why the IPO story under-sells the future.

Not because the prospectus fails to promise enough science fiction. The world has enough Mars poetry already.

It under-sells the future because the real upside is more concrete and more geopolitical:

SpaceX is building the ports before the cities exist.

And in every frontier that ever mattered, the people who controlled the ports shaped the map that followed.

@MorePerfectUS SpaceX is usually framed as a rocket company.

That misses the deeper point: rockets are the ships, Starlink is the utility layer, and Starship is the heavy transport system.

The real question is who controls access to the next geography.

More detail: https://t.co/ALtgMVZsfE

SpaceX Is Not Selling Rockets. It Is Selling the First Toll Road to the Next Economy.

The SpaceX IPO is being discussed as a financial event.

That is already too small.

A normal company goes public because it wants capital, liquidity, index inclusion, prestige and a broader investor base. SpaceX is doing all of that. But underneath the IPO mechanics sits a much larger question: who gets to build the first privately controlled access system to the next economic geography?

Not the next app.

Not the next social network.

A new geography.

That is why the most important SpaceX story is not whether the company is valued at $1.5 trillion, $1.75 trillion or $2 trillion. The real question is whether SpaceX becomes the operating layer between Earth and the space economy: launch, satellite communications, orbital infrastructure, lunar logistics, resource access, energy systems, defense networks and eventually quasi-property rights beyond Earth.

That is not a rocket business.

That is a port empire.

1. The prospectus has to under-sell the frontier

IPO prospectuses are legal machines before they are marketing documents.

They are written to reduce liability. They list everything that can fail: rockets can explode, regulators can delay launches, Starship can miss milestones, AI infrastructure in orbit may never become commercially viable, Mars settlement may remain technically remote, and capital expenditure may consume cash faster than investors expect.

That is why the SpaceX filing sounds more cautious than the public Musk narrative.

Legally, this makes sense. Strategically, it hides the actual thesis.

Because the strongest SpaceX case is not that every futuristic line of business works. It is that all future space businesses depend on the same primitive layer: cheap, frequent, heavy, reliable access from Earth to orbit and beyond.

Every empire starts with movement.

Rivers. Roads. Ports. Canals. Railways. Shipping lanes. Air corridors. Fiber cables. Pipelines.

In space, the first equivalent is launch cadence.

2. Launch cadence is the first chokepoint

Geography creates power by creating bottlenecks.

The Bosporus matters because ships must pass through it. The Suez Canal matters because it compresses distance. Singapore matters because maritime Asia bends around it. Panama matters because geography forced trade through a narrow artificial cut.

Space has its own chokepoint: the gravity well.

For decades, the cost of moving mass out of Earth’s gravity kept space activity narrow, state-led and expensive. Satellites were valuable, but the operating environment was not yet an open industrial geography. It was more like an offshore oil platform: specialized, capital-intensive, hostile and limited to a few actors.

SpaceX’s central achievement is not that it launches rockets.

It made launch repeatable.

Falcon 9 created the operating rhythm. Starlink became the demand engine. Starship, if it works at scale, becomes the heavy transport system that turns orbit from a rare destination into a logistics zone.

That is why Starship failures do not automatically kill the thesis. Frontier infrastructure fails before it standardizes. Railways bankrupted investors. Canals ran over budget. Early aviation killed pilots. Undersea cables snapped. The important question is not whether the frontier is clean. It never is.

The question is whether one operator learns faster than the rest.

3. Starlink is not just internet. It is proof of orbital utility.

Starlink is usually described as satellite broadband.

That description is accurate and insufficient.

Starlink proves that orbital infrastructure can become a mass-market utility. Once space infrastructure serves millions of terrestrial users, orbit stops being symbolic. It becomes part of daily economic life.

That matters because every frontier becomes investable only after it develops utilities.

The American West needed railroads, telegraph lines, water rights, forts, surveys and land registries. Maritime empires needed ports, coaling stations, dry docks, naval protection, charts and insurance. The internet needed fiber, data centers, protocols, browsers, payments and cloud infrastructure.

Outer space will be no different.

Before lunar industry, there must be energy. Before asteroid mining, there must be transport. Before orbital manufacturing, there must be docking, robotics, debris management, maintenance, power, insurance and predictable rules. Before Mars settlement, there must be a supply chain that can survive distance, radiation, equipment failure and political pressure on Earth.

SpaceX is dangerous to competitors because it is not building one piece of this chain.

It is trying to integrate the chain.

4. The property question is bigger than “owning the Moon”

The most provocative claim in the source article is that SpaceX could become the largest real estate story in history.

That is directionally interesting, but the cleaner frame is this:

The first space real estate will not be romantic land ownership. It will be infrastructure real estate.

No serious investor needs a decorative certificate for ten acres of Mars.

What matters is income-producing control over useful locations and systems: landing zones, power sites, orbital platforms, lunar logistics nodes, communication relays, fuel depots, radiation-shielded habitats, regolith-processing facilities, water-ice access corridors and high-value orbital slots.

On Earth, the most valuable real estate is often not empty land. It is the port. The airport. The logistics park. The railway terminal. The data center with grid access. The pipeline corridor. The fiber landing station. The warehouse cluster beside a highway interchange.

Space will follow the same logic.

A future “space REIT” may not own the Moon. It may own leases, operating rights, energy systems, habitats, docking infrastructure or resource-processing facilities that generate cash flow.

Finance does not need romance.

Finance needs enforceable income.

5. Law follows logistics more often than it leads it

The Outer Space Treaty blocks national sovereignty claims over celestial bodies. That matters. It prevents a crude repetition of old imperial flag-planting.

But it does not settle every commercial question.

Private companies operate through states. States license launches. States supervise national companies. Some national laws already recognize rights over extracted resources without claiming sovereignty over the celestial body itself.

That distinction is where the future will be fought.

Not “Who owns Mars?”

But:

Who may extract water ice?

Who may protect a landing zone?

Who may exclude others from a dangerous operating area?

Who gets priority access to a lunar power ridge?

Who insures damage between two private actors?

Who arbitrates interference between mining operations?

Who licenses orbital compute platforms?

Who controls military-use communications infrastructure?

The first property regime in space will likely be a patchwork of safety zones, licenses, contracts, insurance rules, bilateral agreements and de facto operational control.

That sounds boring.

It is how frontiers become markets.

6. The bear case is real

There is a serious objection.

SpaceX may be mixing too many speculative futures into one investment story: launch, broadband, AI, defense networks, orbital data centers, Moon logistics, Mars settlement, asteroid mining and off-world industry.

That is not a small risk. Frontier finance has always produced hallucination.

Railways produced fortunes and frauds. The internet produced Amazon and https://t.co/x49hFrX76I. Shale produced energy abundance and bankruptcies. Space capitalism will do the same.

So the right analysis is not “believe everything.”

The right analysis is hierarchy.

Cash-flow layer: Starlink and launch services.

Strategic layer: defense, communications, orbital logistics.

Cost-reduction layer: reusable heavy launch.

Option layer: orbital AI, lunar industry, asteroid mining, Mars settlement.

The IPO should not be judged as if all layers are equally mature.

They are not.

7. The real SpaceX thesis

The market will price SpaceX as a company.

History may judge it as infrastructure.

If SpaceX succeeds, it will not merely be the firm that made rockets reusable or sold broadband from orbit. It will be the company that made space commercially legible: reachable, serviceable, insurable, financeable and eventually ownable in practice, if not in the old territorial sense.

That is why the IPO story under-sells the future.

Not because the prospectus fails to promise enough science fiction. The world has enough Mars poetry already.

It under-sells the future because the real upside is more concrete and more geopolitical:

SpaceX is building the ports before the cities exist.

And in every frontier that ever mattered, the people who controlled the ports shaped the map that followed.

SpaceX Is Not Selling Rockets. It Is Selling the First Toll Road to the Next Economy.

The SpaceX IPO is being discussed as a financial event.

That is already too small.

A normal company goes public because it wants capital, liquidity, index inclusion, prestige and a broader investor base. SpaceX is doing all of that. But underneath the IPO mechanics sits a much larger question: who gets to build the first privately controlled access system to the next economic geography?

Not the next app.

Not the next social network.

A new geography.

That is why the most important SpaceX story is not whether the company is valued at $1.5 trillion, $1.75 trillion or $2 trillion. The real question is whether SpaceX becomes the operating layer between Earth and the space economy: launch, satellite communications, orbital infrastructure, lunar logistics, resource access, energy systems, defense networks and eventually quasi-property rights beyond Earth.

That is not a rocket business.

That is a port empire.

1. The prospectus has to under-sell the frontier

IPO prospectuses are legal machines before they are marketing documents.

They are written to reduce liability. They list everything that can fail: rockets can explode, regulators can delay launches, Starship can miss milestones, AI infrastructure in orbit may never become commercially viable, Mars settlement may remain technically remote, and capital expenditure may consume cash faster than investors expect.

That is why the SpaceX filing sounds more cautious than the public Musk narrative.

Legally, this makes sense. Strategically, it hides the actual thesis.

Because the strongest SpaceX case is not that every futuristic line of business works. It is that all future space businesses depend on the same primitive layer: cheap, frequent, heavy, reliable access from Earth to orbit and beyond.

Every empire starts with movement.

Rivers. Roads. Ports. Canals. Railways. Shipping lanes. Air corridors. Fiber cables. Pipelines.

In space, the first equivalent is launch cadence.

2. Launch cadence is the first chokepoint

Geography creates power by creating bottlenecks.

The Bosporus matters because ships must pass through it. The Suez Canal matters because it compresses distance. Singapore matters because maritime Asia bends around it. Panama matters because geography forced trade through a narrow artificial cut.

Space has its own chokepoint: the gravity well.

For decades, the cost of moving mass out of Earth’s gravity kept space activity narrow, state-led and expensive. Satellites were valuable, but the operating environment was not yet an open industrial geography. It was more like an offshore oil platform: specialized, capital-intensive, hostile and limited to a few actors.

SpaceX’s central achievement is not that it launches rockets.

It made launch repeatable.

Falcon 9 created the operating rhythm. Starlink became the demand engine. Starship, if it works at scale, becomes the heavy transport system that turns orbit from a rare destination into a logistics zone.

That is why Starship failures do not automatically kill the thesis. Frontier infrastructure fails before it standardizes. Railways bankrupted investors. Canals ran over budget. Early aviation killed pilots. Undersea cables snapped. The important question is not whether the frontier is clean. It never is.

The question is whether one operator learns faster than the rest.

3. Starlink is not just internet. It is proof of orbital utility.

Starlink is usually described as satellite broadband.

That description is accurate and insufficient.

Starlink proves that orbital infrastructure can become a mass-market utility. Once space infrastructure serves millions of terrestrial users, orbit stops being symbolic. It becomes part of daily economic life.

That matters because every frontier becomes investable only after it develops utilities.

The American West needed railroads, telegraph lines, water rights, forts, surveys and land registries. Maritime empires needed ports, coaling stations, dry docks, naval protection, charts and insurance. The internet needed fiber, data centers, protocols, browsers, payments and cloud infrastructure.

Outer space will be no different.

Before lunar industry, there must be energy. Before asteroid mining, there must be transport. Before orbital manufacturing, there must be docking, robotics, debris management, maintenance, power, insurance and predictable rules. Before Mars settlement, there must be a supply chain that can survive distance, radiation, equipment failure and political pressure on Earth.

SpaceX is dangerous to competitors because it is not building one piece of this chain.

It is trying to integrate the chain.

4. The property question is bigger than “owning the Moon”

The most provocative claim in the source article is that SpaceX could become the largest real estate story in history.

That is directionally interesting, but the cleaner frame is this:

The first space real estate will not be romantic land ownership. It will be infrastructure real estate.

No serious investor needs a decorative certificate for ten acres of Mars.

What matters is income-producing control over useful locations and systems: landing zones, power sites, orbital platforms, lunar logistics nodes, communication relays, fuel depots, radiation-shielded habitats, regolith-processing facilities, water-ice access corridors and high-value orbital slots.

On Earth, the most valuable real estate is often not empty land. It is the port. The airport. The logistics park. The railway terminal. The data center with grid access. The pipeline corridor. The fiber landing station. The warehouse cluster beside a highway interchange.

Space will follow the same logic.

A future “space REIT” may not own the Moon. It may own leases, operating rights, energy systems, habitats, docking infrastructure or resource-processing facilities that generate cash flow.

Finance does not need romance.

Finance needs enforceable income.

5. Law follows logistics more often than it leads it

The Outer Space Treaty blocks national sovereignty claims over celestial bodies. That matters. It prevents a crude repetition of old imperial flag-planting.

But it does not settle every commercial question.

Private companies operate through states. States license launches. States supervise national companies. Some national laws already recognize rights over extracted resources without claiming sovereignty over the celestial body itself.

That distinction is where the future will be fought.

Not “Who owns Mars?”

But:

Who may extract water ice?

Who may protect a landing zone?

Who may exclude others from a dangerous operating area?

Who gets priority access to a lunar power ridge?

Who insures damage between two private actors?

Who arbitrates interference between mining operations?

Who licenses orbital compute platforms?

Who controls military-use communications infrastructure?

The first property regime in space will likely be a patchwork of safety zones, licenses, contracts, insurance rules, bilateral agreements and de facto operational control.

That sounds boring.

It is how frontiers become markets.

6. The bear case is real

There is a serious objection.

SpaceX may be mixing too many speculative futures into one investment story: launch, broadband, AI, defense networks, orbital data centers, Moon logistics, Mars settlement, asteroid mining and off-world industry.

That is not a small risk. Frontier finance has always produced hallucination.

Railways produced fortunes and frauds. The internet produced Amazon and https://t.co/x49hFrX76I. Shale produced energy abundance and bankruptcies. Space capitalism will do the same.

So the right analysis is not “believe everything.”

The right analysis is hierarchy.

Cash-flow layer: Starlink and launch services.

Strategic layer: defense, communications, orbital logistics.

Cost-reduction layer: reusable heavy launch.

Option layer: orbital AI, lunar industry, asteroid mining, Mars settlement.

The IPO should not be judged as if all layers are equally mature.

They are not.

7. The real SpaceX thesis

The market will price SpaceX as a company.

History may judge it as infrastructure.

If SpaceX succeeds, it will not merely be the firm that made rockets reusable or sold broadband from orbit. It will be the company that made space commercially legible: reachable, serviceable, insurable, financeable and eventually ownable in practice, if not in the old territorial sense.

That is why the IPO story under-sells the future.

Not because the prospectus fails to promise enough science fiction. The world has enough Mars poetry already.

It under-sells the future because the real upside is more concrete and more geopolitical:

SpaceX is building the ports before the cities exist.

And in every frontier that ever mattered, the people who controlled the ports shaped the map that followed.

The key point is that depopulation does not hit assets evenly. It destroys marginal housing first: inland cities, weak labor markets, bad logistics, excess supply. Strategic nodes survive longer because geography still creates scarcity. China’s property crisis is really a test of whether automation can replace household formation.

https://t.co/3Hn6qsuvD8

The next global crisis may not be inflation. It may be too few buyers.

For 70 years, the modern economy was built on a simple assumption: more workers, more households, more mortgages, more roads, more consumption. Japan broke that model first. Its working-age population peaked in 1995. The land-and-housing bubble never really returned.

China is now facing the same empire-cycle problem at much larger scale. Its population is already shrinking, births are far below deaths, and the property sector is no longer a one-way machine for household wealth, local government revenue, and steel demand.

Geography makes this worse. Empty apartments in shrinking inland cities are not the same asset as scarce housing in Shanghai, Shenzhen, Tokyo, Paris, or New York. Depopulation does not hit “real estate” equally. It destroys the periphery first and protects the strategic nodes: ports, capitals, tech clusters, logistics hubs.

The geopolitical result is a split economy. Countries with young workers, migrants, food, energy, and urban growth gain bargaining power. Aging powers compensate with robots, AI, semiconductors, drones, automation, and capital exports. The contest becomes: can technology replace missing people fast enough?

China’s real estate crisis is not just a financial story. It is the first major test of whether an industrial empire can survive after the household-formation engine stalls.

What matters more in the next 30 years: population size, or machine productivity?

The next global crisis may not be inflation. It may be too few buyers.

For 70 years, the modern economy was built on a simple assumption: more workers, more households, more mortgages, more roads, more consumption. Japan broke that model first. Its working-age population peaked in 1995. The land-and-housing bubble never really returned.

China is now facing the same empire-cycle problem at much larger scale. Its population is already shrinking, births are far below deaths, and the property sector is no longer a one-way machine for household wealth, local government revenue, and steel demand.

Geography makes this worse. Empty apartments in shrinking inland cities are not the same asset as scarce housing in Shanghai, Shenzhen, Tokyo, Paris, or New York. Depopulation does not hit “real estate” equally. It destroys the periphery first and protects the strategic nodes: ports, capitals, tech clusters, logistics hubs.

The geopolitical result is a split economy. Countries with young workers, migrants, food, energy, and urban growth gain bargaining power. Aging powers compensate with robots, AI, semiconductors, drones, automation, and capital exports. The contest becomes: can technology replace missing people fast enough?

China’s real estate crisis is not just a financial story. It is the first major test of whether an industrial empire can survive after the household-formation engine stalls.

What matters more in the next 30 years: population size, or machine productivity?

The interesting part is not that drones make every country food-independent. They won’t. Water, soil and climate still rule. But cheap computer vision can reduce the productivity gap for countries with decent land — and shift dependency from grain exporters to chips, sensors, batteries and agronomic software.

https://t.co/fBVndxJ0cG

A cheap drone may become one of the quiet weapons of food sovereignty.

Not because it replaces land, rain or soil. It does not. Geography still decides who has black earth, river systems, long growing seasons and cheap irrigation. Egypt will not become Ukraine. Singapore will not become Iowa.

But agriculture has always been an empire problem: feed the cities, secure the grain routes, control the surplus. Rome needed Egypt. Britain needed global wheat lanes. Today many states depend on a handful of exporters, from the Black Sea to North America, Brazil and Southeast Asia.

Computer vision changes the margin.

A drone that can count plants, detect disease, map water stress and guide fertilizer use gives small and medium farms something once reserved for industrial agribusiness: field intelligence. That can raise yields, cut waste, reduce pesticide and fertilizer dependency, and make local production less blind.

The geopolitical result is not autarky. It is selective de-risking.

Countries with enough land, water and labor can use AI agriculture to close part of the productivity gap. Importers may still buy wheat, rice or soy, but they become less exposed to shipping chokepoints, export bans, currency shocks and fertilizer bottlenecks.

The new dependency moves upstream: drones, sensors, chips, cloud models, batteries, satellite data and agronomic software.

Food power will not disappear. It will migrate from grain elevators to data layers.

Will the next agricultural superpower be the country with the most land — or the one that turns every hectare into a measured system?

A cheap drone may become one of the quiet weapons of food sovereignty.

Not because it replaces land, rain or soil. It does not. Geography still decides who has black earth, river systems, long growing seasons and cheap irrigation. Egypt will not become Ukraine. Singapore will not become Iowa.

But agriculture has always been an empire problem: feed the cities, secure the grain routes, control the surplus. Rome needed Egypt. Britain needed global wheat lanes. Today many states depend on a handful of exporters, from the Black Sea to North America, Brazil and Southeast Asia.

Computer vision changes the margin.

A drone that can count plants, detect disease, map water stress and guide fertilizer use gives small and medium farms something once reserved for industrial agribusiness: field intelligence. That can raise yields, cut waste, reduce pesticide and fertilizer dependency, and make local production less blind.

The geopolitical result is not autarky. It is selective de-risking.

Countries with enough land, water and labor can use AI agriculture to close part of the productivity gap. Importers may still buy wheat, rice or soy, but they become less exposed to shipping chokepoints, export bans, currency shocks and fertilizer bottlenecks.

The new dependency moves upstream: drones, sensors, chips, cloud models, batteries, satellite data and agronomic software.

Food power will not disappear. It will migrate from grain elevators to data layers.

Will the next agricultural superpower be the country with the most land — or the one that turns every hectare into a measured system?

Space will not be colonized by rockets alone.

It will be colonized by enforceable claims.

The old empire cycle is repeating above Earth: first exploration, then logistics, then law, then capital. The American West did not become an economy because wagons existed. It became one because land, railroads and risk could be priced.

Geography still rules. The Moon’s south pole is not romantic terrain; it is a future chokepoint because water ice can become oxygen, fuel and life support. Asteroids are not treasure chests unless someone can extract, transport, insure and sell the material under a recognized legal regime.

This is why space law matters for geopolitics. The 1967 Outer Space Treaty blocks national sovereignty claims. The 1979 Moon Agreement pushes toward “common heritage.” The US-led Artemis Accords try to normalize resource extraction without formal colonization. China’s ILRS offers a competing institutional gravity well.

The technology stack is already moving: reusable rockets, lunar landers, robotics, solar power, autonomous mining, comms, AI navigation and semiconductor-heavy control systems. But capital will not scale into a legal fog.

The next space race is not only NASA vs CNSA or SpaceX vs state programs.

It is a race to define which rules turn geography into property, property into investment, and investment into power.

Who writes those rules first?

The Vatican is not afraid of artificial intelligence because it is new.

It is afraid because it looks old.

Every empire created a sacred technology of order: roads for Rome, fleets for Britain, nuclear weapons for the United States, bureaucracy for modern states. AI may become the next one: a system that predicts, ranks, disciplines, rewards and excludes at civilizational scale.

Pope Leo XIV’s call to “disarm” AI is not really about banning chatbots. It is about power. Who owns the models? Who controls the chips? Who governs the data centers, cloud platforms, cables, energy grids and military systems beneath the friendly interface?

Geography still decides the game. AI is not floating in the cloud. It sits in Taiwan’s semiconductor chain, America’s hyperscale data centers, Gulf energy capital, European regulation, Chinese industrial policy and undersea cables crossing maritime chokepoints.

This is why the Church sees the danger so clearly. It has spent centuries watching belief systems become institutions, institutions become empires, and empires become machines for obedience.

The real question is not whether AI becomes “religion.”

The question is whether it becomes priesthood: a small class interpreting reality through models nobody else can inspect.

Can humanity govern AI before AI becomes the governing layer of humanity?

@KemiBadenoch Russia’s weakness is not lack of resources.

It is that its empire must sell continental resources through maritime systems it does not fully control.

That is the strategic trap: land power funded by sea-dependent exports.

More here:

https://t.co/XKXs4kKNHx

Russia is not just fighting with tanks.

It is fighting with oil fields, pipelines, ports, ice, tankers, insurance contracts and discount barrels.

That is the old geography of Russian power.

From the Tsars to the Soviet Union to today’s Kremlin, Russia has tried to solve the same structural problem: it has enormous land, huge resources and strategic depth — but weak maritime access, long internal distances and a narrow export base.

Empire on land is expensive.

Empire funded by commodities is vulnerable.

In 2025, Russia’s federal oil and gas budget revenues fell by 24% to 8.48 trillion rubles, the lowest level since 2020. Oil and gas still remain one of the Kremlin’s key fiscal pillars, but the mechanism is no longer clean: Russian crude must move through discounts, longer routes, shadow fleets, non-Western buyers and higher transaction costs.

Sanctions did not “stop” Russian energy. That was never the real test.

The real test is whether sanctions turn Russia’s resource advantage into a logistics tax.

Every extra tanker, insurance workaround, rerouted shipment, lower price cap and damaged refinery converts geography into friction. A barrel still sold is not the same as a barrel sold cheaply, late, uninsured and through constrained ports.

This is where empire cycles matter. Spain had silver. Britain had coal and sea lanes. The Soviet Union had oil, gas and industrial depth. Resource empires look strong until their extraction system becomes harder to defend than their enemies need it to attack.

Russia’s question is no longer simply: can it export oil?

The harder question is: can a continental empire finance a long war when its main revenue artery increasingly depends on maritime loopholes it does not fully control?

@NAFOvoyager The real story is not whether Russian oil still moves.

It does.

The story is that every barrel now carries a logistics tax: longer routes, discounts, shadow tankers, insurance workarounds.

That is how sanctions turn geography into friction.

More here:

https://t.co/XKXs4kKNHx

Russia is not just fighting with tanks.

It is fighting with oil fields, pipelines, ports, ice, tankers, insurance contracts and discount barrels.

That is the old geography of Russian power.

From the Tsars to the Soviet Union to today’s Kremlin, Russia has tried to solve the same structural problem: it has enormous land, huge resources and strategic depth — but weak maritime access, long internal distances and a narrow export base.

Empire on land is expensive.

Empire funded by commodities is vulnerable.

In 2025, Russia’s federal oil and gas budget revenues fell by 24% to 8.48 trillion rubles, the lowest level since 2020. Oil and gas still remain one of the Kremlin’s key fiscal pillars, but the mechanism is no longer clean: Russian crude must move through discounts, longer routes, shadow fleets, non-Western buyers and higher transaction costs.

Sanctions did not “stop” Russian energy. That was never the real test.

The real test is whether sanctions turn Russia’s resource advantage into a logistics tax.

Every extra tanker, insurance workaround, rerouted shipment, lower price cap and damaged refinery converts geography into friction. A barrel still sold is not the same as a barrel sold cheaply, late, uninsured and through constrained ports.

This is where empire cycles matter. Spain had silver. Britain had coal and sea lanes. The Soviet Union had oil, gas and industrial depth. Resource empires look strong until their extraction system becomes harder to defend than their enemies need it to attack.

Russia’s question is no longer simply: can it export oil?

The harder question is: can a continental empire finance a long war when its main revenue artery increasingly depends on maritime loopholes it does not fully control?

Russia is not just fighting with tanks.

It is fighting with oil fields, pipelines, ports, ice, tankers, insurance contracts and discount barrels.

That is the old geography of Russian power.

From the Tsars to the Soviet Union to today’s Kremlin, Russia has tried to solve the same structural problem: it has enormous land, huge resources and strategic depth — but weak maritime access, long internal distances and a narrow export base.

Empire on land is expensive.

Empire funded by commodities is vulnerable.

In 2025, Russia’s federal oil and gas budget revenues fell by 24% to 8.48 trillion rubles, the lowest level since 2020. Oil and gas still remain one of the Kremlin’s key fiscal pillars, but the mechanism is no longer clean: Russian crude must move through discounts, longer routes, shadow fleets, non-Western buyers and higher transaction costs.

Sanctions did not “stop” Russian energy. That was never the real test.

The real test is whether sanctions turn Russia’s resource advantage into a logistics tax.

Every extra tanker, insurance workaround, rerouted shipment, lower price cap and damaged refinery converts geography into friction. A barrel still sold is not the same as a barrel sold cheaply, late, uninsured and through constrained ports.

This is where empire cycles matter. Spain had silver. Britain had coal and sea lanes. The Soviet Union had oil, gas and industrial depth. Resource empires look strong until their extraction system becomes harder to defend than their enemies need it to attack.

Russia’s question is no longer simply: can it export oil?

The harder question is: can a continental empire finance a long war when its main revenue artery increasingly depends on maritime loopholes it does not fully control?

America’s greatest weapon was not the dollar, the aircraft carrier, or Silicon Valley.

It was the map.

The United States became the dominant power because geography made power unusually cheap. Two oceans protected it. The Mississippi basin connected it. The Great Lakes industrialized it. Vast farmland fed it. Shale and hydrocarbons powered it. Weak land borders freed it from the permanent security nightmare that shaped Europe, Russia, China, and the Middle East.

This is the Peter Zeihan logic: most empires must spend enormous energy overcoming geography. America was built on geography that reduced friction. Goods, grain, coal, oil, steel, people, and capital could move across one continental market before the U.S. even needed to dominate the world’s sea lanes.

Britain had maritime reach, but limited continental depth. Russia has depth, but poor warm-water access. China has scale, but depends on imported energy and exposed maritime routes. The U.S. combined food security, energy, navigable rivers, ports on two oceans, strategic depth, and later the world’s largest blue-water navy.

That old geographic advantage now shapes the technology race. Cheap energy, inland logistics, LNG exports, aerospace corridors, chip fabs, AI data centers, cloud infrastructure, and defense production all sit on the same continental platform.

The uncomfortable question is not whether America has the best geography.

It is whether its institutions are still good enough to use it.

America is not retreating from the world – it is retreating from the impossible role of sole global policeman.

Is geography reasserting itself on the high seas?

What’s your take?

The Mongol Empire – history largest empire – collapsed when its supply lines failed. Geography and overextension proved stronger than military genius

The US long guaranteed safe global sea lanes and supply chains. In today’s multipolar world it can no longer control every ocean.